Pork Wrap June 24

Things continued on an upward trajectory this week in the hog and pork

complex as the negotiated hog markets averaged about $2.50/cwt

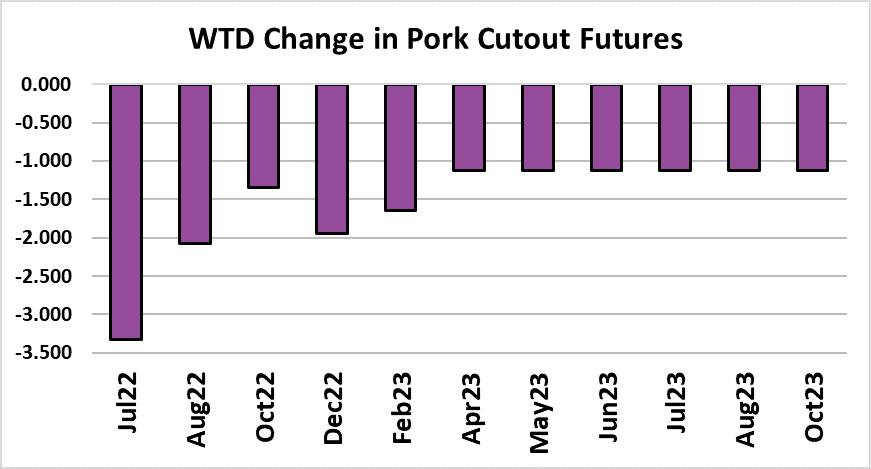

higher and the cutout managed to eeek out a $0.80 gain. The notable

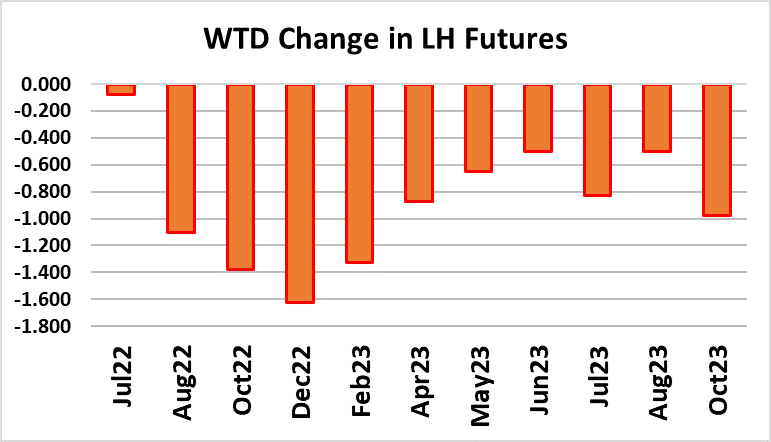

event of the week was a sharp drop in the futures on Thursday without

any significant change in the fundamentals. The Jul contract lost $3.30

on Thursday and the Aug contract finished $4.65 lower as the hog

market got caught up in a big sell-off across most of the commodity

markets. Traders soon realized the error of their ways and the market

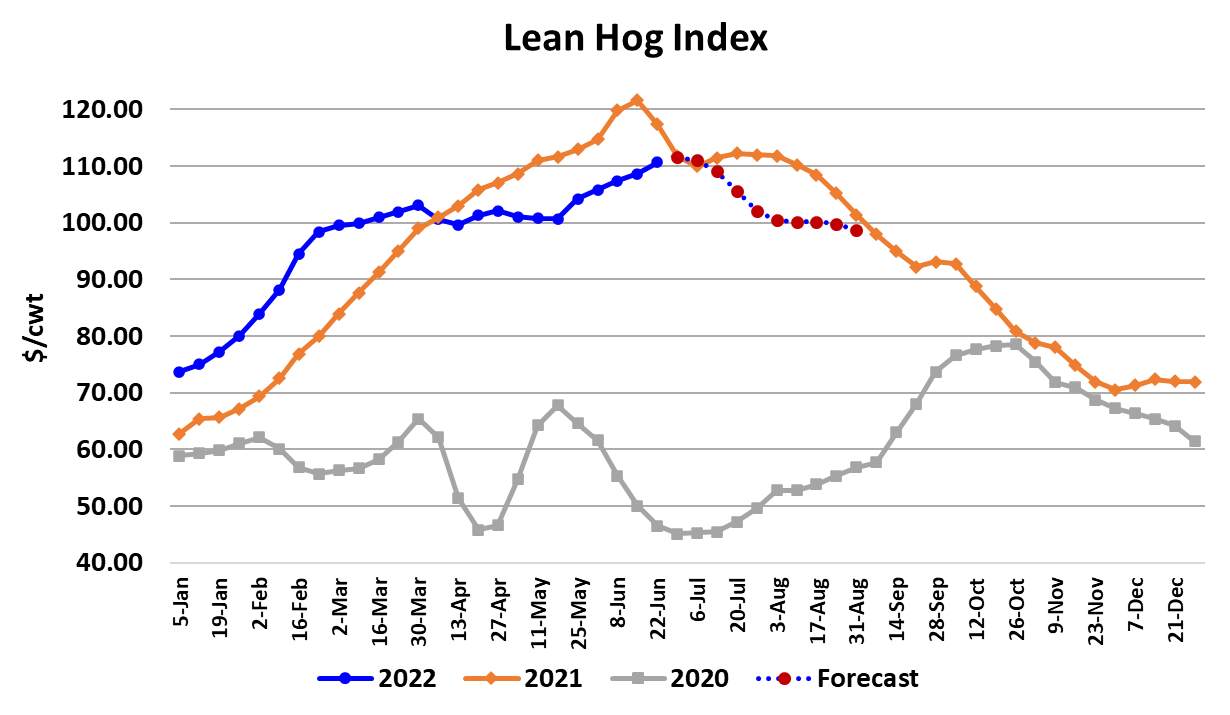

bounced back sharply on Friday. The LHI currently sits at $110.90

with three weeks until expiration. Prior to Thursday’s sell-off, the Jul

futures had been carrying a small premium to the LHI, but now the

futures are almost dead on the index. The bears seem to be getting a

little nervous, and with good cause, as the industry will soon be moving

into the smallest kills of the year. The July 4 holiday, because it falls on

a Monday, will result in a very small Saturday kill next week. Then

comes the actual holiday week itself when the Monday harvest will be

zero.

By the time those two short production weeks are behind us, the Jul

contract will only be a few days from expiration. My thought has been

that the cutout will hold steady over $110 over the next couple of weeks

and then decline as production ramps back up following the holiday

week. I have fair value for the Jul contract currently pegged at $109,

but I could be too low on that. Pork demand seems to be holding up

fairly well as we head toward July. The combined margin is still moving

higher, but this week’s gain was very small. A lot will depend on how

well buyers are prepared for the upcoming holiday. If they haven’t

sourced enough product and have to scramble to procure more then

that would show up as further demand strength. If they are adequately

bought, they might not need to bid up the pork market and thus we

could see demand plateau or turn lower. In either case, the combined

margin sure looks like it is set to make a top soon. Whether that comes

before or after July 4 remains to be seen. USDA did provide a cold

storage update this week that showed total pork in cold storage up 17%

YOY.

Cold storage stocks are not yet back to pre-pandemic levels, but they

are headed in that direction. Bigger stocks give buyers an alternative

to the spot market when cash prices get high and thus they tend to

have a price-depressing effect. Now that a lot of the uncertainties

surrounding the pandemic have faded, pork users seem to be more

confident in holding larger inventories in cold storage. Once again, it

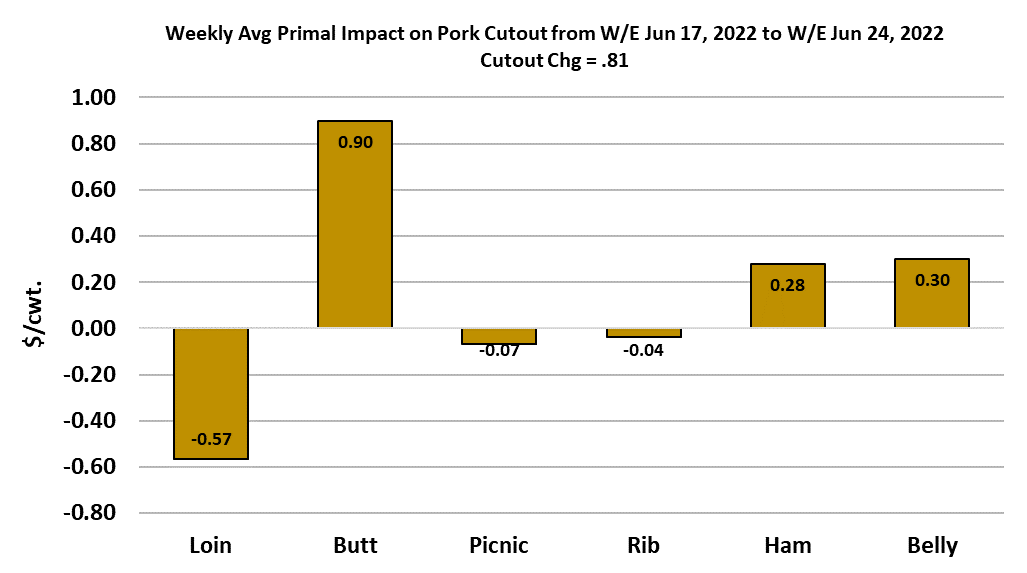

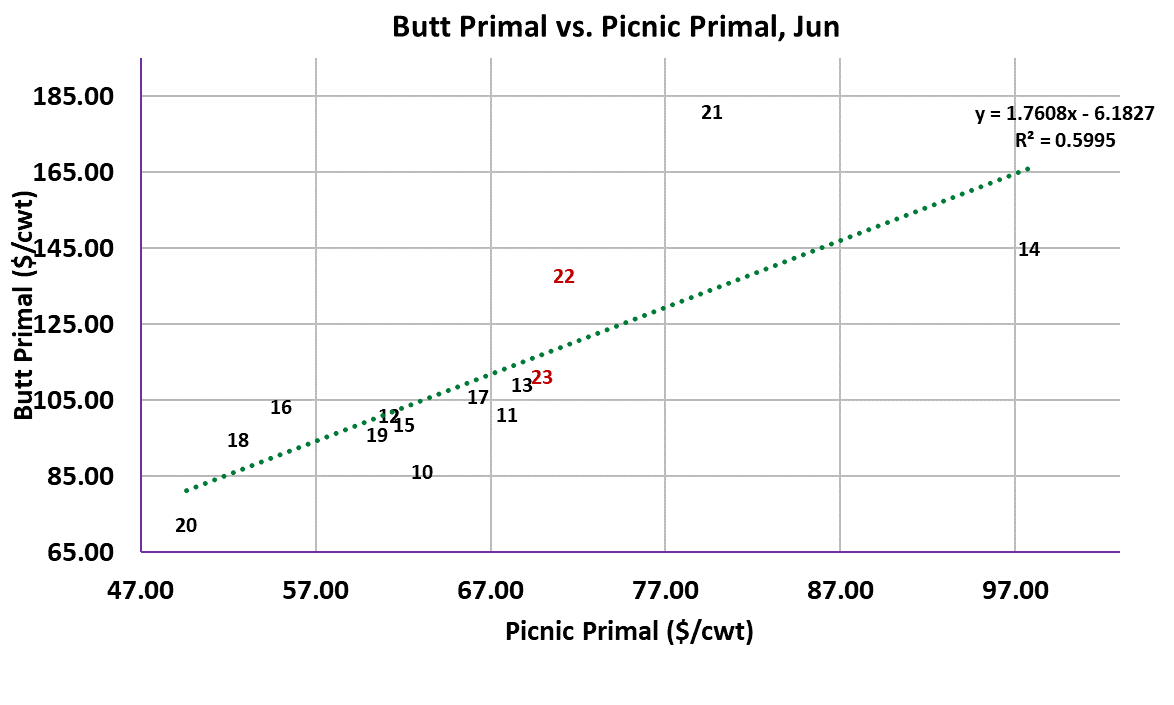

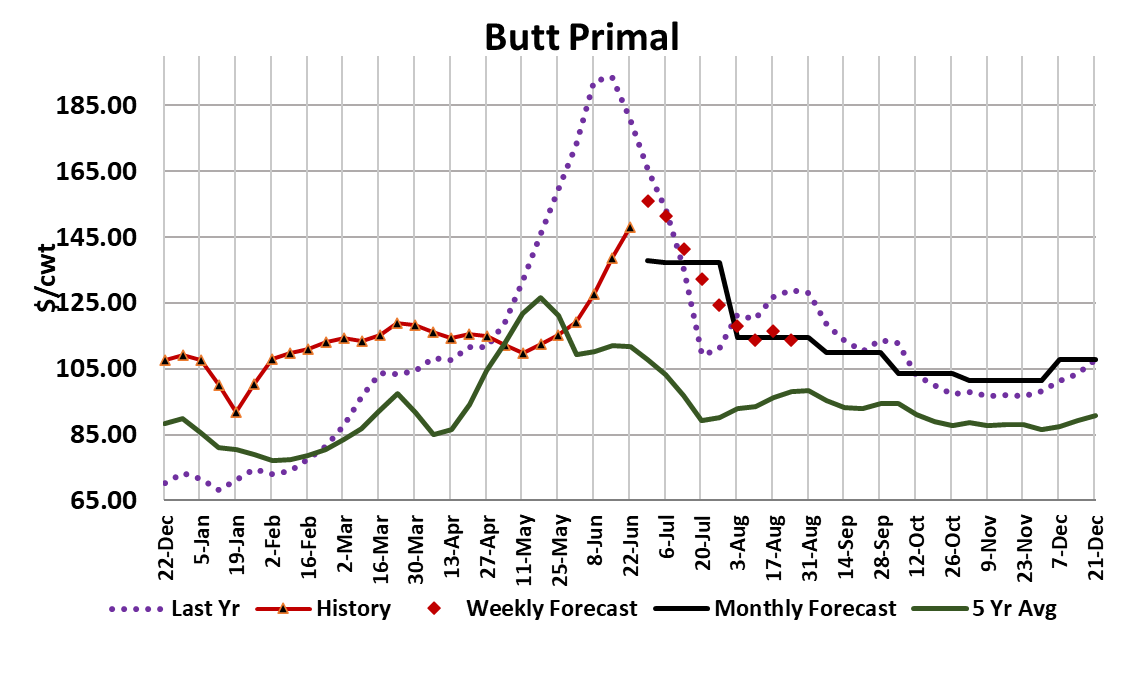

was the butts that provided most of the lift to the cutout. I haven’t found

a satisfactory explanation for why the butts are so strong right now, but

the attached scatter between the butt primal and its close cousin, the

picnic, indicates that butts are indeed extra strong this June, but not

nearly to the degree that they were last year. Hams and bellies also

provided some modest support this week and we saw the 23/27 hams

trade over $100 for a while.The bellies have been creeping slowly higher on a weekly average basis,

but the averaging process helps mask some big price swings on a daily

basis. I see both hams and bellies keeping firm pricing over the next week

or two as production will be light. After that, both could be vulnerable to a

downturn. This week’s kill clocked in at 2.3 million head, which is about 2%

below last year. Next week’s kill should be even smaller, perhaps around

2.28 million head and then for the holiday week I’m expecting the kill to drop

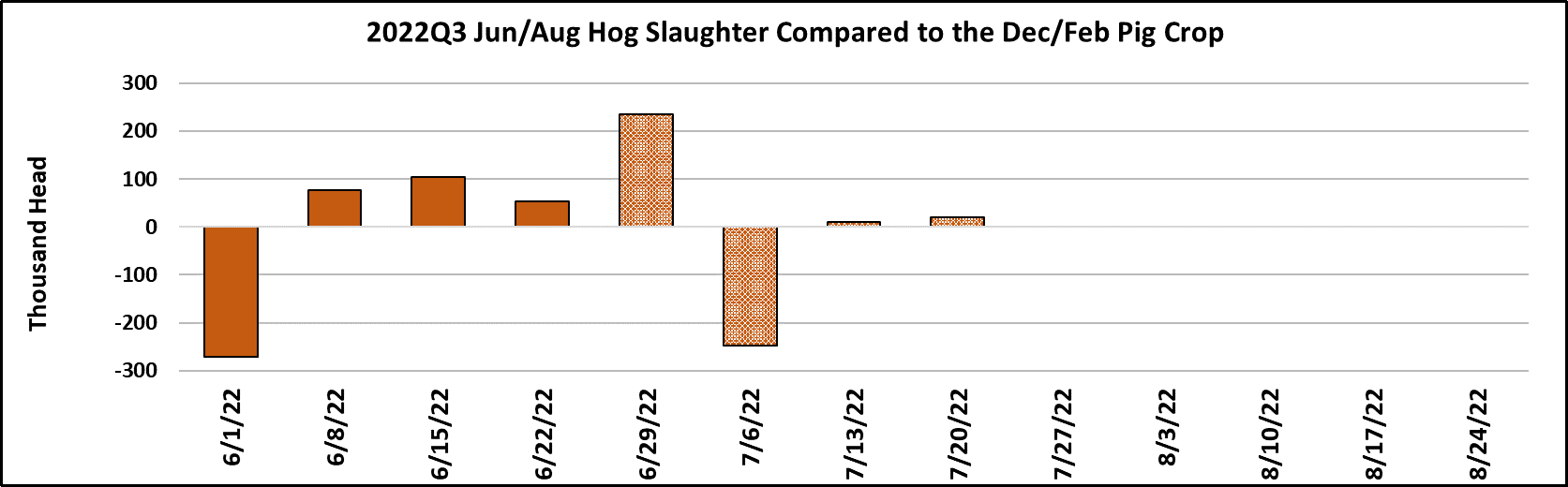

to 2.05 million head. This week’s slaughter was just a bit larger than what

the pig crop suggested, but if we look at the first four weeks of the quarter

taken together, the deviation from the pig crop is almost zero. So it looks

like USDA may have nailed this pig crop right on the head and thus I can be

pretty confident about forecasted slaughter levels in July and August. After

the week of July 4, kills should start to slowly expand and by the first week of

August, they could be back up to 2.4 million head per week. By the end of

August, we might see 2.5 million head per week.

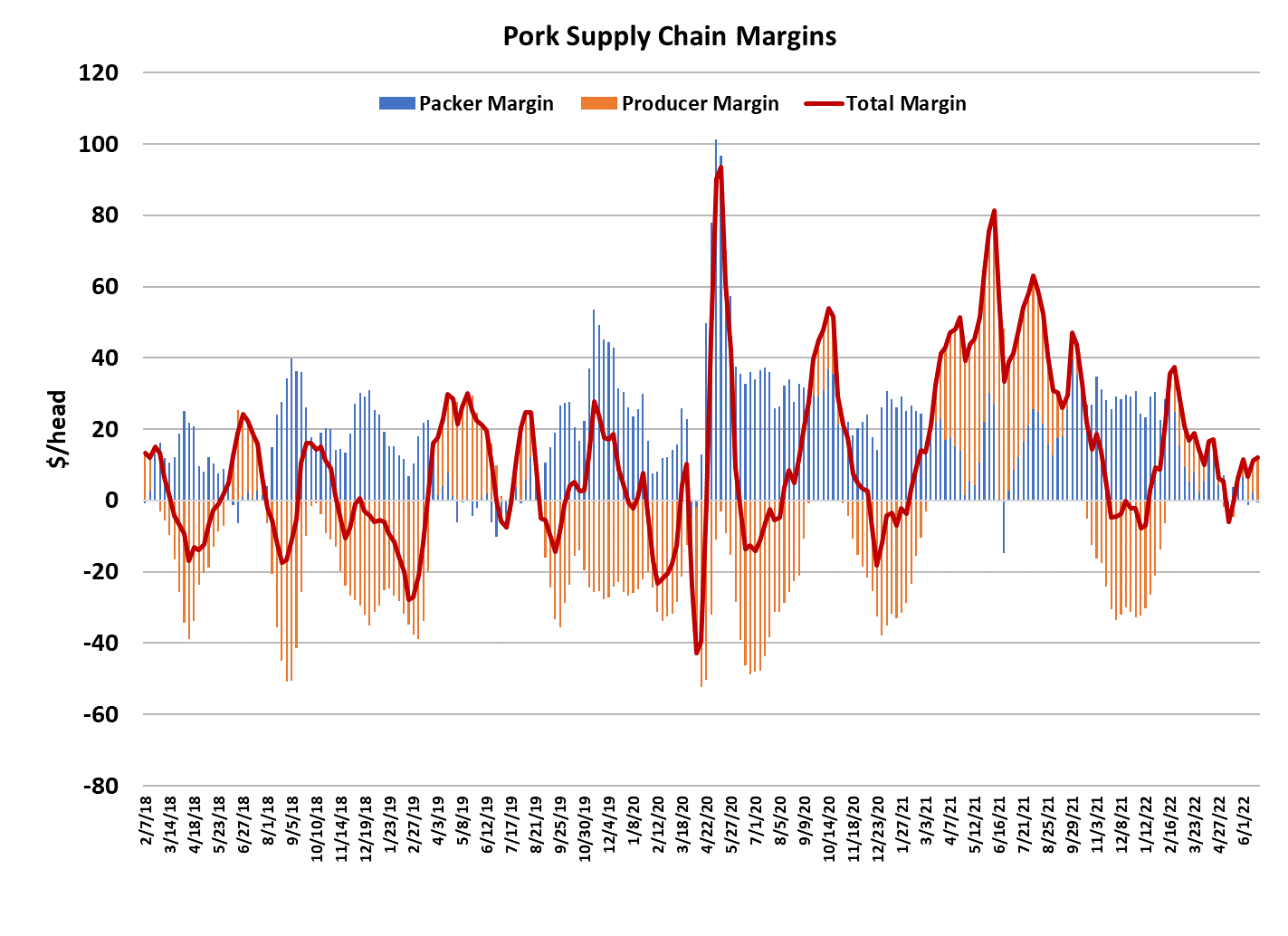

Of course now that we are right on the verge of the smallest kills of the year,

packer margins are under pressure as they are forced to compete

more aggressively for what few hogs might be available to fill out

their kill schedules. Packers have bid up hog prices to the point where

negotiated prices are only a couple of dollars below last year’s strong

showing in the low $120s. I calculate this week’s packer margin at -$0.60/

head and expect that it will get more negative next week. Look for packer

margins to remain close to, or just below zero through July. By

August, they should be expanding again and could average around

$5-7/head. Hog weights continue to behave normally, declining

seasonally as expected. The heat dome that had been forecast to appear

over the Midwest never materialized and so that has helped to mitigate the

near-term supply side risk. We should remain vigilant about the weather

however because summer is still young and there will be plenty more

opportunities for a heat wave to cause rapid weight loss in market hogs.

USDA will release the next issue of its Hogs and Pigs report on

Wednesday and I’m looking for it to show a steady to slightly smaller hog

herd compared to what they reported back in March. There is not much

financial incentive for producers to expand in this high cost environment

and I’d say that if there is a surprise in next week’s report it may be that hog

numbers are smaller than the pre-report estimate. We all know how much

futures traders love a bullish Hogs and Pigs report. The other area

where a potential surprise could develop is in the belly market. Last year

around this time the bellies crashed hard, taking the cutout, and

eventually cash hogs, down. I think the probability of that happening this

year is much lower, mostly because belly prices are not elevated nearly

to the degree that they were last year. Volumes moving into export have

been pretty steady over the past couple of months, but they are still

below last year’s level. At current pork prices, it is hard to imagine that

exports will provide any surprises in the near-term. Next week, watch the

weather in the Midwest and keep an eye on butt prices because if they start

to break it will likely pressure the cutout lower

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}