Pork Wrap June 21

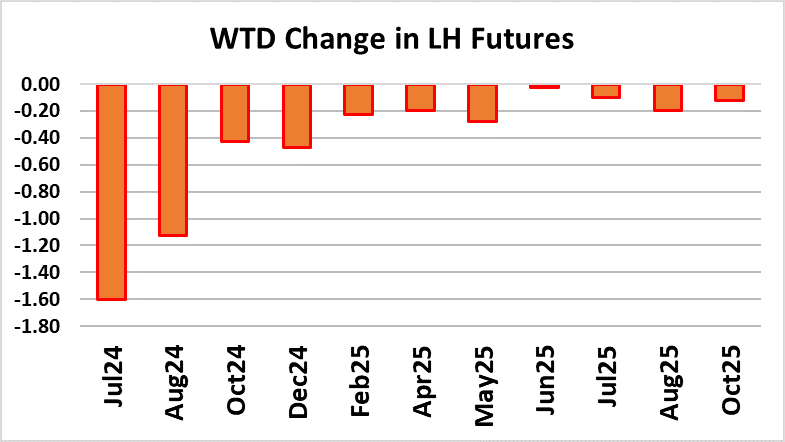

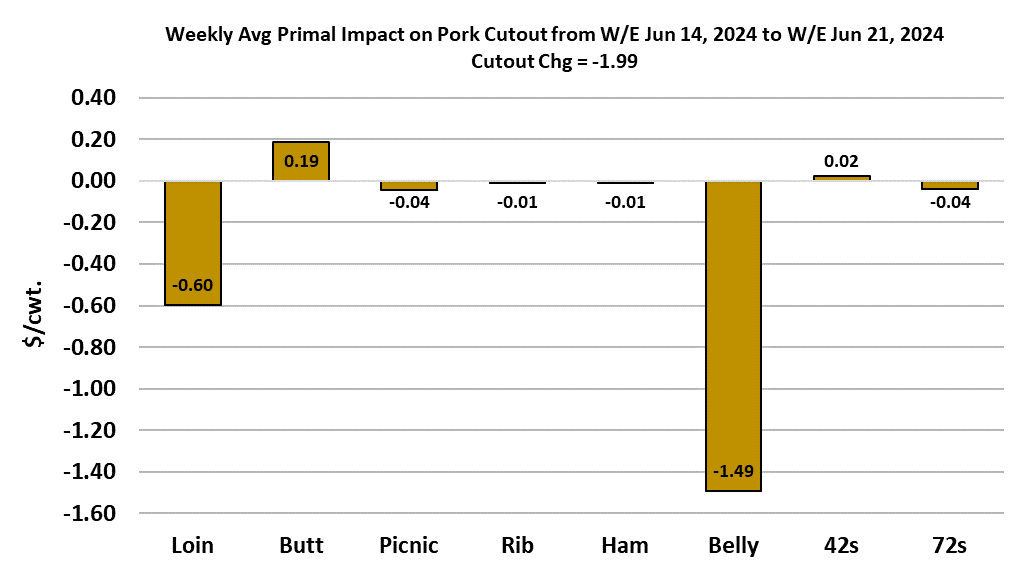

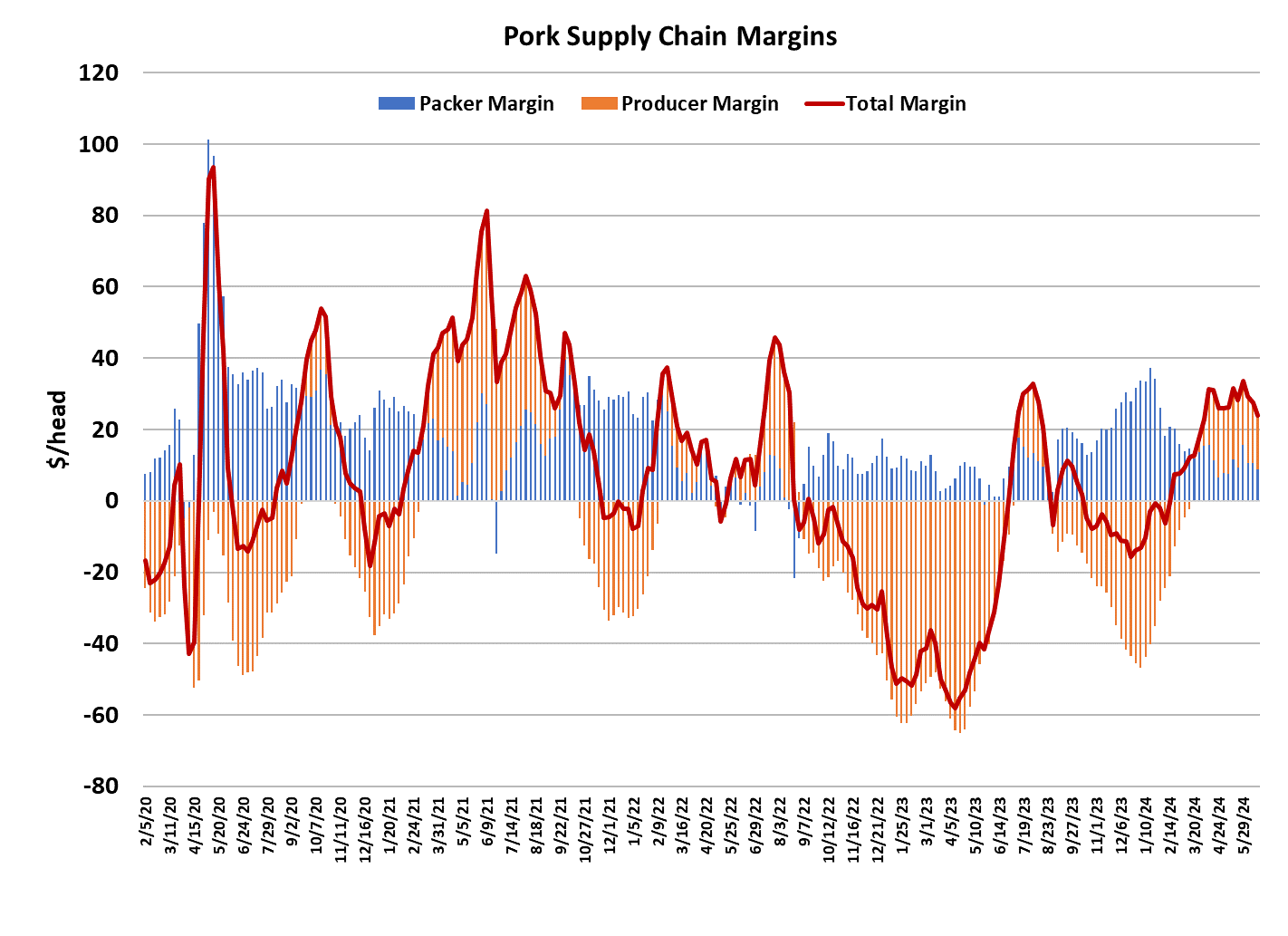

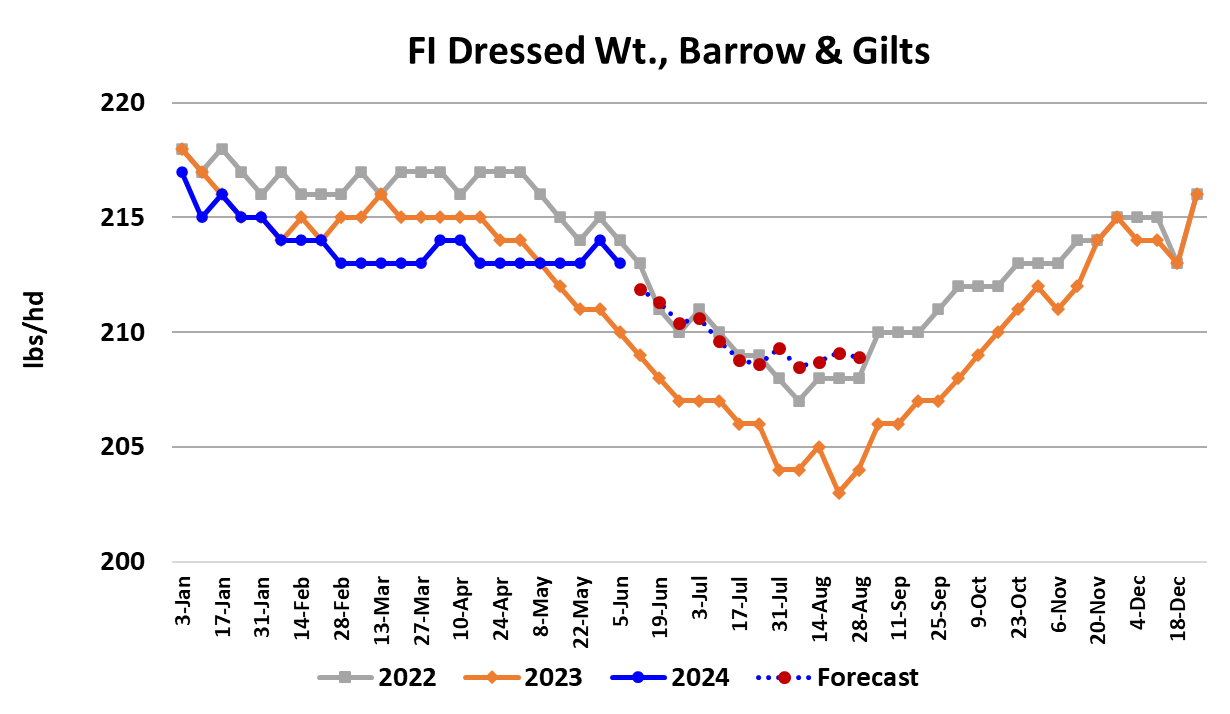

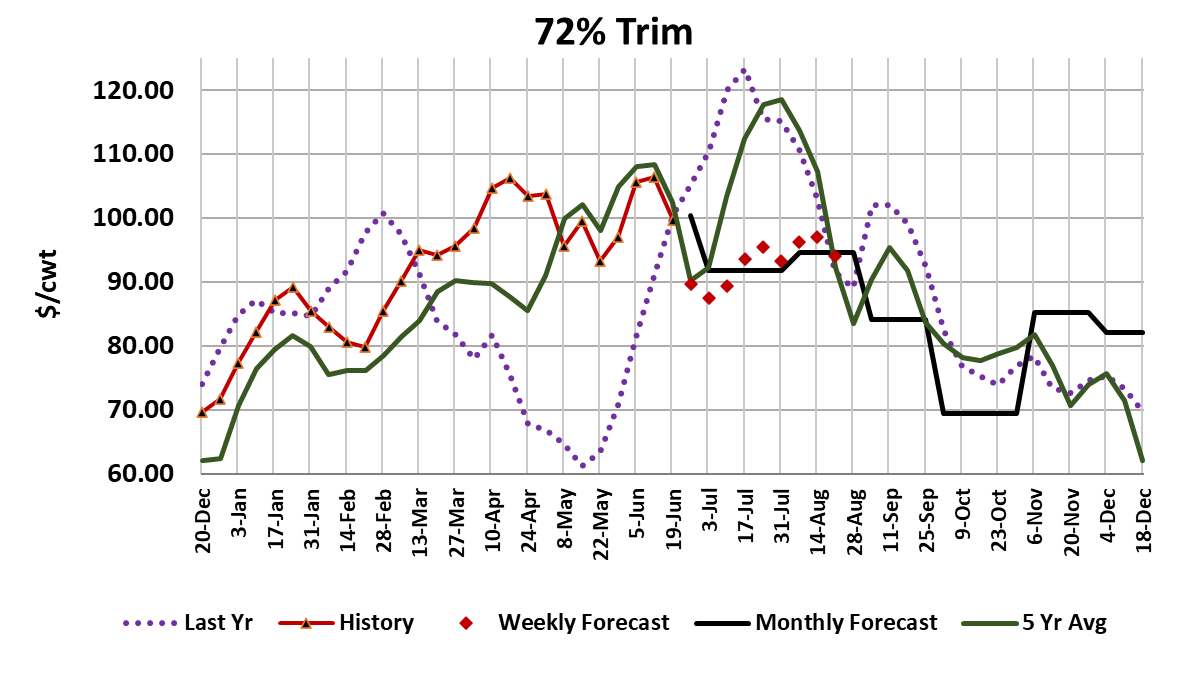

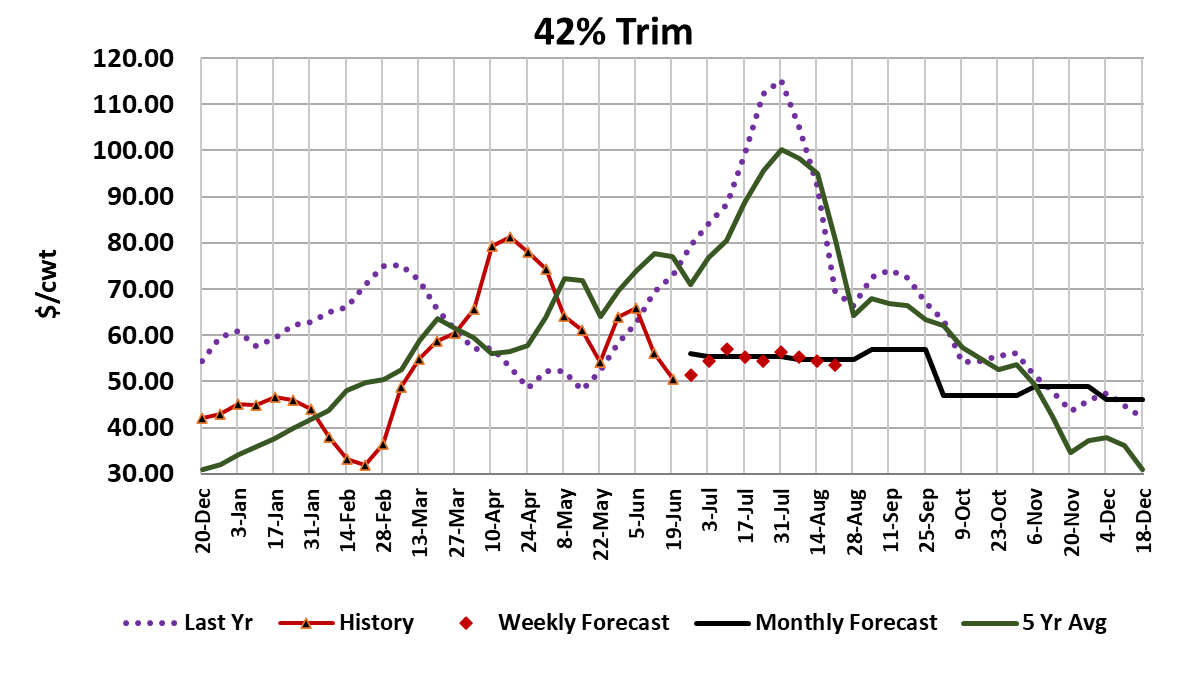

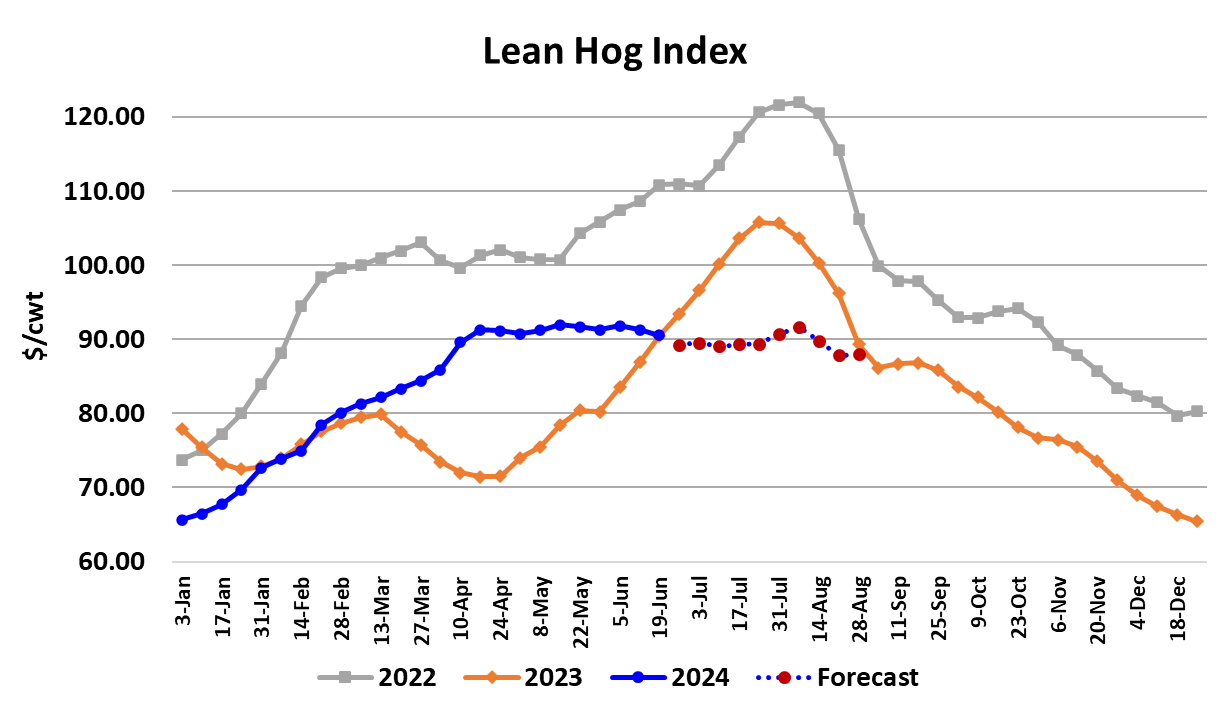

The pork cutout went on the defensive this week as price weakness in the bellies and loins helped the cutout lose $1.99 on a weekly average basis in moving to $98.30. Cash hog markets were mostly steady as the WCB negotiated price lost only $0.20/cwt. on its way to averaging $87.54. That caused packer margins to compress down to $7.75/head, about $3 lower than the week before. It is clear now that pork demand is struggling and when we pair that up with hog supplies that seem to be more than ample for this time of year, it has mostly erased the chances of a summer price rally and we might even be looking at a declining price environment through the remainder of the summer and into fall. I am certainly concerned about the apparent inability of belly prices to advance, but even more concerning is the softness that was seen in some of the retail items this week. Loins, in particular, saw significant price weakness at times this week and that prompted me to lower the price forecasts for retail items through the balance of summer. Just judging by the calendar, it is time for the hams to turn higher, but I’m concerned that they might continue to struggle. Ham movement into Mexico looks a bit subdued based on the weekly FAS sales/shipments and the peso has lost value relative to the dollar, making US hams more expensive for Mexican buyers. So, if hams do gain a little seasonal lift in the next few weeks, I wouldn’t expect the price gains to be very large. Next week provides some demand risk as processors will likely curtail their raw material orders because the following week will be shorted by the Independence Day holiday. That might make it difficult to get much lift on items such as hams, bellies and trims. Speaking of trims, both the 42s and 72s moved lower this week and the 72s had a particularly nasty print on Friday at 88 cents after trading at $1.14 on Monday. If the 72s are in trouble, that doesn’t bode well for the hams or even the cutout. We will need to keep a close eye on that. It really doesn’t look like the demand side of the market is going to be much help over the next few weeks, so how about the supply side? Well, next week could very well mark the lowest non-holiday weekly kill of 2024, but it probably won’t be much lower than this week’s level, which was pegged at 2.42 million head. My estimate has next week somewhere close to 2.38 million head. After that comes the week containing July 4, and there we could see the weekly kill drop to 2.1 million head. After that however, the pig crop points to a steady diet of 2.4 million head kills until late July when they should start creeping higher. By the time Labor Day approaches kills might be back near 2.6 million head per week, so the window of opportunity for a price rally driven by tighter supplies is pretty narrow. The heat wave that had been forecast for the Midwest seems to have shifted more to the Eastern part of the country and probably will not affect hog weights as much as initially anticipated. It is possible that the shift eastward will make the heat event a negative for pork prices because it could depress consumption in the population centers along the East Coast, rather than decreasing hog performance in the Midwest. FI barrow and gilt weights did tick down this week, but all that really did was move weights back to the 213-pound level where they have been stuck since late February (see chart). The forecast has weights working lower over the next couple of months, but remaining 2-3 pounds stronger than last year. So, neither of the important supply side variables, carcass weights or hog numbers, look particularly bullish here in late June. And we’ve already said that the demand side doesn’t hold a lot of promise over the near term, so upside price potential from here is limited. I reflected that in this week’s price forecast revisions and now the fundamental forecast has the cutout remaining below $100 for the balance of summer. Next Thursday, USDA will provide the results of their quarterly Hogs & Pigs survey and I expect that it will show a slight YOY increase in total swine inventories even though the breeding herd is expected to be reported down 3-4% from last year’s level. That is the result of soaring productivity as producers have been able to make more baby pigs with less sows over the past few quarters. If my estimates are close to what the survey reveals, I don’t think futures traders will view that very positively. Traders already seem to be struggling with how to price the nearby July contract, which traded near $96 early this week but settled close to $92 on Friday. The current fundamental forecast has the LHI at expiration near $89, and if that happens, we will have the July contract expire below the April contract. It is an odd year indeed. Next week, look for the cutout to print a dollar or two lower and this time the cash hog market could follow the cutout down.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}