Pork Wrap June 2

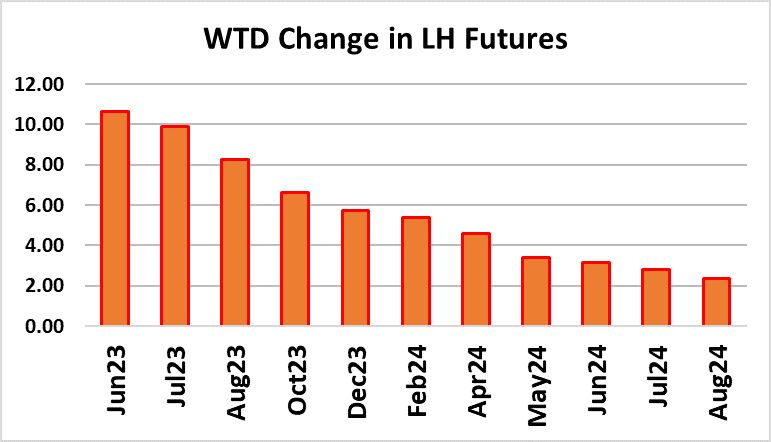

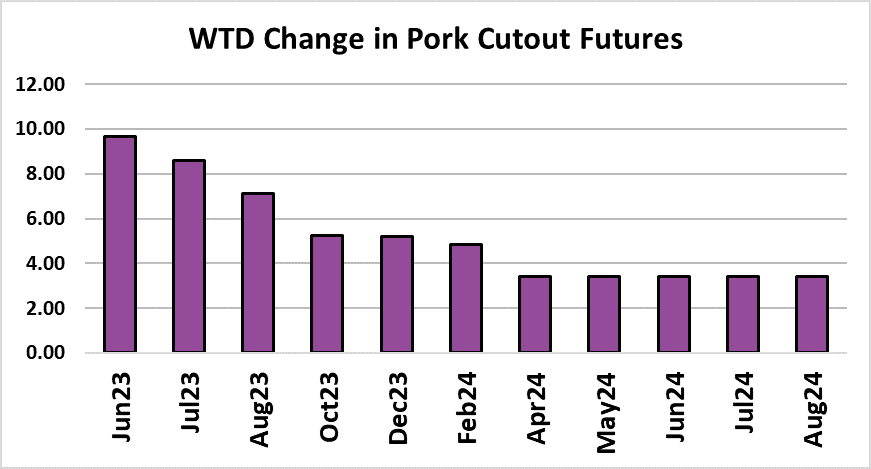

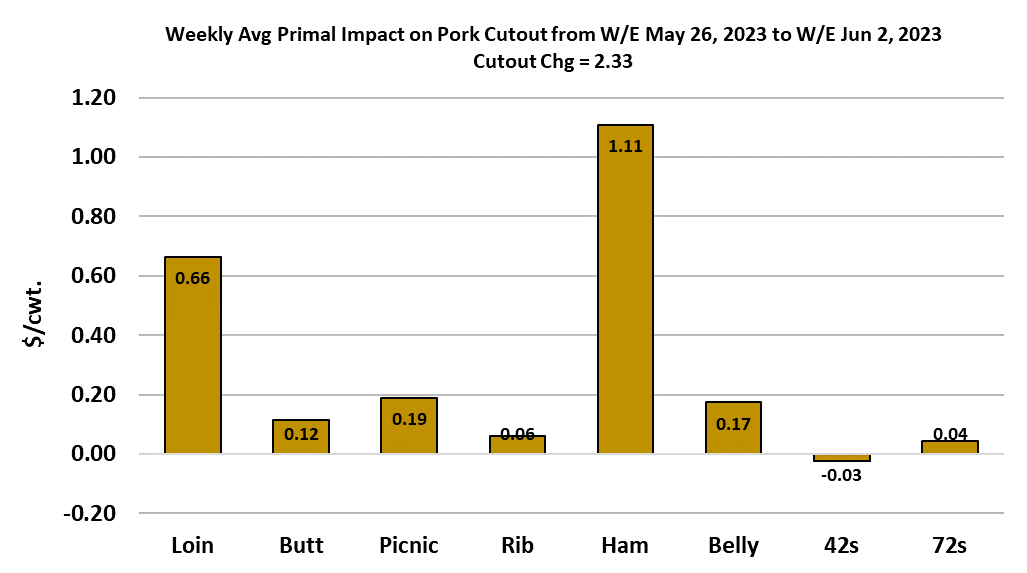

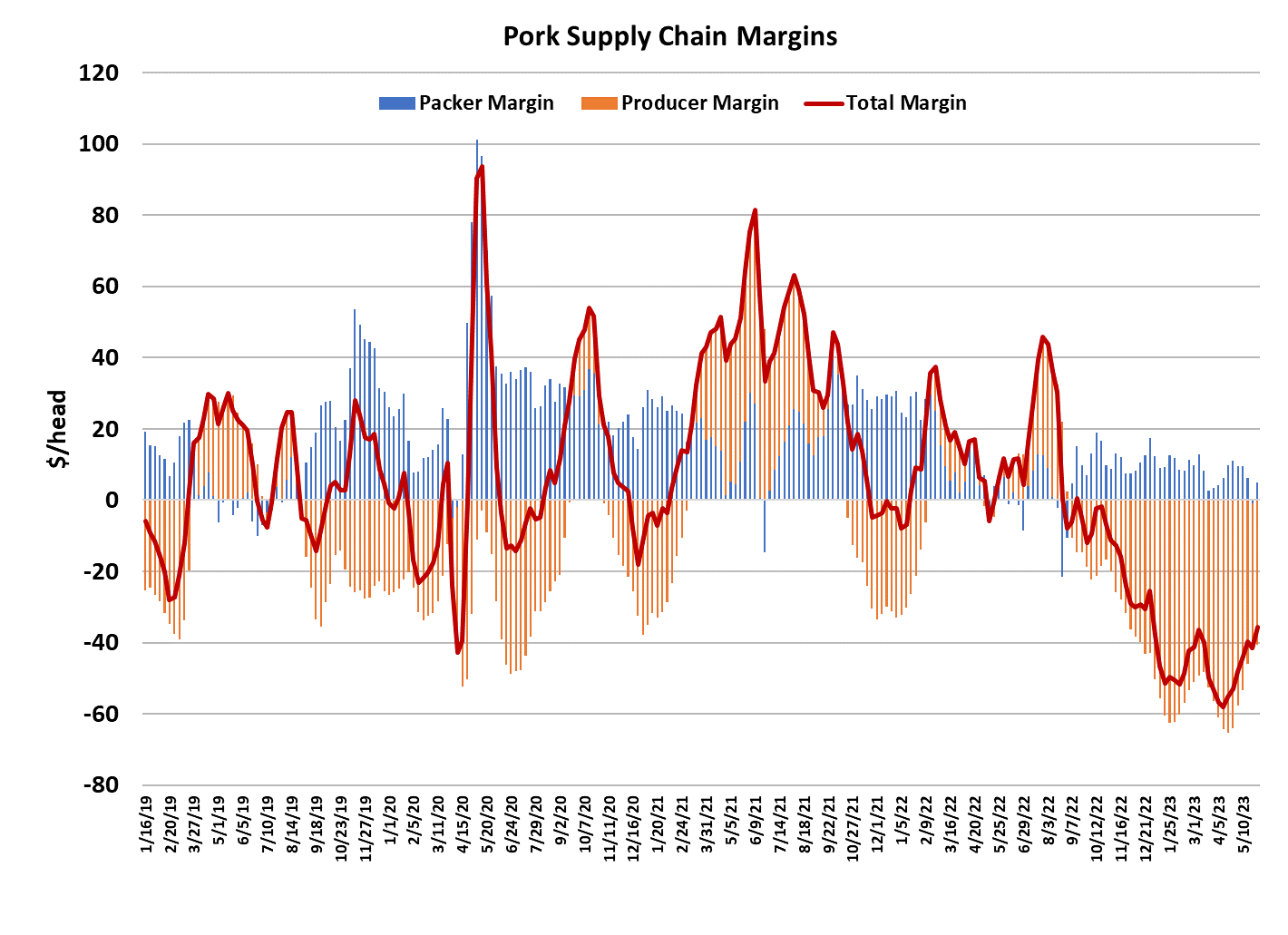

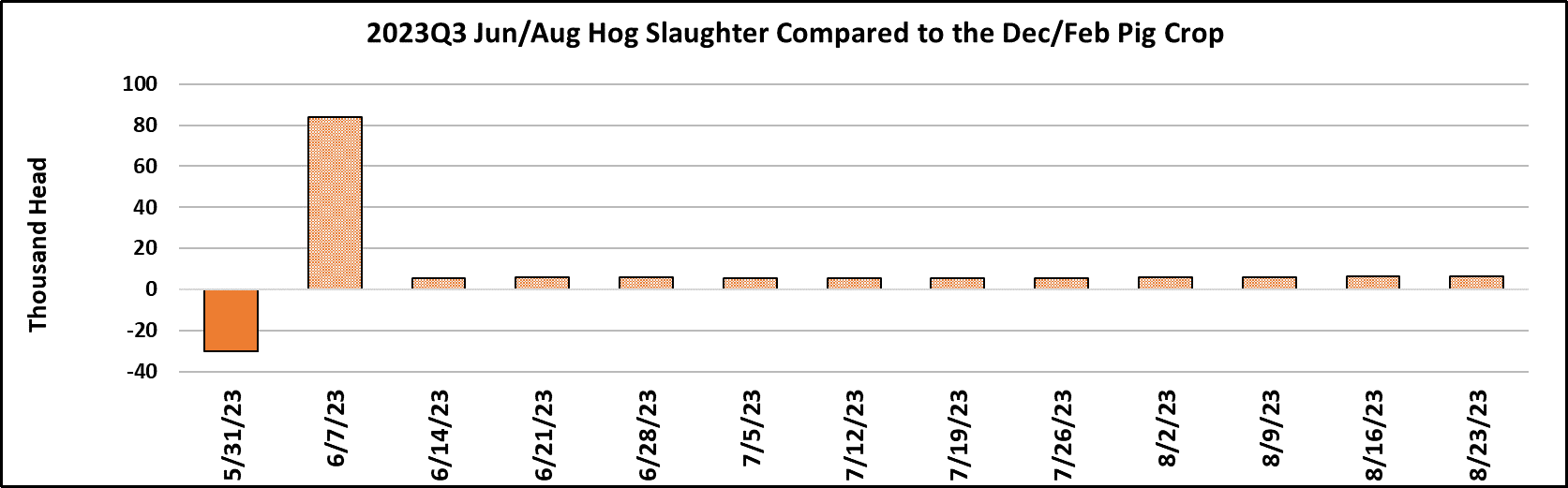

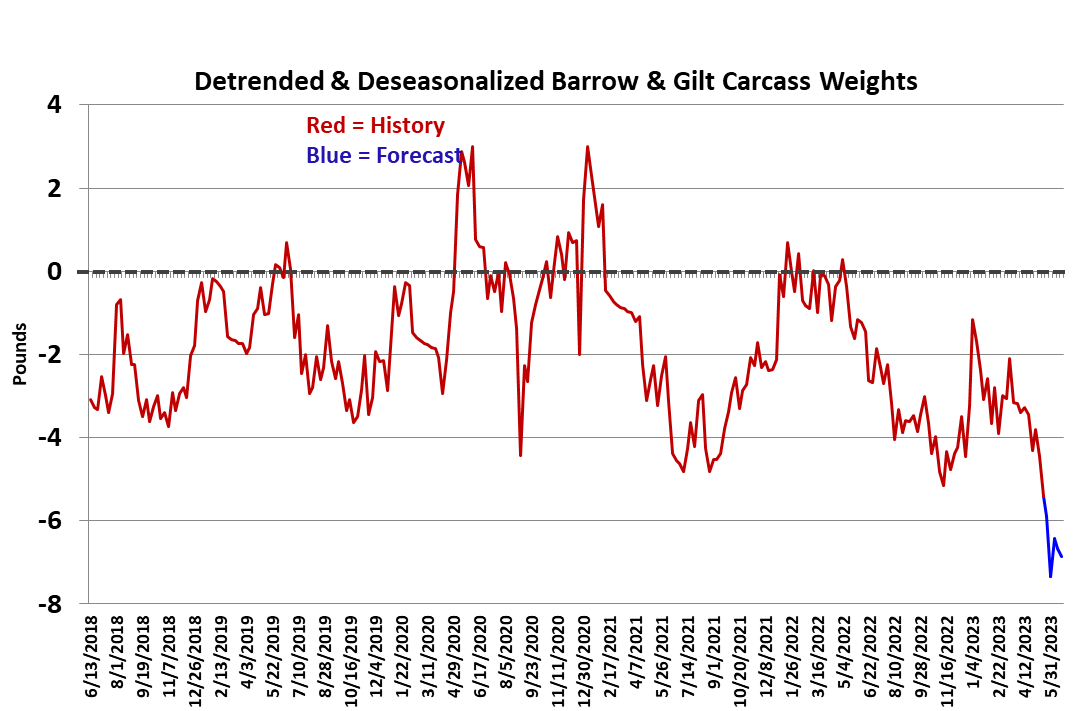

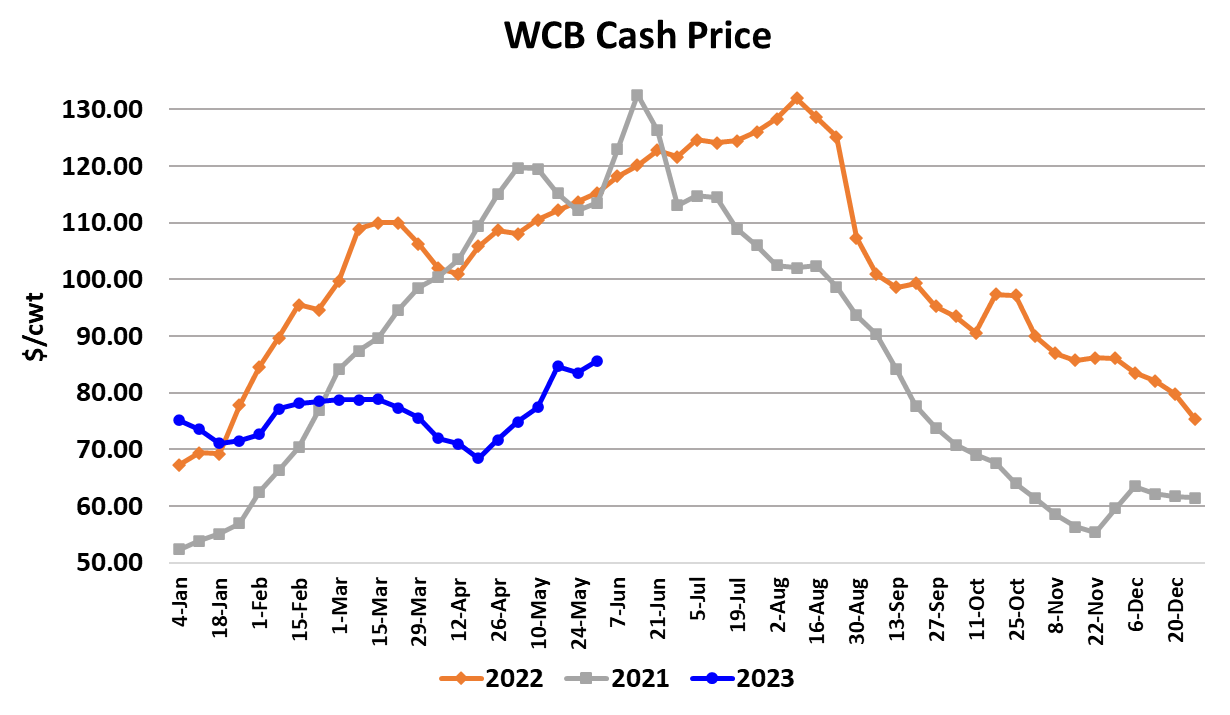

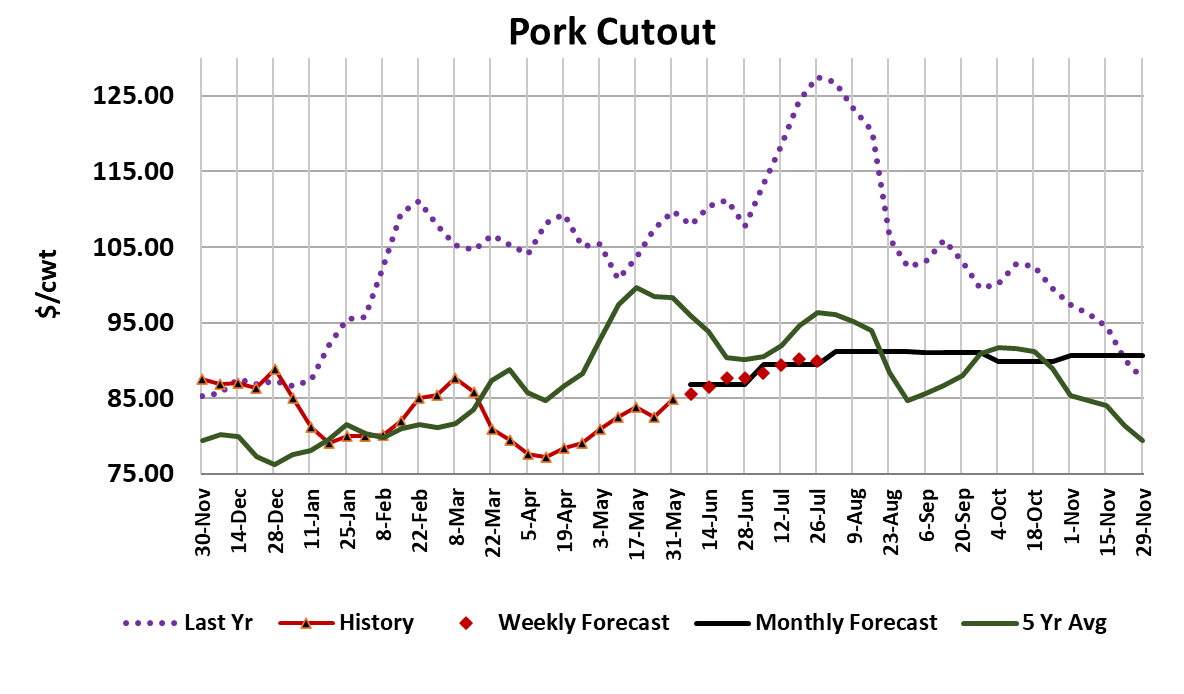

This week’s holiday reduced kill helped packers add $2.33/cwt to the pork cutout on a weekly average basis. At the same time, they paid close to $3/cwt more for cash hogs in the negotiated market. Price gains in early June should not be a surprise to anyone and the holiday-shortened kill helped to make that happen. I’m actually surprised at how orderly and predictable the hog and pork complex has been, especially compared to the volatility in the cattle and beef complex. This week’s kill clocked in at 2.03 million head and packers killed 119k on Saturday, so they are well on their way to replenishing the pipeline. I think next week’s kill could possibly challenge 2.4 million head again and that makes me think that the cutout isn’t going to run sharply higher. Cash hogs, on the other hand, could see some bigger gains next week. My sense is that the hog supply is tightening up a little more than seasonal and packers will need to pay up if they want to run a full schedule this week. Packer margins this week were close to $5/head, which is pretty good for this time of year. However, next week those margins should shrink down close to $0 as this week’s gains in hog prices become fully incorporated into the LHI. For the next couple of months, I’d look for packer margins to be just a few dollars either side of zero. Barrow and gilt carcass weights were down another pound this week, in typical seasonal fashion. Weights are now three pounds below last year. It seems as though producers have done a good job moving hogs out of the door recently and the de-seasonalized and de-trended carcass weights tend to confirm that. Those weights are now approaching -6 pounds (chart attached) and forecast to go even lower. That is easily the lowest they have been in the past five years. We have seen some powerful price rallies in recent years, but most of those have been demand driven. This year, if there is to be a strong rally, it will likely have to originate from the supply side. We are starting a new quarter, and this was the first week where part of the Dec/Feb pig crop went to slaughter. That pig crop was estimated to be up 0.3%, but I think that will be mostly offset by lower carcass weights and thus pork production over the summer could be flat with, or perhaps a little below last year. This week’s kill actually registered a little below what the pig crop implied, but that could just be an artifact of the holiday and perhaps next week the industry may overkill the pig crop once again. This week’s increase in the cutout was led by a rebound in ham pricing. The 23/27 lb hams added close to $5/cwt on the week. That was badly needed, as up until this week, the hams had been a big drag on the cutout. Bellies firmed a tiny bit but are still at very low levels historically. The retail primals all posted modest gains and the trims were higher too. So, this market is very well behaved and moving according to expectations. What isn’t well-behaved is the futures market, where the Jun contract added over $10 this week and finished within spitting distance of $87/cwt. Given that the LHI is currently at $81ish and there are 8 trading days left to go, getting to $87 is a tall task. Sure, the index has climbed that fast before, but that usually happens in a red-hot demand environment, and it is pretty clear that doesn’t describe the pork market in 2023. Demand for hogs will probably pick up as packers compete for a smaller supply of available hogs, but I don’t think the index can post a $6 rally purely on the back of the hogs. It would need some significant help from the cutout as well. I am going to stay with the program and call the cutout up another $1 next week. Week after week, we’ve seen that is about all we can expect unless there is a short kill. The combined margin is still on an upward trajectory, so that provides some hope that perhaps the industry is on its way to putting this dismal demand period in the rearview mirror. I calculate this week’s producer margin at -$40/head and look for that to become more positive as we move deeper into June and hog prices rises. Breakevens, which are currently near $99/cwt., should slowly decline into the low $90s by the end of July. With the Aug contract trading near $82 today, that is telling producers not to expect any positive profits this summer. We got a little more clarity on Prop 12 this week. It appears that California will move forward with the July 2 start date on the program, but the state Dept. of Agriculture has indicated that it is fine for sellers to work through any non-compliant product they have in inventory, even if it is on hand after the start date. It also sounds like enforcement is not going to be a high priority initially, so that relieves some of the concern around pork shortages inside California and pork excesses in the other 49 states. However, after July 2, any pork sellers in California looking to restock inventory will need to purchase only compliant pork in order to do so. But the good thing is that there probably won’t be mass chaos on July 2. It will probably take a couple of months for the full impact to be felt in the markets and for analysts to determine just how important Prop 12 is to overall hog and pork pricing. Right now, the deferred contracts are acting as if its not a big deal, but that could change as we get deeper into the summer. Next week, look for further appreciation in the cash hog markets as packers fight just a little harder for shrinking supplies. Watch the hams and bellies also, since any meaningful gains in the cutout will hinge on what happens in those markets.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}