Pork Wrap June 17

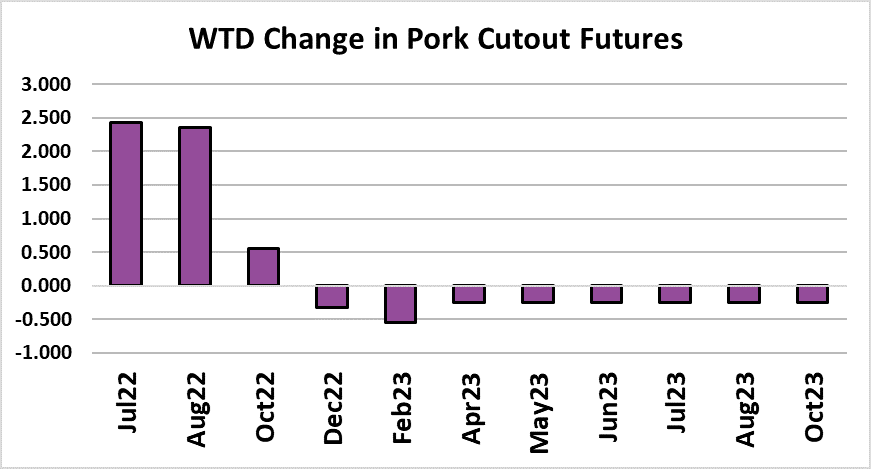

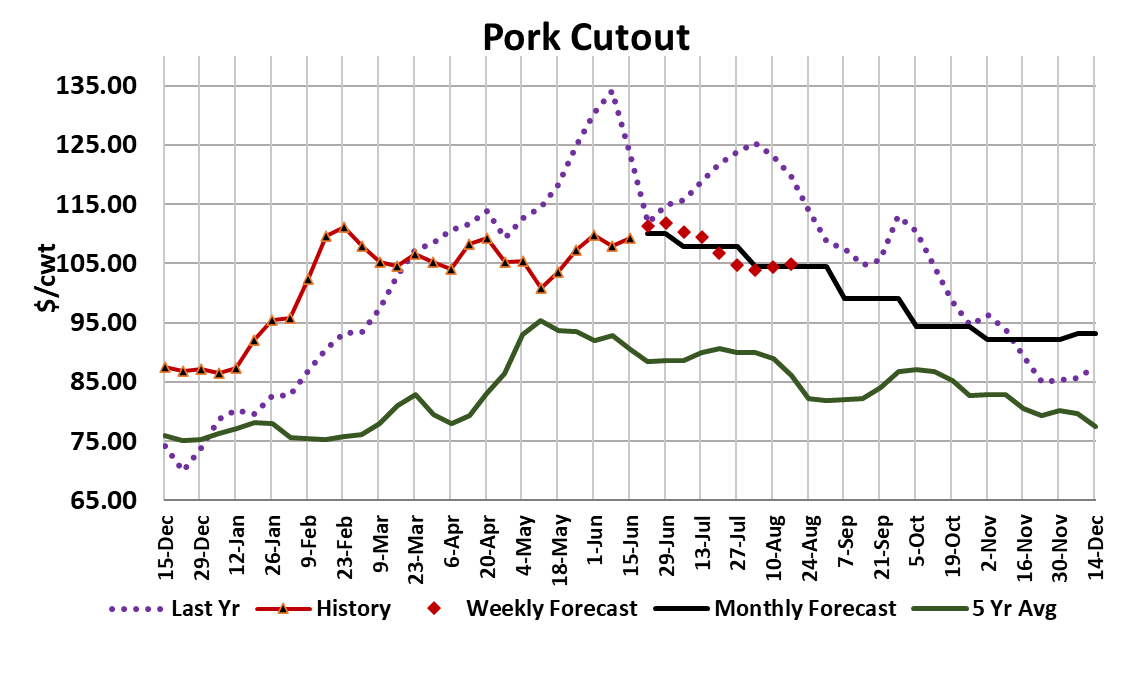

The hog and pork complex continued to work higher this week, and

it definitely felt like a lot of work. The NDD negotiated market was

up $1.48/cwt through Thursday and the cutout was up $1.43/cwt.

Traders got a bit of a scare on Wednesday when the belly primal

printed sharply lower, but it bounced back on Thursday, and all was

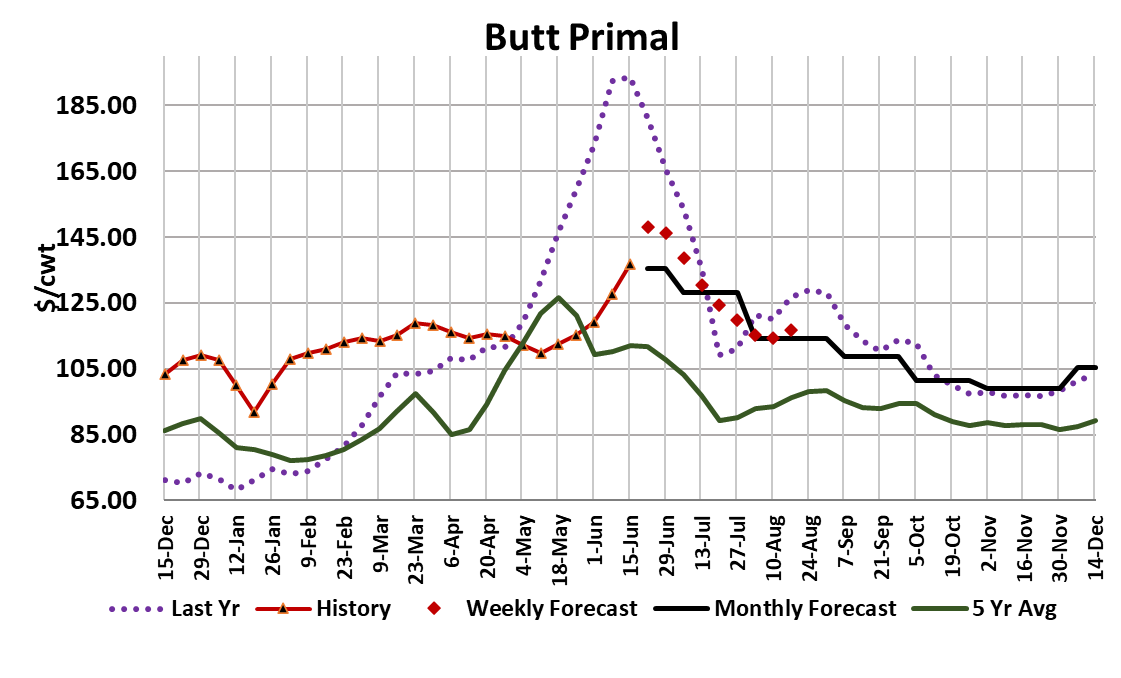

well. It wasn’t the belly primal that provided support for the cutout

this week. Instead, it was the mighty butt primal with some help

from the hams. I’m not quite sure what lit a fire under the butts over

the past few weeks, but it has outperformed all of the other primals

in terms of percentage price gains. The two likely sources of

strength would be either a major retailer preparing to feature butts

heavily for Father’s Day or Independence Day or S. Korea sucking

them out of the domestic market. Either way, the gains in butt

prices came at an opportune time and probably kept the cutout from

slipping lower over the past few weeks.

I don’t see the strength in butts continuing much longer, perhaps

another week or two, and then I’d expect butt pricing to move back

more in line with the other retail primals. My presumption is that,

going forward, the bellies will provide the primary support for the

cutout, but I have to admit that right now that theory looks a little

shaky. Demand for bacon is very inelastic and so it is normal for

belly prices to rise and kills shrink in the summer. Bacon also sells

well through foodservice channels and I am expecting that

foodservice business will be brisk this summer as consumers travel

like crazy now that COVID fears have faded. Just because the belly

rally hasn’t taken hold yet doesn’t mean that it won’t, so I will hold

out hope for the bellies a little longer. Hams are getting very

expensive, with the primal printing over $98 on Thursday afternoon.

I think it can hold that level, but wouldn’t expect it to advance much

beyond it. So, hams may provide temporary support for the cutout

while the bellies are getting organized for their rally.

At some point in the next 2-3 weeks, we could see a hand-off from

the hams to the bellies and that could keep the cutout firm. I’m

forecasting the cutout to average over $110 for the next 3-4 weeks

and that should put us past the smallest kill of the year. The

negotiated hog market has shown no signs of backing down and

we’ve seen quotes near $120 for several days now. I’m nervously

watching for the heat dome that the weather service says is forming

over the hog production regions. That has the potential to bring

excessive heat to hog barns in the Midwest, slowing gains and

forcing packers to compete even harder for the available hog supply.

In my opinion, this potential weather event is the most important

factor to watch for in the next few weeks. If I’m wrong on the nearterm price forecasts, it will likely be that I was too low because the

heat wave cut production and thus drove prices higher than

expected.

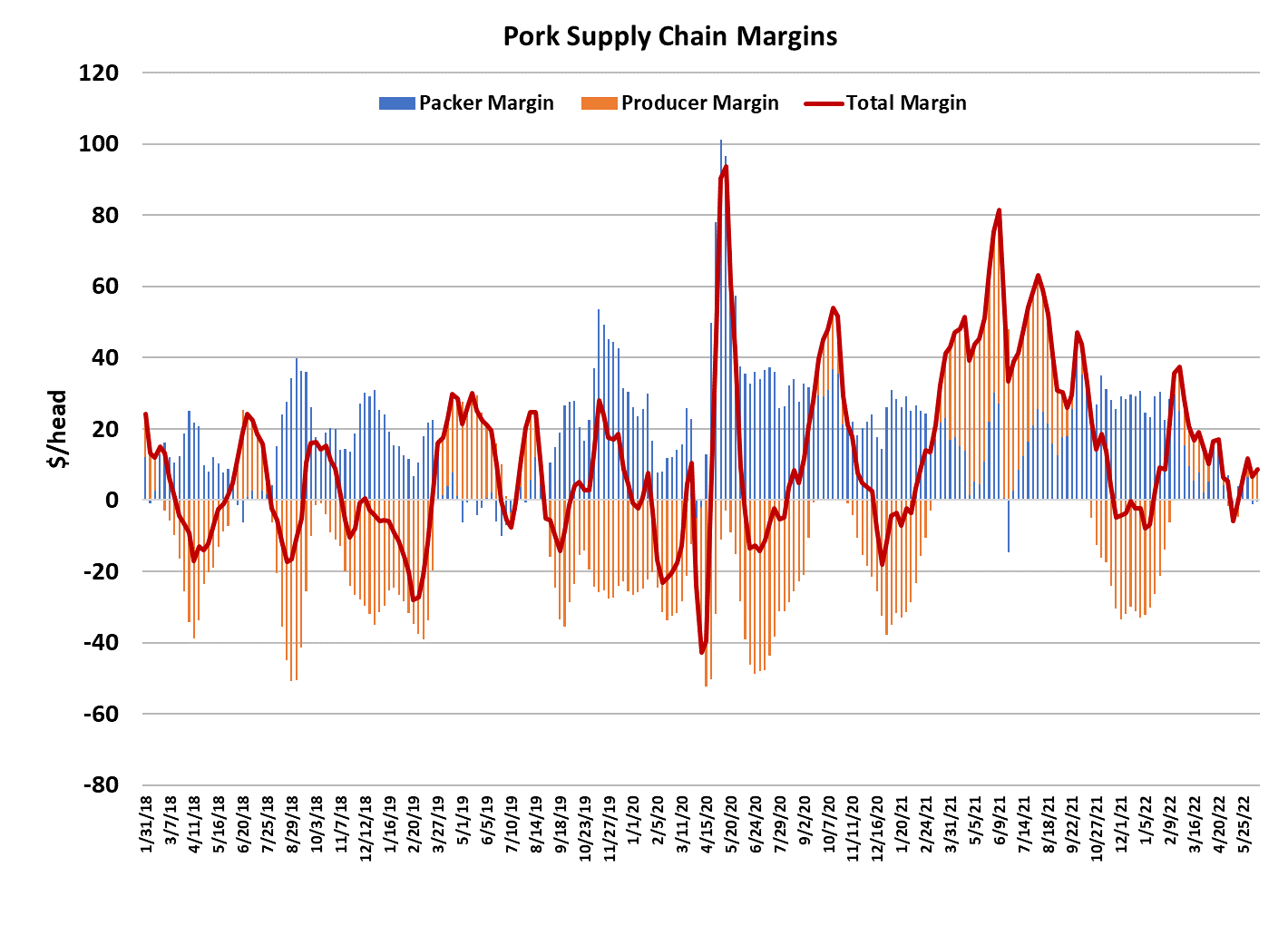

Pork packer margins were about -$1/head this week and I suspect that

margins will get worse before they get better. This is just a fact of life for

pork packers that margins are soft in the summer. The industry must

have enough packing capacity to handle the seasonal surge in hogs each

fall and so they have built toward that goal, but this creates an overcapacity problem in the summer when hog numbers are seasonally tight.

Packers are forced to compete vigorously for those hogs that are

available, driving up cash hog prices and sending margins into the red.

USDA is set to release its summer issue of the Hogs and Pigs survey in a

little less than two weeks. I am looking for it to show the breeding herd

about flat with what they reported in March and 2% below last year. I’m

calling the March/May pig crop down 1% as improving productivity helps

to offset the 1.9% smaller breeding herd that was available to produce

that pig crop.

So, from what we already know about past pig crops and my

expectations for the breeding herd on June 1, it is safe to say that market

hog availability should be down about 1% YOY for the balance of 2022.

Of course, exports are expected to be way down this year (the current

estimate is 6% below last year) and so that will take some of the edge off

of smaller domestic pork production. In the end, it seems likely to me

that 2022 per capita domestic pork availability will be very close to what

we saw in 2021 but price levels should be lower because of the demand

fade coming out of COVID. I’m expecting total hog slaughter this week

to be close to 2.35 million head, which would be 3.6% below last year.

My guess is the kill will continue to shrink until we see a sub 2.3 million

head kill in late June or early July and that will mark the smallest nonholiday kill of 2022. By the end of August, kills should be back near 2.5

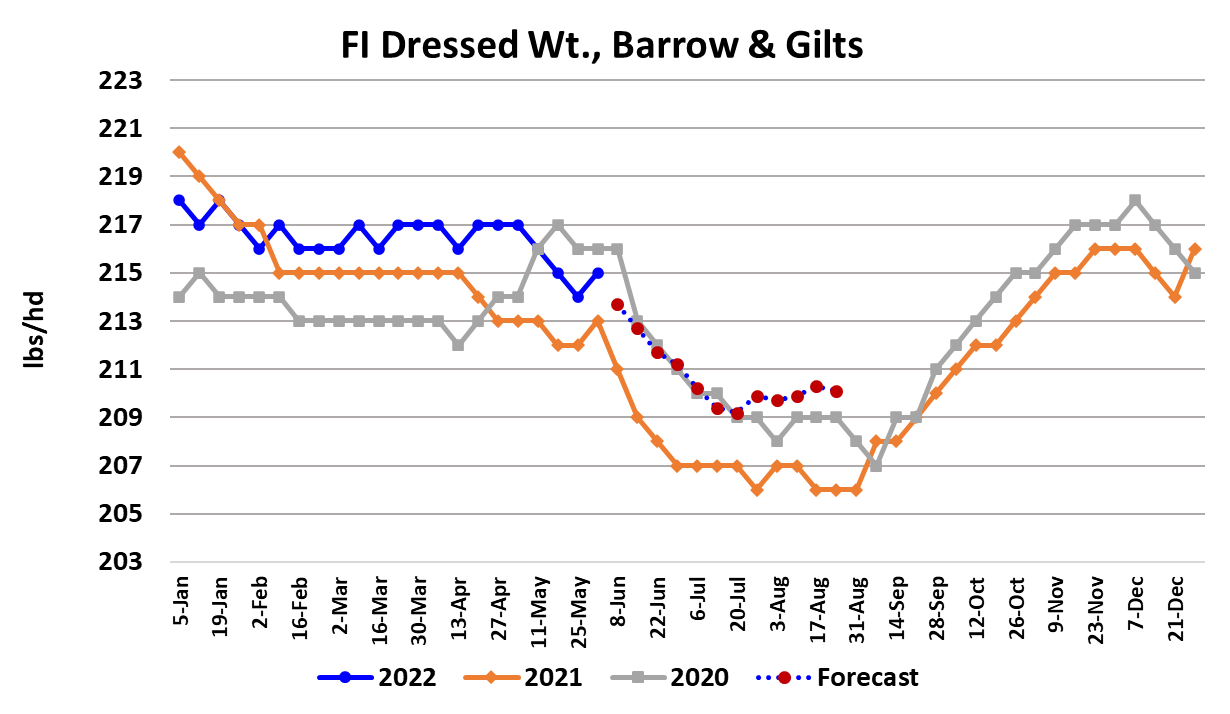

million head per week. Barrow and gilt carcass weights ticked higher

this week to 215 pounds, but the data was for the holiday week, so that

isn’t too concerning.

Weights seem to be pretty normal and in a good spot right now. That

may turn out to be fortuitous if a heat wave sets in. At least we won’t be

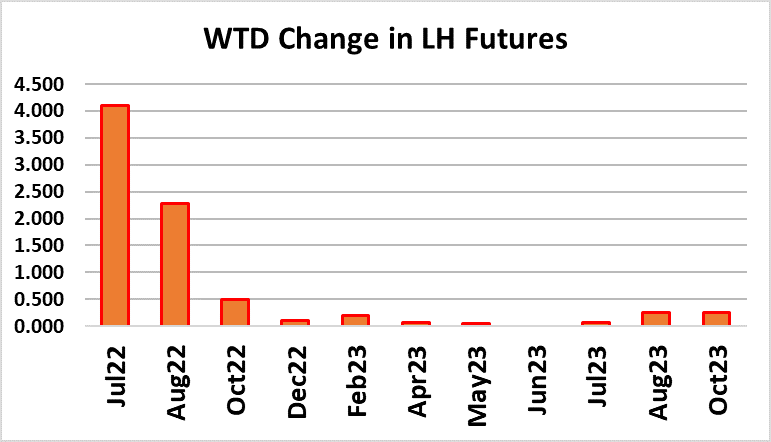

starting out with excessively light carcass weights. Jun futures expired

on Tuesday at $108.57, a little more than $8 over where May expired. I

suspect that Jul will expire a lot closer to Jun than May did, but the wild

card is the weather over the next couple of weeks. I guess I’m a little

surprised that traders haven’t run the Jul contract further out in front of

the cash index in anticipation of potential supply tightness due to

weather. Either way, that puts the weather forecast firmly at the top of

our watch list for next week. A close second will be to watch the belly

primal for signs of life that could put the cutout in position to exceed $110

for a few weeks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}