Pork Wrap June 16

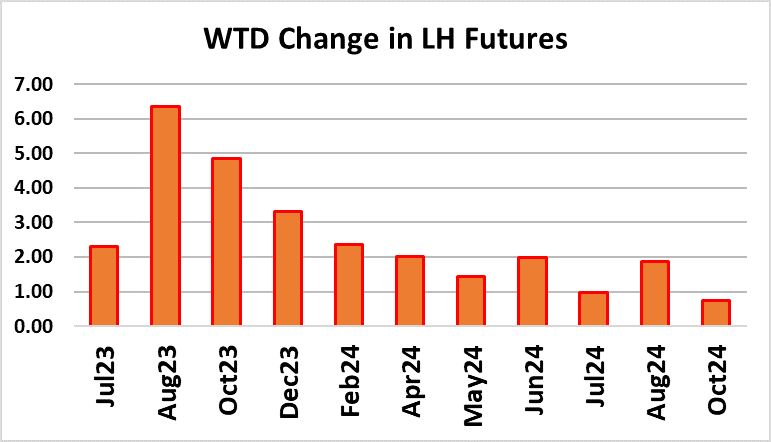

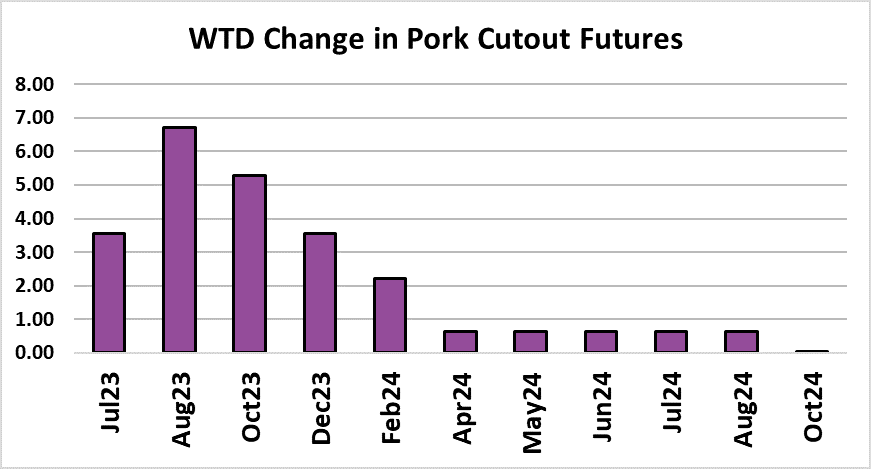

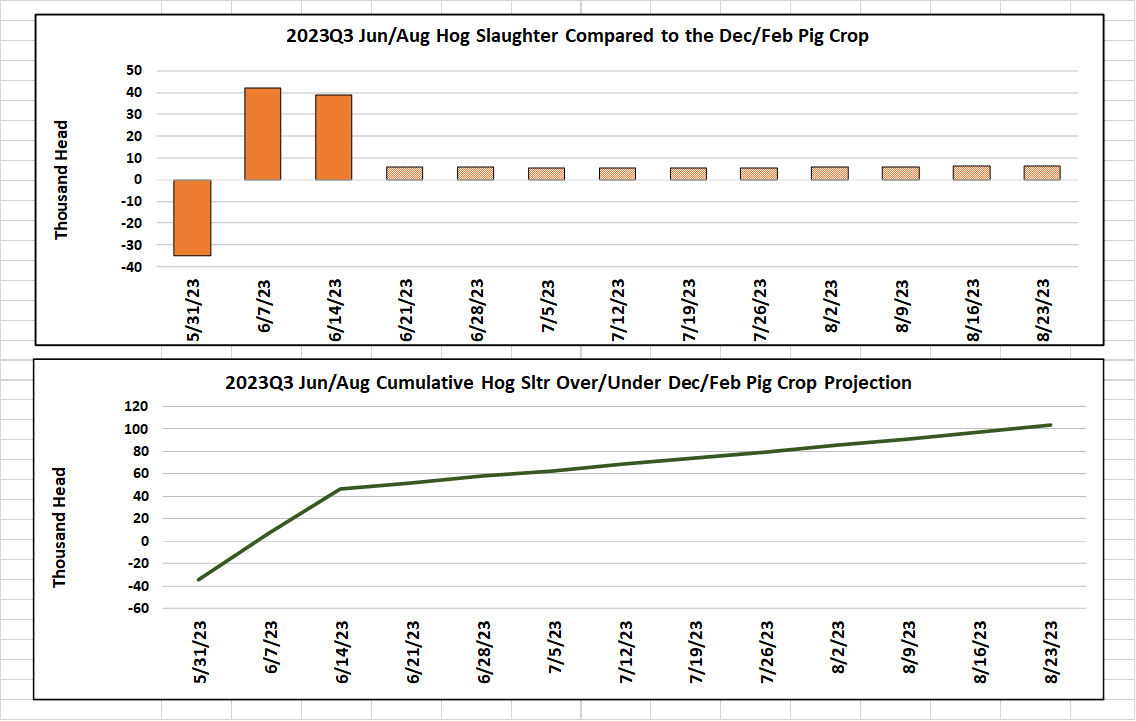

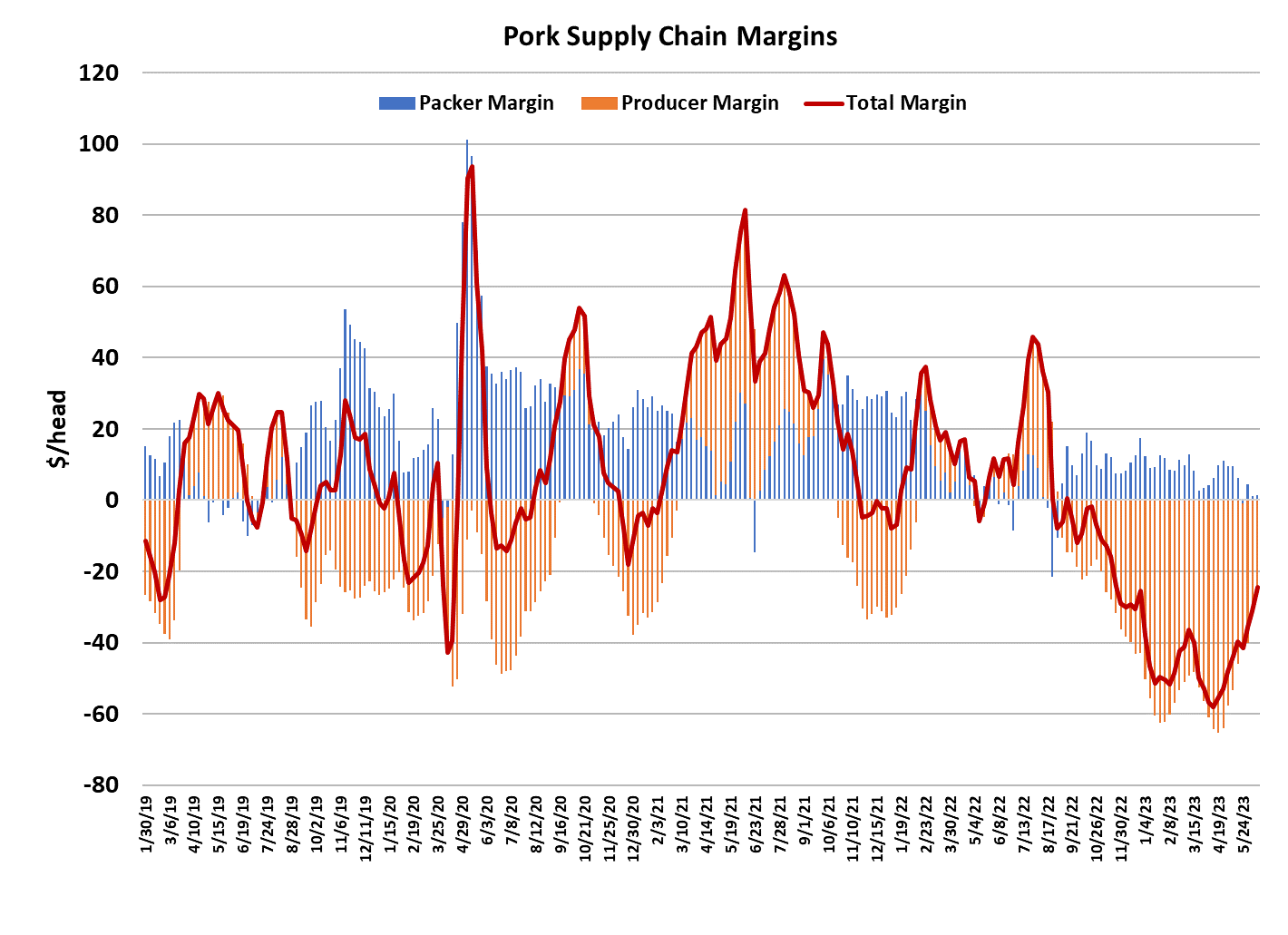

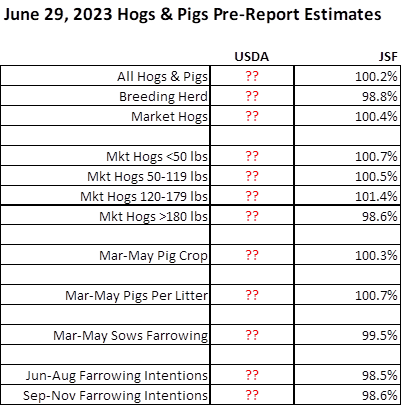

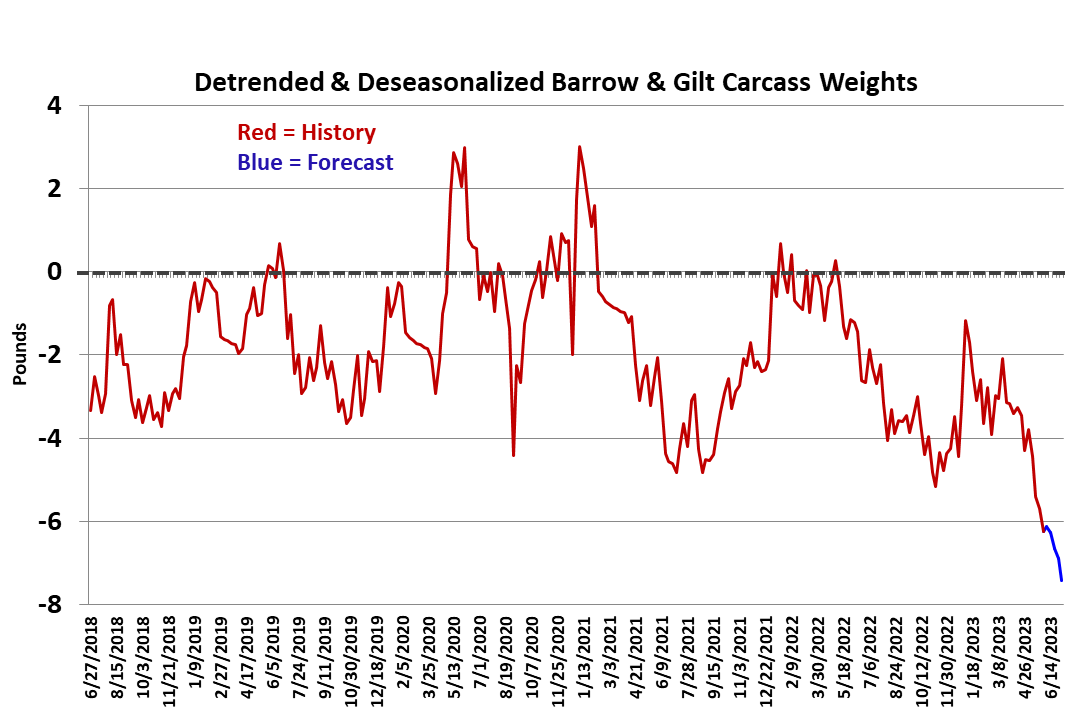

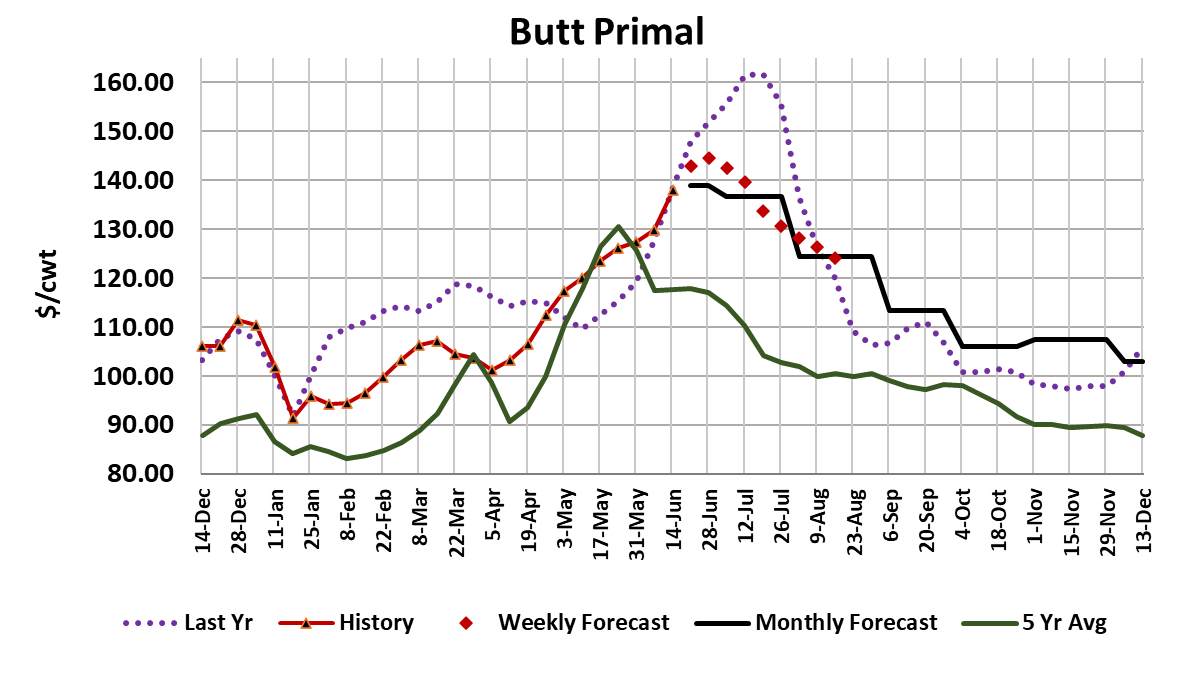

Prices in the hog and pork complex continued higher this week, with the NDD negotiated hog market adding $3.69/cwt on a weekly average basis. The cutout was also stronger, averaging $2.93/cwt higher through Thursday. So now instead of $1 or $2 gains in the cutout, now we are getting close to $3 a week. That kind of acceleration is just what the bulls like to see, and it is coming at the time of year where it is easy to imagine it will continue to accelerate as hog slaughter declines seasonally. Thursday afternoon’s cutout printed just over $90. The last time it was that high was around Christmas. It has been a rough road to get here, but things are finally looking better for hog producers. Seasonally shrinking hog supplies are coinciding with better domestic demand to lift prices in a meaningful way. It doesn’t mean that hog producers are turning a positive profit, but at least the losses they are experiencing now are a lot smaller than record-low margins they saw back in the spring. I calculate this week’s producer margin at -$26/head. Five weeks ago, the negative margin was double that size. I’m projecting this week’s slaughter to total 2.33 million head, down slightly from last week and next week could see the kill drop below 2.3 million head. The next few weeks will likely produce the smallest non-holiday kills of 2023. However, it still looks like this week’s kill was about 40k larger than what the Dec/Feb pig crop implied, so we might have another quarter where USDA underestimated the pig crop and kills this summer come in consistently larger than expected. It is still early in the quarter, but this bears watching. By mid-July, slaughter levels should start to slowly work higher and by the end of August we should have at least a couple of weeks where slaughter exceeds 2.5 million head per week. USDA reported FI barrow and gilt weights down another pound this week and the DTDS weights have moved to really low levels. That suggests that producers have marketed their hogs aggressively and the pipeline is lean at the moment. I recently went through all of the supply forecasts in anticipation of the upcoming Hogs and Pigs report and I settled on projecting the breeding herd to be down 1.2% YOY as of June 1. It is hard to know just how much liquidation of breeding stock has occurred in recent months, but dreadful producer margins make it impossible for me to believe that the breeding herd will hold steady or increase. That said, 1.2% is not a huge reduction and I feel sure there will be further reductions as we move into the second half of the year. Recall that the breeding herd as of March 1 was up 0.5% YOY and thus I’m forecasting the March/May pig crop to be up 0.3%. Those are the hogs that will be slaughtered during the upcoming Sep/Nov quarter. So, if I’m close on those estimates, we won’t see a significant YOY reduction in hog slaughter until perhaps December. The supply side of the market doesn’t look very bullish for the remainder of 2023, but the good news is that the demand side seems to be healing. I am particularly encouraged by price strength that has showed up recently in the retail primals and trims. It makes me think that perhaps we are now starting to see a meaningful shift toward pork by retailers. Also, there is the possibility that we could see a demand boost in the second half of June due to Prop 12 (oddly enough). The California Dept of Agriculture has made it abundantly clear that they won’t be sending the Prop 12 police out on July 1 to check compliance and they have also signaled that it is fine to sell non-compliant product that was in inventory prior to July 1. Thus, we could see a lot of buying interest near the end of June from California retailers looking to build up inventories and thus avoid paying the premium for compliant product in early July. Butts are one item that have appreciated rapidly over the past few weeks, and they don’t seem to be running out of gas. Even the rib primal, which as been in the dumpster for most of the past year, has started to climb higher. On the processing side, hams were a little lower this week and bellies were a little firmer. I see the hams as mostly sideways to modestly higher over the next few weeks, but bellies are likely to keep pushing higher as production declines. To be sure, any demand improvement that we see in mid-summer is going to pale in comparison to the red-hot demand that existed in the summers of 2021 and 2022, but every little bit helps. I am forecasting August cautiously because that is when many Americans will have to resume payments on student loans. That has the potential to be a significant negative for pork demand. Another encouraging sign for demand is that USDA reported retailers didn’t increase the retail price of pork, on average, during May, but the retail price of beef shot higher. Pork is becoming more competitive in the retail meat case. Of the three major holidays in June/July, Memorial Day and Father’s Day are seen as more important for beef, whereas pork is usually king in July 4th retail ads. Memorial Day is long gone and after this weekend Father’s Day will be in the rearview mirror also. So, the calendar is turning more favorable to pork. Next week, look for further gains in both the cutout and negotiated hog pricing. Keep an eye on the weather in the Midwest because if a heat wave materializes while the hog pipeline is so current, it could quickly reduce weight gains, resulting in faster price increases.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}