Pork Wrap June 14

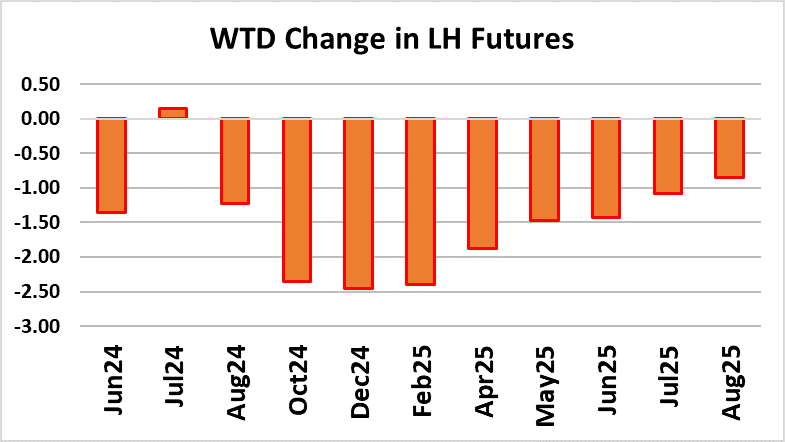

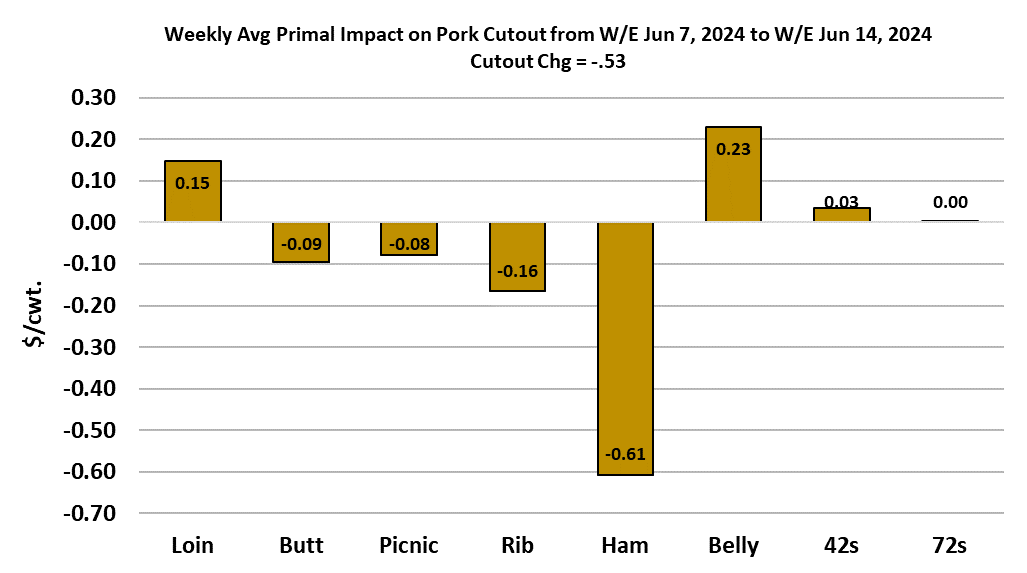

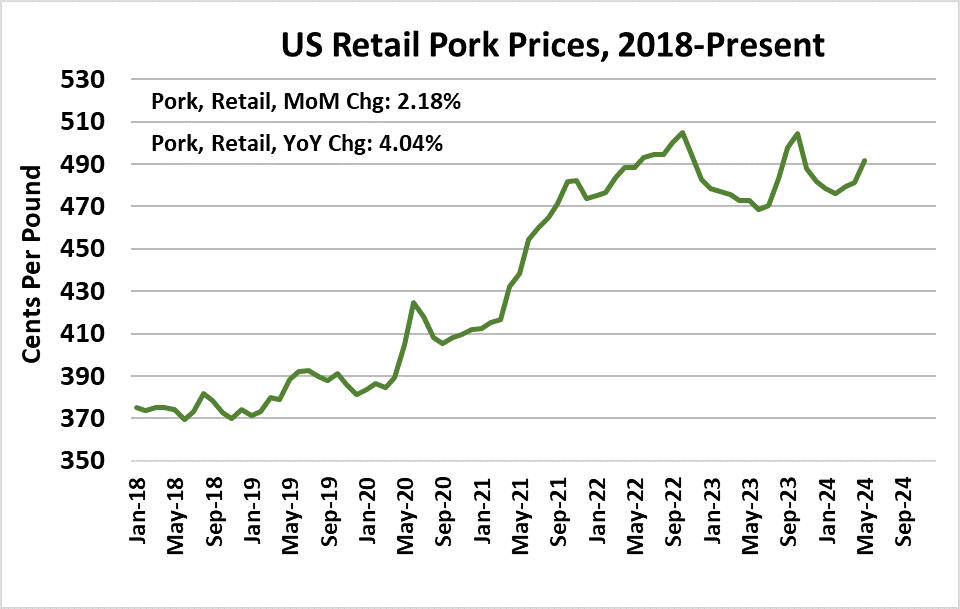

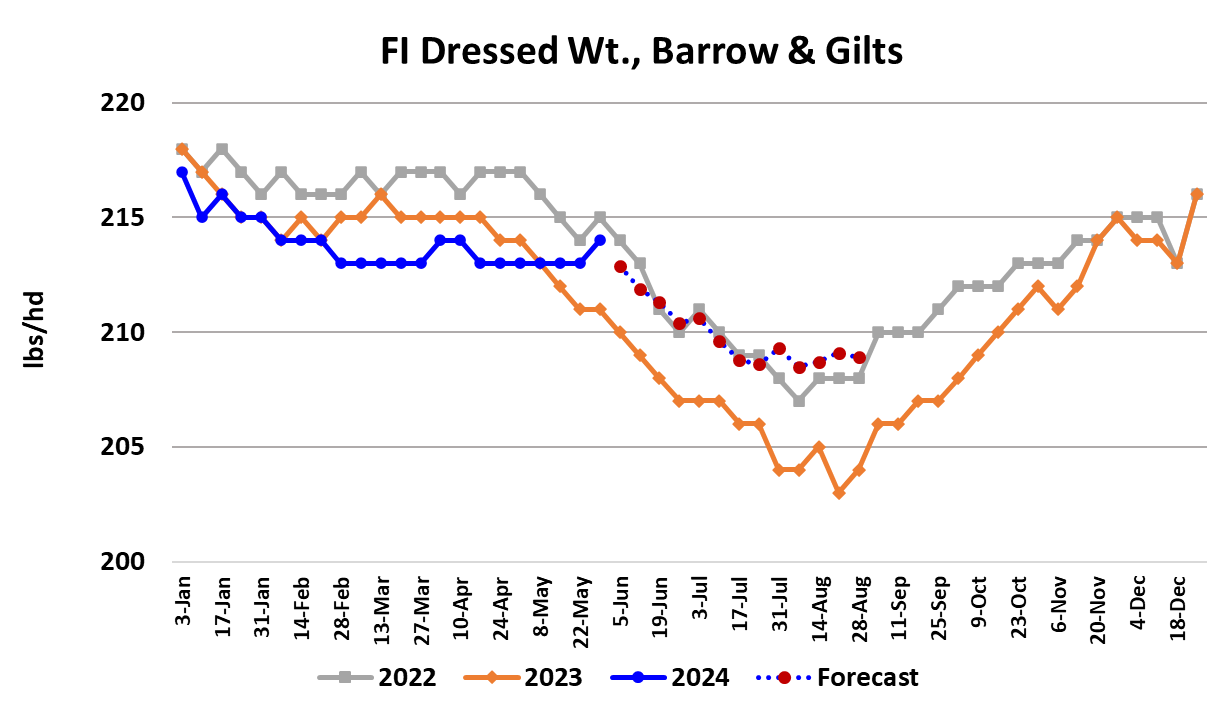

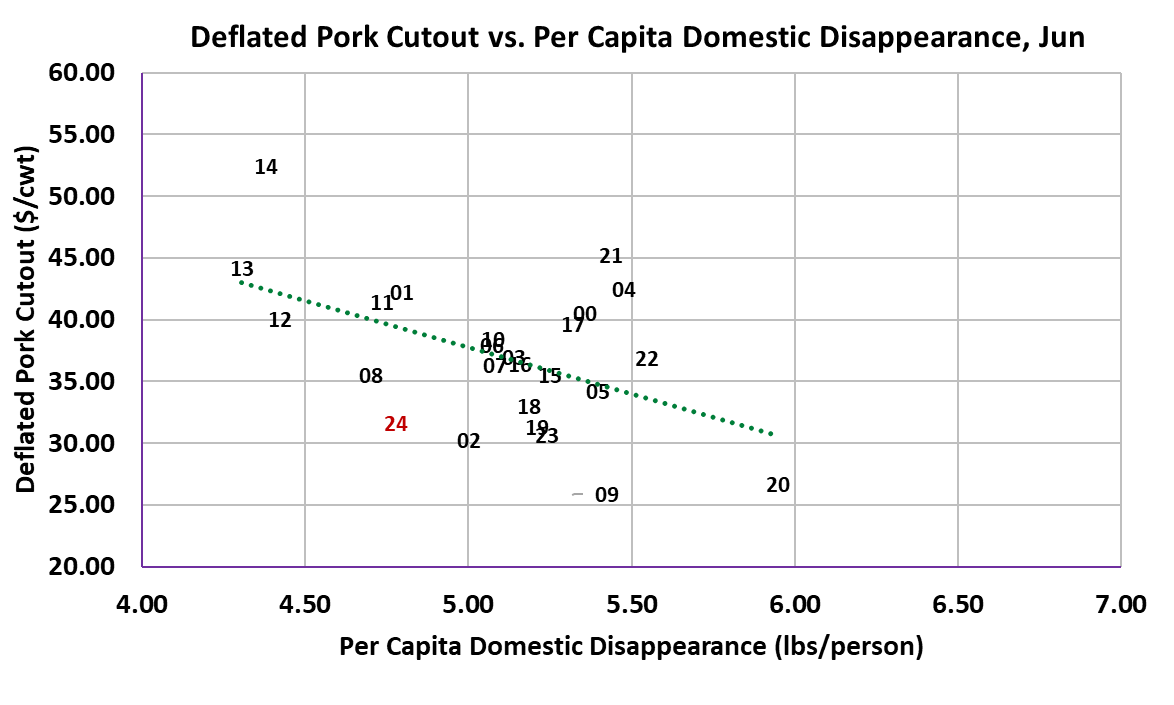

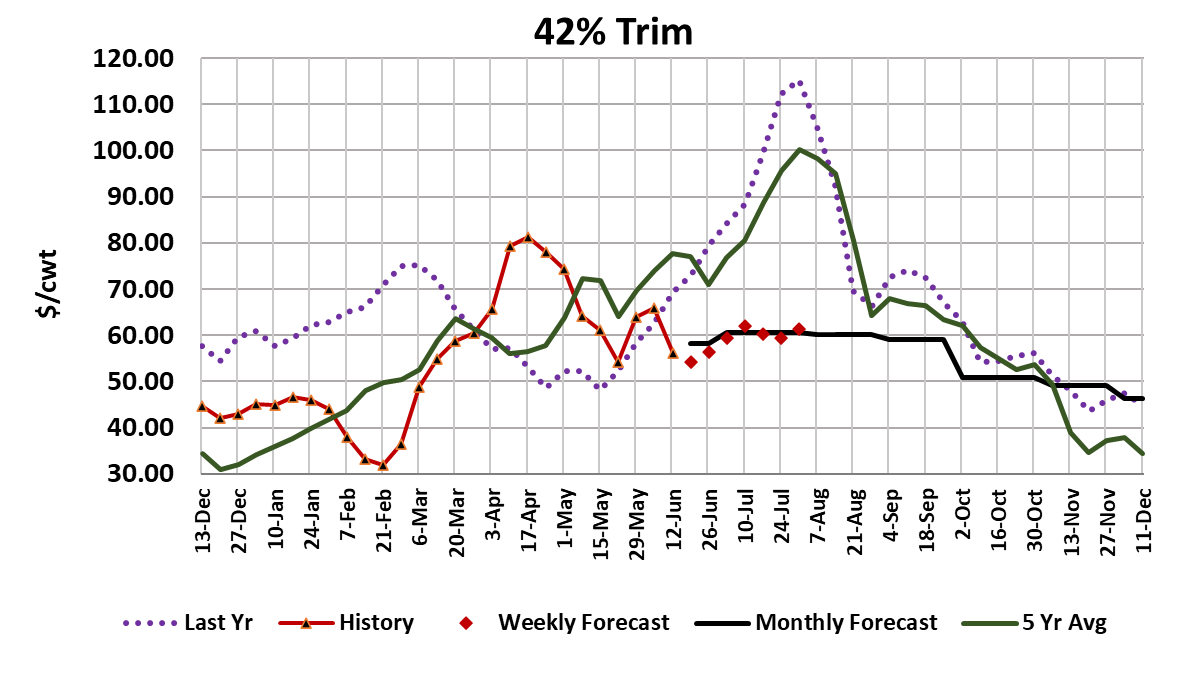

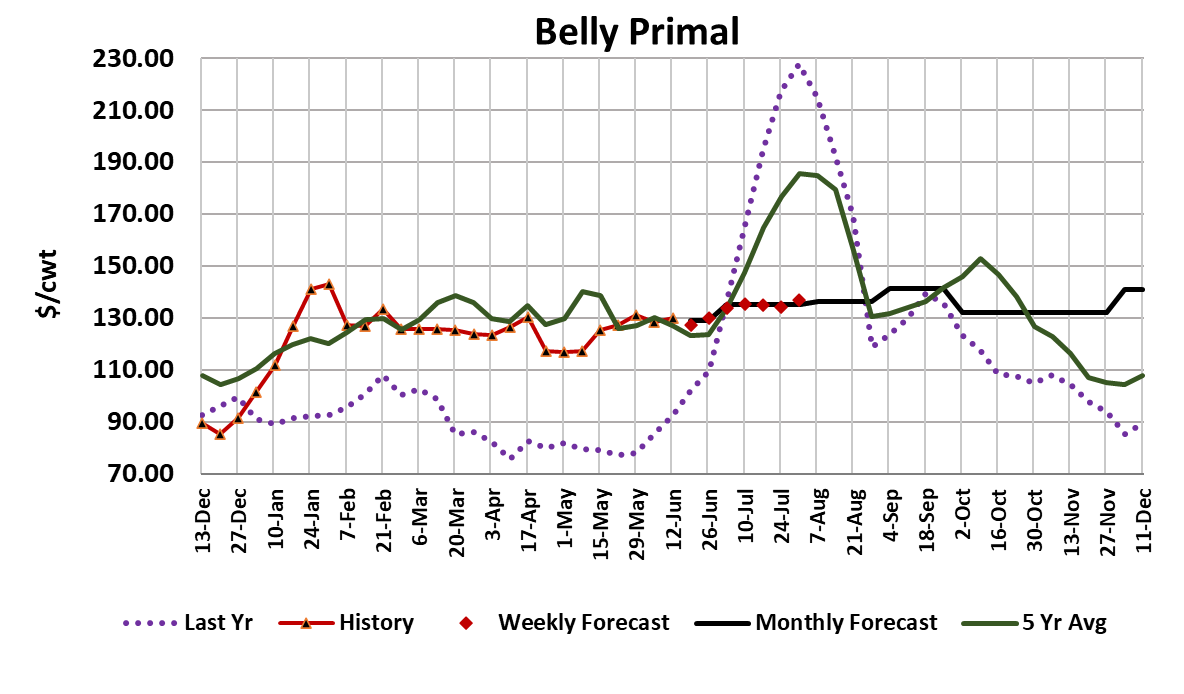

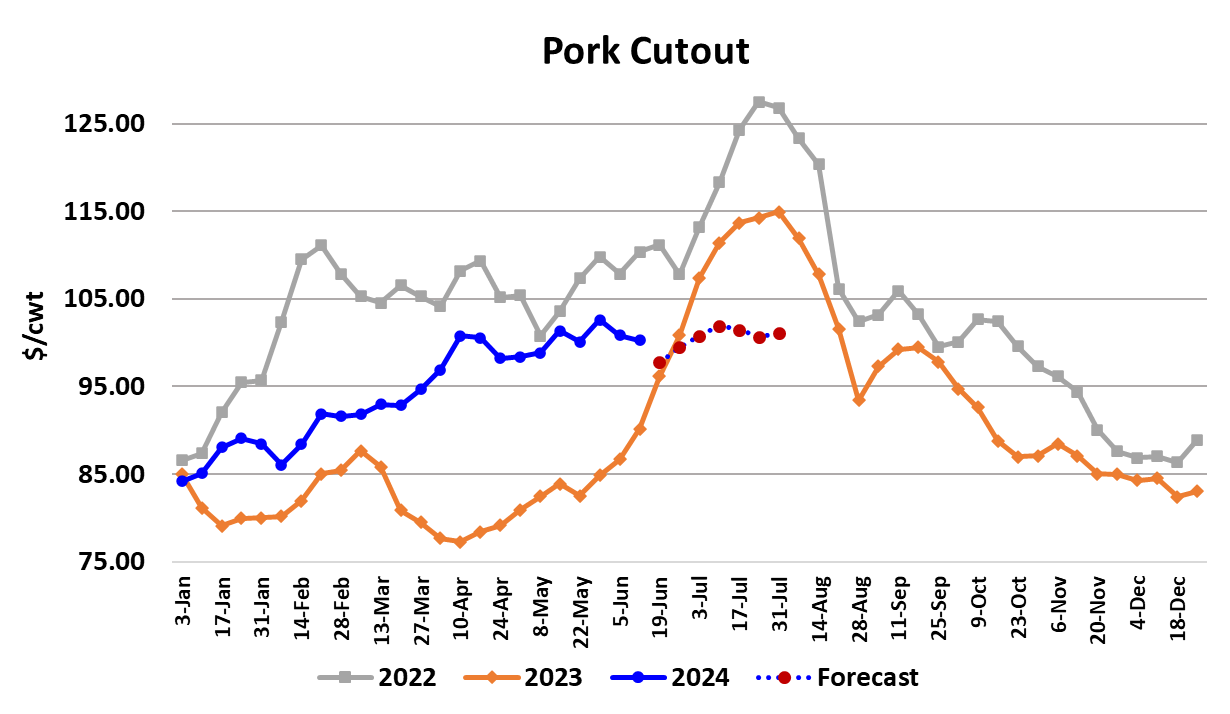

Stagnant continues to be the best description of the price action in the hog and pork complex. The cutout lost $0.53 on a weekly average basis in moving to $100.29 and the NDD negotiated market added only $0.20 this week. The lean hog index averaged $0.40 lower on the week and settlement on the Jun contract, which expired today, looks like it will be slightly under $91. For those keeping track, the Apr contract expired just under $91 and the May contract expired slightly over $91. So, prices have been basically stagnant for the better part of three months now. Further, I don’t see a lot of evidence that is going to change any time soon. Hog slaughter is nearing its seasonal low, which might not be very different from current levels and hog weights have been stubbornly resistant to moving seasonally lower. There is finally some hot weather in the forecast for the Midwest, so that has the potential to reduce weights and thus cause producers to slow the movement of hogs to market, but that that takes some time to develop and the hogs are coming into this hot spell with weights heavier than normal. In fact, this week’s FI data actually showed barrow and gilt carcass weights increasing and three pounds heavier than last year at this time. In addition, producers are getting better at mitigating the impact of heat in hog barns by using technology, so there are reasons not to expect too much in the way of price gains as the result of a transient heat wave. However, if a heat dome forms over the Midwest and keeps the hogs sweltering for weeks on end, then the risk of a sharp increase in both hog and pork prices is significant. This week’s slaughter registered 2.39 million head, 2.8% stronger than last year but about 32k below the week prior. Next week’s kill is projected near 2.4 million head and I don’t really think it is going to get much smaller than perhaps 2.35 million head during the non-holiday weeks. So, there isn’t much relief coming on the supply side unless the weather drives weights sharply lower. The demand side of the market is looking weaker than it has in a while. The attached scatter diagram for June shows the 2024 data point riding lower to the regression line (“average”) than what we saw in June, 2023. Back in the spring we were talking about how much better demand was this year compared to last, but that has flipped now. If we aren’t going to get much help from the supply side this summer and the demand side looks pretty soft too, what is the impetus for higher pricing? There isn’t much. The best hope the bulls have is that the hot weather in the Midwest will be enough to crater weights and thus significantly reduce production. I’d rate the odds of that as not much better than about 50/50. It could be that weights do start to come down faster than expected, but by mid-July hog numbers bottom and start to increase, thus negating the price impact of falling weights. One thing that traders can watch to help discern if the heat is having an impact on the hogs is the price of fat trim. This week, 42s took a sharp dive lower and are now priced about 20% below last year. If 42s prices suddenly reverse course and head higher that can be an early indicator that hot weather is having an effect on weight gains. This week, the hams were the biggest drag on the cutout, while the bellies were mildly supportive. The ham primal has moved lower over the past two weeks and my guess is that it has about one more week of softness before it starts turns upward again. Absent a significant weather impact, I don’t think the ham primal has what it takes to reach last year’s level this summer. The belly primal has been confounding also. The attached price chart shows that the belly primal has been stuck more-or-less in the $120-130 range for nearly all of 2024. Historically, belly prices have been the most volatile of any part of the carcass, but not this year. This week I brought the forecast down substantially finding it easier to just call the bellies steady rather than to keep calling for a summer rally and continuously having to adjust lower. It is also hard to see much further upside in the primals that represent retail items, although loins might still make a modest push higher after Independence Day. That doesn’t leave much to drive the cutout higher and thus the fundamental forecast now has the cutout topping in the low $100s this summer, before turning lower in August. Another ominous sign that appeared this week came from the retail price data for May, which showed the retail pork price up 2.2% from where it was in April. The trend toward higher retail prices, should it continue, could slow consumer off-take, making it more difficult for wholesale prices to advance. The weekly export data hasn’t looked all that great recently either. At present, I can identify several price-negative factors in the market, but the only price-positive factor that seems to exist is hot weather in the Midwest. Maybe the hot weather can offset the influence of all the negative factors, thus helping to extend this stagnant price environment into July. That seems like the safest call to go with, so I’m looking for next week to give us more of the same with the cutout barely changed to possibly lower next week and the negotiated hog markets maybe just a little higher.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}