Pork Wrap June 10

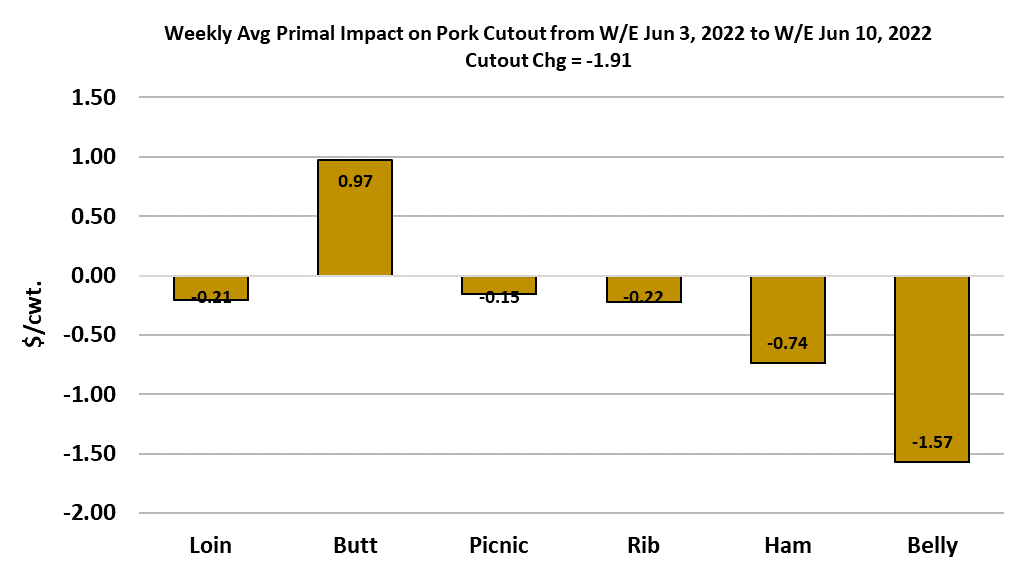

Things got a little more uncomfortable for pork packers this week with

the cutout declining and the price of cash hogs rising. On a weekly

average basis, the cutout dropped $1.91/cwt this week and the WCB

negotiated market was up $2.88/cwt. By my calculation, that pushed

packer margins a little more than $1 into the red. Negative margins

are not that unusual at this time of year when hog supplies tighten, so

packers are probably taking it in stride, knowing full well that they will

more than make it up this fall when hog numbers expand seasonally.

The dip in the cutout caused the combined margin to move lower this

week, but as usual, I want to see another data point before declaring

that the demand upcycle is done. The lower cutout this week can be

directly tied to a very weak belly print that occurred on Wednesday,

but prices bounced back near the end of the week. That is the type

of event that seems more like a distressed sale rather than a

substantial turn in demand.

However, even if this turns out to be a brief downward blip in the

cutout, my guess is that the current demand upcycle doesn’t have

much more than 2-3 weeks to run. Hams traded a bit lower this

week, but that could be due to stronger volumes and thus we are only

moving along the demand curve, not shifting it. Time will tell on that.

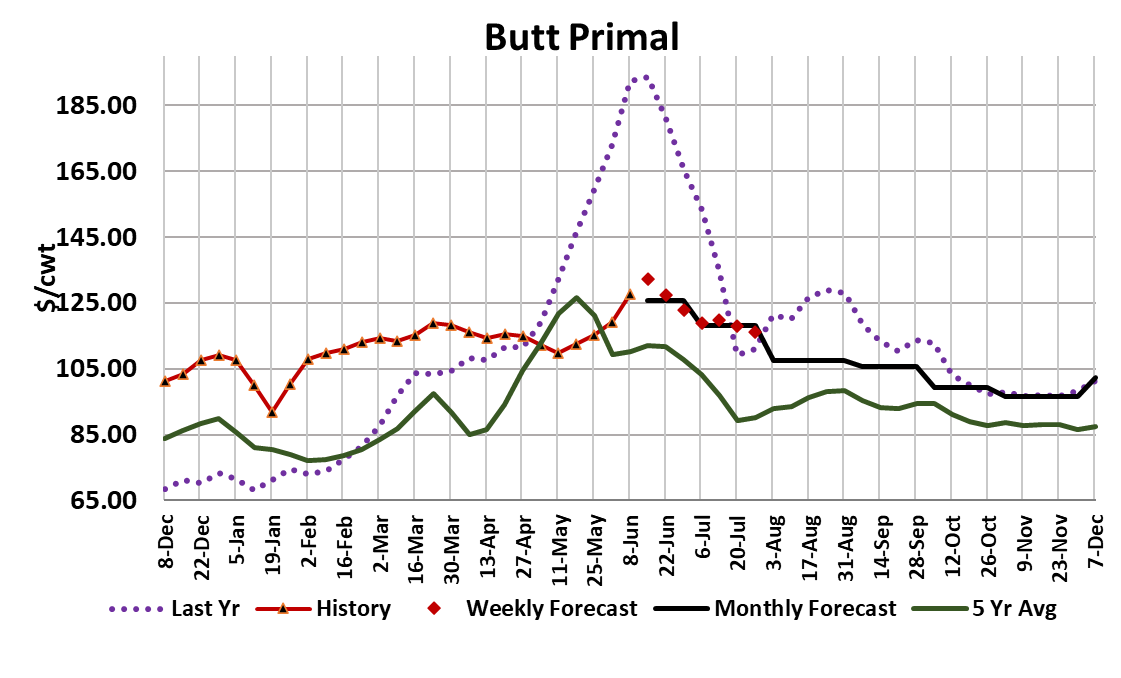

The retail primals held up well this week, with most of them nearly

steady except for the butts which have been on a tear lately and are

now at their highest level so far in 2022. Perhaps one of the large

retailers is planning on featuring butts for Father’s Day or

Independence Day. If they are being exported, the likely destination

is S. Korea. Even if demand holds steady and doesn’t improve from

this point forward, we should still see prices working higher over the

next few weeks because production should shrink. I say “should

shrink” because so far this summer kills have exceeded expectations

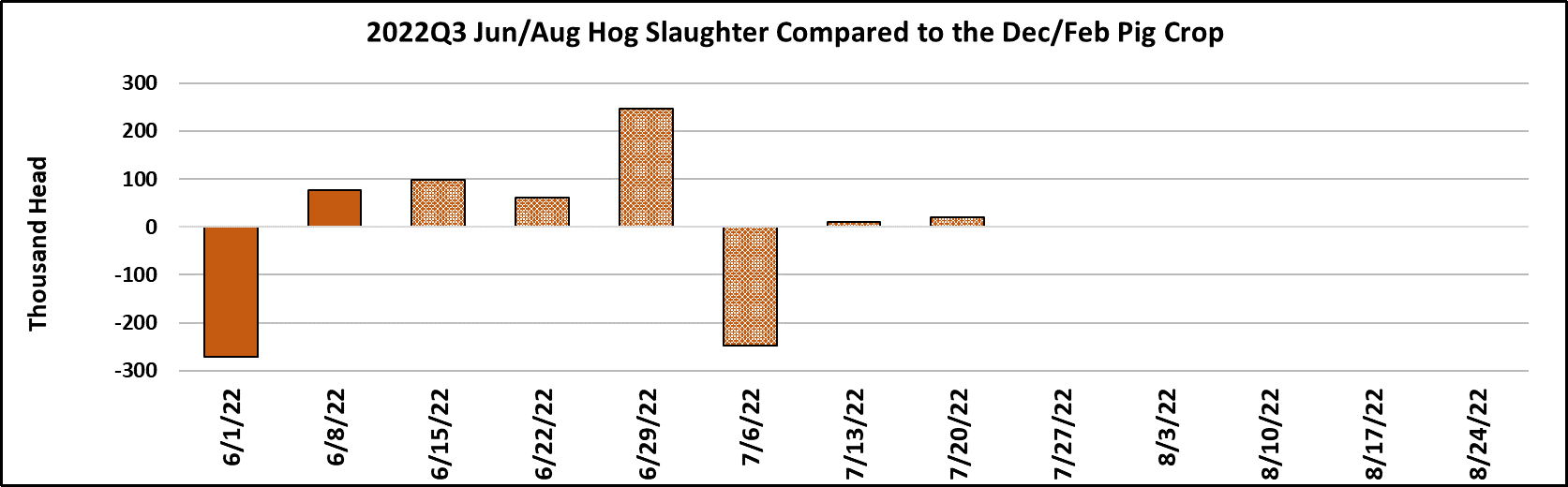

and not shown much of a tendency towards declining. This week’s

kill came in at 2.37 million head, which is actually larger than the 2.34

million head kill in the week prior to Memorial Day.

Go figure. That was about 75k more than what the Dec/Feb pig crop

implied. I am already getting the uneasy feeling that USDA

underestimated this pig crop, just like they did for the one that was

harvested in March/May. As might be expected in this tight supply

environment, packers did a very small Saturday kill this week, but the

daily kills were much stronger than expected. I suspect that packers

have replenished their labor force at a much higher wage than in the

past and don’t want to let that labor go unused, if possible. That

means they have to compete a little harder for negotiated hogs to

round out some shifts and thus we are seeing stronger cash hog

prices. It also means that cutting the kill is not a viable option to

protect their margins. So, they just grin and bear it for now. The dip

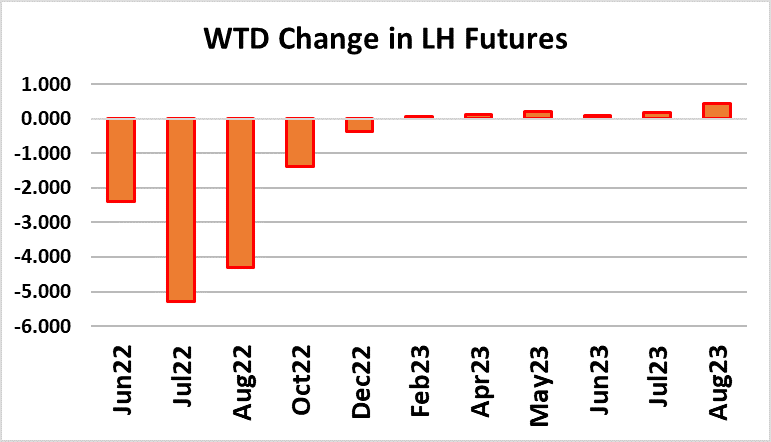

in the cutout this week caused a strong selling reaction in the futures,

with the Jul and Aug contracts both losing over $4.

Jun is too close to expiration to react to the same degree and that was

probably a good thing because the cutout bounced right back late in the

week. I still maintain an expectation for Jun to expire in the $108-109

range, with $108.50 being the most likely. Now that Jun is almost done,

the focus turns to Jul and whether or not the recent advance in the LHI will

continue for another 30 days. My guess is that it will continue in a mild

way for a couple more weeks and then ease lower again so that Jul

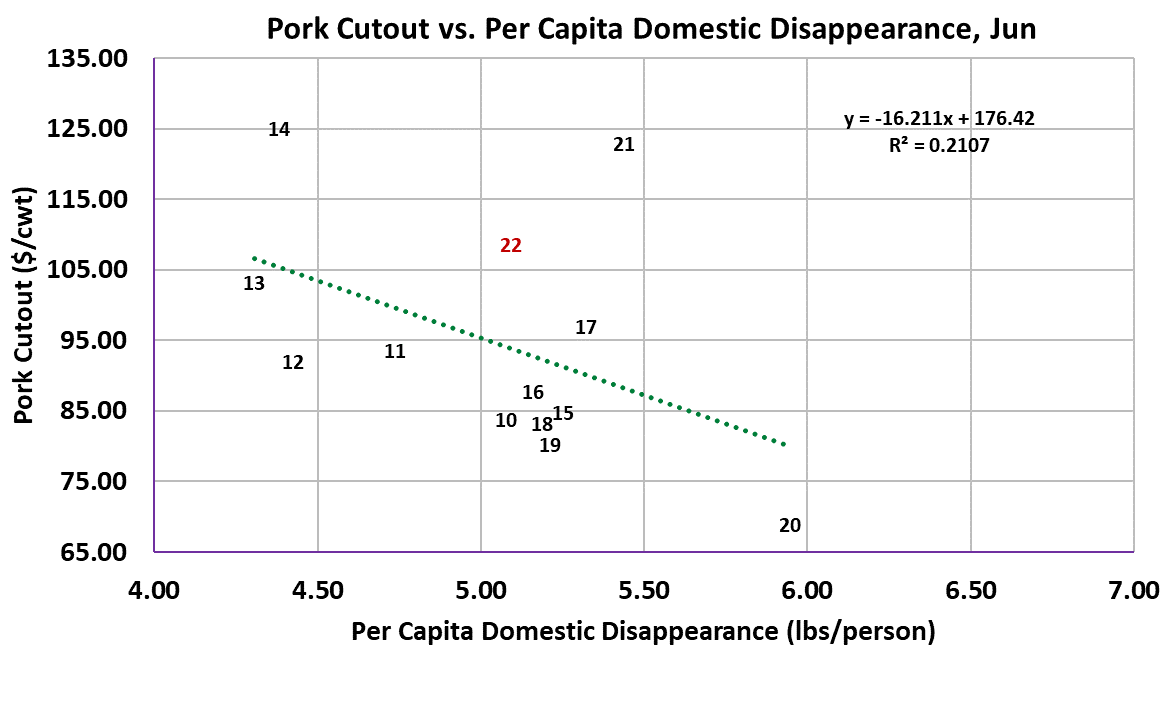

expires a few dollars under Jun. Per capita disappearance this Jun will

be just a tad smaller than last year, reflecting smaller production from a

smaller herd which is at least partially offset by weaker exports compared

to last year. The attached scatter diagram clearly shows how demand is

pulling back from the red-hot level we saw last year. Export markets

aren’t helping. USDA reported the official export data for April this week

and it showed YOY exports down 19.3%. There was even a 20 million

pound decline from March into April.

At the same time, pork imports were strong again at 49% over last April.

Canada is responsible for a big chunk of that increase. So, weaker

demand, both domestic and international, is helping to keep pork prices

below last year’s levels even though pork production is projected to be

3.7% smaller than last June. I think that means that buyers can expect a

better-behaved and perhaps more predictable market this summer than

what we’ve seen in the past couple of years. Barrow and gilt carcass

weights took another step down this week, dropping one pound to 214.

We could see weights rise next week when USDA publishes the

information that they collected during the recent short-kill week, but after

that I’d expect maybe another 5 pounds of downward movement in

weights before they bottom. The weather forecast is calling for some very

hot weather over the middle of the country in the next couple of weeks, so

there is a risk that weights will fall quicker than anticipated. Corn futures

rebounded this week, with the nearby Jul contract adding 46 cents per

bushel to $7.73.

Hog producers are probably happy to keep marketing hogs quickly in this

environment. The hog’s growth curve flattens a lot as they reach the end

of the feeding period and that means it takes a lot more feed to put an

additional pound on them than when they were younger. Feed efficiency

falls rapidly and if feed is expensive, the best option is to get them out the

door quickly so the feed can be used on more efficient gainers. Hot

weather has the effect of stretching out the production pipeline because

appetite declines and it takes longer for an animal to reach target weight.

That would be bad news for packers who are already having to pay stiff

prices in the cash hog market. Thus, a strong heat wave can put more

pressure on packer margins and keep them negative longer than

otherwise would be the case. So, next week’s assignment is to watch the

weather closely and the reported hog weights. We will also be watching

for some reduction in the weekday kills as an indication (hopefully) that

USDA wasn’t too far off the mark with their estimate of the Dec/Feb pig

crop.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}