Pork Wrap July 9

The pork cutout looks like it will eek out another small gain this

week, probably less than $1 on a weekly average basis. Very

light production as a result of the July 4th holiday is helping to

support the cutout currently. Packers are not planning a very

large Saturday kill this week, which is a reflection of seasonally

tight hog supplies. By keeping the kill constrained, they hope to

push the cash hog market lower while supporting the cutout and

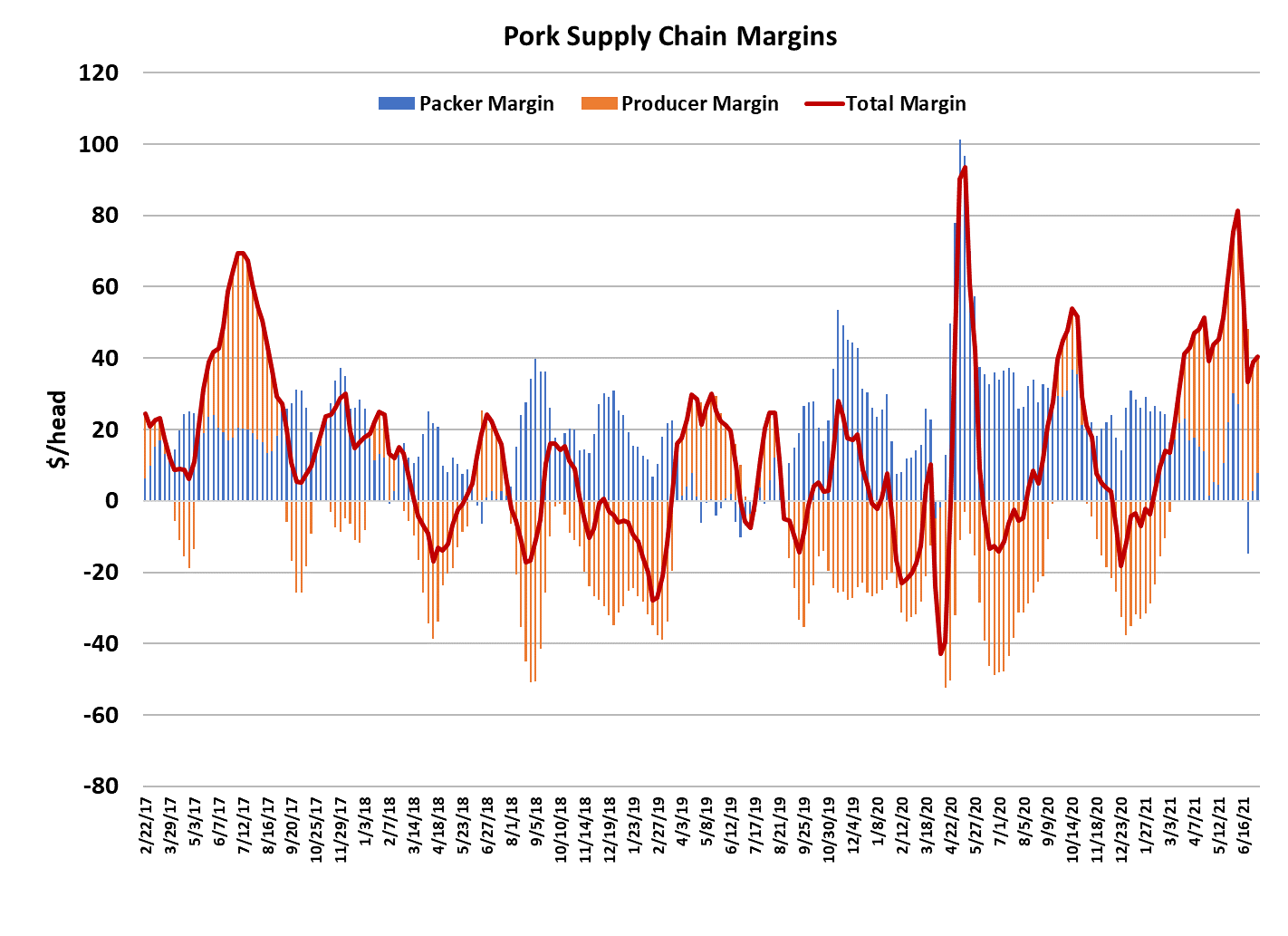

thus improving their margin. They made good headway this

week, with the margin increasing to almost $8/head from just $3/

head the week before.

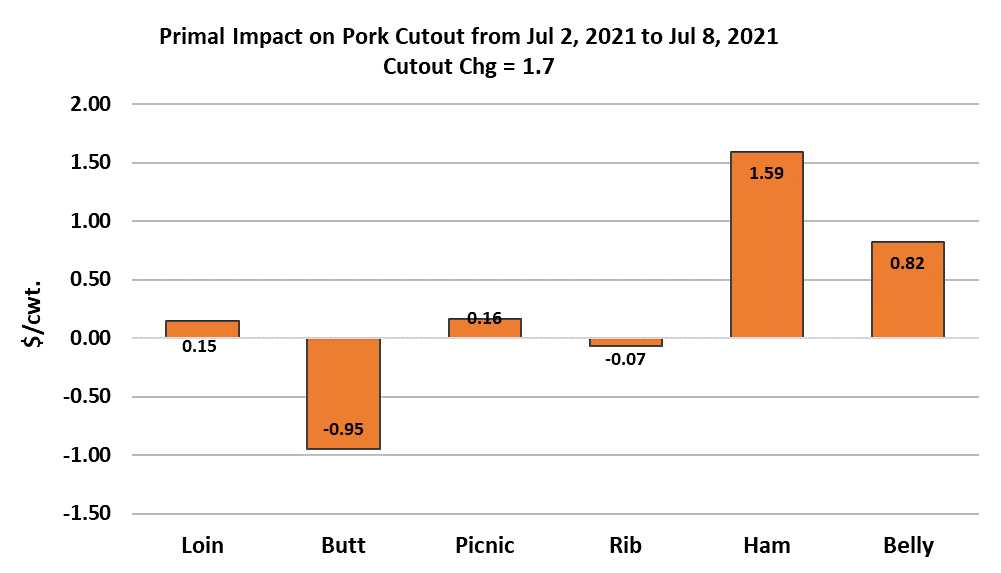

Once again it was the processing items, hams and bellies, that

provided support to the cutout while the retail items were flat or

lower. This is the time of year that ham processors start looking

to begin purchasing for their end-of-year holiday needs. They

are going to find price levels this summer well above what they

have experienced in the past two years, but stocks of hams in

cold storage are about 17% below the long run average, so more

product will need to come from the fresh market this year. Some

buyers may try to wait longer than normal this year under the

hope that bigger production near the end of summer will push

prices lower, but that is a dangerous game because processing

capacity is so tight this year due to the labor situation.

If they wait too long, they may find that they can’t get all of the

hams they need processed in time for the holidays. As a result,

many will likely just pay what they have to in the spot market and

that should keep the hams fairly well supported over the next few

weeks. The cold storage situation in bellies is even worse, now

about 40% below the long run average. That suggests that

bellies won’t come crashing down in the near-term either.

Americans are traveling again and a lot of bacon gets consumed

in foodservice settings so I would expect that belly demand holds

fairly strong at least until mid-August. The retail items will be

vulnerable as production increases next week and I expect that

effect to outweigh the support provided by the bellies and hams,

thus the cutout should ease lower.

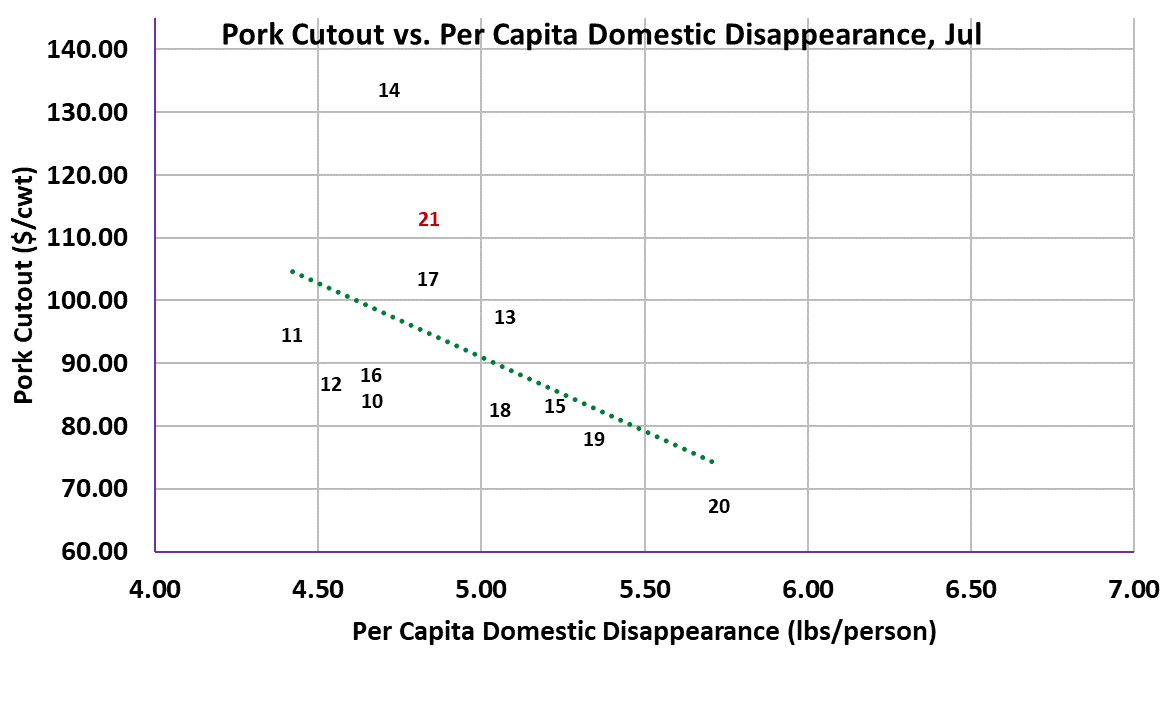

Pork demand is still very good by historical standards (see

July scatter below), but it is slowly fading as the pandemic

recedes and people find other things to do besides cook at

home. Export demand also seems to be softening,

particularly from China. That is pretty worrisome, given the

large proportion of US production that gets exported

(26-30%).

This week we got the official export data for May and it

showed an 11% improvement over last year. That was way

bigger than what the weekly data suggested. I think the

June and July data will show single-digit YOY increases, but

am concerned about what might happen if Chinese demand

continues to drop off in the next few months. It bears close

watching, but unfortunately quality data that is timely on

exports doesn’t exist.

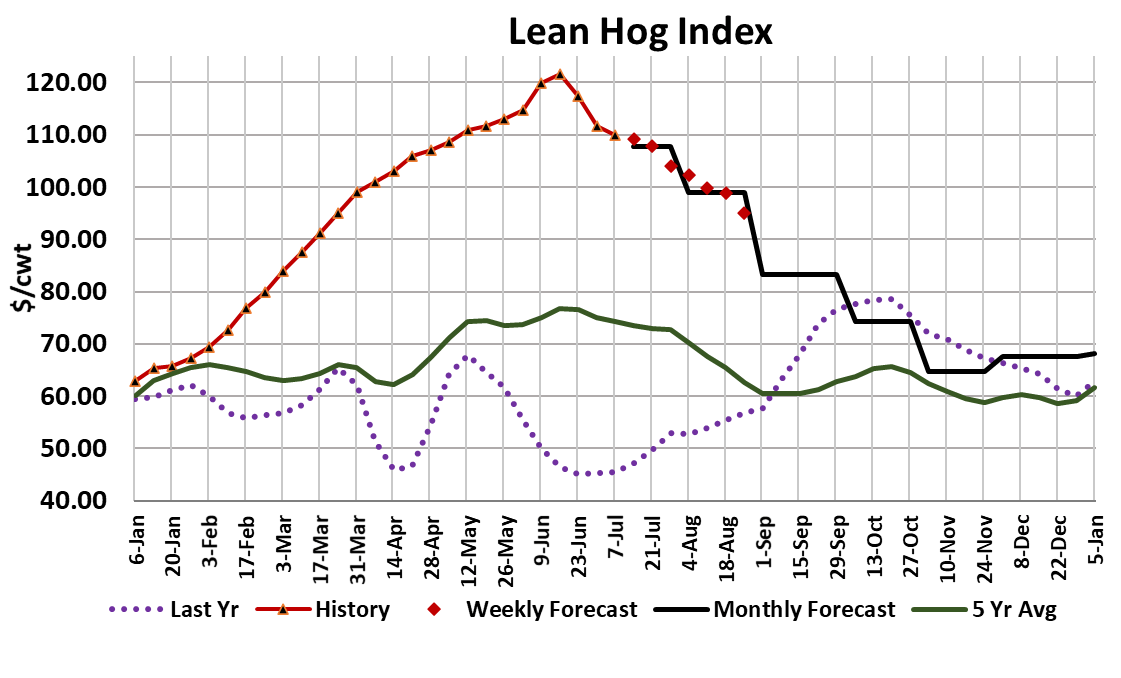

I’m projecting this week’s kill to come in at a little over 1.9

million head, but expect packers to bounce back with a 2.39

million head kill the following week. By the time August

rolls around, weekly kills should be solidly above 2.4 million

head and could reach 2.55 million head just ahead of Labor

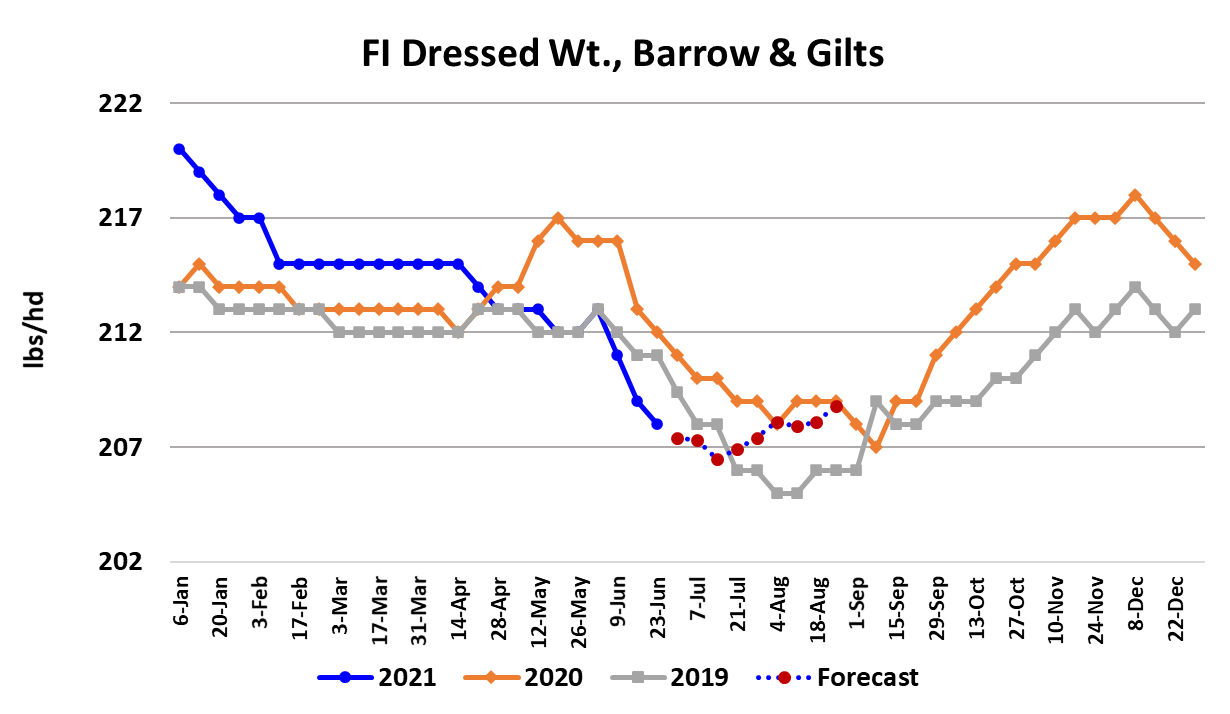

Day. Barrow and gilt carcass weights are now 4 pounds

below last year and 2 pounds below 2019. High corn prices

have likely contributed to the sharp drop in hog weights this

summer, since the weather has not been overly hot.

Small kills + light weights = small production and that is

what the industry is experiencing at the moment and is likely

why the cutout is being supported in the mid one teens.

That will start to change as we move out of July. Kills will

grow and weights will increase seasonally as the weather

starts to cool. If I’m right that demand will continue to fade

over time, then we have the perfect recipe for lower hog and

pork prices from August through December (increasing

supply, decreasing demand).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}