Pork Wrap July 7

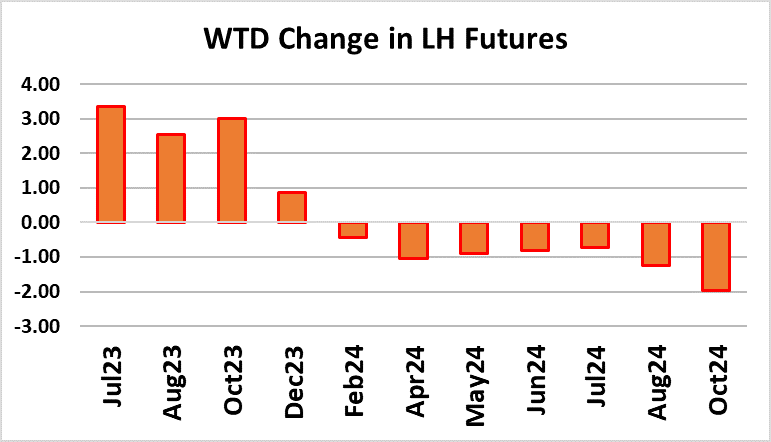

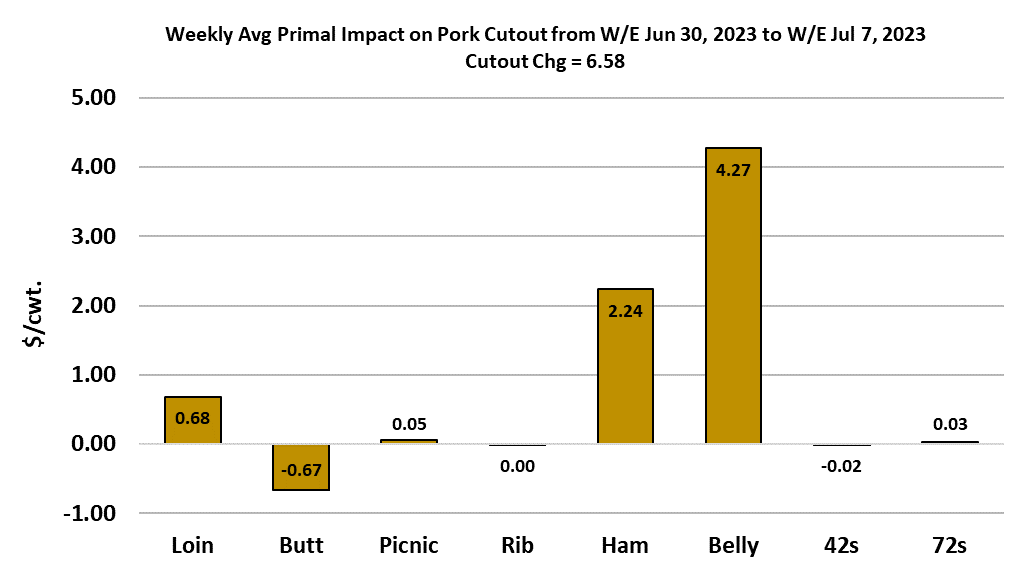

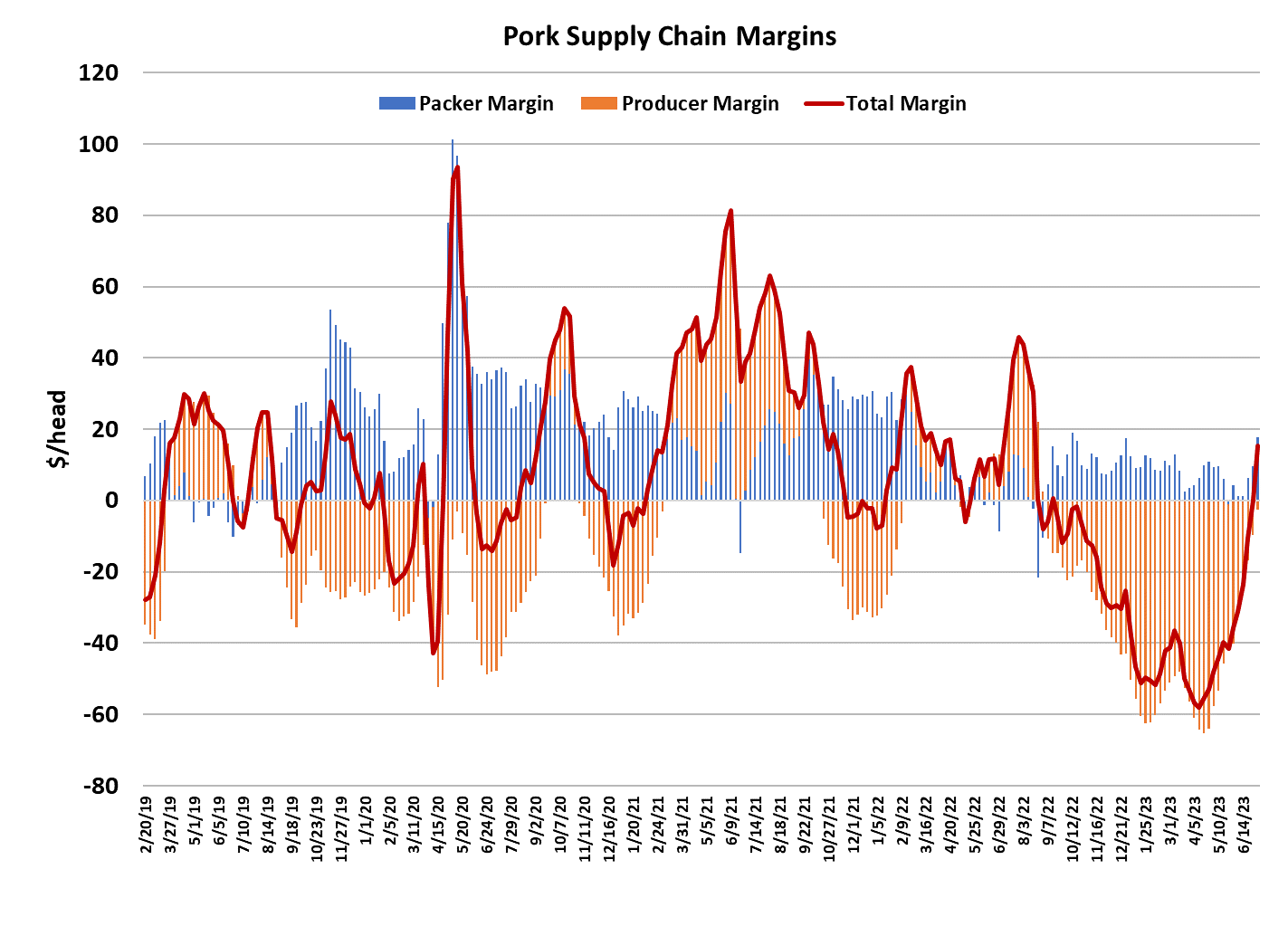

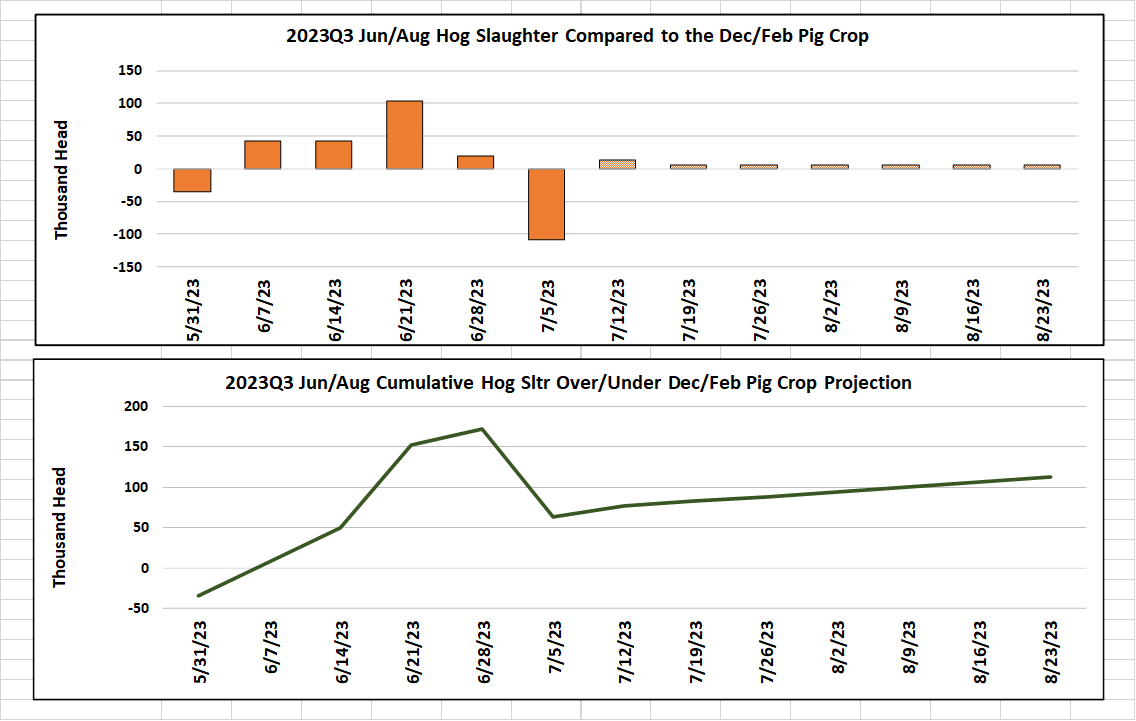

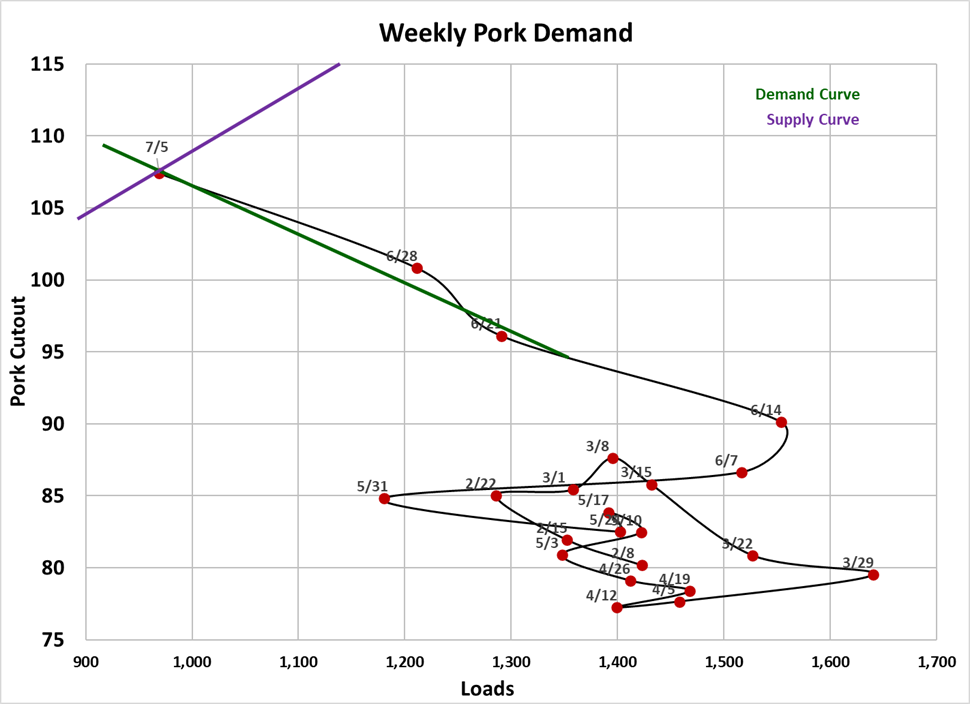

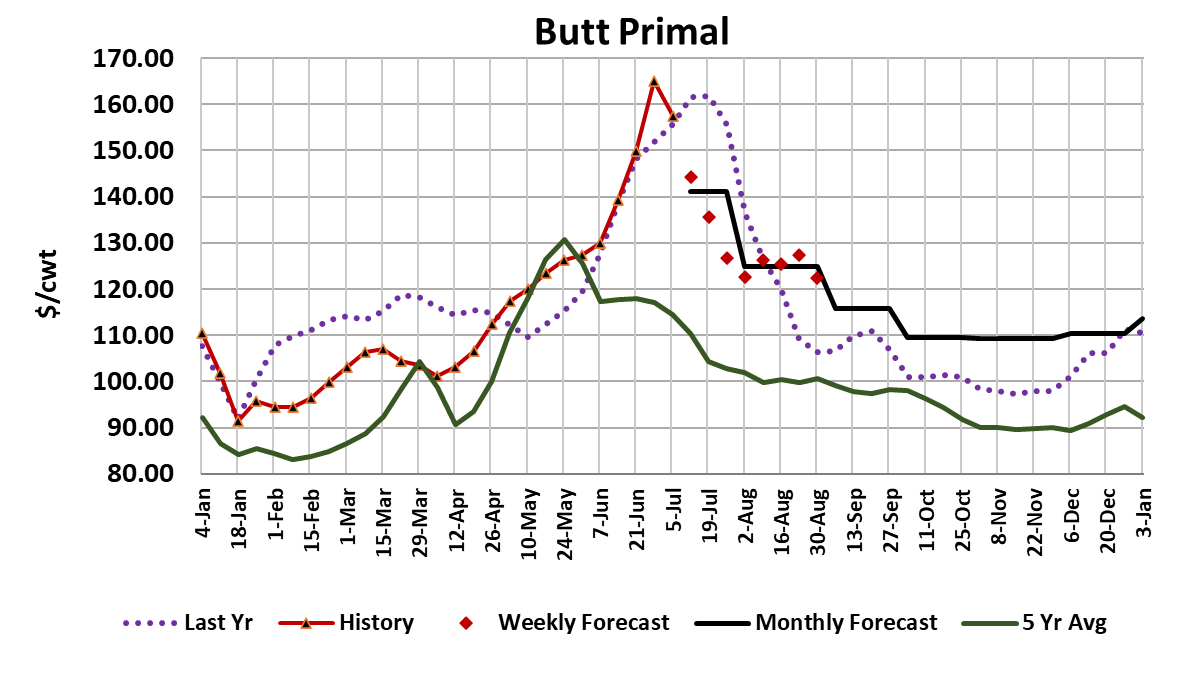

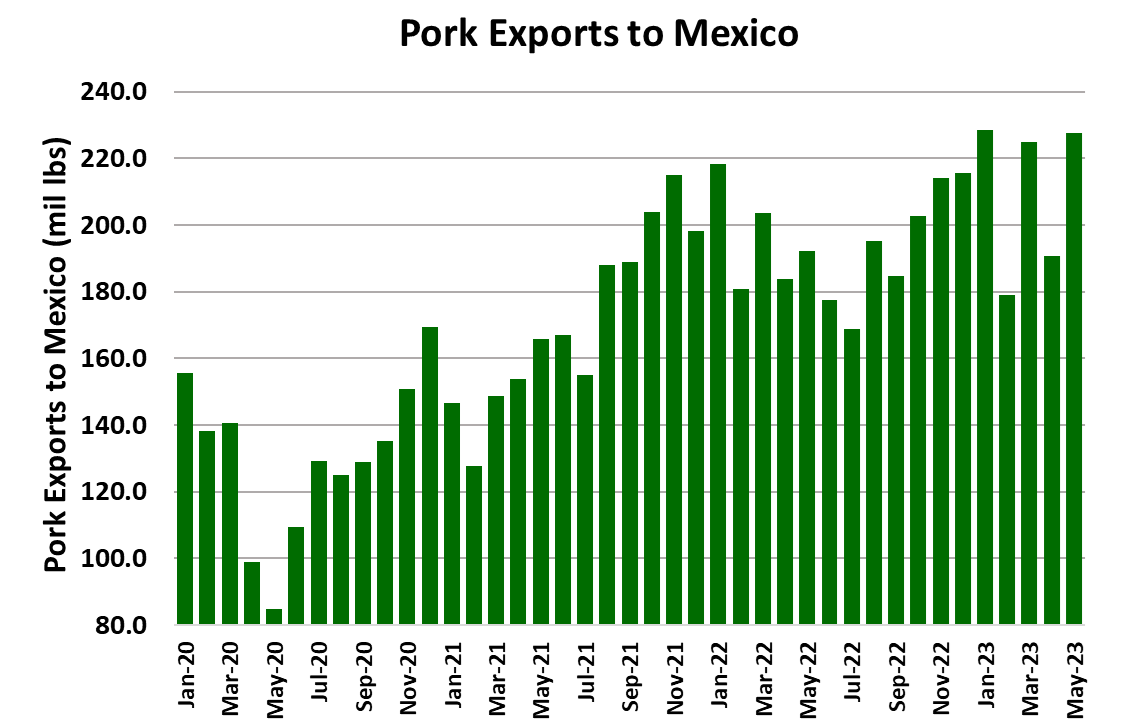

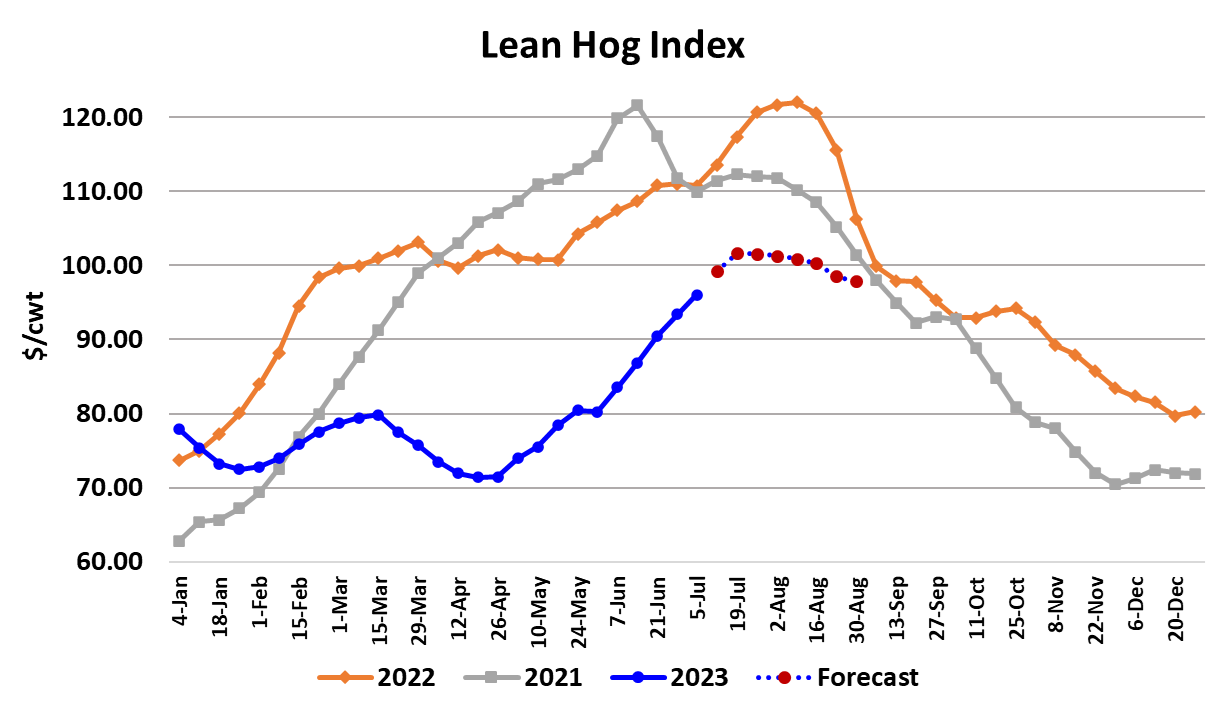

Price levels continued to march higher in the hog and pork complex this week. The cutout added $6.58/cwt. on a weekly average basis and as of Friday afternoon was just a whisker away from $108. This is really starting to look like the kind of summer market that we have all grown accustomed to. Triple digit cutouts and even a few triple digit negotiated hog prices were registered this week. The WCB negotiated market was $4.32 higher on a weekly average basis and printed over $100 briefly on Thursday. It is amazing what can happen when the hams and bellies simultaneously strengthen. The bellies, in particular, have really come to life. The belly primal printed over $143 on Friday afternoon and last Friday it finished at $111. Of course, some of that move is likely related to the short production week due to the holiday, but I don’t get the feeling that belly prices will back down next week when we get back to full production and they could have a lot further to run. Keep in mind that last July and August, the belly primal spent several weeks over the $200 level. I’m not forecasting that yet, but wouldn’t rule it out. Often when price levels have been very low for a very long time and they finally wake up, the move higher will be impressive. The weekly export data showed strong movement to Mexico and that is probably helping to support domestic ham prices. 23/27 hams printed just under $100/cwt. on Friday afternoon. Last summer those went over $120. The trim markets have also seen strong gains recently. Suddenly, it seems, the processing sector is ready to roll and needing raw materials. The retail primals were mixed this week, with the loins posting further gains while the butts moved lower. It isn’t unusual for butts to peak and turn lower at this time of year and I suspect that further declines are coming in the next few weeks, but that might not be enough to offset the price strength in the processing items. The combined margin continued its epic upswing this week, now approaching +$20/cwt. and reaching levels that were considered normal before the awful downdraft that hit the market this spring. It has been a long road back to normal, but it doesn’t appear to be too far off at the moment. But before we read too much into the cutout rocking up to $108, it is important to consider that part of that move might be more related to shrinking pork supplies rather and any huge improvement in demand. The attached scatter plots the weekly average cutout vs. negotiated load counts. By this measure it looks like the demand curve has been almost stationary since the week of June 14 and thus the improvement in price has been mostly due to smaller and smaller amounts of pork trading in the negotiated market. If that is the case, will the cutout move back down the demand curve when production increases next week after this holiday-shortened week? Possibly, but we could also see the demand curve shift. It is pretty rare for demand to stay so stable for so long. My sense is that it is more likely to move rightward than leftward (i.e., improving demand), but time will tell on that. This week’s slaughter was tiny at 1.95 million head, smaller than what I had dialed in. Packers could have done a much larger Saturday than the 154k that was reported, but they didn’t. That tells me that the supply of hogs is pretty tight right now. Carcass weights are also telling the same story. It is notable that this is the first week in quite a while where the slaughter level was actually below what the pig crop implied by a significant amount. Through the balance of July, expect weekly kills to be sideways around 2.3 million head per week before they begin to increase seasonally in August. The pork industry is getting some help from export markets also. The monthly ERS export data was released today and it showed a 12.7% YOY increase during the month of May. I wouldn’t be surprised to see several more months of YOY increases in exports. As mentioned above, Mexico has been key to boosting export volumes and ham prices. The sharp increase in the cutout really boosted packer margins this week. I calculate them at nearly $18/head. That is unheard of during July. Look for producers to grab some of that margin next week through higher hog prices. Packers will need to remain disciplined and not try to push the kill too hard in the next few weeks, as tempting as that might be. The DTDS weights were lower again this week and are simply screaming that the hog pipeline is very current. I’ve noticed that sow slaughter has been a bit elevated in recent weeks and that might be pointing to some breeding herd liquidation that will show up in the next Hogs and Pigs report. That helps makes the case for most of the deferred futures being too low presently. Next week, watch the bellies, hams, and trim to see if they can maintain their upward momentum as production levels return to normal. Also, it is reasonable to expect cash hog prices to advance as packers will need to work a little harder to flesh out their slaughter schedules. With the Lean Hog Index currently sitting at $97.43, it won’t take much to push it into triple digits just in time for the July expiration a week from Monday. Ah yes, it really is starting to feel like summer in the hog and pork complex.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}