Pork Wrap July 5

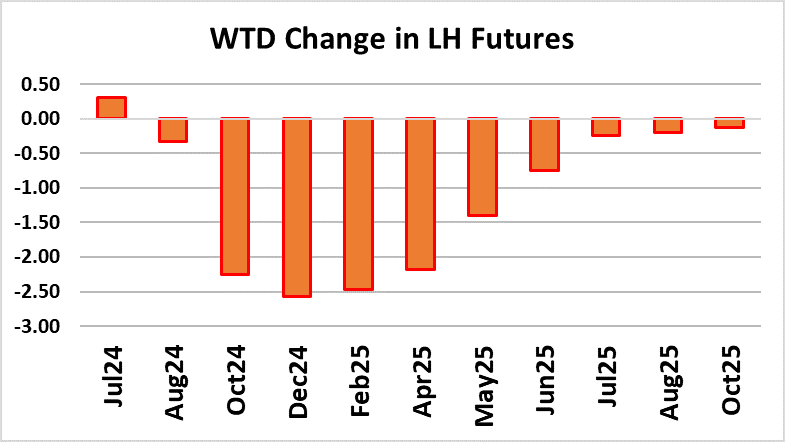

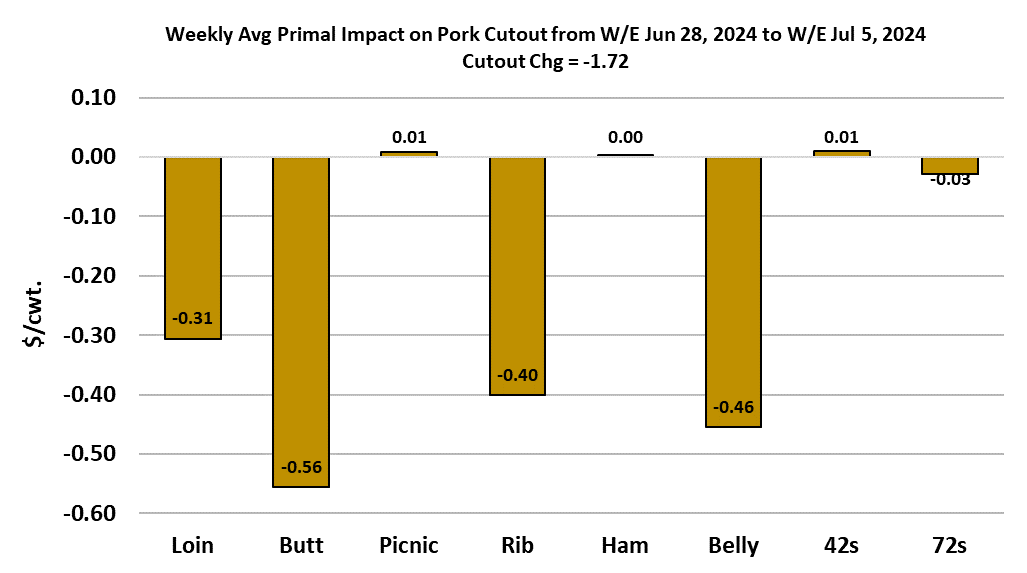

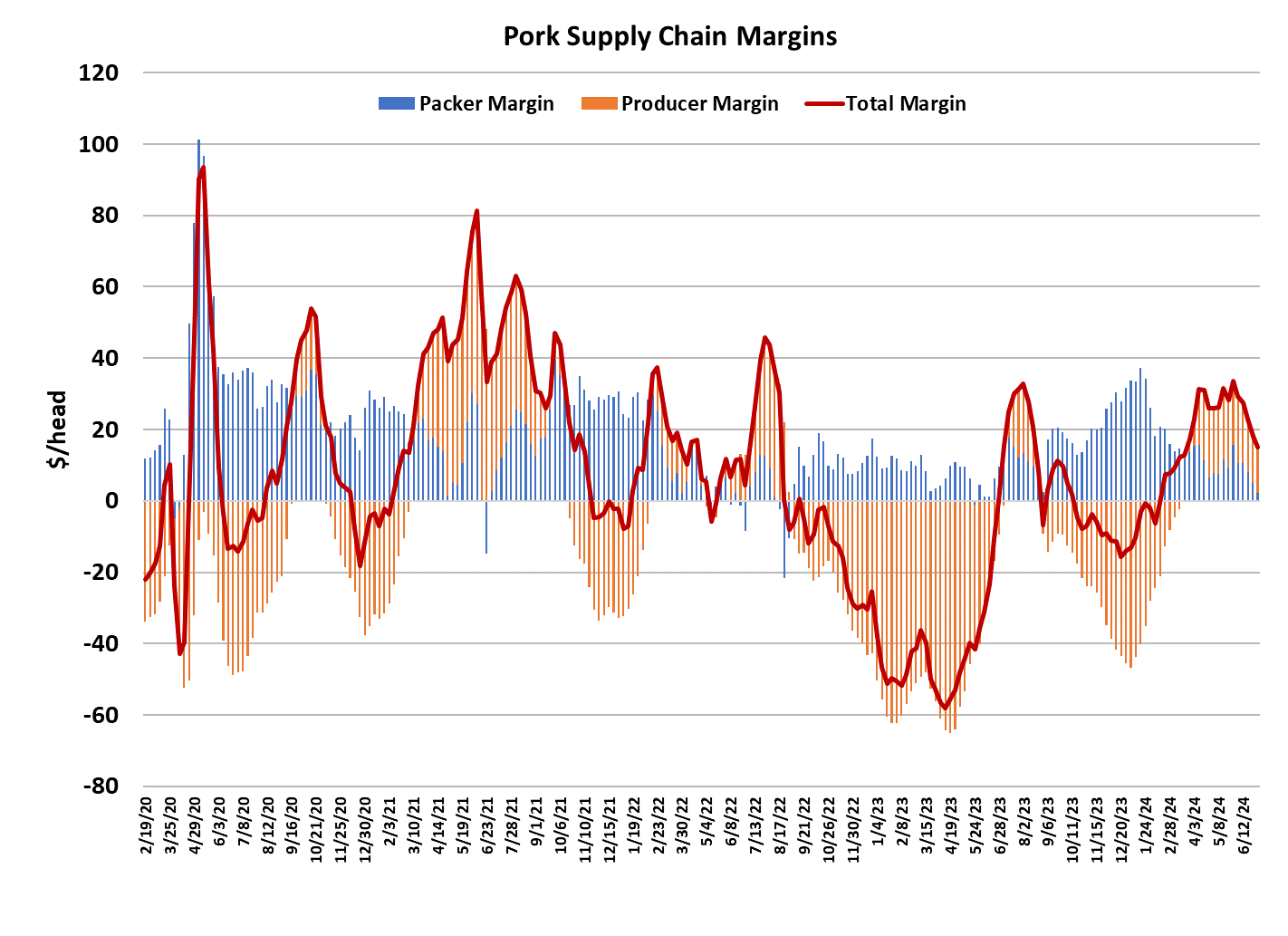

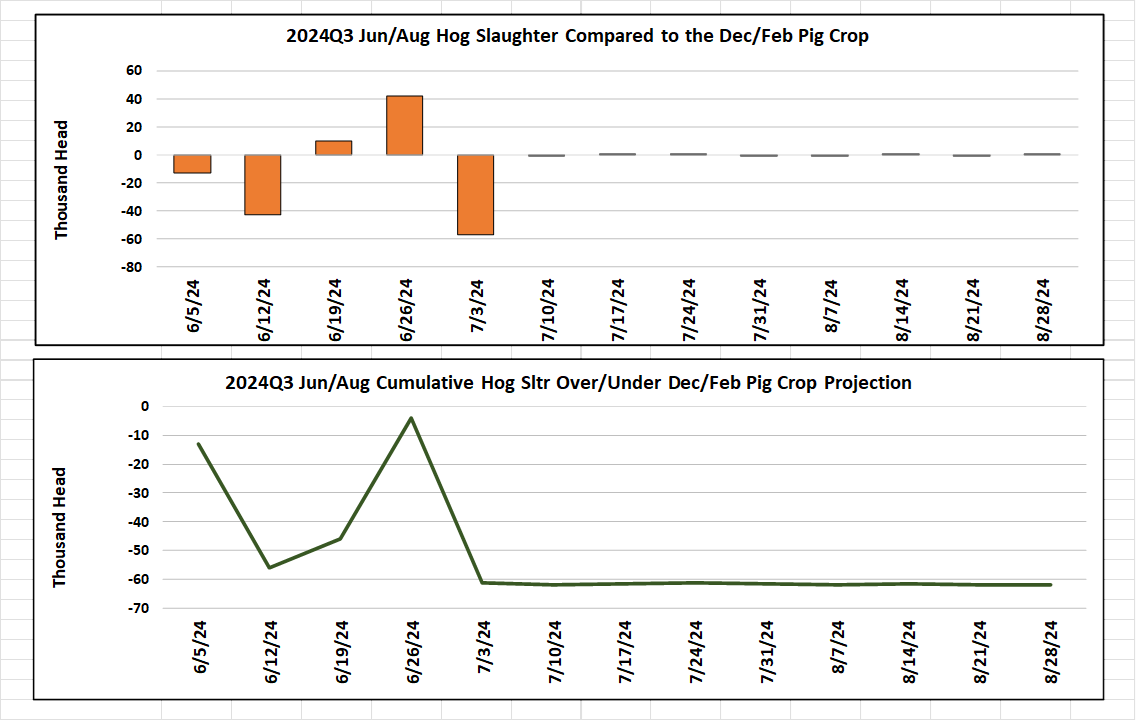

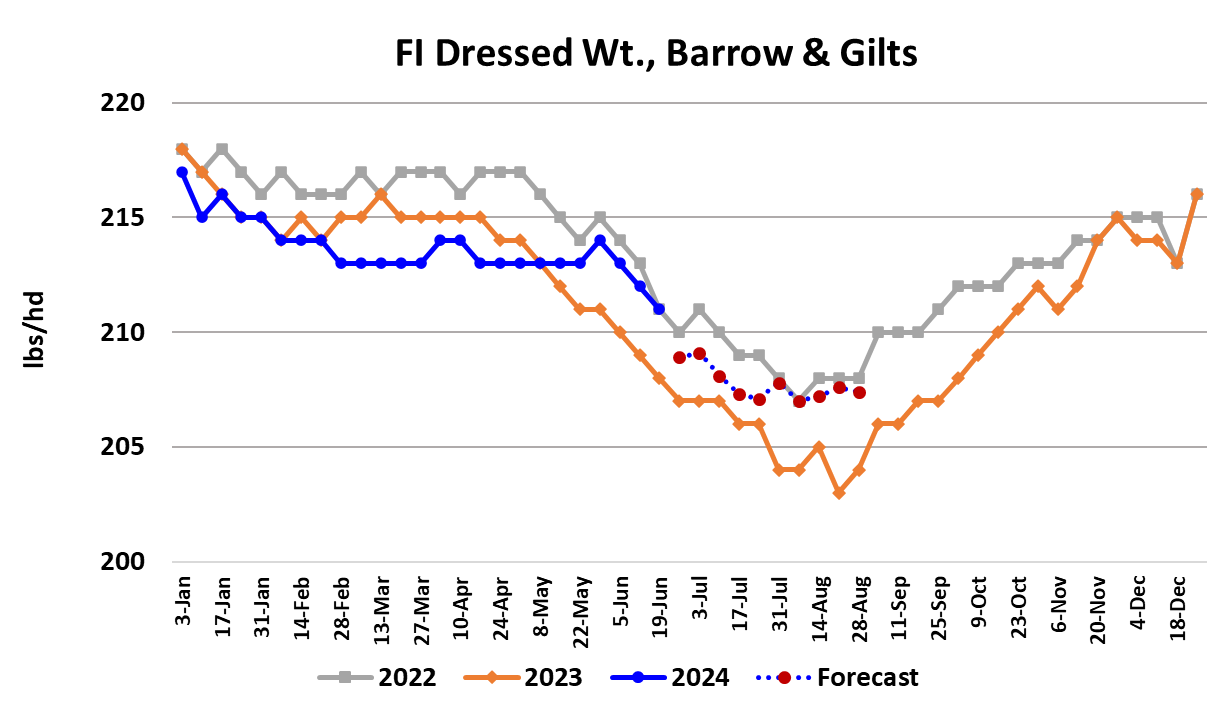

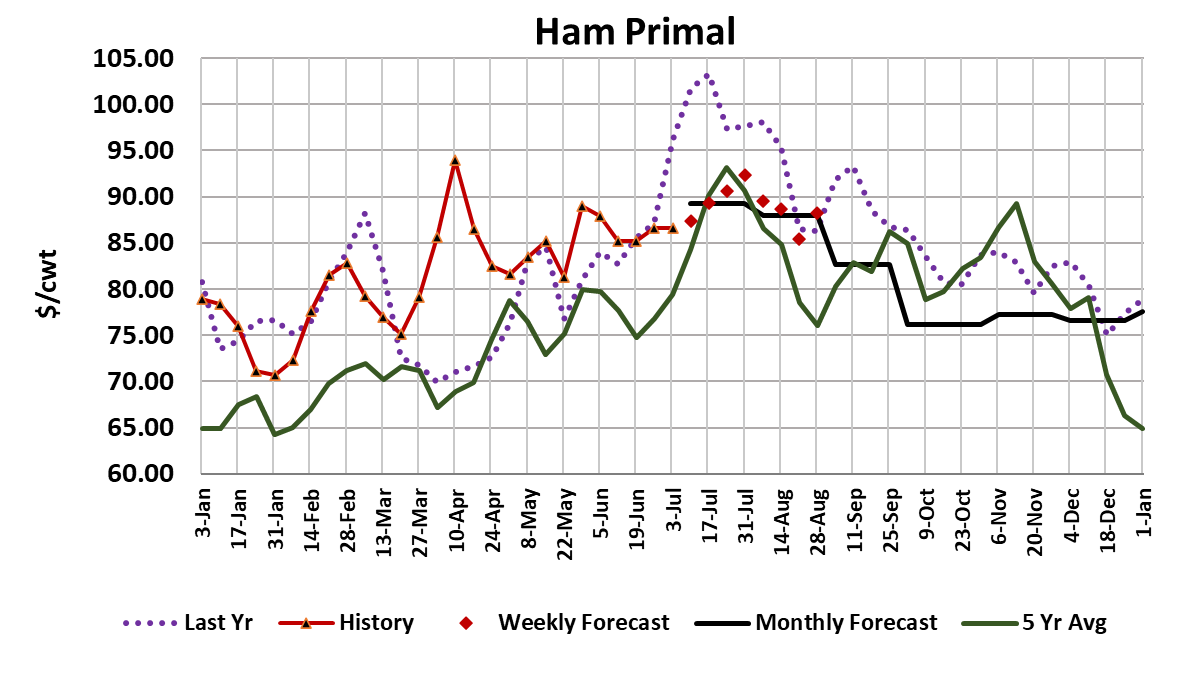

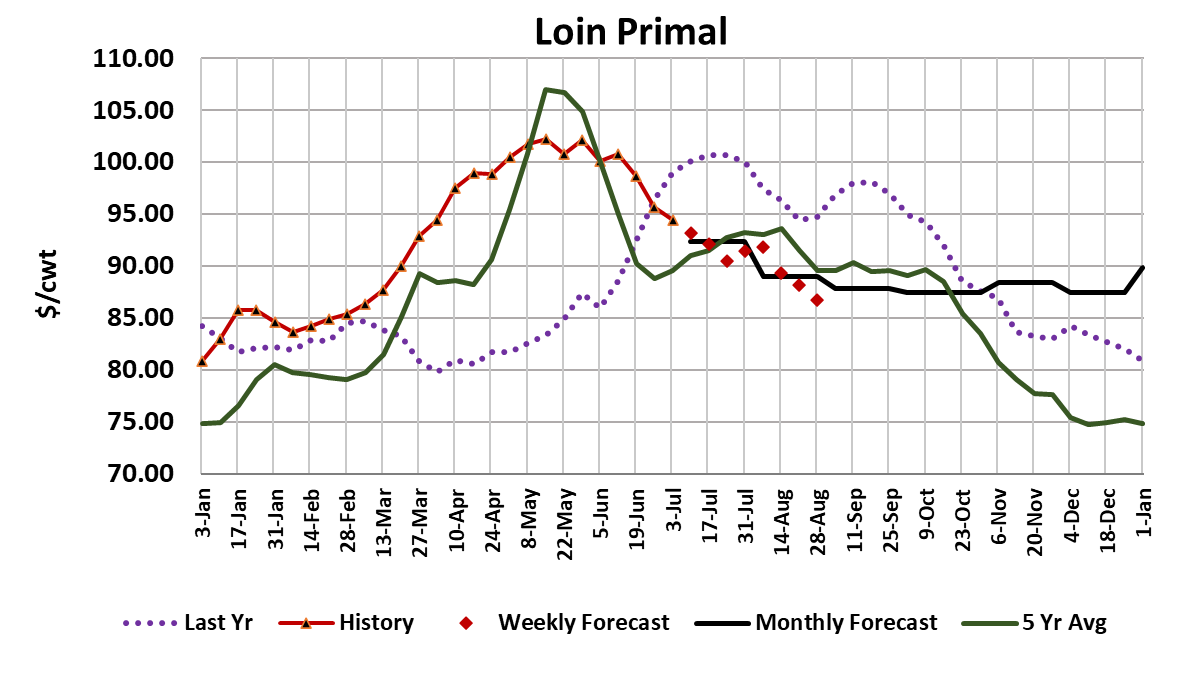

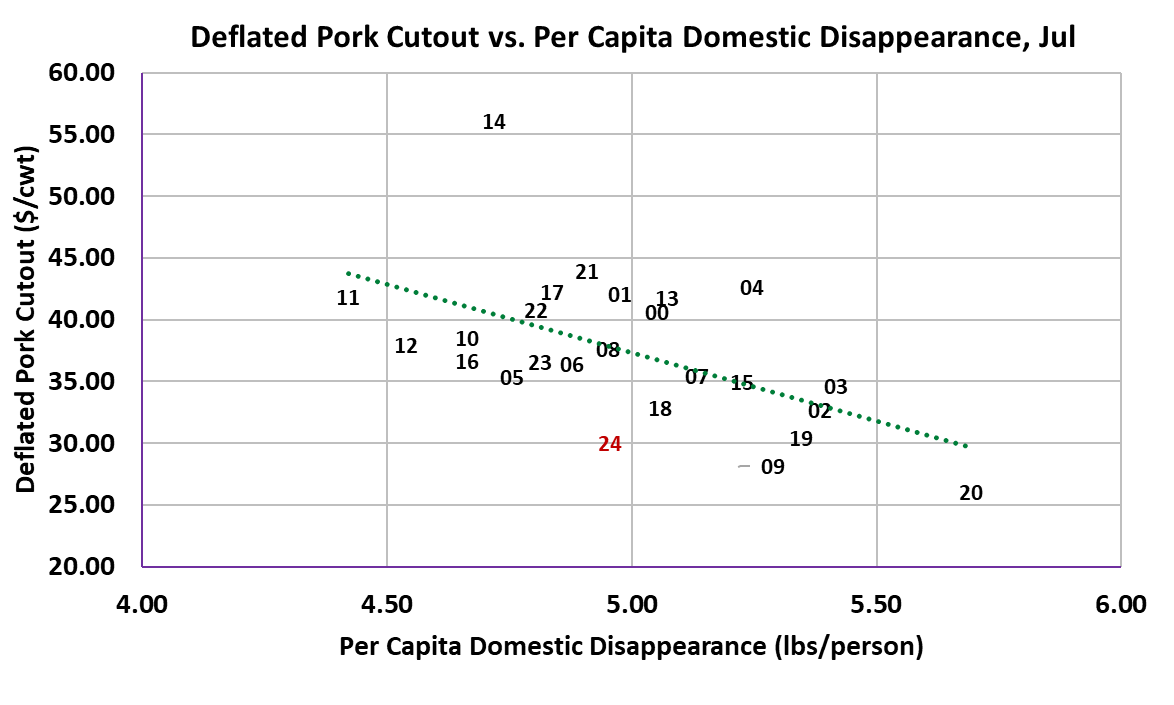

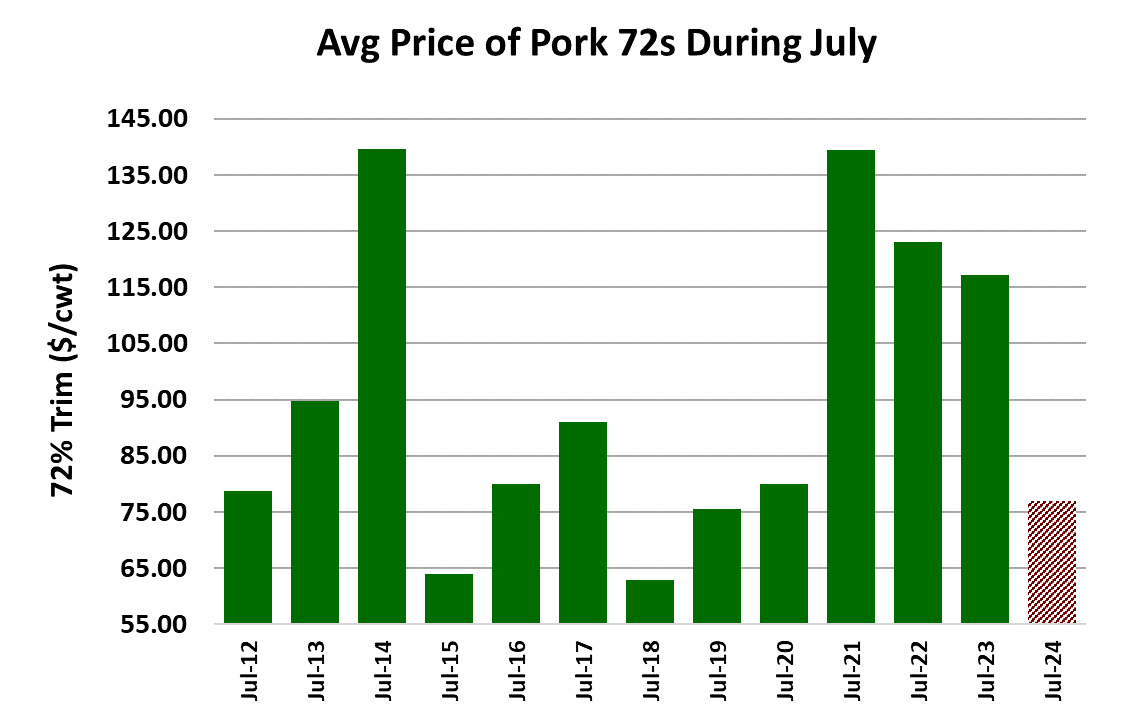

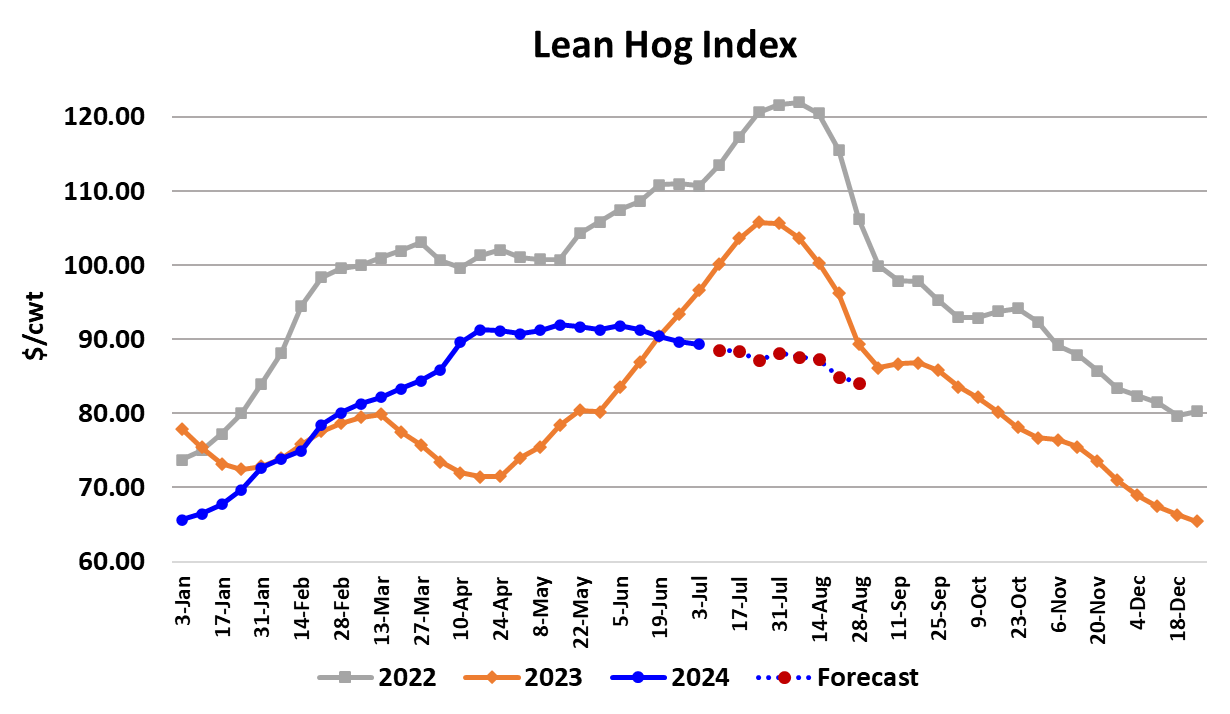

Pork packing margins continued to compress this week as the cutout dropped while negotiated hog prices were a little higher. The cutout lost $1.72/cwt. on a weekly average basis on its way to $94.57. That was the first sub-$95 weekly average since the end of March. The NDD negotiated market averaged $1.66 higher at $90.20. The negotiated hog market is now a tad bit over the LHI and just a few dollars under the cutout. Packer margins fell to $2.29/head, down about $2.50 from the week before. Margins should be very close to their low point for the year because hog supplies are near their low point for the year. This week’s kill clocked in at 2.05 million head due to the holiday, but should bounce back to 2.4 million or better next week. So far, it looks like kills are tracking the Dec/Feb pig crop estimate fairly well—the cumulative error through the first five weeks of the Jun/Aug quarter is running close to -60k, which suggests that USDA might have slightly over-estimated the Dec/Feb pig crop. In any case, a 60k error isn’t enough to cause any concern. If kills continue to track closely with the pig crop then we should expect 2.4 million per week through July and then kills start moving toward 2.55 million head at the end of August. The demand structure of the market doesn’t seem prepared to handle bigger kills without some further price concession. Carcass weights are finally moving lower seasonally, with this week’s FI barrow and gilt weights coming in at 211pounds, a one-pound drop from the week before. Weights should continue to ease lower until about mid-August. There has been a lot of heat across the country this summer, but none of it seems to be focused on the hog producing regions in the Midwest. That has kept the decline in weights orderly and probably means that they will remain above last year through the balance of summer unless a significant heat wave develops in the producing regions. This week it was the loins, butts, ribs and bellies that exerted pressure on the cutout, but none of the other primals exerted much in the way of counterbalancing strength. Ham prices have been mostly sideways over the past three weeks, but the forecast still has them working a little higher towards a top in late July. Bellies have been easing lower since early June, but it still seems like a risk to expect that trend to continue. As a result, I’m forecasting very gentle increases in belly pricing over the next few weeks. Loins, however, are being forecast lower with that primal not expected to find much support until the $85-90 range. The combined margin continued lower this week, but it is still in positive territory. It is rare for the combined margin to bottom before it slips below the zero line, so that makes me think that this demand downcycle still has a good ways to go. That it ominous for the Aug futures, which are currently doing their best to stay par with the July, but the odds of the LHI holding flat from July to Aug seem rather low at this point. This week, futures traders finally punished the fall and early winter contracts after failing to do so in the wake of last week’s moderately bearish H&P report. Oct24 through Apr25 were all down more than $2 on the week while the front of the curve was mostly steady. This is the first time in four years that the cutout has been below $100 on Independence Day. If we adjust for inflation, it looks like the cutout this July will be the lowest since 2009, not counting the pandemic year of 2020. Fortunately for producers, sharp declines in the corn market have lowered their cost of production considerably and so they are still eeking out a small profit even though demand is weak and prices are low. However, when hog supplies expand seasonally this fall and winter that small positive margin will likely evaporate quickly and we could very well see yet another year where producers lose money on average. Perhaps that will spur the further reductions in the breeding herd that will be necessary to foster a return to profitability for producers. On a more positive note, the weekly export data released this morning showed large sales to Mexican buyers last week, so that may give the ham market some support over the next few weeks. It seems this market is quickly becoming a “show me” market, where traders need to see sustained evidence of better demand before they are willing to stick their necks out on the long side very far into the future. Next week, look for some further easing in the cutout as production ramps back up after the holiday. Cash hog markets are likely to be steady to perhaps a little higher.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}