Pork Wrap July 30

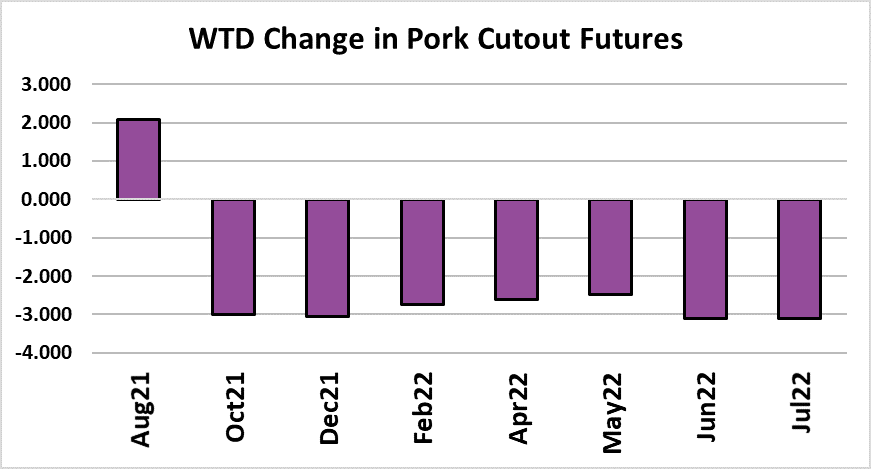

The pork cutout added a little over $2 this week, but the cash hog

markets remained on the defensive. The WCB negotiated market

declined about $3 on a weekly average basis. With the negotiated

market moving lower and the cutout moving higher, the LHI stayed

essentially flat on the week. In fact, the LHI is at nearly the same

level it was when the July contract expired over two weeks ago

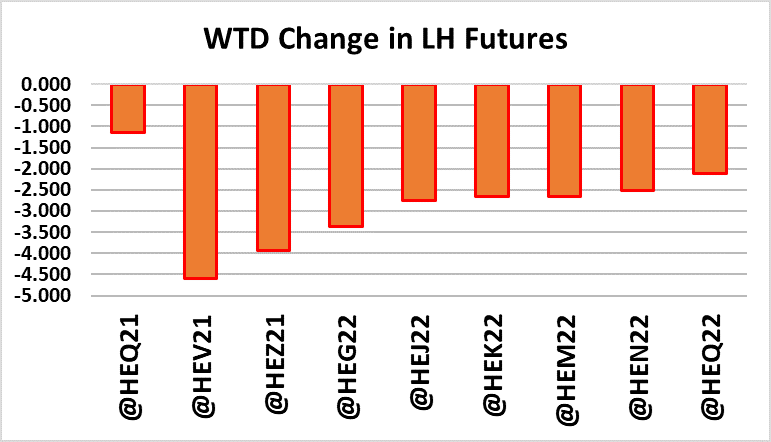

($112). That didn’t stop the futures from selling off this week, with

the Oct contract losing over $4.50.

Traders are likely becoming more pessimistic about the export

prospects for this fall since the recent weekly export data hasn’t

looked all that good. In addition, there may be concern that hog

supplies this fall will test packing capacity, which has been limited

by labor shortages. But while the futures market was becoming

more bearish, I was becoming more bullish. I was forced into a

major forecast revision this week because the strength in the

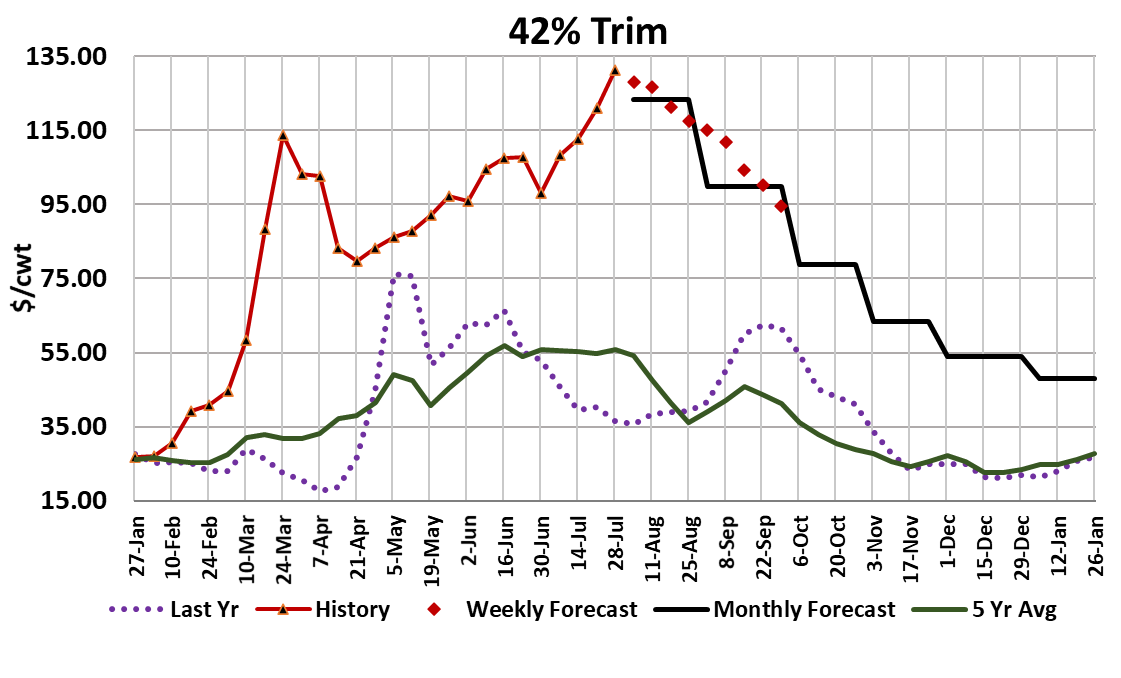

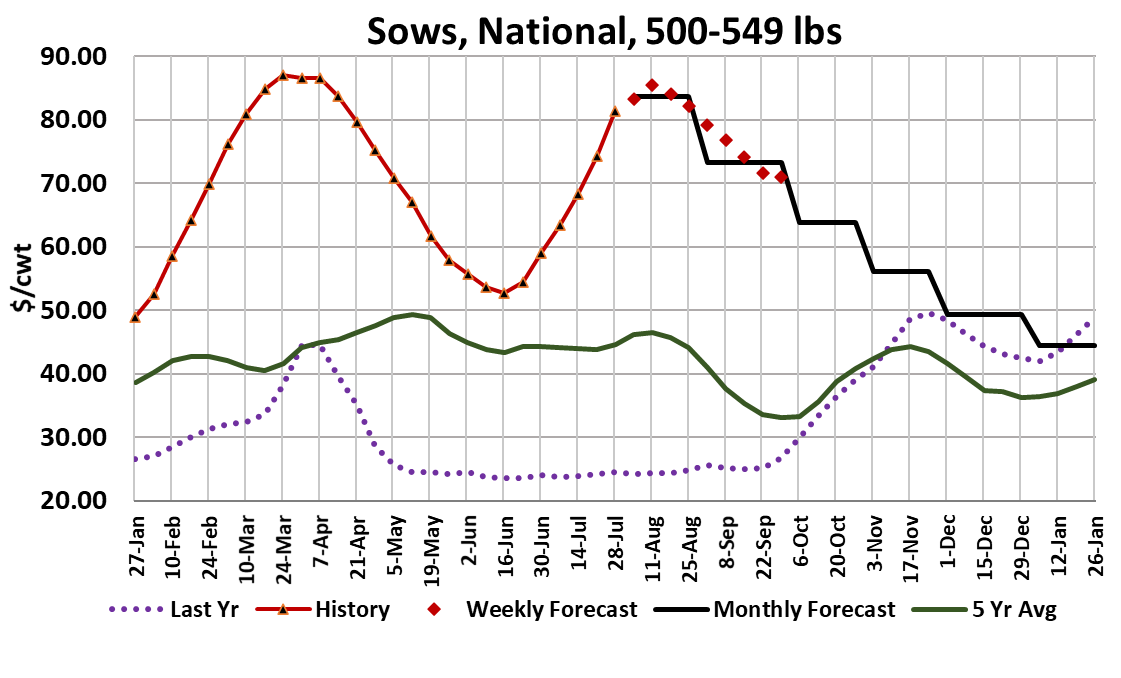

cutout has not abated as quickly as I anticipated. Trim markets are

on fire and sow prices are heading higher rapidly. I pushed the

price forecast for nearly all of the primals higher over the next

several months. That, in combination with the futures selloff,

helped to remove a lot of the mis-pricing from the fall and winter

contracts. I’m also now showing Aug as under-priced given that

the index hasn’t moved in two weeks and the contract only has 10

more trading days until expiration.

At today’s close, the Aug contract is nearly $6 under the LHI and

that gap seems excessively wide for a market where the index

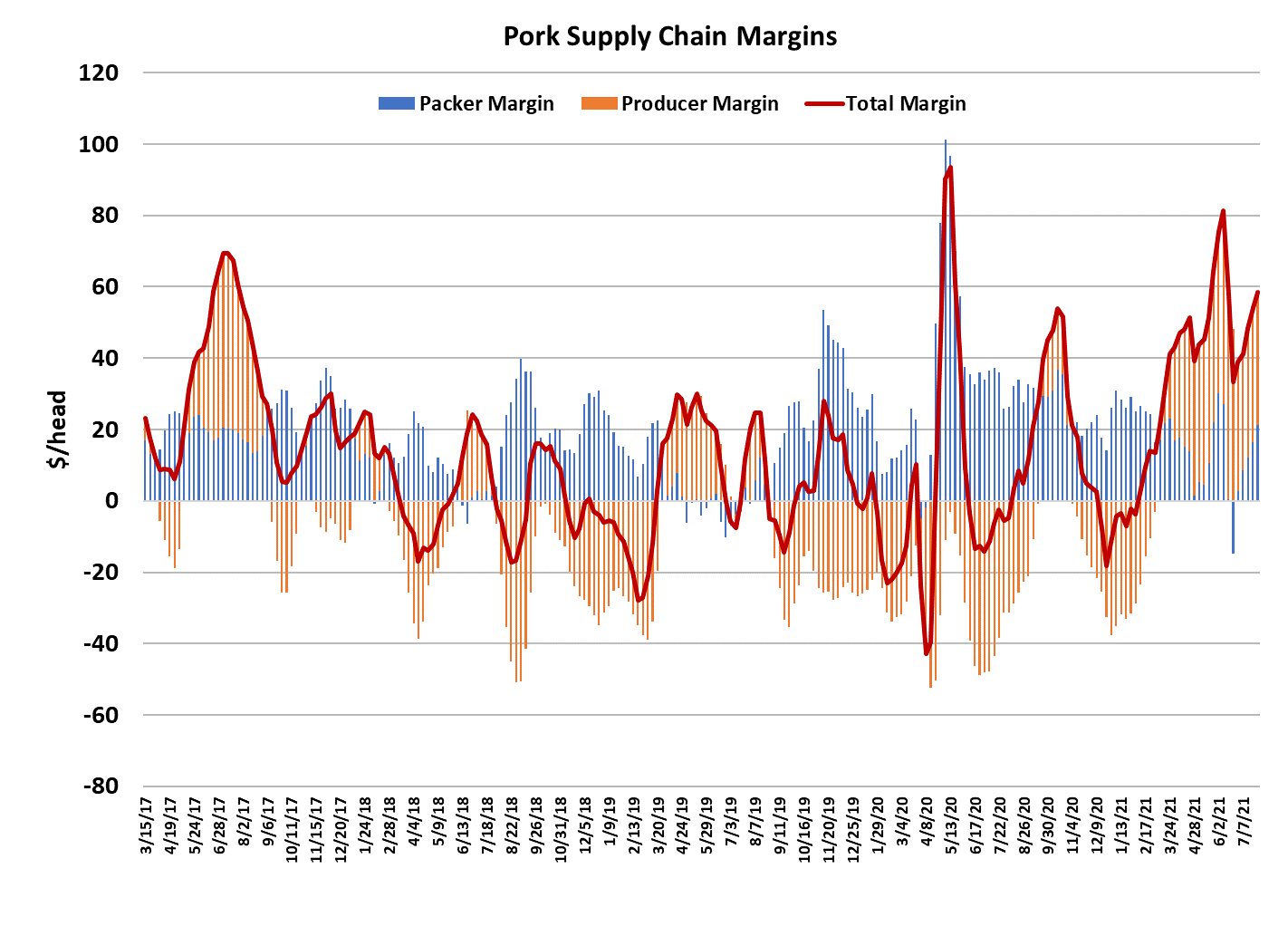

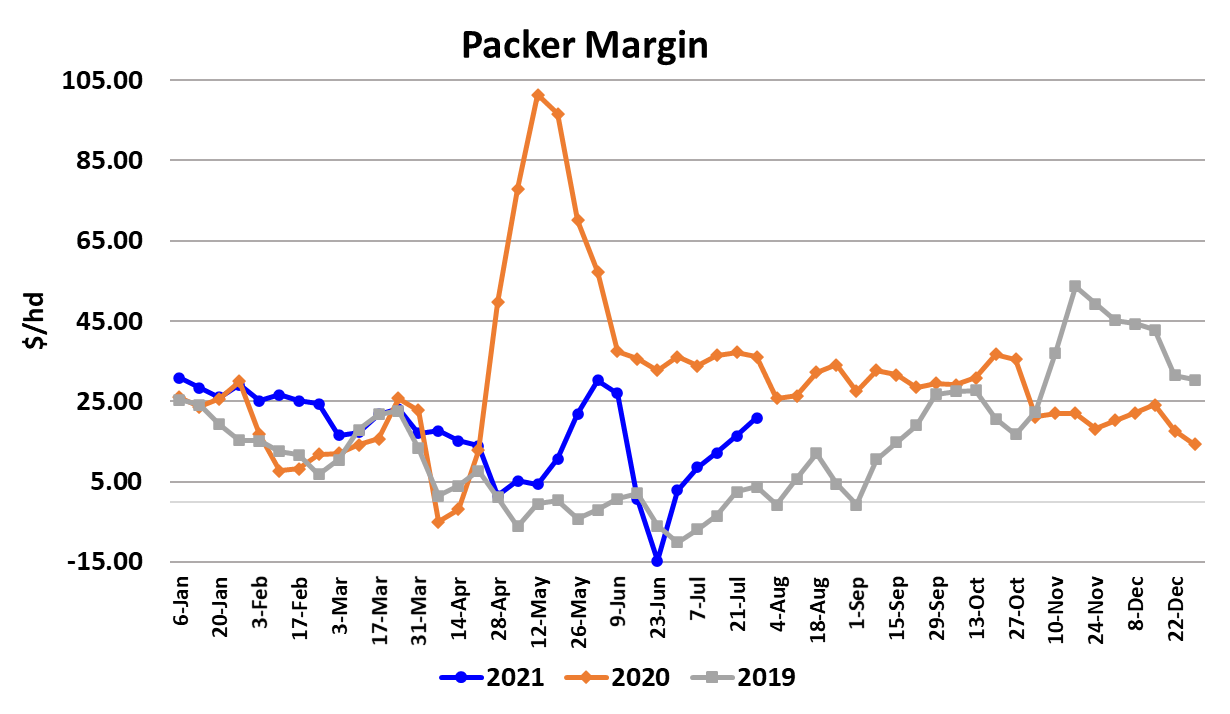

hasn’t shown much movement. Pork demand seems to be back on

the rise, as indicated by the combined margin chart below. I

thought that perhaps the combined margin was giving us a head

fake by moving higher a few weeks back, but now it is hard to deny

that an uptrend is back in place. At the same time, hog supplies

have been slow to expand after reaching a bottom around

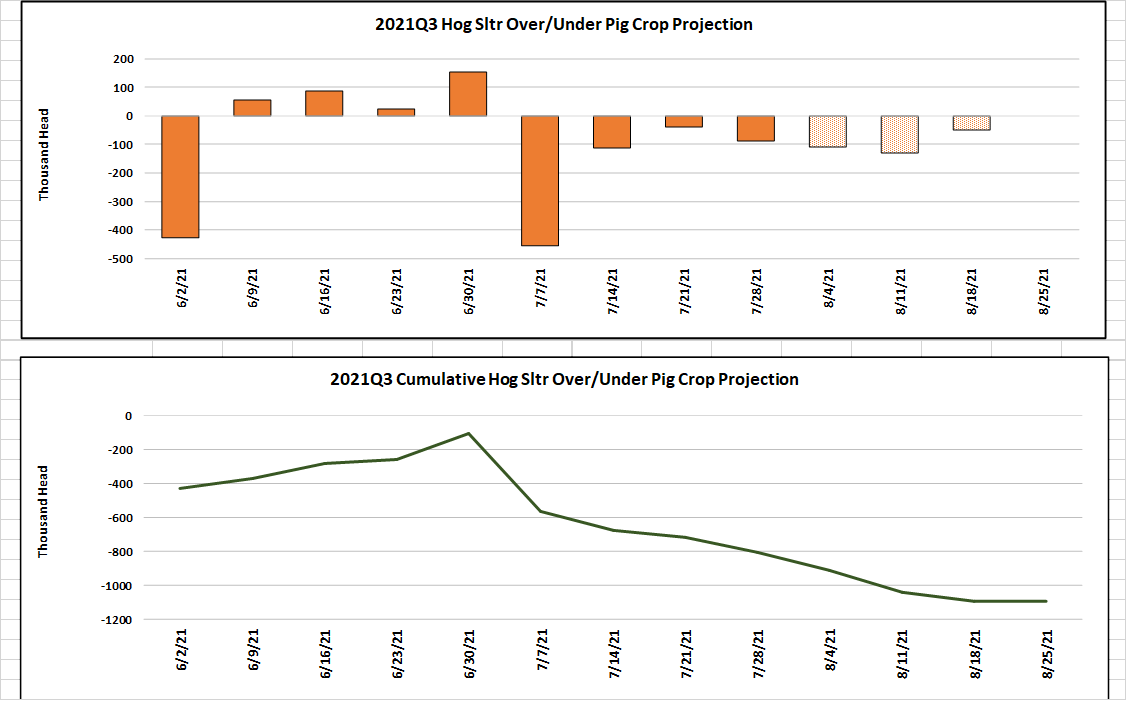

Independence Day. This week’s kill was estimated at 2.33 million

head, essentially unchanged from the week before. That was less

than the pig crop projected and the chart below shows that with

four weeks to go in the quarter, the cumulative under-kill of the pig

crop has amounted to around 800k head. If these under-kills

continue, we will likely experience a total shortfall of about 1.1

million head for the quarter. You would think that with actual hog

supplies tighter than expected during the summer, that hog prices

would be rising and packer margins would be tight. Instead, the

opposite is true.

Packer margins this week came in at close to $21/head, a $5

increase from last week and a really hefty margin for this time

of year. Packers are simply not interested in pressing the kill

higher and that probably has something to do with the tight

labor situation. So, it is like they are in margin management

mode without having any actual margin problem. So far, the

carcass weight data isn’t indicating any significant back up of

hogs in the system and in fact the DTDS weights are near all-time lows.

I expect that packers won’t let the margin get much bigger

without sharing some of it with producers and so if the cutout

continues to strengthen, I think it increases the chances that

negotiated hog markets stop declining. I’m not looking for a lot

more strength in the cutout from current levels, but I could be

wrong about that. The belly primal made another all-time high

this week and 42s averaged an astounding $131. The small

kill this week could support the cutout again next week.

Looking further out, it does worry me that USDA seems to have

missed the current pig crop so badly and raises the possibility

that they also underestimated the Mar/May pig crop, which we

will begin killing in September. The government told us that

the Mar/May pig crop was down 3.1%, so if they were too high

on that we might be looking at something closer to a 5% YOY

decline in hog availability this fall. If that is the case then we

won’t likely see the type of price decline that normally happens

in the fall.

I’m still rating the Oct and Dec contracts as too high, but that is

probably not the case if it turns out the Mar/May pig crop was

underestimated. On the demand side, if the current COVID

wave intensifies in the fall, it will likely cause a resurgence in

stay-at-home behaviors and we already know from experience

that is strongly positive for red meat demand. So the perfect

storm this fall would be for COVID to surge and the pig crop to

be smaller than expected. Next week, watch the negotiated

hog markets for signs that they are slowing their descent or

even bottoming.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}