Pork Wrap July 29

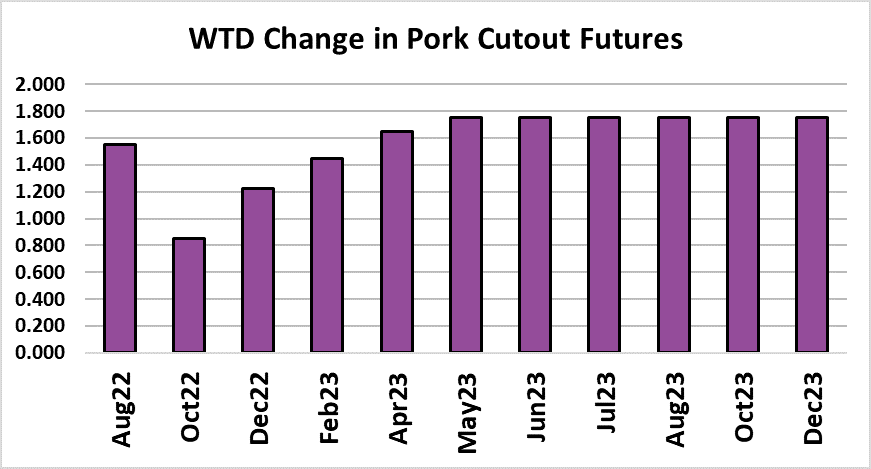

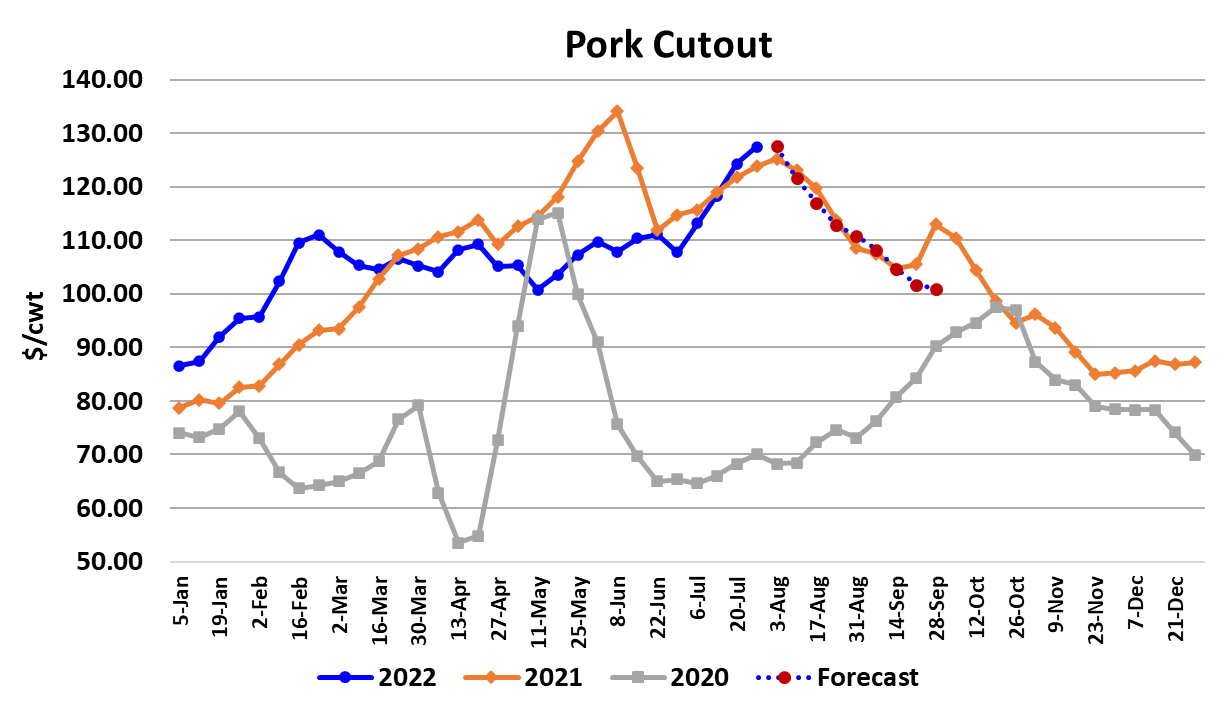

Prices in the hog and pork complex continued higher this

week, with the cutout adding $3.24/cwt on a weekly average

basis and the WCB negotiated market up $1.57/cwt. We are

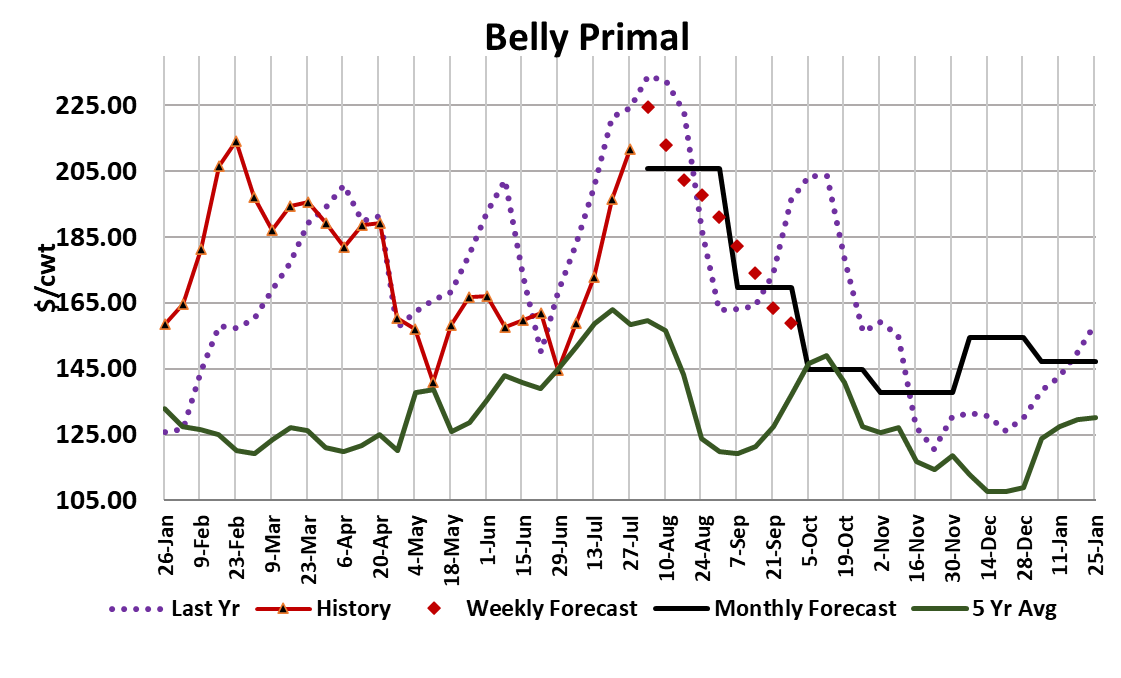

still seeing a strong positive influence on the cutout from the

bellies and hams. The ham primal averaged close to $117/cwt

for the week and that was the highest it has been since 2014

when the PEDv crisis cut hog supplies unexpectedly. Further,

the cutout, which averaged over $127/cwt this week is also at

its highest level since 2014. So, this is a pretty rare market

that we are experiencing right now. Of course, the question on

everyone’s mind is, “how long will it last?” If history is any

guide, it probably won’t last too long.

When prices in the pork complex move to extreme levels and

then top, they tend to fall rapidly and I expect that is what will

happen once the current strength in the hams and bellies has

run its course. It is difficult to know exactly when the top will be

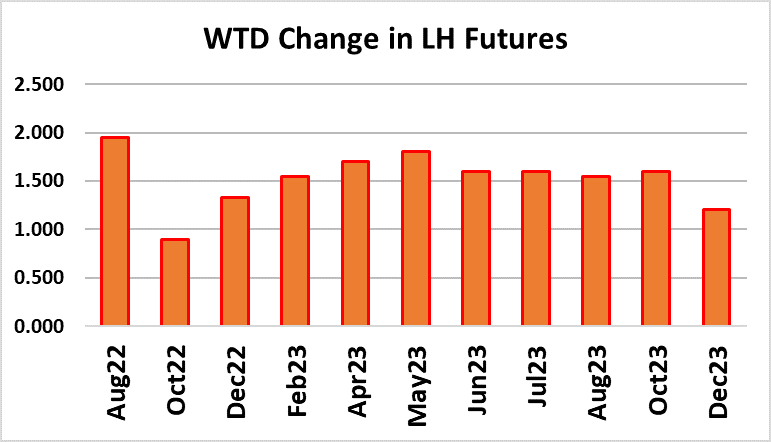

made and that is causing traders in the Aug futures to be

somewhat cautious. That contract only has 10 trading days to

expiration and for those that have positions, it will be very

important whether or not ham and/or belly prices break lower

before or after expiration. Traders did close the gap between

the Aug contract and the LHI this week, but the Index is

projected to print close to $123 early next week and by the

time that happens there will only be seven more trading days

left. And of course, there is always the risk that it will continue

to trend upward beyond the $123 level.

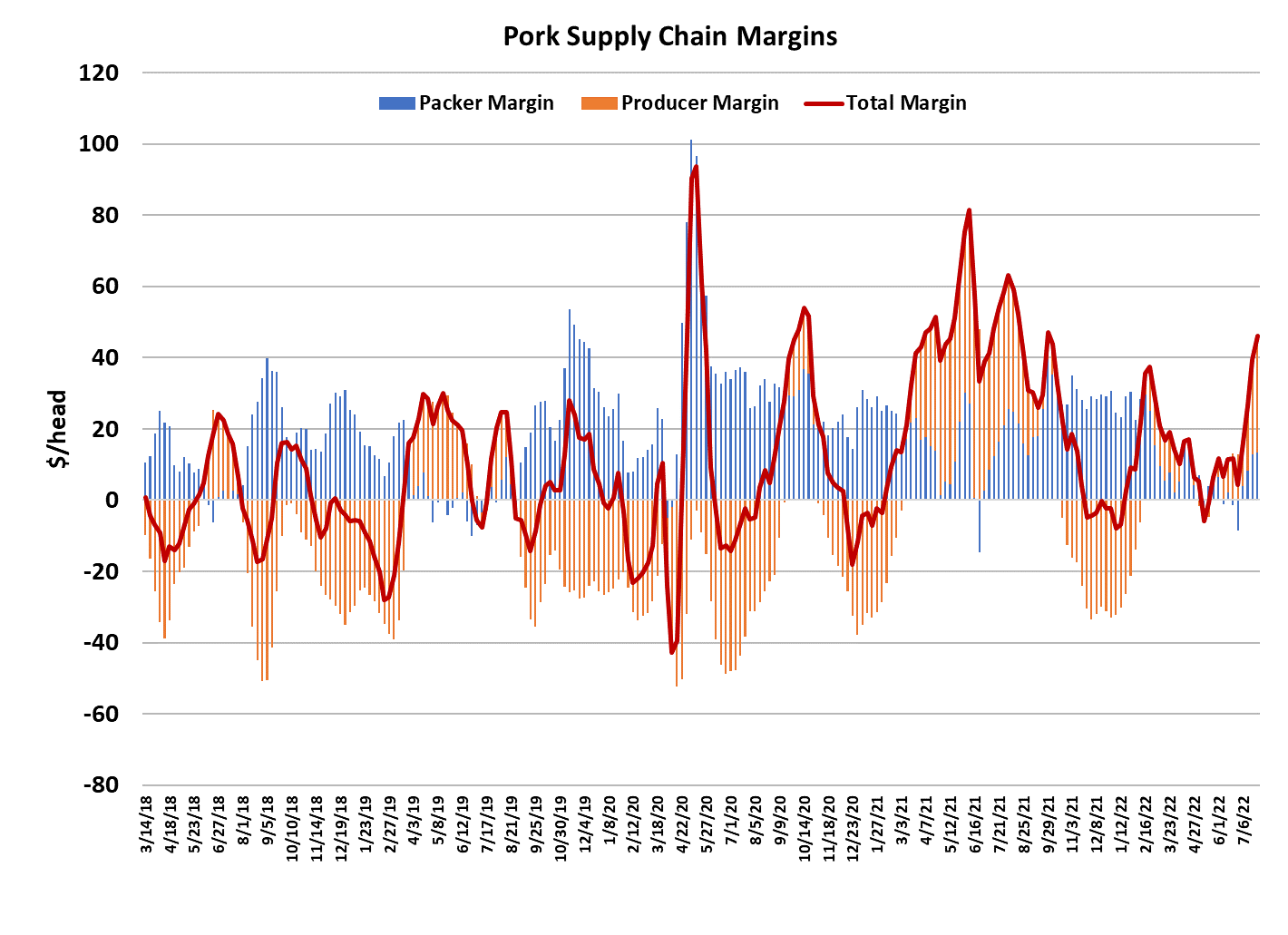

As a result, the hog and pork complex has a level of

excitement and uncertainty that just doesn’t exist in the beef

market right now. The combined margin chart continued on its

steep upward trajectory this week, but it normally doesn’t take

long to reverse course, so just because it moved a lot higher

this week doesn’t mean that it can’t move sharply lower next

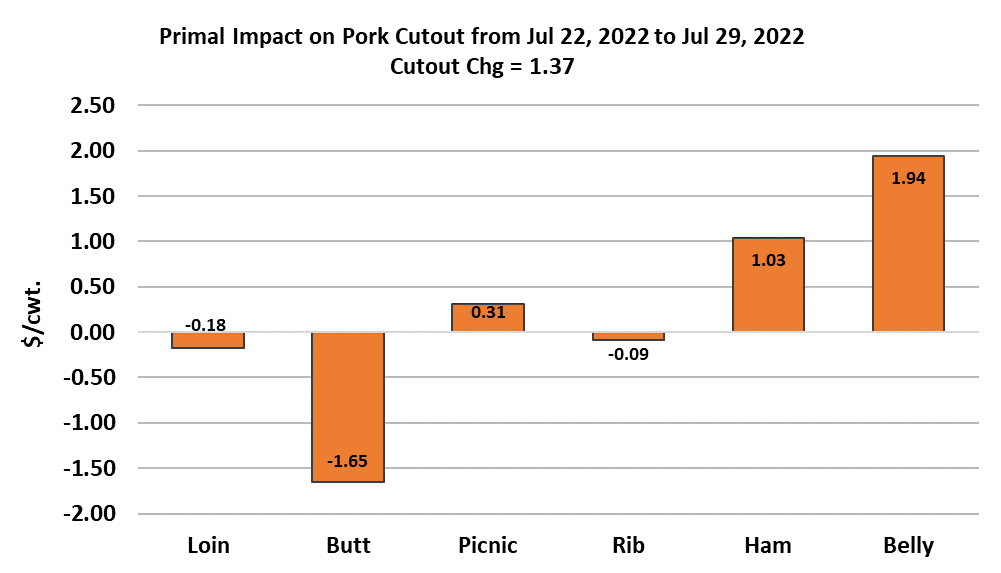

week. It has already gone further than I thought it would. The

retail primals looked a little more shaky this week, with the

butts in particular losing some luster. I don’t think any of the

retail primals are going to exert a lot of downward pressure on

the cutout until after Labor Day, although the butts probably will

continue to leak lower. Trim prices are very, very strong right

now also.

42s averaged almost $125 this week and the 72s averaged close to

$134. Kills are small and that likely contributes to the high price

levels, but I can’t shake the feeling that somehow the high ham price

is also feeding into the price of trimmings. Perhaps there just isn’t

much ham trimming going on domestically right now. Maybe

untrimmed hams are being moved into export channels and that is

keeping the supply of domestic trim tight. My guess is that when we

do see ham prices break lower that will be followed pretty quickly by

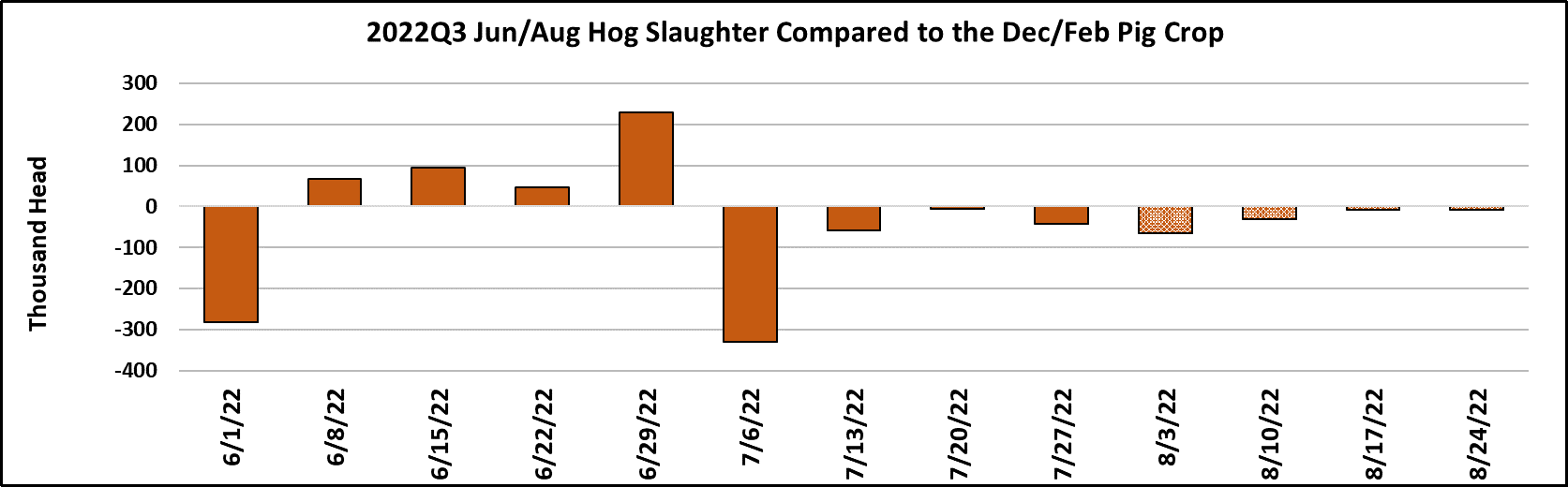

lower trim pricing. This week’s kill registered 2.29 million head, up

only 6,000 from the week before. Next week, we should see the kill

back over 2.3 million head and it will likely be 2.4 million or more by

the end of August.

Carcass weights likely have further to fall before they bottom and the

heat wave that is in the forecast for the Midwest during the first two

weeks of August will likely help that along. The DTDS weights are a

bit on the low side and that may be part of the reason why negotiated

hog prices have been so firm lately. Packers only scheduled 9000

head to be killed on Saturday, so either they can’t find enough hogs

out there or they are attempting to cool off the negotiated market. I

would lean toward the former explanation since margins this week

were calculated over $13/head. That is a pretty robust margin for

August and we need to recognize that it is supported by the small

volumes of hams and bellies that are reported in the negotiated

market each day. If packers have bigger volumes booked at lower

prices then their actual margins would be less than the cash-to-cash

calculation suggests.

I don’t think that the spot hog market will decline substantially until

after the cutout breaks lower. The forecast has margins tightening

up as we move through August, and we could even see some brief

periods of negative margins if the cutout moves down quickly. Export

activity seems to be slowing a bit in response to high domestic pork

prices. There is no evidence yet that China is eager to increase its

purchases of US pork. Next week, the hams and bellies will continue

to be center stage because price changes there will determine the

direction of the cutout and ultimately where the Aug LH futures

expires. It is important to continue to watch the weather also,

because if the Midwestern heat wave turns out to be hotter than

expected that could cause the price strength in the pork complex to

persist longer than currently envisioned.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}