Pork Wrap July 23

The negotiated hog markets were lower this week, with the NDD

market dropping over $3 and the WCB off a little more than $5.

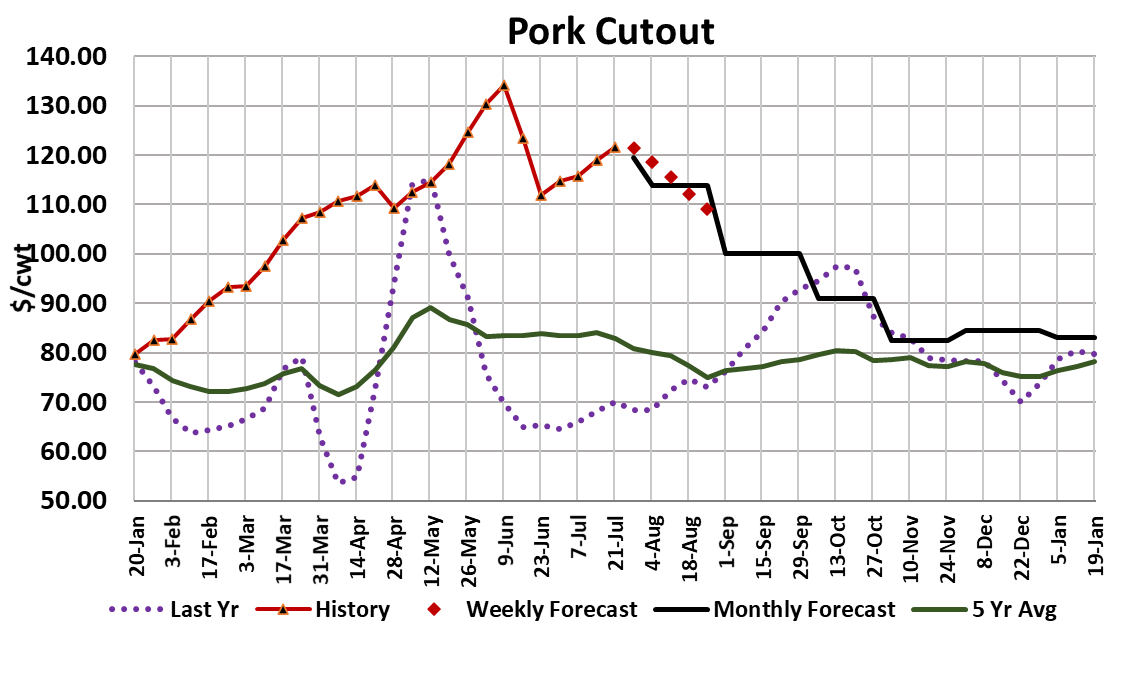

The cutout, meanwhile, added about $2.50 on a weekly average

basis. That helped move packer margins back up to $15/head and

it is beginning to feel like packers are in control again after that

disastrous drop in the cutout and margins back in June. This week

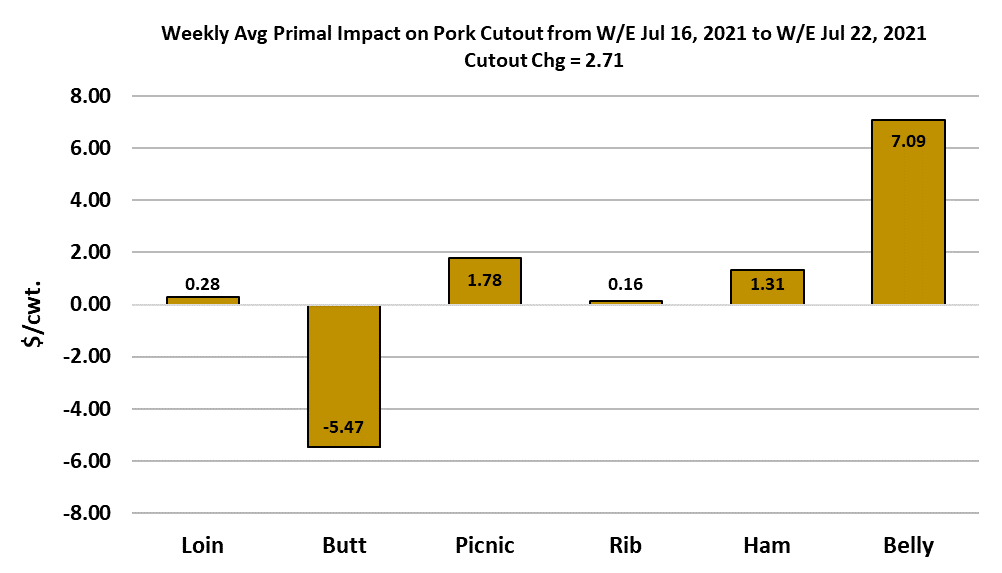

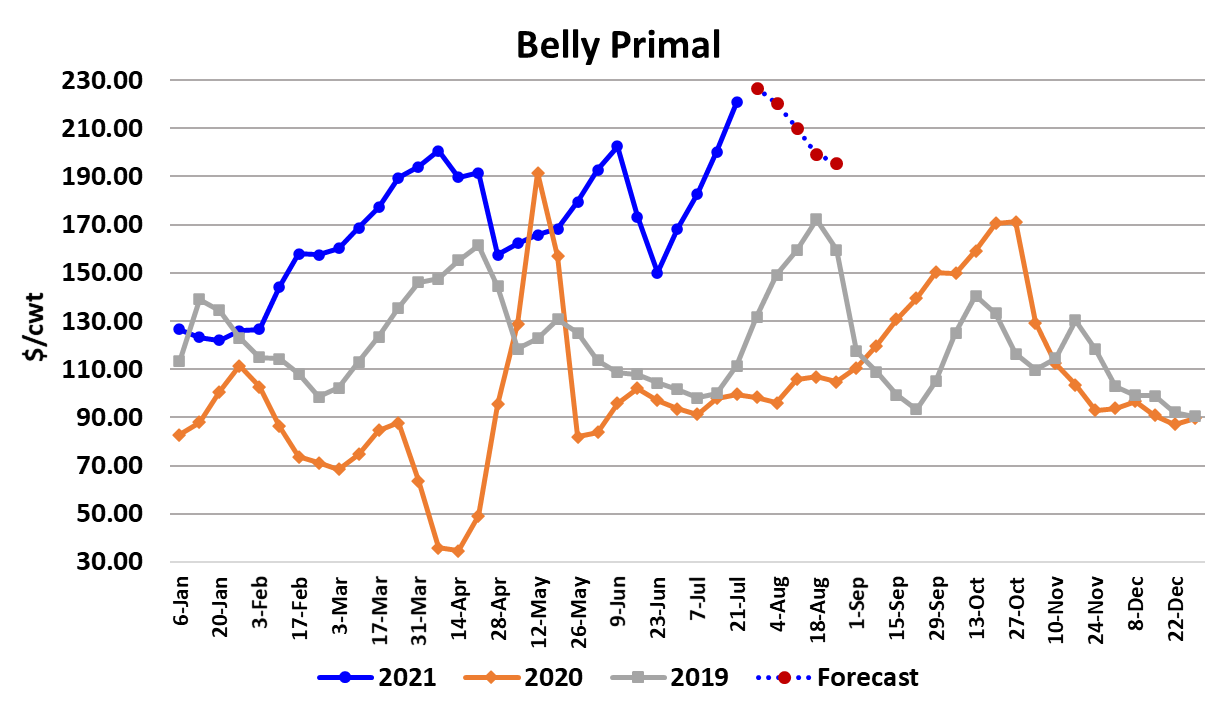

was all about the bellies, which have now moved to an all-time

high.

Without the strength in the bellies, it is a good bet that the cutout

would have been lower on the week. Bellies can be a fickle beast

and very volatile. Recall that it was a sharp drop in belly prices

back in June that precipitated the big decline in the cutout. At that

time, the belly primal went from around $200 to $150 in just 2

weeks. That type of downdraft could happen again at any moment

given how high belly prices are. I suspect that bellies are caught

up in a demand surge for products containing fat. Pork 42s also

made an all-time high this week. There is no telling how long that

demand boost will last, but with high corn prices it is a pretty good

bet that livestock producers are not going to feed animals any

longer than they have to and that will tend to limit the amount of

animal fat that gets produced. Other parts of the carcass are

struggling. The butts took a huge price hit this week and the loins

look to me like they may be next. In order to turn the cutout lower

we need to see increased pork production.

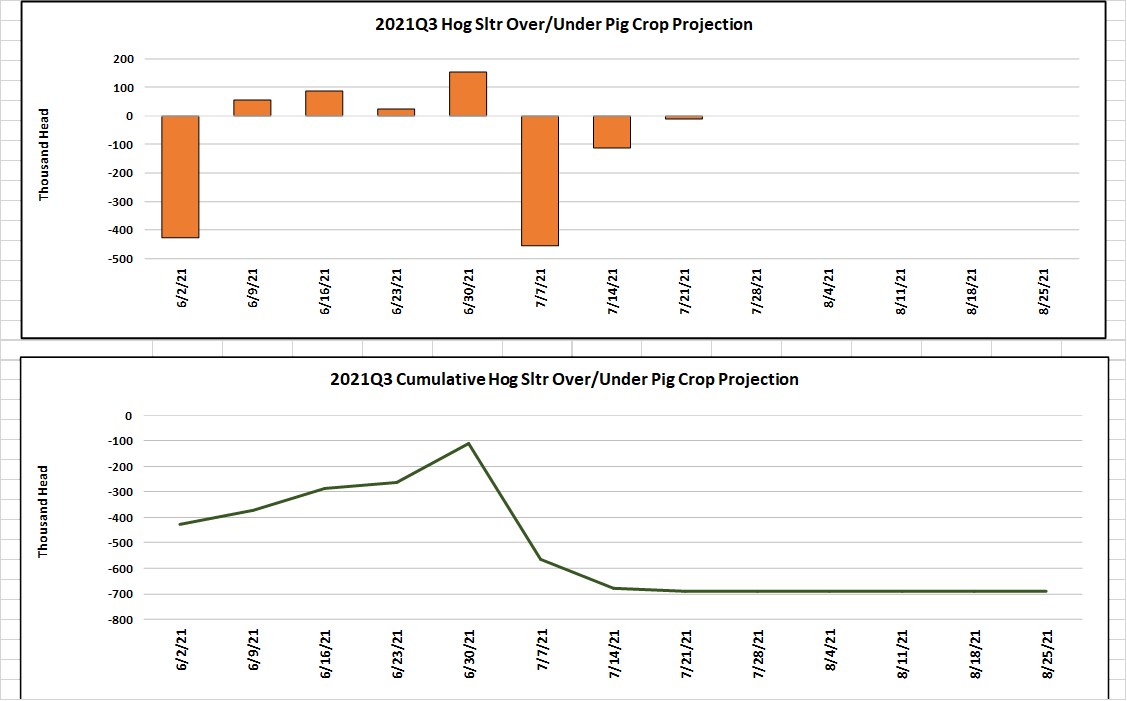

We are at that point in the calendar when kills begin to expand

seasonally and it looks to me like this week’s kill will be

considerably larger than last week—perhaps around 2.36 million

head. That is pretty close to what the pig crop implied (chart

to the right). By Labor Day, I expect to see kills north of 2.55 million

head. If that doesn’t turn the cutout lower then it will be time to buy

everything in the complex with both hands because something very

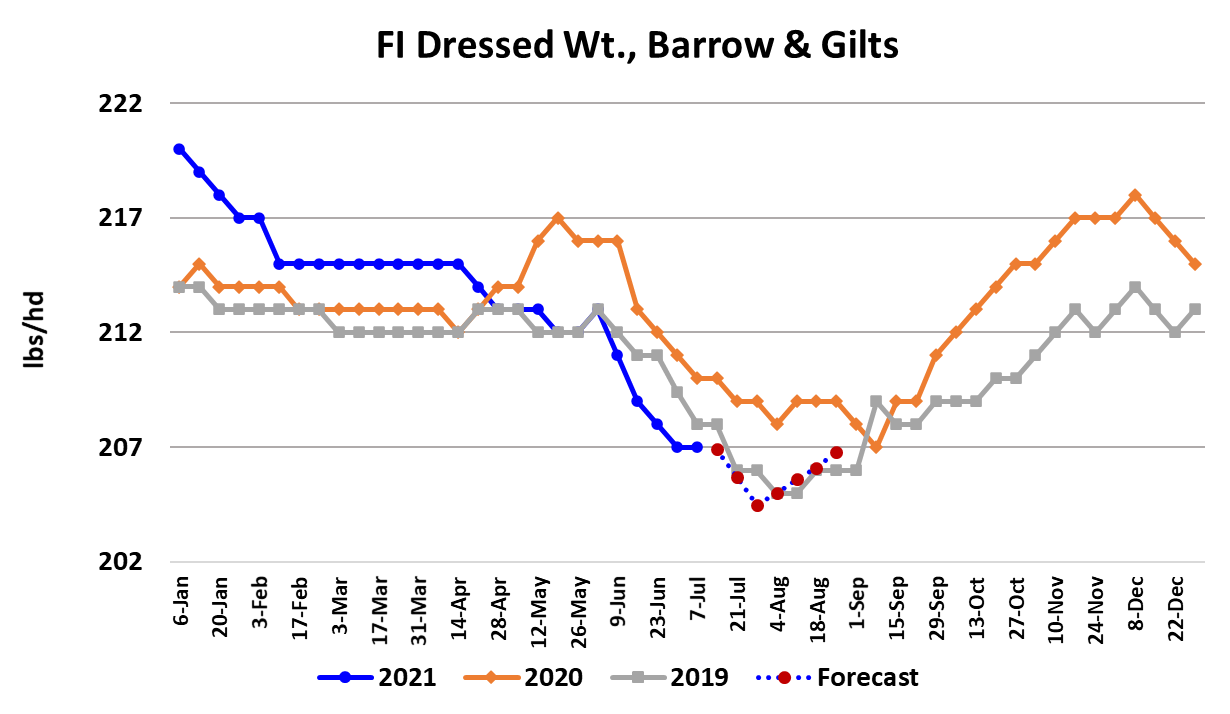

unusual is going on. Hog weights are currently approaching their

annual lows and this week’s data confirmed that they haven’t

started to rise yet. That will come in August. The DTDS weights

are at all-time lows, which tells me that hog producers must be very

current. It is a mystery why the negotiated market has been

printing lower in recent days if hogs are so light and current.

Now that packers have a decent margin once again, perhaps

they will focus on increasing the kill and that might stabilize the

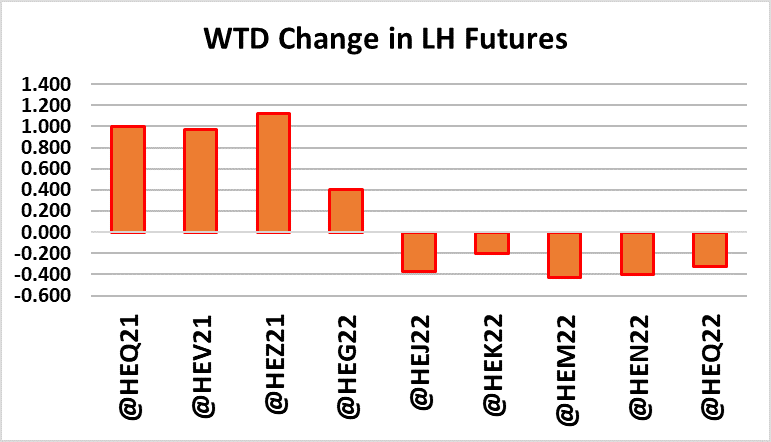

negotiated hog market. Right now, the LHI seems to be stuck

around $112 as higher cutout values are being offset by lower

negotiated hog prices. My forecast has the LHI beginning to

move lower in the next couple of weeks, that means that Aug is

likely to expire well above where traders thought just a few

weeks back when it ventured into the high $90s. I guess we

shouldn’t be surprised by that since traders at one point were

pricing the Jul contract at $100 and it ended up expiring at

$112.

I see the price declines accelerating between the Aug and

Oct expirations. The cutout futures are valuing the cutout at

$103 in October and that just looks way too high for me. Kills

will be much larger then and the hogs will be heavier. I favor a

cutout in the low $90s for October. If I’m right about that then

the LHI might trade in the low $80s since with

expanding supplies we would expect packer margins to be

relatively wide in October. One sharp belly pullback like we saw

in June would quickly correct that problem. The export

data released Thursday morning wasn’t very encouraging.

Net new sales to China were negative, meaning there were

more cancellations than new sales. Movement was pretty

good to Mexico and Japan, but if China is withdrawing from

the US market then I’m afraid it will leave a hole that is too big

for other destinations to fill.

It seems that recently the futures have spent the early part of

the week pumping up the deferred contracts in response to

the rising cutout but then when Thursday arrives the export

data throws a wet blanket on the party. Next week, watch the

bellies and hams. They are the main drivers of the cutout at

this point. Any stumble in either one of those has the potential

to greatly alter the psychology of this market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}