Pork Wrap July 22

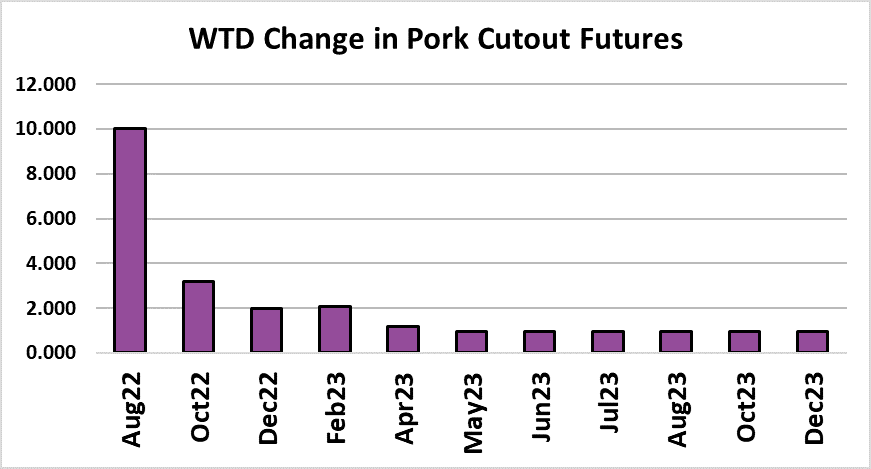

Cash hog prices held about steady this week, but the cutout

gained nearly $6/cwt on a weekly average basis. The chart

below indicates that, once again, it was the processing items that

were the main drivers of the cutout increase. Bellies in particular

caught fire this week. It is a dangerous combination when hams

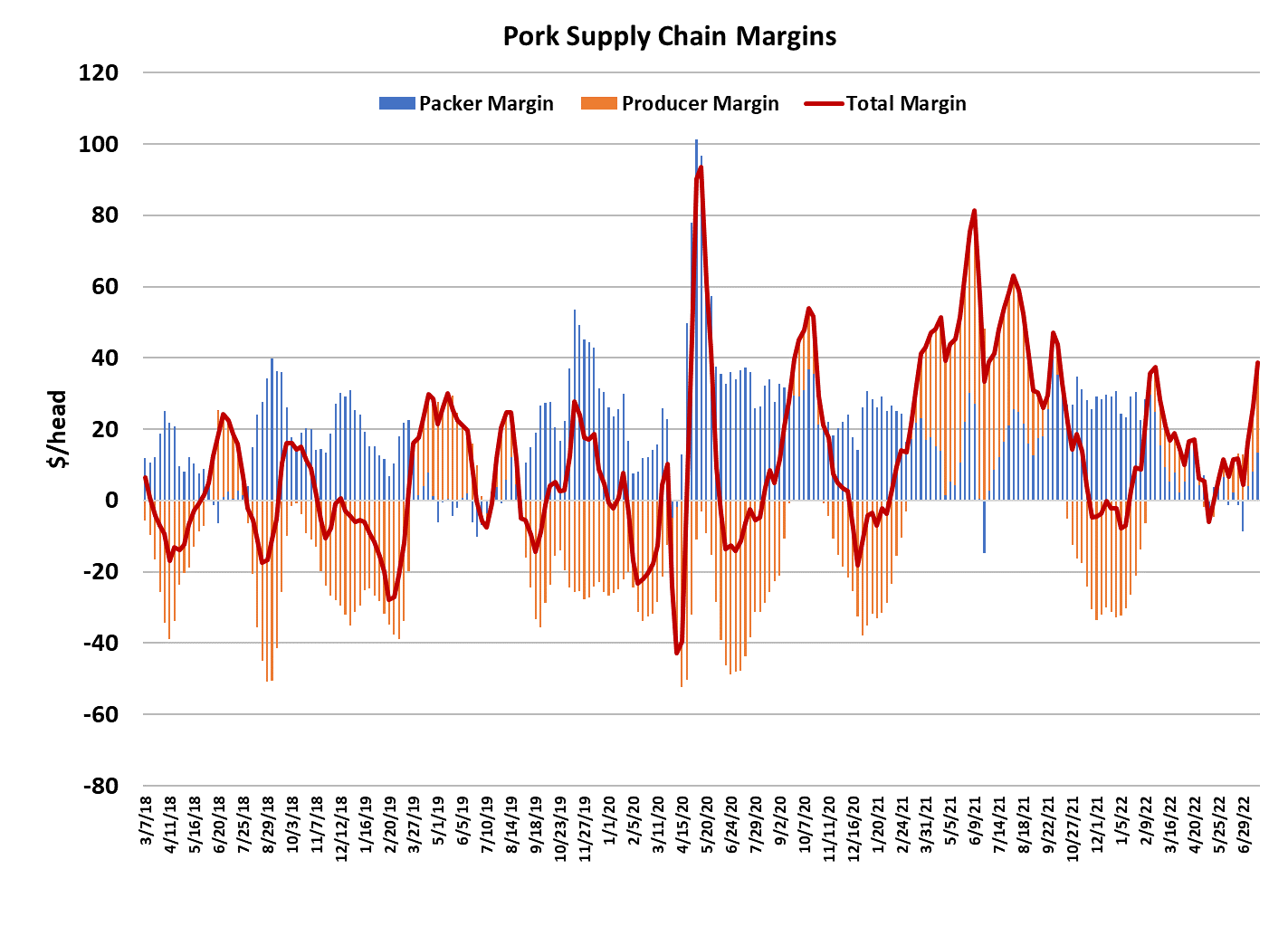

and bellies are moving higher in tandem. Naturally, packer

margins expanded in a big way. I calculate this week’s margin at

slightly over $13/head, up over $5/head from last week. That is a

pretty wide margin for July and I don’t expect it to stay that way.

Packers are busy scrounging for any extra hogs they can find to

keep their plants operating at a reasonable utilization rate and I

think that is going to cause a further strengthening in the cash hog

market. The weather has not been as hot as advertised in the

Midwest, but it has been hot and that might have some hogs

falling behind schedule for finishing, thus giving producers more

leverage when packers come calling for any hogs that are at

market weight.

Another reasonable question to ask is whether or not the belly

rally has run it course. I don’t think so. Last year, the belly primal

peaked at about $240/cwt in early August and right now the primal

is only at $202/cwt. My forecast has bellies increasing for another

two weeks and then starting to work lower. I don’t see the top

being quite as high as last year, but it could easily reach the

$215-220 area on the primal. Hams, on the other hand, are

probably a lot closer to topping. They have been trading over last

year since early June and the primal is now $7/cwt over where it

was last year at this time. Buyers should soon start to balk at

these high ham prices. If I’m right that the hams are nearing a

top, but the bellies keep going, that means the cutout could hold

around the $125 area or better for 2-3 more weeks and by then

the Aug contract will be nearing expiration.

The belly rally seems like a normal occurrence that was due and

is probably driven by retail features that are scheduled for Aug/

Sep. The ham rally, on the other hand, seems out of the ordinary

and I sure would like to know what is behind it. It is hard to

imagine that Mexico is buying a lot of hams out of the US at these

high prices. More likely, users forward contracted back in the

spring for delivery of hams this summer and now as packers are

delivering on those orders, it has greatly tightened up the spot

market supply. Once those orders are filled, we should see

greater spot availability and retreating price levels. The

processors that normally come into the market in mid-to-late

summer looking to secure raw material for their holiday hams

must be sweating bullets right now.

Or maybe they are the ones taking delivery on booked orders. The retail

primals are holding value well, but not increasing to the degree that the

processing items are. Butts held steady this week but look like they are

making a top. Loins were also steady and probably don’t have a lot of

upside potential from here. On thing that should have been a strong

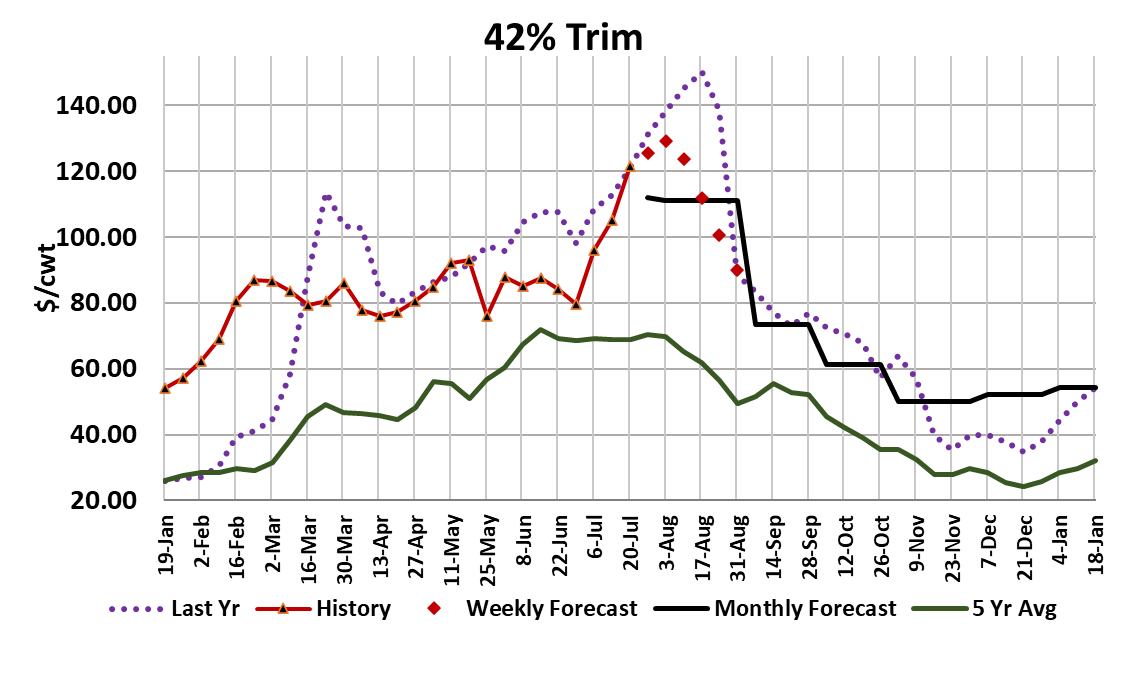

indicator that the pork complex was going to rally is the price of trims.

Both fat and lean trim have been moving rapidly higher. That is a sign

that processing has slowed, most likely due to limited raw material

availability. Of course, it is the middle of July, so we shouldn’t be too

surprised that pork availability is tight and price levels are high. The

combined margin continued to rocket upward this week as belly and

ham buyers scrambled to find product in the spot market. That shows

up as strong demand and a strong combined margin when the cutout

rises.

My guess is that the combined margin has at least 2 more weeks to

move higher before it makes a top. Users aren’t getting much relief

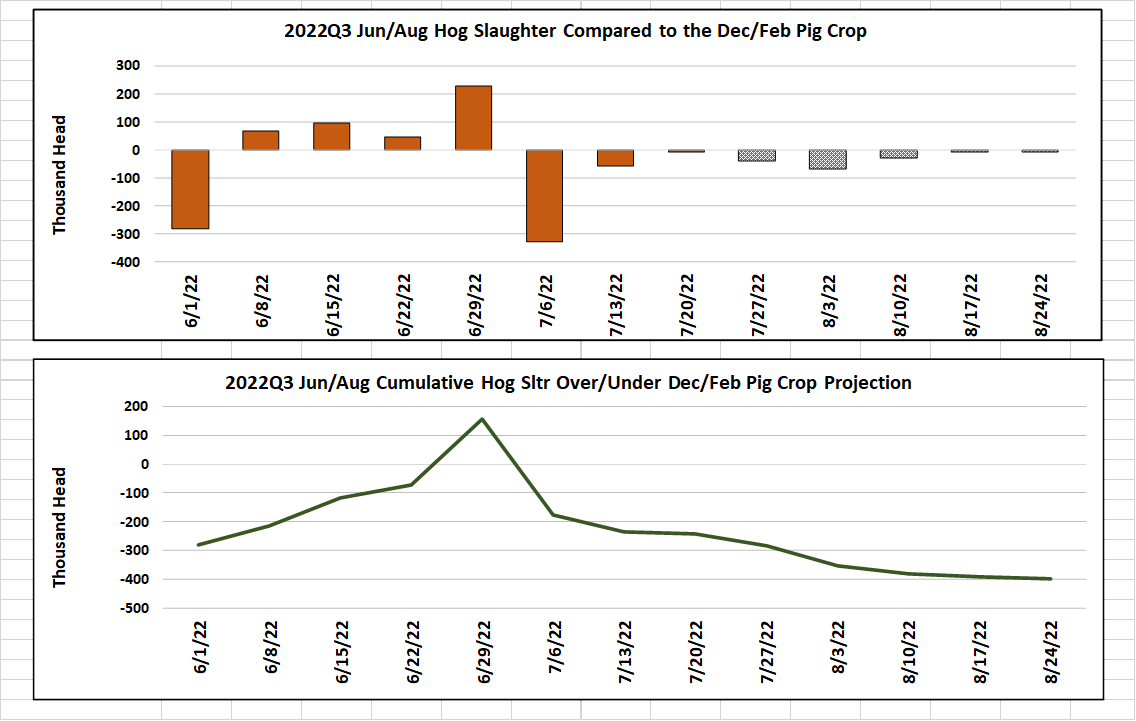

from the supply side of the market. This week’s kill registered 2.29

million head, which was very close to what the pig crop implied for this

week. However, we are now halfway through the Jun/Aug quarter and

cumulative slaughter is down about 300k from what the pig crop

projected. It’s not a huge miss, but it does suggest that perhaps the hog

supply was a little snugger than advertised. Another possibility is that

the heat has slowed down the hog pipeline so that it makes the hog

supply look tighter than expected, but those hogs will eventually come

tumbling out of the pipeline. I guess that is what the futures bears are

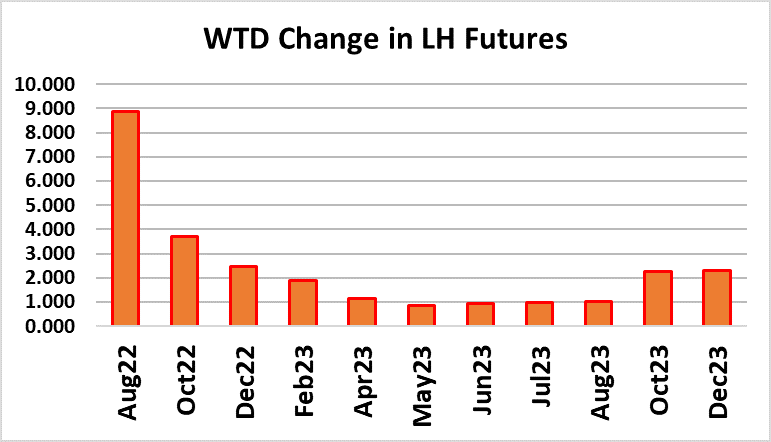

counting on because they are pricing the Oct contract at a whopping $22

under the Aug contract. My fundamental forecast has Oct expiring

almost $29 under Aug, so I can’t argue with the wide spread.

Of course, the longer the current price strength persists, the more likely

that I will need to raise the Oct forecast. Carcass weights ticked one

pound higher this week, but the data were for the week including July 4,

so the gain is probably temporary. The DTDS weights look rather

normal and are not indicating a super-current hog supply yet. We will

need to keep a close eye on that because the potential for heat-related

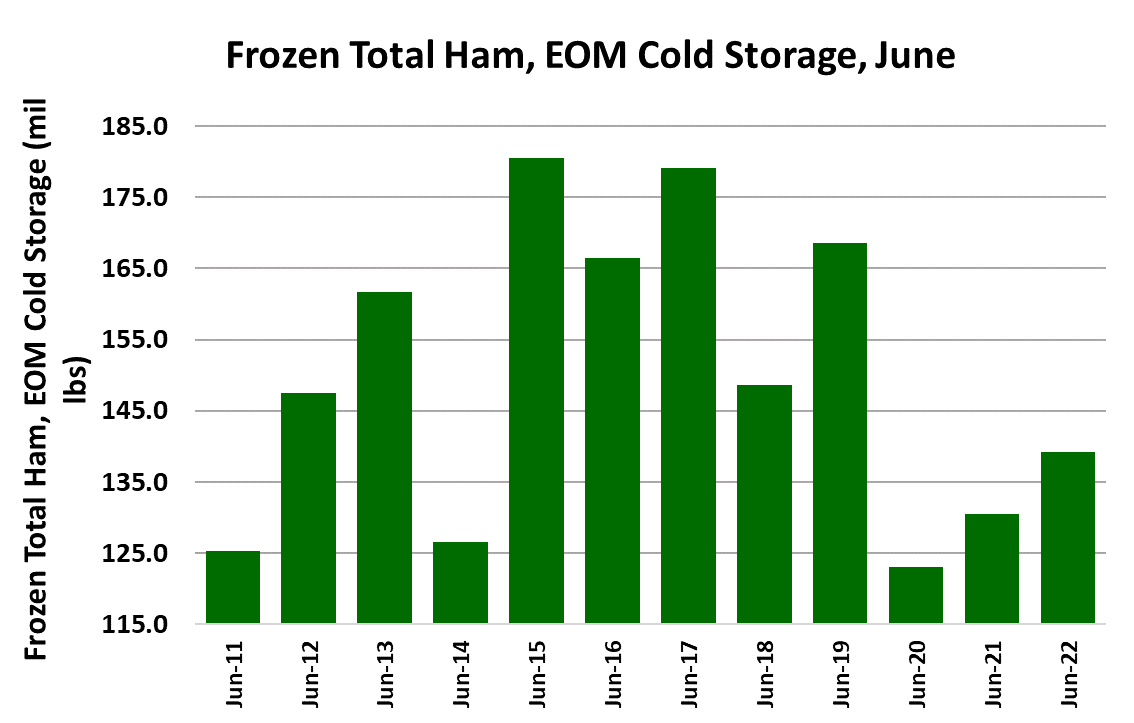

weight loss doesn’t really go away until late August. Today’s Cold

Storage report showed about a one percent out-movement of product

during June for pork as a whole, but hams showed a 10% increase in

cold storage stocks over the 30 days in June. Total pork in cold storage

is up 22% YOY, but hams in cold storage are only up 6.6%. Belly stocks

are up 46% YOY, so no problems there. Next week, watch the hams

and bellies for further gains and also watch for strength in the negotiated

market as packers continue to search high and low for available hogs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}