Pork Wrap July 21

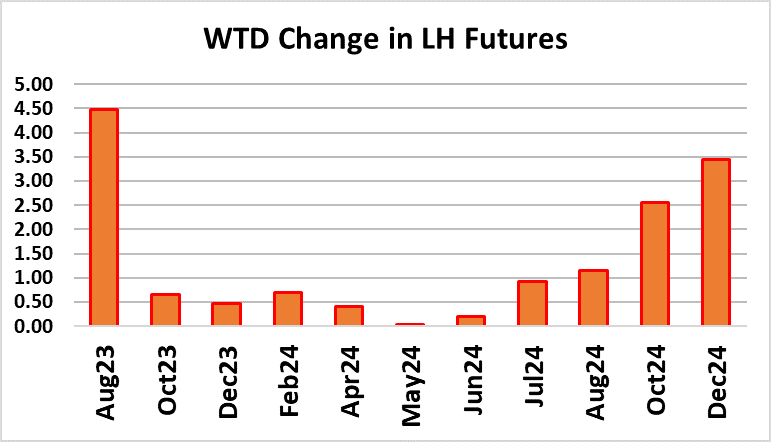

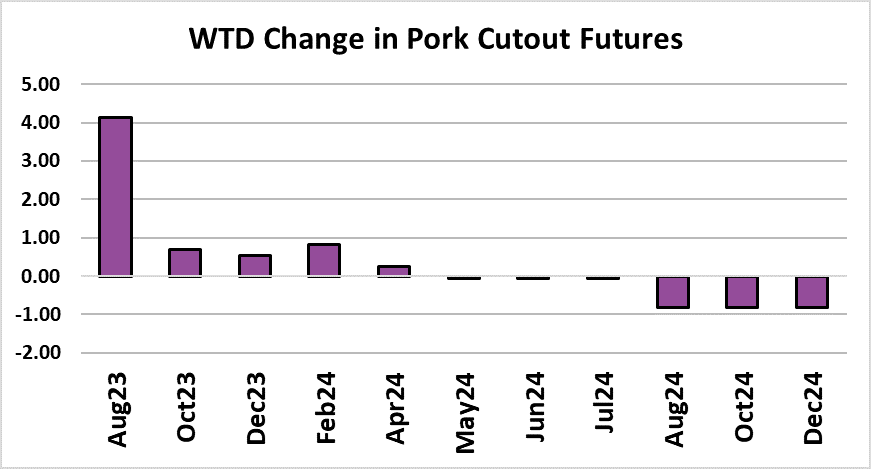

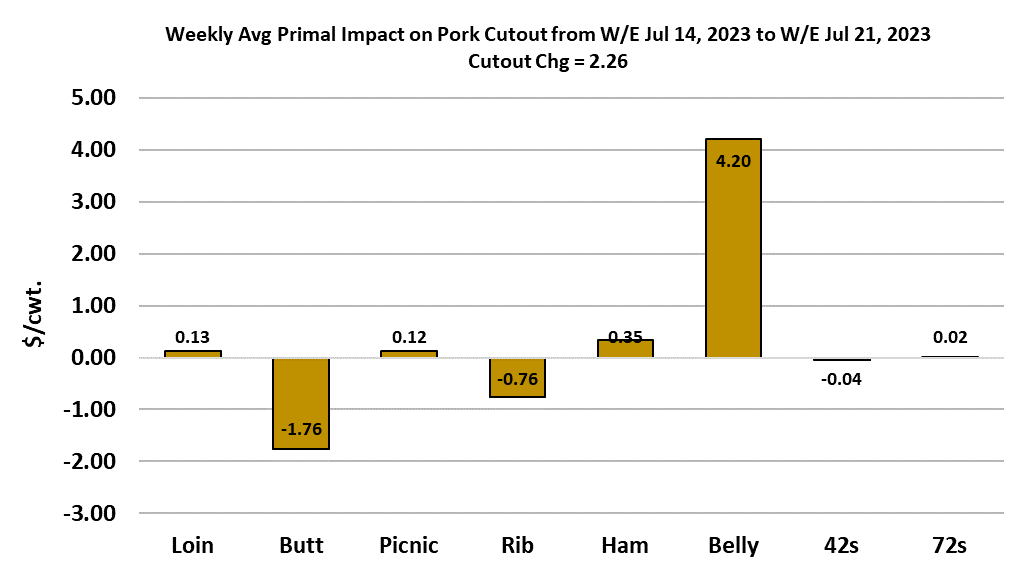

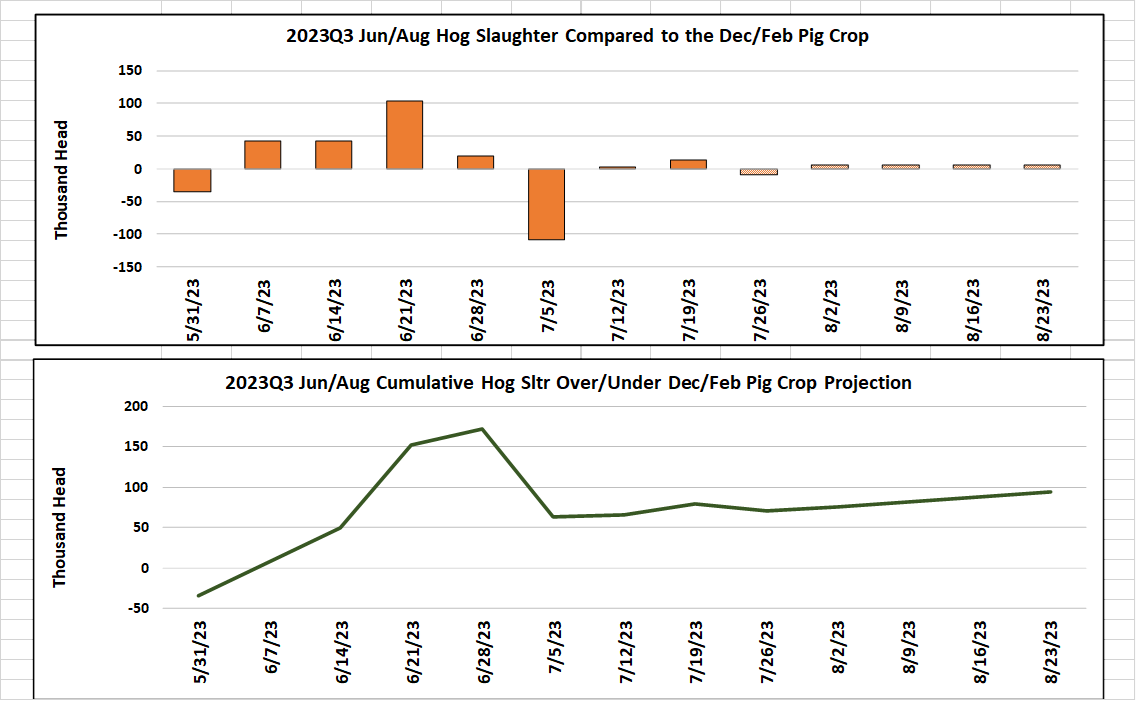

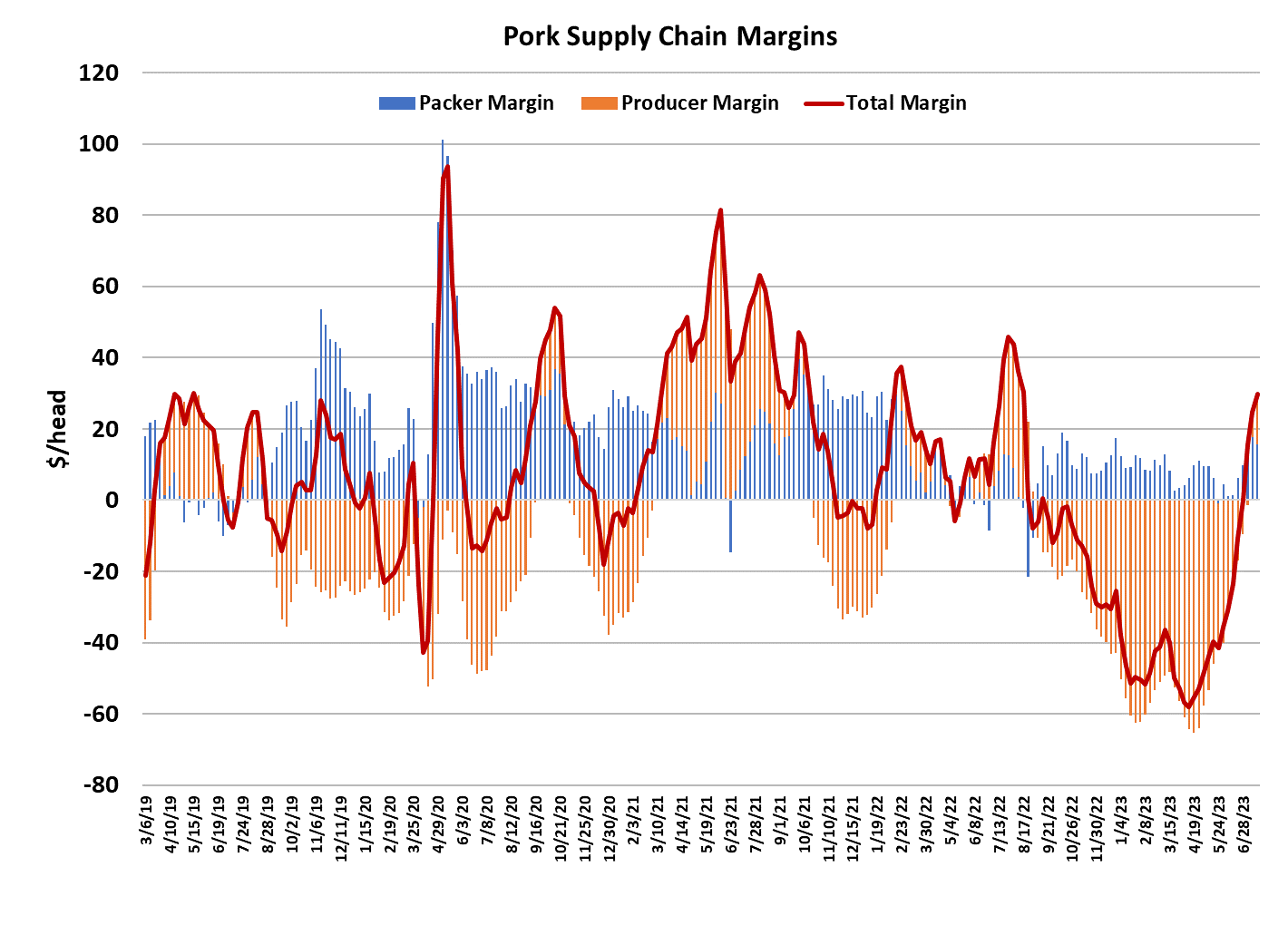

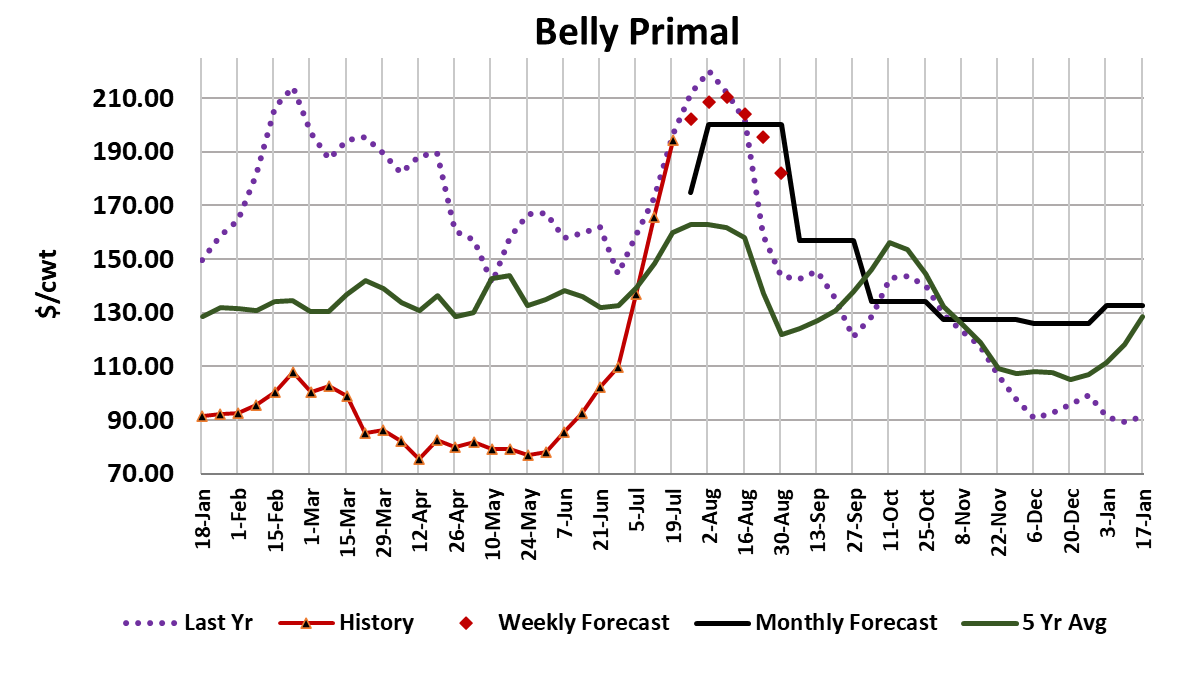

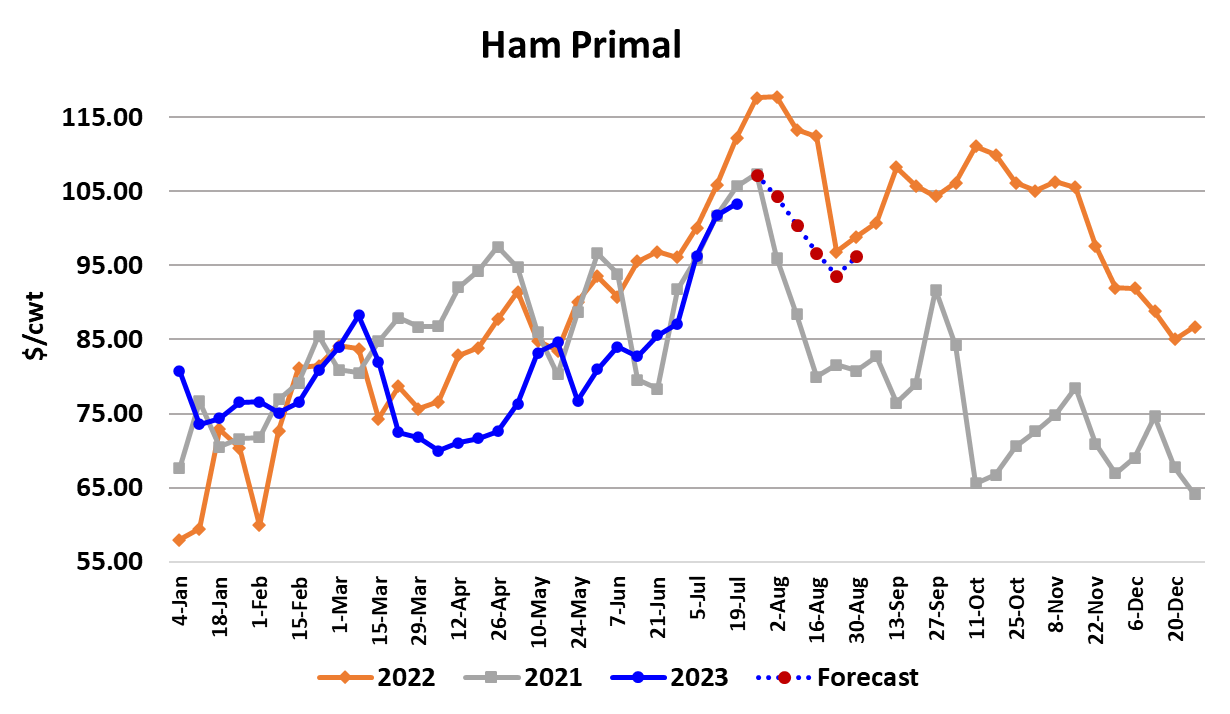

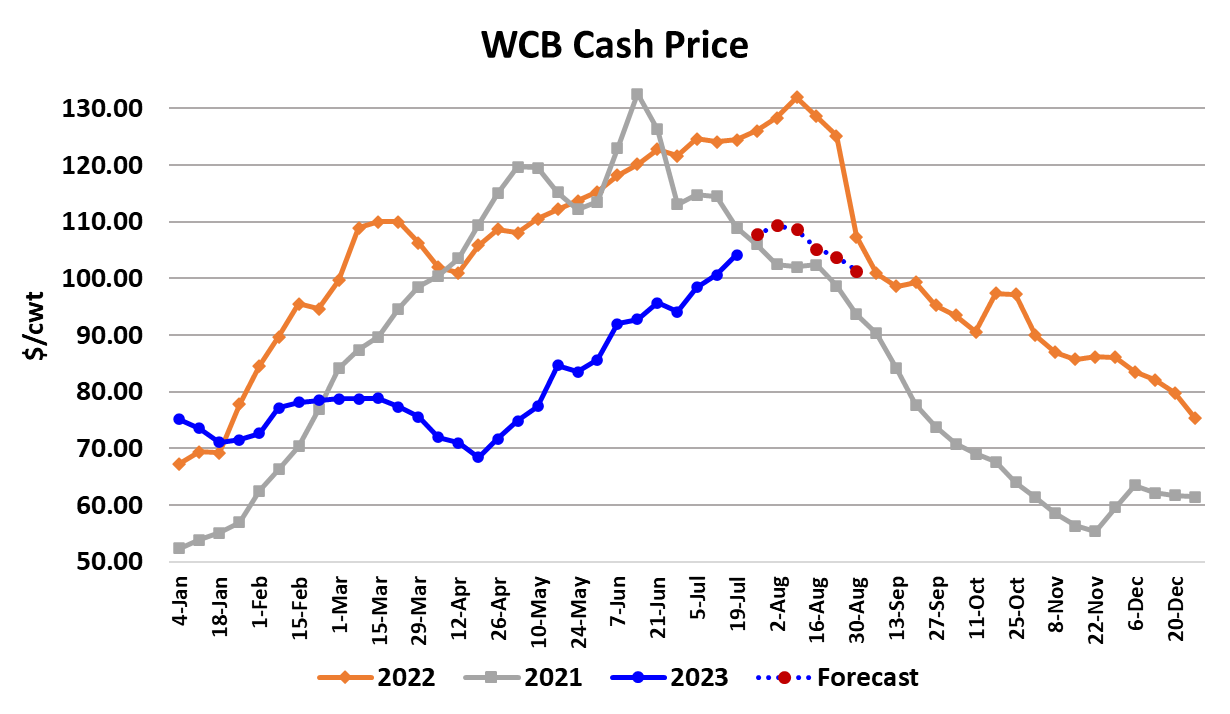

Cash hog prices worked higher again this week, with the WCB negotiated market averaging $104.13, a $3.50/cwt increase from last week. Packers can afford to pay more for hogs because they are getting more for their pork. This week, the cutout averaged $113.67, up $2.26 from last week’s average. The cutout has been moving higher since mid-April and doesn’t seem to be ready to turn lower yet. One worrisome feature of this week’s market is the fact that most of the increase in the cutout could be traced back to just one item—the bellies. The belly primal added almost $30/cwt on a weekly average basis. At the same time, the retail items were pricing steady to softer. Butts continue to be the weak sister of the carcass, but they may be nearing the end of a very steep downward correction. Hams were a little stronger this week, but it is beginning to look like some of the wind is starting to come out of those sails too. Toward the end of the week the 23/27 lb hams printed a little softer, but the test on those was mild and I want to see how they perform early next week before I declare the ham rally to be dead. That leaves the bellies as the sole source of support and they are rising rapidly as bellies are often prone to do, but everyone knows that bellies can turn on a dime and come down just as fast as they went up so a certain level of nervousness is understandable. My forecast has the bellies continuing higher for another couple of weeks before high prices start to cure high prices. At the same time, I don’t really expect the other primals to fall apart rapidly, but rather gently ease lower as production starts to expand in August. That results in a forecast that has the cutout holding near $115 for a couple more weeks and then easing downward toward $106 at the end of August. Last year, the cutout peaked in the last week of July, then dropped $3 a week for the next two weeks before a major belly crash took the cutouts quickly lower near the end of August. The ham situation is uncertain because some softening of domestic demand typically takes place during August, but we also export a lot of hams to Mexico and hog and pork prices in Mexico are very high right now, so we could continue to see good movement of hams into the export market. Even though ham prices are at their highest level so far in 2023, they have been consistently lower than last year since the middle of March. Further, last year the hams peaked in the last week of July, so if we are on that same schedule again this year, then a move lower in the hams could be just around the corner. The combined margin continued higher again this week, so that is a sign that we are still in a demand upcycle. However, everyone knows that this cycle has been exceptionally long and is overdue to turn lower. Certainly, futures traders are thinking that way, as the Aug contract settled today at $100.67 while the LHI that is settles to is projected to reach $106 by early next week. Given that Aug will expire in a little over three weeks, it is pretty brave for traders to keep the futures at such a big discount to an index that is trending higher. The Aug contract did add almost $4.50 this week as traders soon realized that pricing in the mid $90s was untenable. This week’s kill registered 2.32 million head, which was very close to what the pig crop suggested. It is starting to look like USDA did a much better job of estimating the Dec/Feb pig crop than they did in previous quarters because the cumulative overkill is only about 50k head—well below what we saw Q1 and Q2. I look for next week’s slaughter to be similar to this week and then in the first week of August we could see the kill expand modestly to 2.4 million head. By the end of August, the kill should reach 2.5 million head if the pig crop estimate is correct. Carcass weights were reported steady this week, but they likely will decline at least another couple of pounds before they turn seasonally higher. That should keep pork supplies relatively snug for a couple more weeks and that is a big reason why I don’t expect a significant near-term softening in the cutout. So far, there hasn’t been much evidence of a Prop 12 effect in the pork market, but that doesn’t mean that traders don’t continue to worry about it. My thought is that if Prop 12 is going to cause a pricing problem, it is more likely to happen in the fall or early winter when hog and pork supplies are seasonally large, and the state of California is more focused on enforcement than they are right now. Next week, expect more of the same, with cash hog prices moving higher and bellies continuing to show strength. Watch the hams closely for signs that the rally there may be coming to an end.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}