Pork Wrap July 19

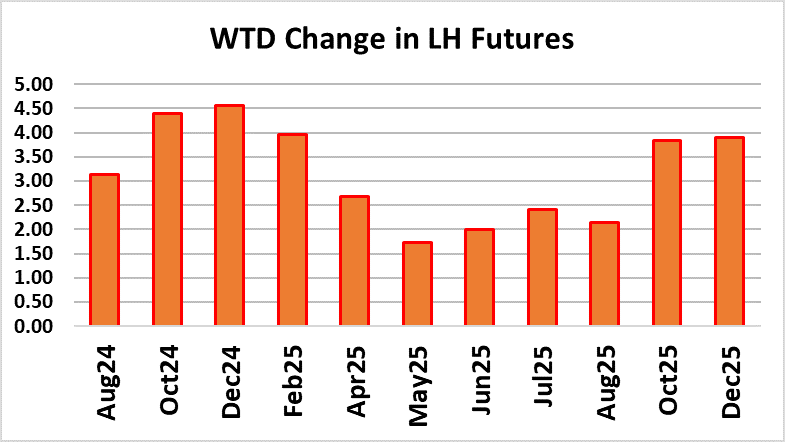

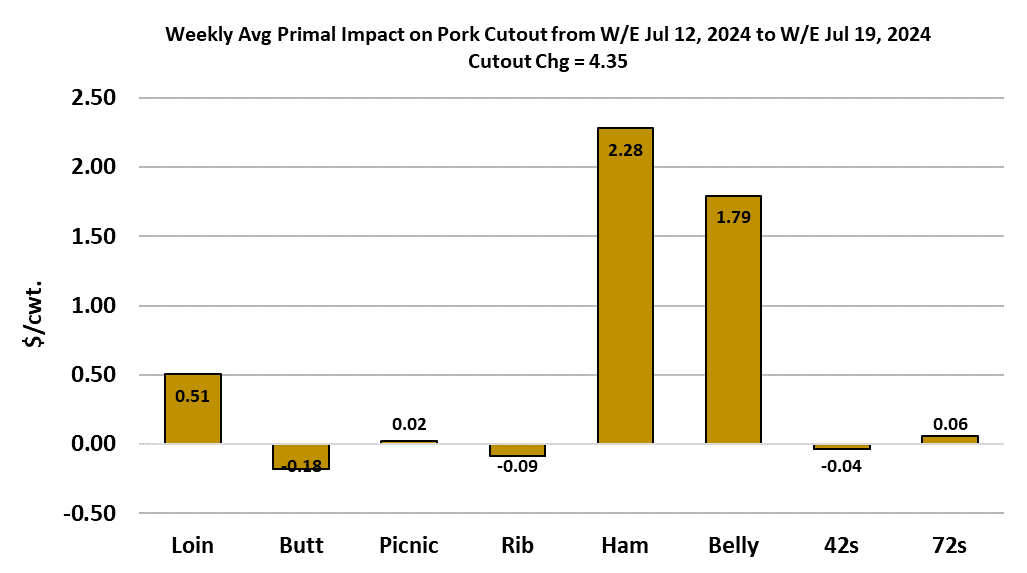

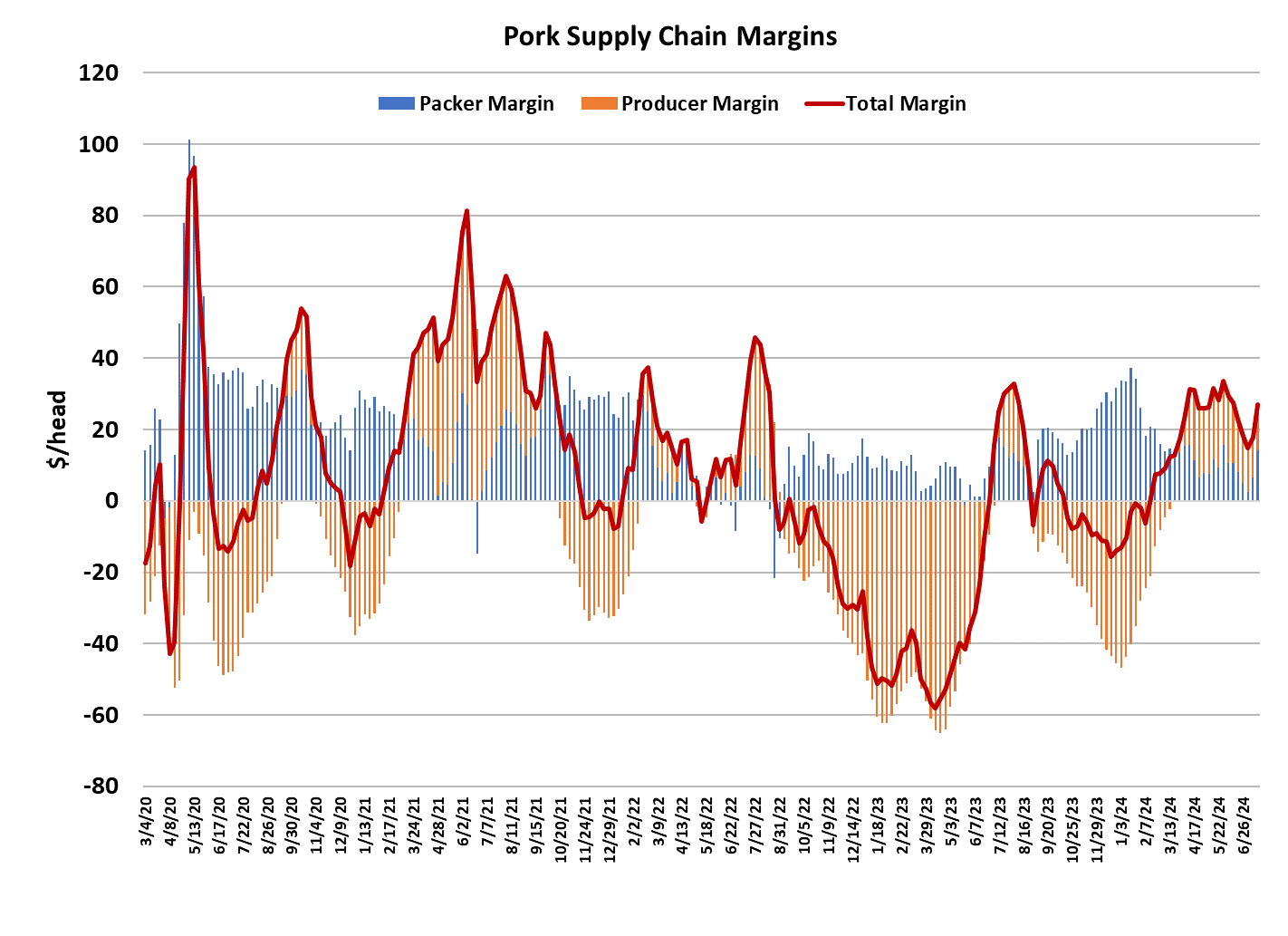

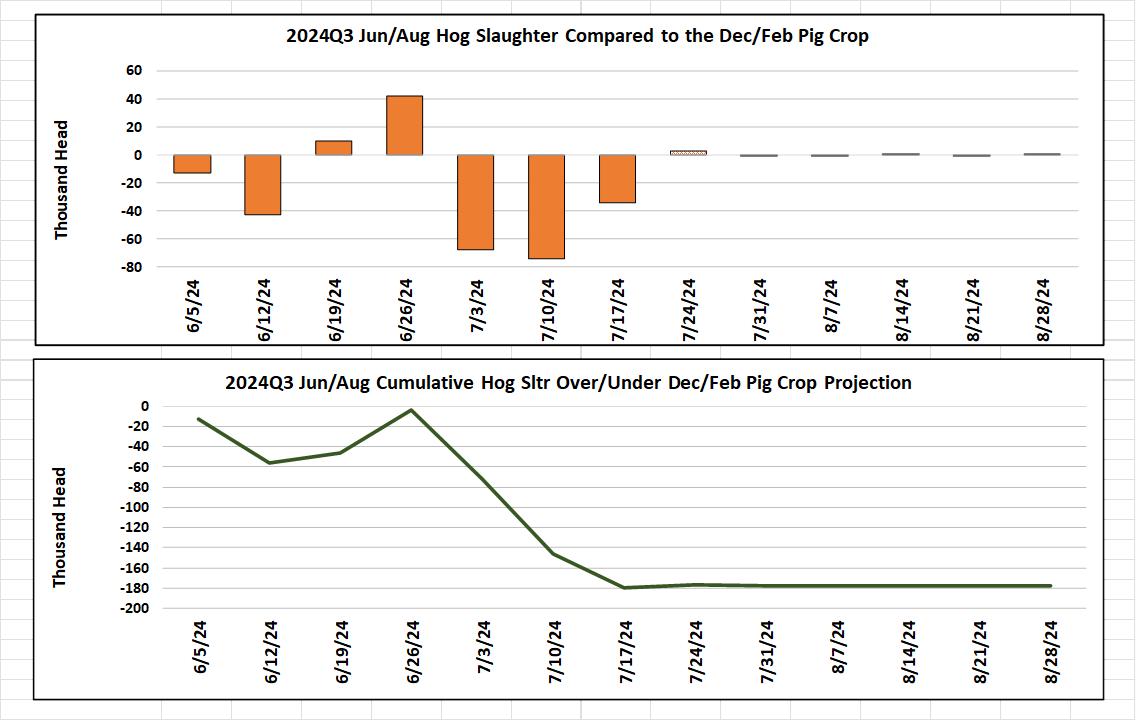

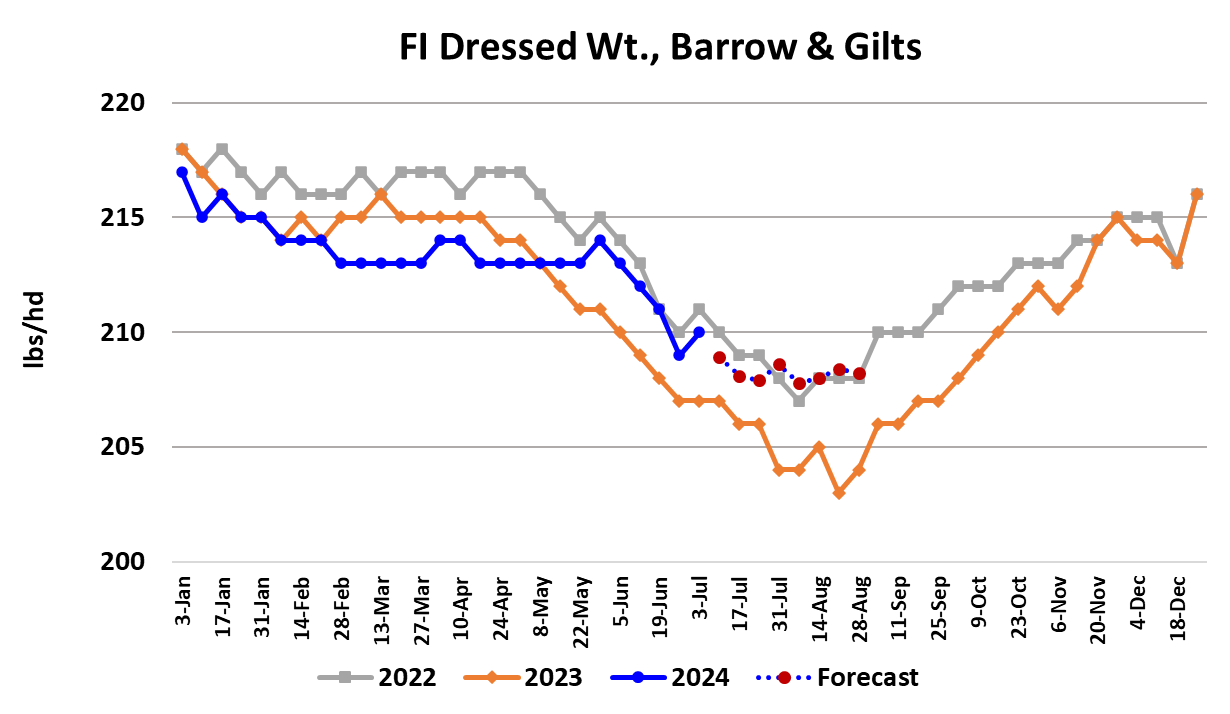

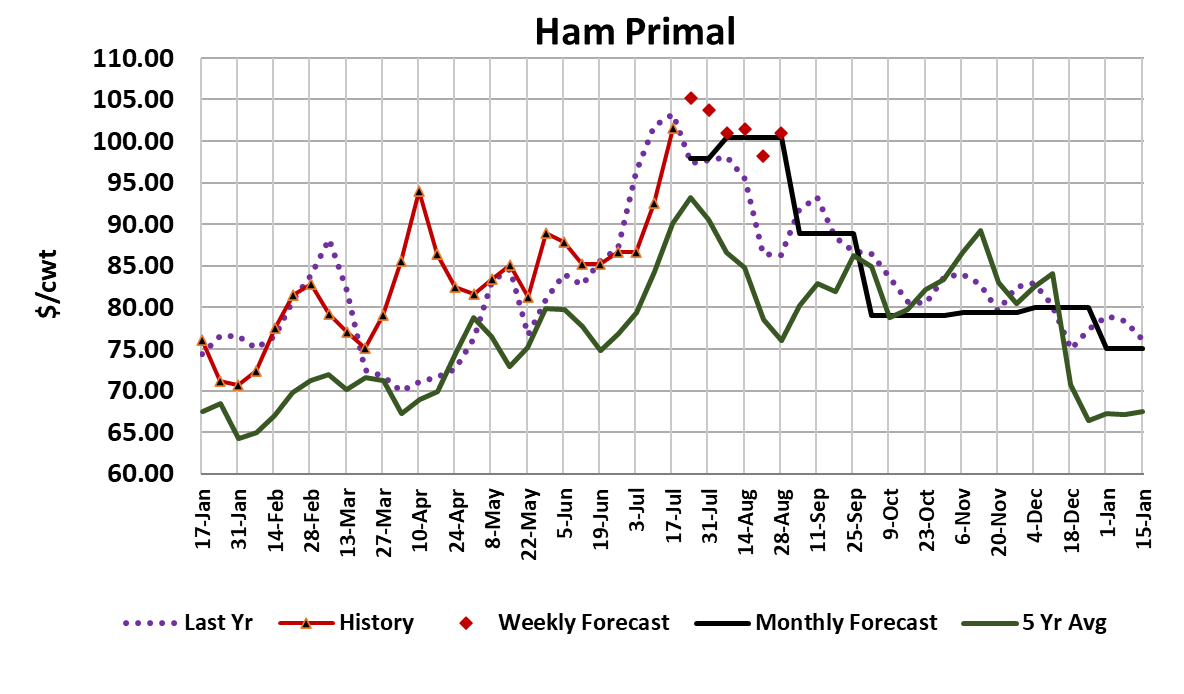

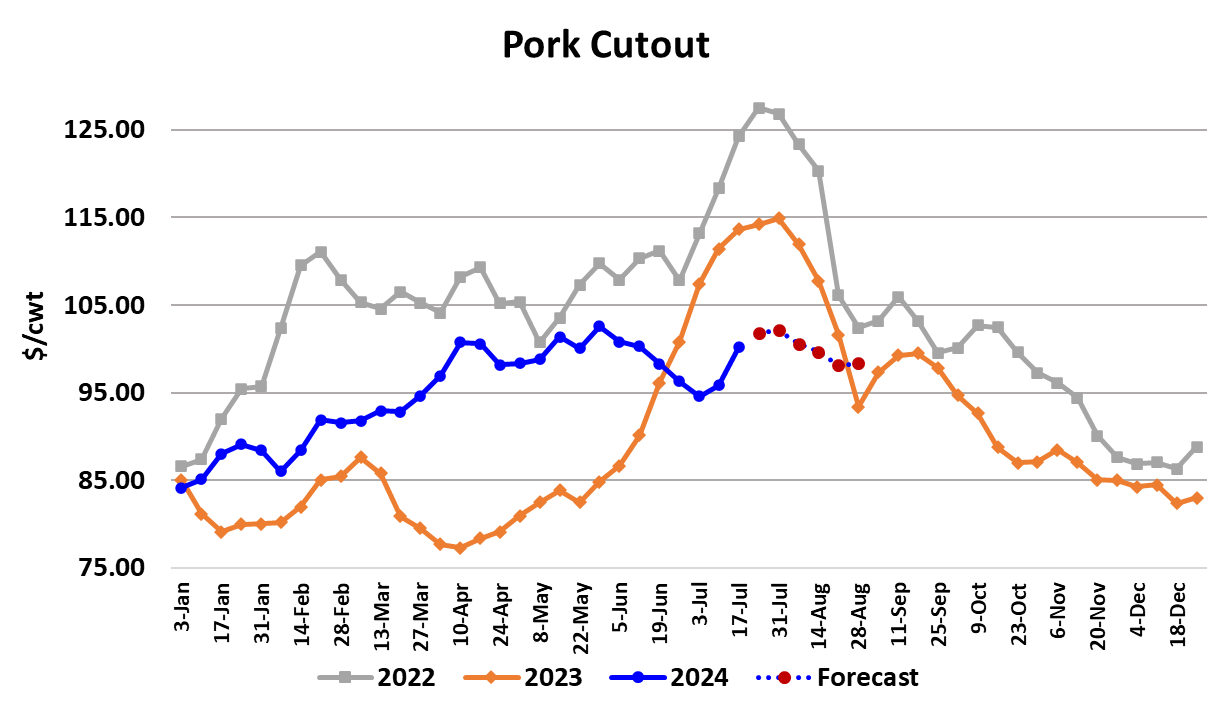

Well, it finally happened. The pork cutout came to life this week, adding $4.35 to average $100.18. That is the biggest increase in the cutout in over a year. The sharp gains were driven by the perfect storm of hams and bellies both moving higher at the same time. Both were on our watchlist and they didn’t disappoint. This week’s average on the ham primal was $101.57, which is very near last year’s high of $103. So far, the hams haven’t shown signs of slowing down, so I’ve got another increase built in for next week, but that may be the top. The bellies, on the other hand, seem to be just getting started and that move higher could span several weeks. Packers reaped all of the benefit from this week’s price increases since they were able to keep cash hog prices moving lower. The WCB market dropped $3.22 on a weekly average basis and the NDD market was down $3.48. As a result, packer margins ballooned out to a little over $14/head. That is not the kind of margin one expects to see in the middle of the summer. Just two weeks ago, packer margins were near $2/head. That suggests that hogs are relatively plentiful at the moment and packers aren’t having to strenuously compete. In fact, packers seem to be slowing the kill rather than ramping it up in response to better margins. This week’s slaughter tallied 2.37 million head, smaller than expected and about 35k below what the pig crop implied. Quarter-to-date, the cumulative kill is about 180k below what the pig crop indicated. However, this week’s kill was still bigger than last year by about 2% and with carcass weights running about 1.5% over last year, FI pork production is well above 2023’s level. Given that this week’s volume cleared the market at higher prices, it is clear that pork demand is seeing some improvement. The combined margin seems to be confirming that. The demand improvement seems to be concentrated in the processing items since not only did hams and bellies improve this week, but trim pricing was also significantly higher. The 42s added a little under $10 this week to average just north of $68 and the 72s were in the same boat, adding $10 as they moved over the $95 mark. The retail items had less success this week, but the loin primal did manage to add close to $2, which was its biggest gain since the middle of April. As I look across the carcass, I only see 2 primals that are still trending lower, the butt and the rib, which together only comprise about 15% of the cutout’s volume. The other 85% of the carcass is seeing prices trend higher. Of course, there is always the question of how long this turn higher will last. The hams probably only have a 1 or 2 weeks of stronger pricing, but the bellies could run higher into the middle of August. Thus, the forecast has the cutout holding firm in the low $100s for 3-4 more weeks before it starts to succumb to the pressure of seasonally increasing production. Hog pricing is a different matter and this week’s sharp increase in margins forced a recalibration that increased the margin forecast at the expense of hog pricing. There may be some modest gains in the negotiated markets over the next couple of weeks, but I’m betting on packer margins holding above $10/head for the rest of the summer, so that will limit the upside potential in cash hog prices and may keep the futures from running too far out in front of the cutout increases. The Aug contract, which finished the week at $91.57, is only about $1.50 over the LHI at the moment, which seems like a very narrow basis in a situation where both hams and bellies are actively advancing. All in all, it looks like we are going to get a summer rally after all, even if it is muted compared to summer rallies in the recent past. Soon, however, hog supplies will start to grow seasonally and the attention will turn to fall and winter, where pork production could easily be up 2-3% YOY if USDA’s pig crop estimate is close. Traders have already shown that they are nervous about the prospects for pricing later in the year and, up until this week, those contracts have taken a beating. Even though the Oct and Dec contracts added over $4 this week, they still look overly pessimistic relative to the fundamental forecast, which has demand improving modestly from what we’ve seen so far this summer. Next week, watch for further increases in the processing items and another, somewhat smaller, advance in the cutout. Cash hog prices are likely to stabilize and perhaps print higher as packers share a little of their newfound margin.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}