Pork Wrap July 16

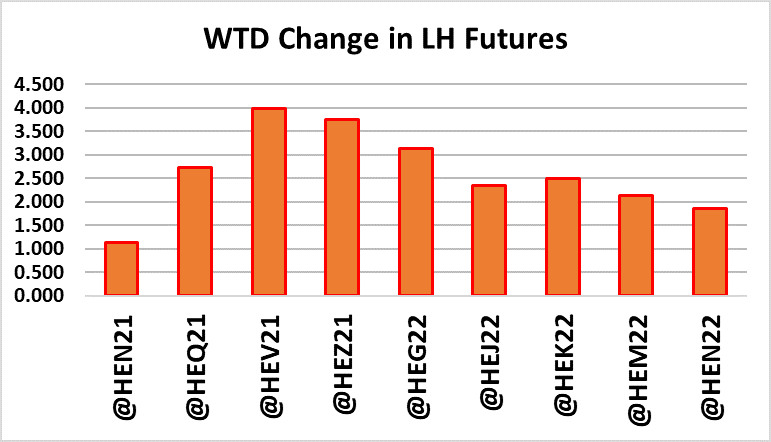

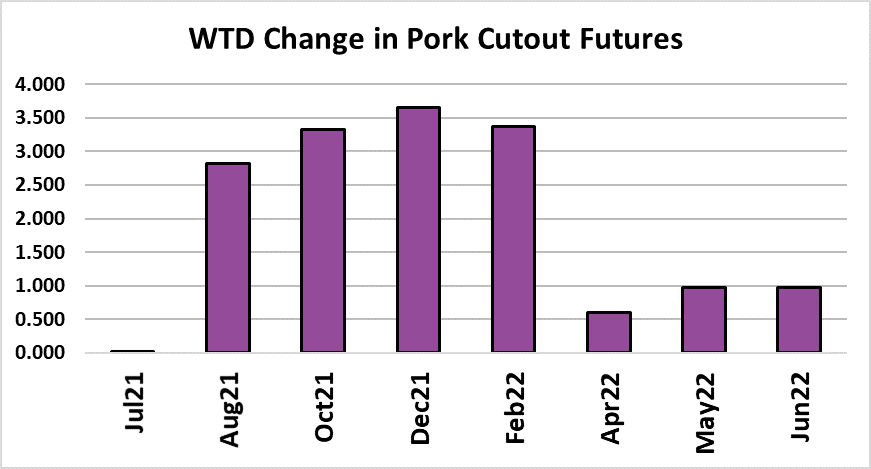

Prices in the hog and pork complex firmed up this week, with the cutout

gaining a little over $3 and the LHI up a little over $1 on a weekly

average basis. It seems as though all of the doom and gloom that

characterized this market a couple of weeks back has now faded. Pork

buyers backed away from the market in late June as the cutout fell, but

they couldn’t stay out of the market forever and now they are back and

have pushed the cutout back near $120 as of this afternoon.

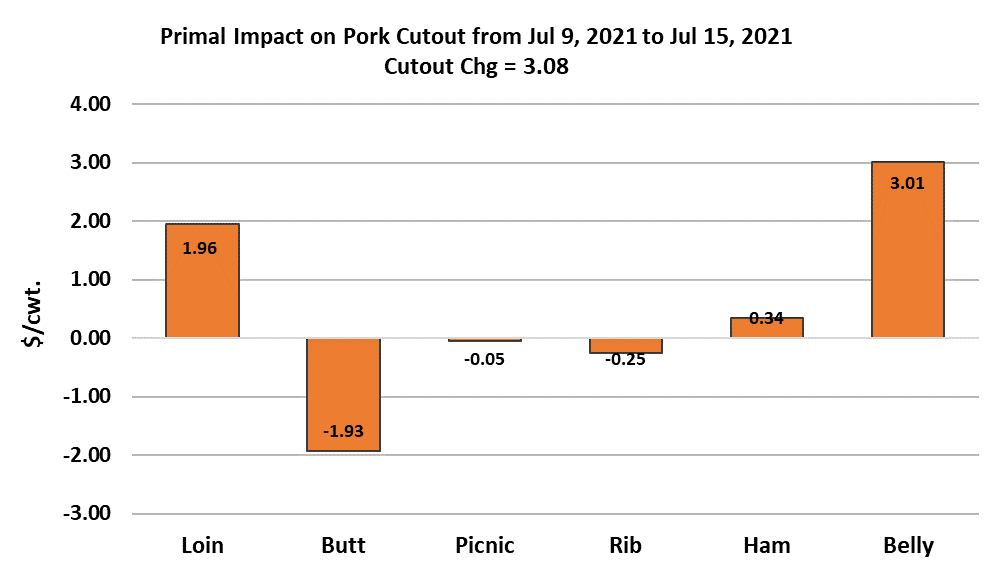

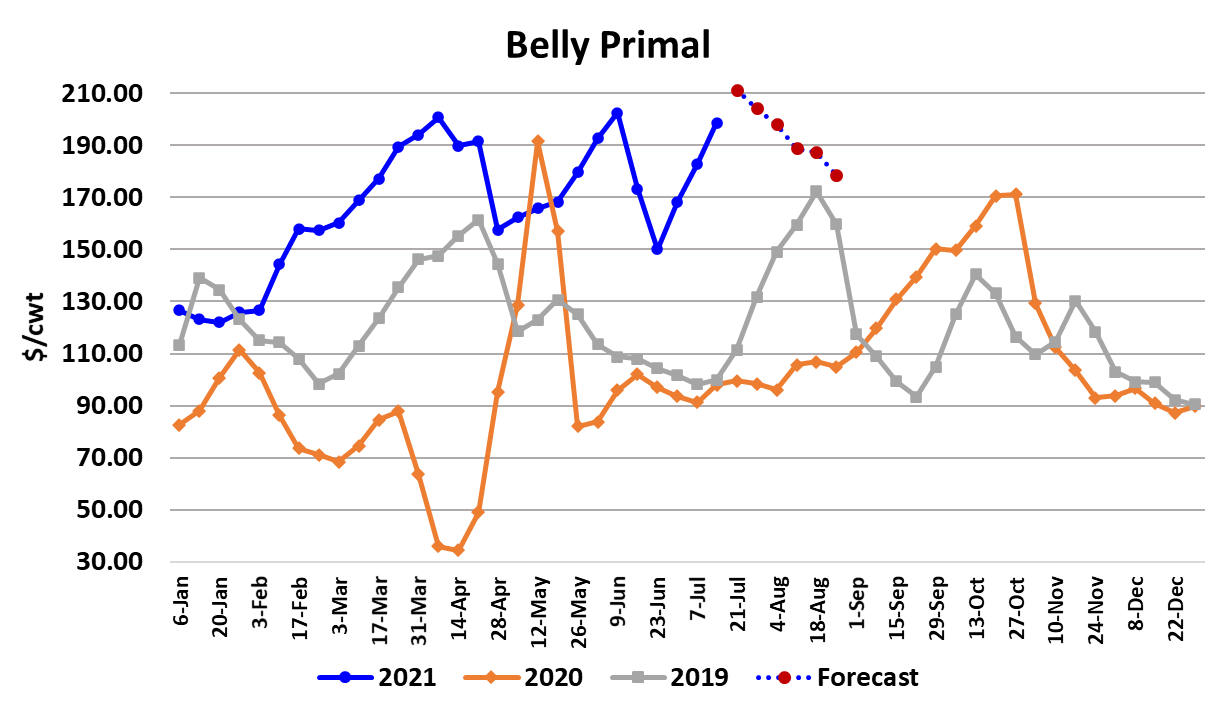

This week, it was the bellies and loins that did the heavy lifting in the

cutout. Hams are still posting strong numbers too, but the gains there

have slowed somewhat. All of this begs the question, “Was the sell-off

back in late June just a dramatic head fake?” Possibly, but I think that

the market has peaked and is in the process of heading lower just like

the beef market, but it can’t come down as fast because we are in the

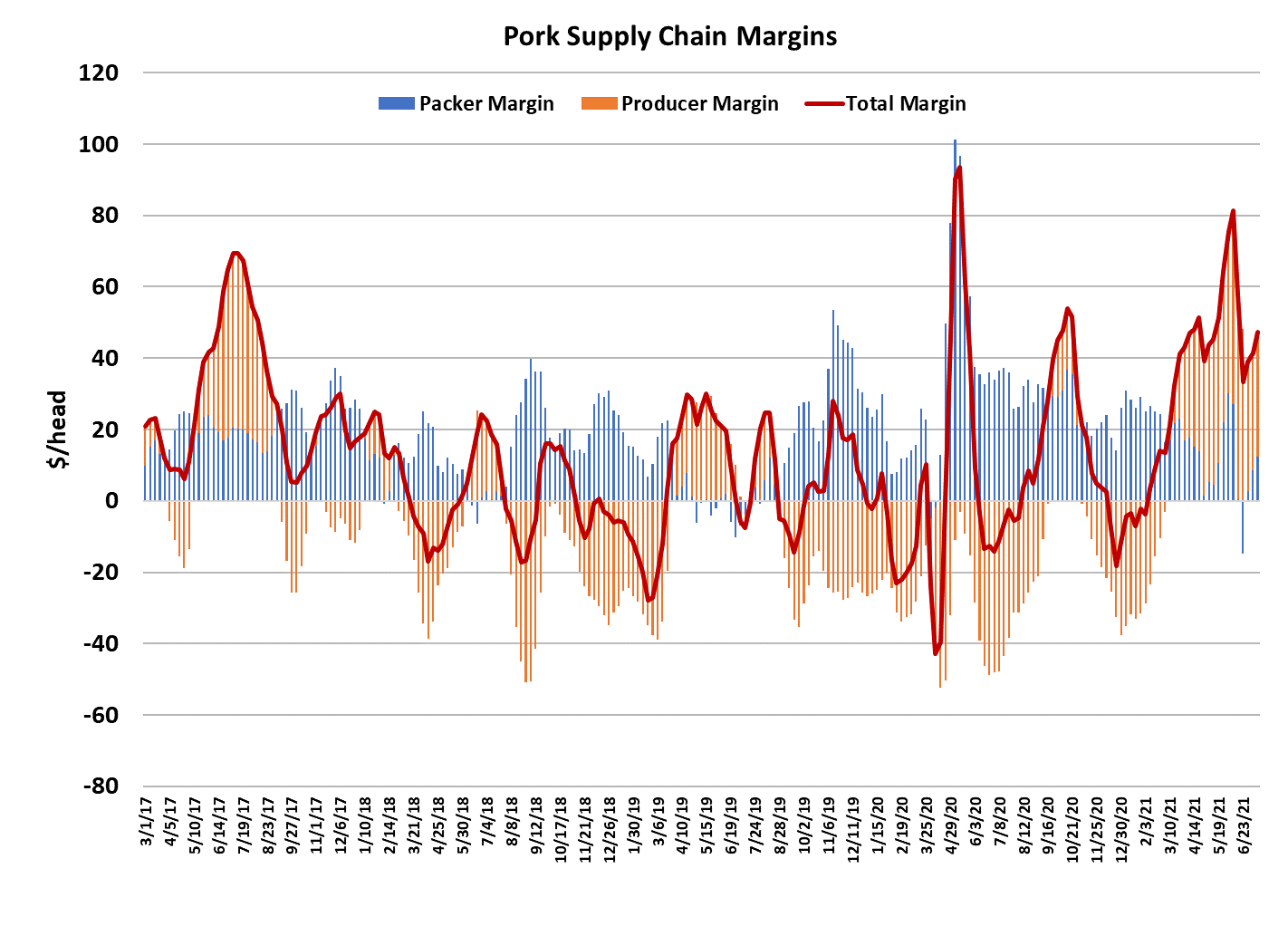

tightest hog supply period of the year. The combined margin chart

below shows an increase over the past two weeks. But rather than call

it a head fake, it looks to me more like a classic head and shoulders

chart pattern, which is considered a bearish indicator. Retailers have

now jacked up retail pork prices to a level that will begin to curtail pork

consumption at retail and that will eventually reverberate through the

wholesale market. USDA reported retail the retail price of pork for June

at $4.55, which is an all-time high. Retail prices never got to this level

during the PEDv problems of 2014, nor did they get this high last year

when COVID was closing packing plants.

If this doesn’t slow pork movement out of retail, I will be very surprised.

This slowing of demand will happen just as hog and pork supplies are

beginning to expand. The gains will be gradual through the balance of

July, but will accelerate in August to the point where the industry should

be killing close to 2.55 million head per week by the time Labor Day

arrives. Retailers will likely be slow to lower prices, given what they

have just been through over the past six months, and that sets up a

situation where wholesale prices could fall dramatically in September

and October. Helping to offset that will be the government’s latest

version of stimulus payments, which are directed at families with

children. Lower income households will receive a minimum of $250 for

each child, each month, for the next 12 months.

That is a substantial boost and there is a good chance that the

Democrats will extend the payments for several years to come in a

separate bill yet to be passed. Families are typically big meat

consumers and so this money will hit in a good spot for the pork

industry. We should watch closely to what happens to red meat

demand over the next couple of months as these new payments get

incorporated into family budgets.

If this spring provides any indication, it should have a strong

positive impact. I wouldn’t look for the program to return pork

demand to the levels that we saw this spring, but it will probably

keep it higher than pre-pandemic averages. International demand

for US pork is beginning to look like it may be in trouble. The

weekly export data has been weak lately and movement to China

has been declining rapidly.

Net-new sales to China in this morning’s report were actually

negative, meaning that there were more cancellations than new

sales to that destination. This bears close watching because the

export market is currently absorbing more than 30% of US pork

production and if China goes back to importing minimal amounts of

US pork, it will leave a lot more that needs to be consumed through

domestic channels (at lower prices, of course). So, the

fundamental tea leaves for the hog and pork complex are a bit

murky at present. On one hand we have very small kills and light

carcass weights propping up the market, but both will be expanding

soon. We have weakening domestic and international pork

demand, but also a new government spending program that could

boost pork demand. Rapidly declining beef prices will also tempt

retailers to shun pork in favor of beef over the next couple of

months.

My guess is that the overall direction of prices for both hogs and

pork is lower, once July is behind us and maybe sooner. Once the

tightness in supply starts to fade, I think the lower price trend will be

more evident. Near-term however, we could easily see a few more

dollars added to the cutout and cash hogs before that turn takes

place. Futures traders apparently see it the same way, as the

August hog contract, which becomes the nearby tomorrow after

July expired today, is trading about $8 under the current index.

The August cutout futures are pointing lower also, down around

$112. Next week, watch for some softening in the cash hog

markets. That would indicate that the packer’s near-elimination of

the Saturday kill is causing producers to fall behind on their

marketings. Also, watch the belly primal because that seems to be

the main mover of the cutout recently.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}