Pork Wrap July 15

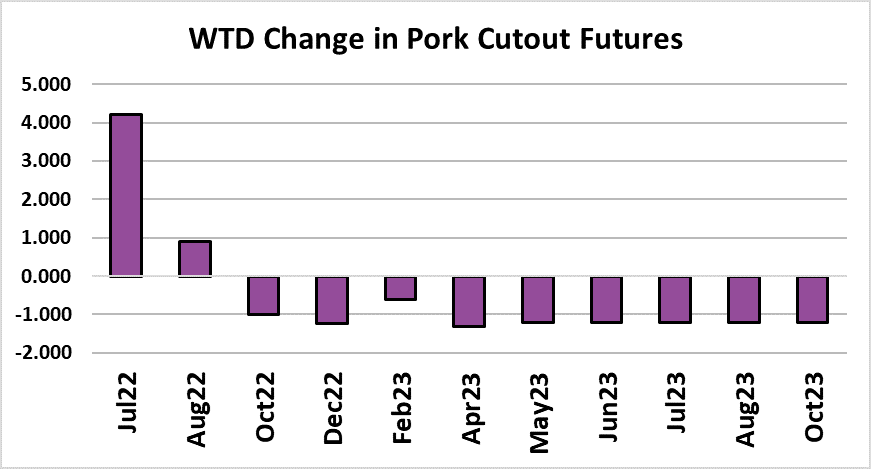

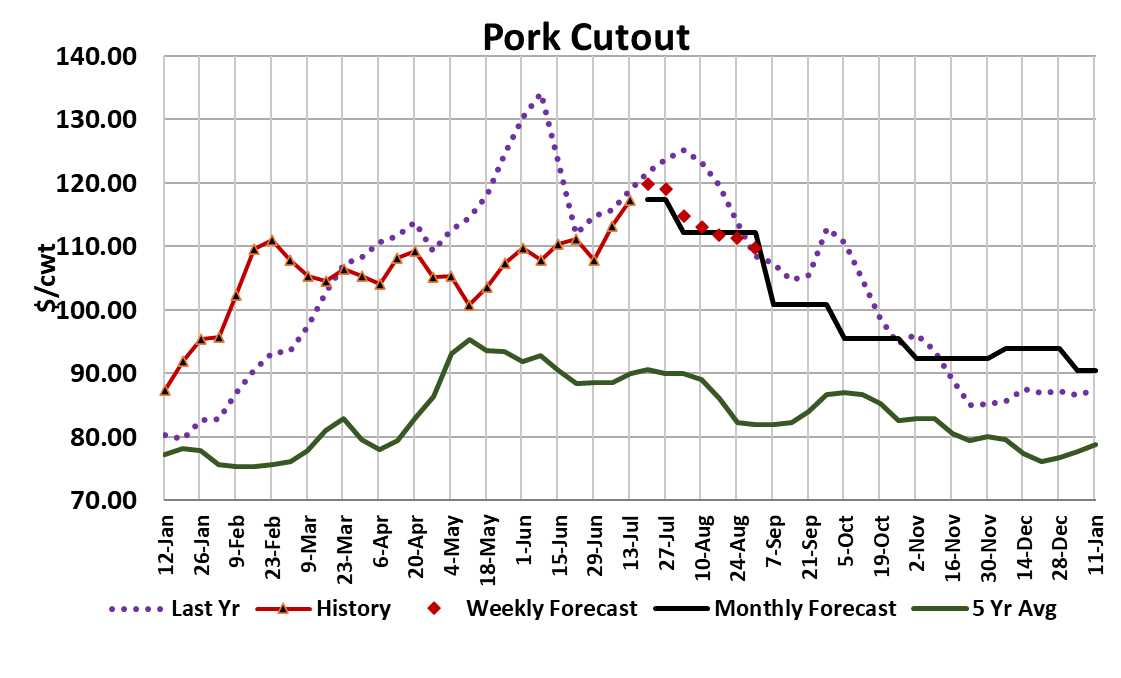

The pork cutout surged higher this week, gaining $4.13 through

Thursday to reach $118.51 and demolishing my theory that last

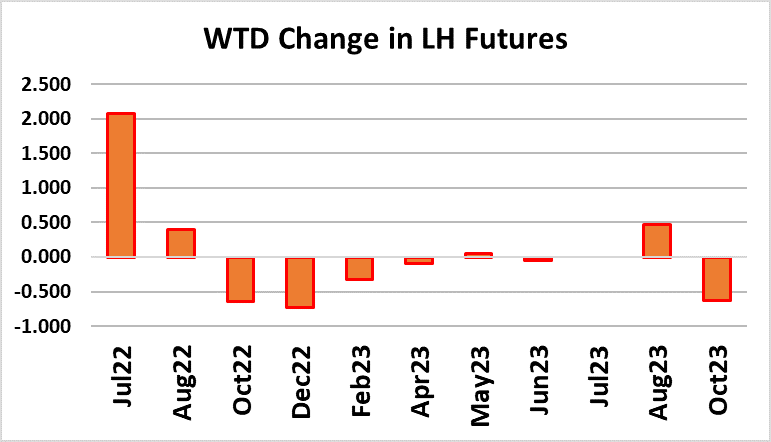

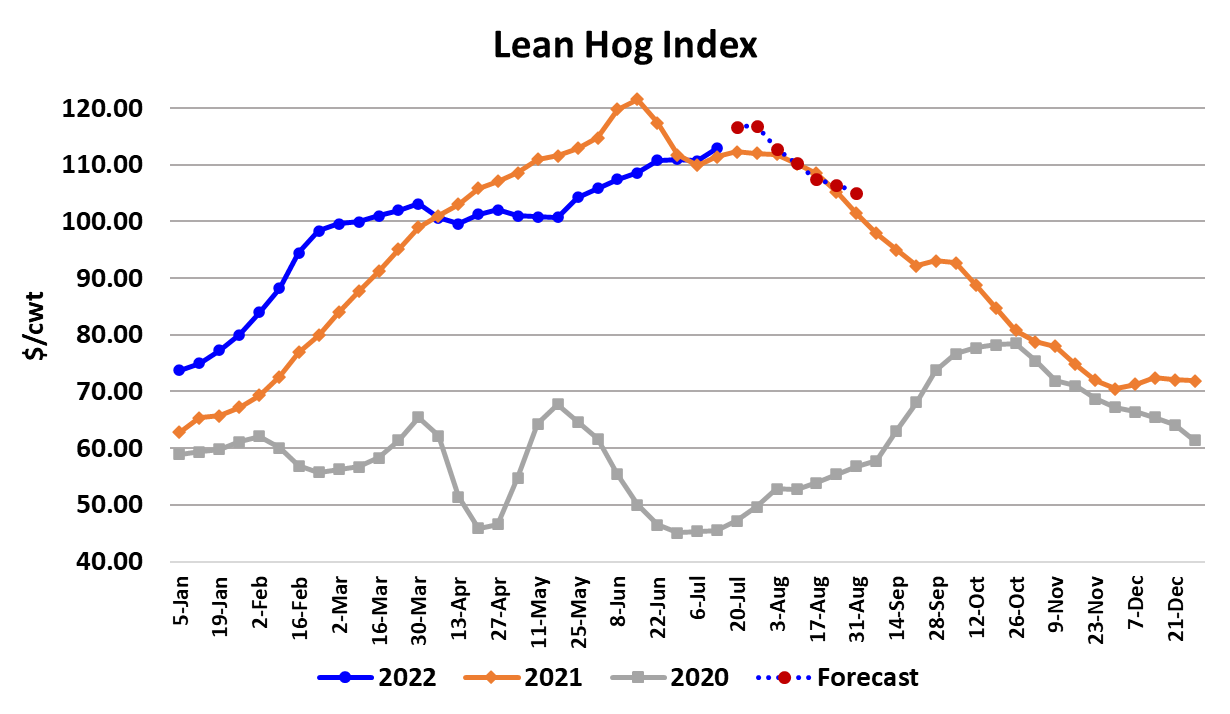

week was the top in the cutout. The LHI gained $2.21 through

Thursday as it reacted to the higher cutouts and should have at

least another $2 worth of follow-through if nothing else

changes. The negotiated hog markets were stalled this week

and the NDD average through Thursday was down about

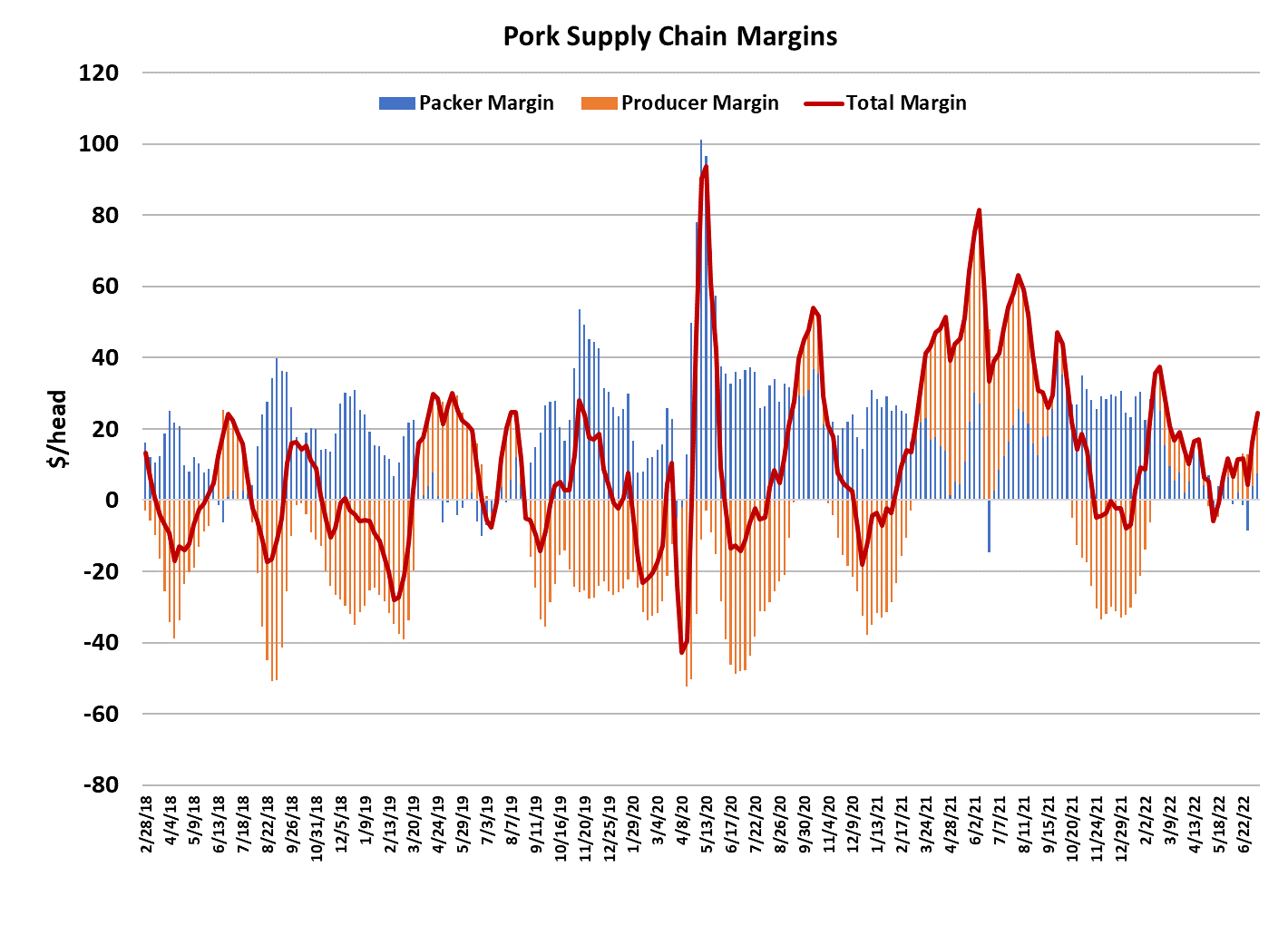

$0.55/cwt. That allowed packer margins to expand with the

cutout and I have margins averaging a little over $7/head this

week. As a result, packers are likely to continue to bid

aggressively in the negotiated markets and it wouldn’t be

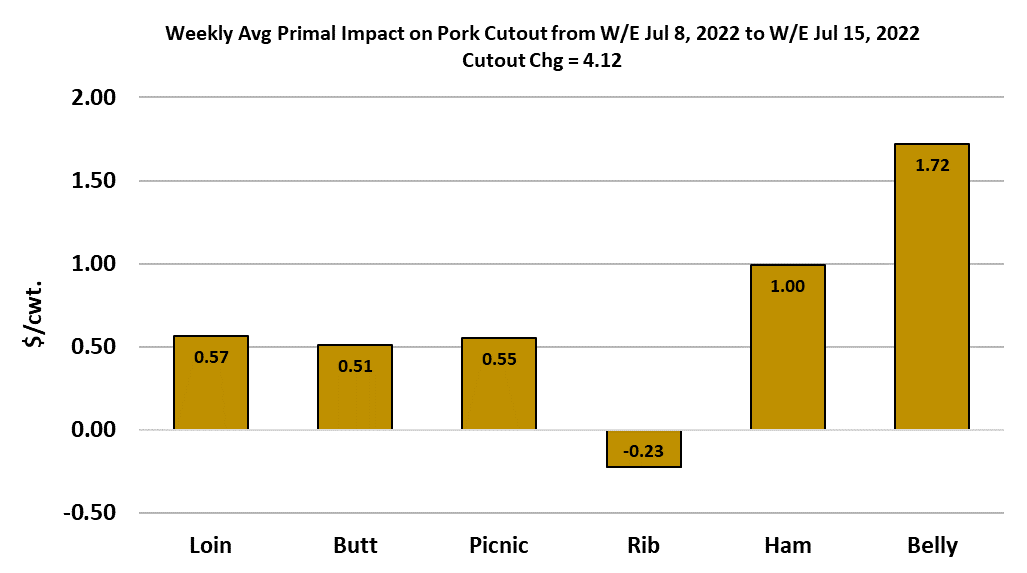

surprising to see them gain some next week. The processing

items led the way this week, with both bellies and hams moving

higher. Together, the belly and ham primals make up 41% of a

hog carcass so when they start moving in the same direction it

is a powerful force.

23/27 bone-in hams were quoted over $118 on Wednesday

and through Thursday the weighted average was $108.31.

Clearly, someone was needing bone-in hams pretty badly. The

belly move higher was less surprising, only because the bellies

were rather lethargic during June and were overdue for an

increase. It is worth noting that the retail primals also posted

gains this week and that could just be from a general tightness

in availability coming off of the holiday week. When we put it

all together, it equates to a strengthening cutout and the big

question is whether or not this week’s momentum can be

continued. The sharp increase in the cutout moved the

combined margin higher and makes it look like perhaps a new

demand upcycle is starting.

The timing of that is a bit surprising to me, but it is difficult to

argue with the data. So, it is possible that we might have to

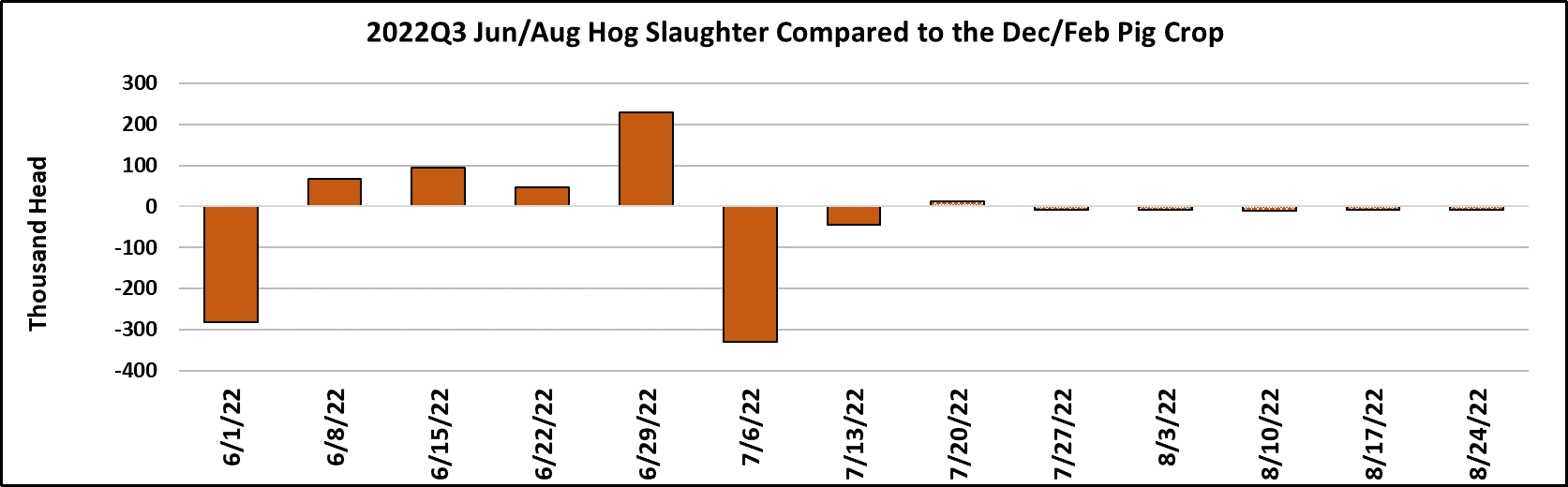

wait a little longer to see the cutout top. Slaughter levels will

likely remain pretty constrained in the next few weeks, so the

amount of supply side relief for prices should be limited. I’m

projecting this week’s slaughter at 2.27 million head, which is

just a hair smaller than the week leading up to Independence

Day. If that forecast is correct, then this week’s kill would be

almost dead-on what the pig crop implied. Now that packers

have a little margin back in their pockets, they might look to

expand the kill next week, provided they can find the hogs.

They will need to walk a fine line because if they press it too

much, they run the risk of accelerating the negotiated market

higher.

All of this renewed price strength happening right before the July

expiration has been a problem for the bears and it now looks like July

will expire close to $115. This week’s price action has also caused

me to revise most price forecasts higher. I now see fair value for Aug

somewhere close to $110, but there is a very real risk that it trades a

lot higher before that. There is some very warm weather forecast

for the next two weeks in the Midwest and that creates a concern

about hog weights falling faster than expected and thus reducing the

available supply of market-ready hogs in the near term. That has the

potential to be price supportive at a time when prices are already

rising. I am factoring that into my forecast for the Aug futures and

buyers should be watching the weather forecast closely in the next

couple of weeks. USDA released its estimate of retail pork prices for

June this week and the average price was up almost $5/cwt to

$493.10.

That is another all-time record and I don’t expect that retailers will be

lowering prices much, if any, until after Labor Day when they should

be seeing much more favorable wholesale pricing due to larger

slaughter levels. The macro picture remains pretty dismal, with

equity markets moving consistently lower and increasing fears that

the Fed will send the economy into a recession this fall as it raises

rates to battle inflation. Eventually, those things will matter to pork

pricing, but right now seasonally small supplies and weather issues

far outweigh demand concerns. Hog and pork prices are rising fairly

fast in China and that raises the potential that they will purchase

more pork out of the US, but so far we haven’t seen any indication of

that in the data. If they do become bigger buyers of US pork, they

would likely wait until fall when price levels should be much more to

their liking.

A very strong US dollar could work to discourage pork exports and

encourage imports in the second half of the year. Traders in the corn

market are watching the weather situation carefully too. Corn futures

are well off of their highs, with new crop corn trading around $6/bu,

but the next couple of weeks encompasses the critical pollination

phase for corn and if it is too hot and dry during that period, yields will

suffer. I estimate that the drop in corn prices, along with rising cash

hog prices, has helped restore profitability to the hog production

sector, where margins are now around $17/head. Next week, watch

the weather above all else and keep an eye on the hams and bellies

too because they are the engine that has been responsible for the

recent upward burst in the cutout.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}