Pork Wrap July 14

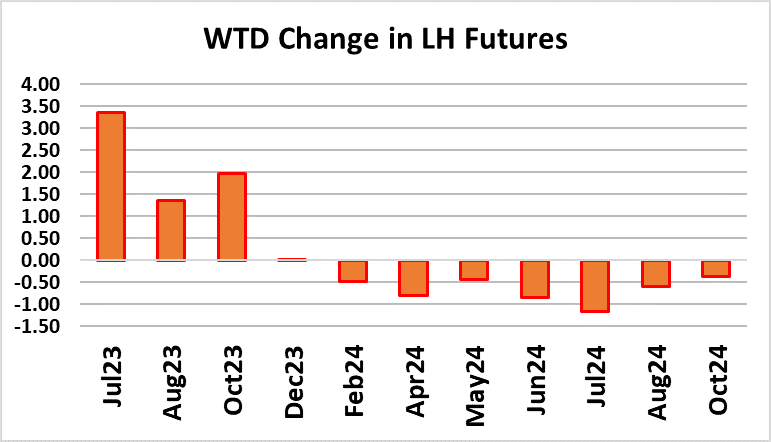

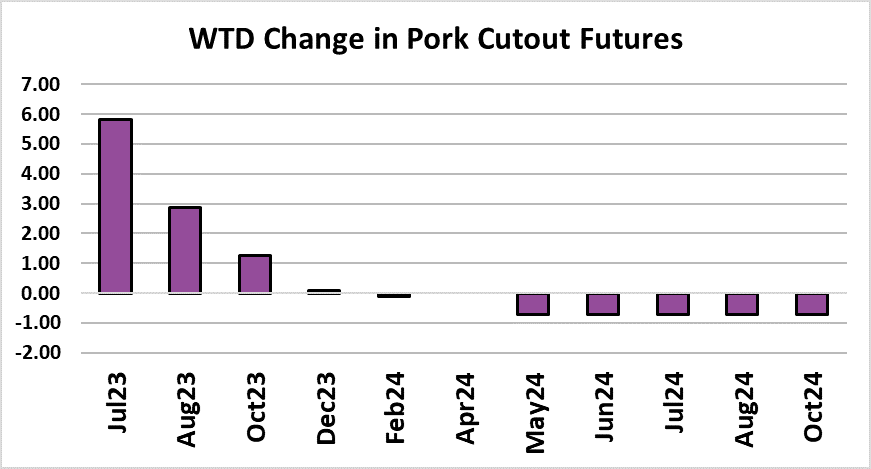

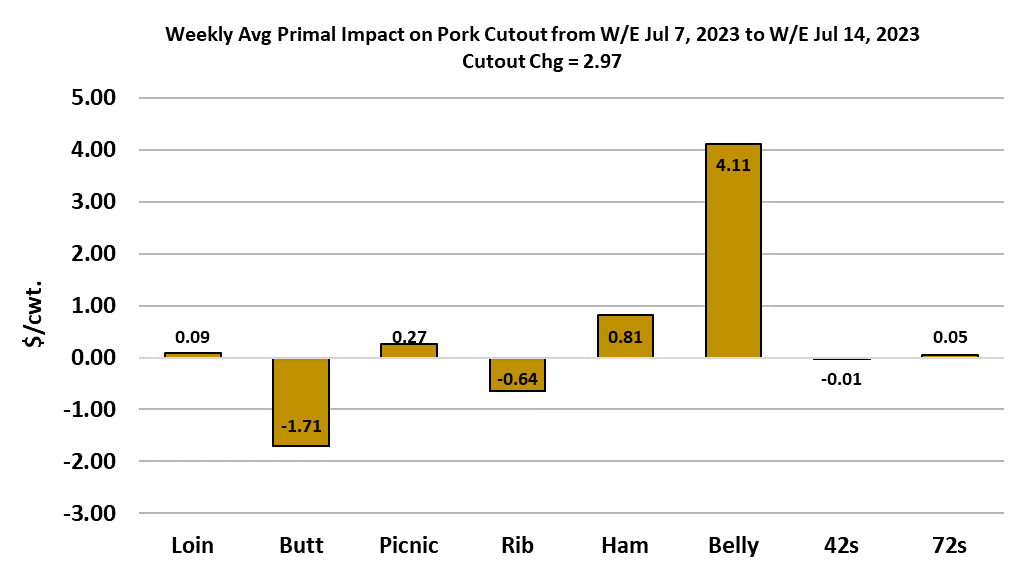

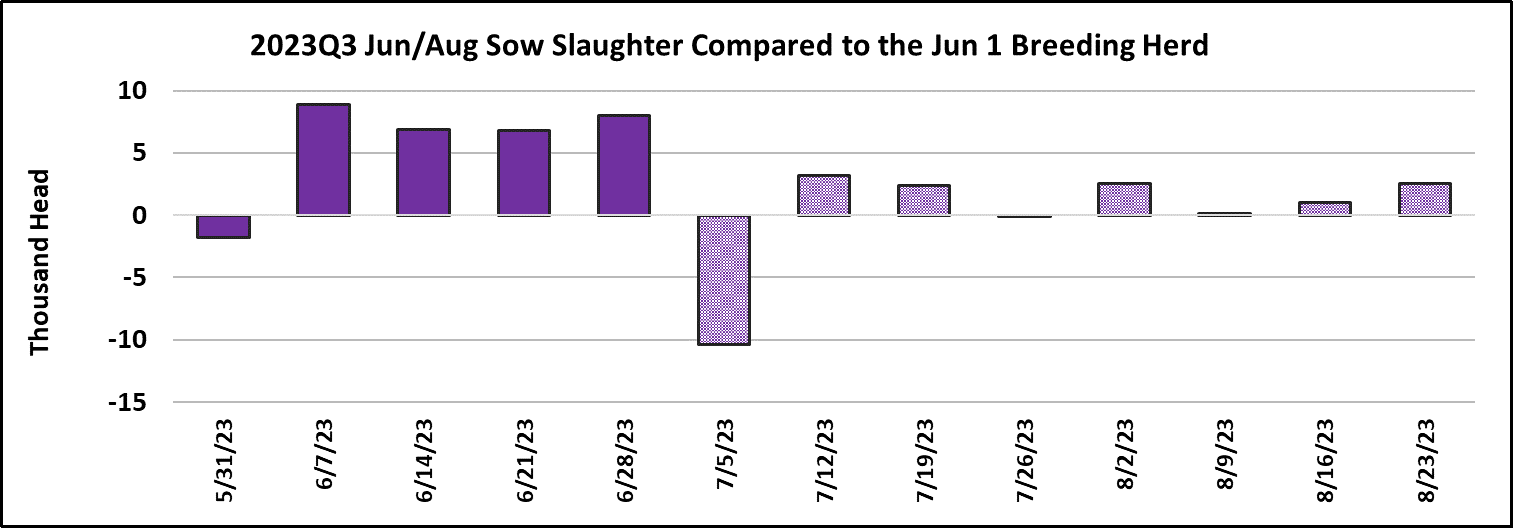

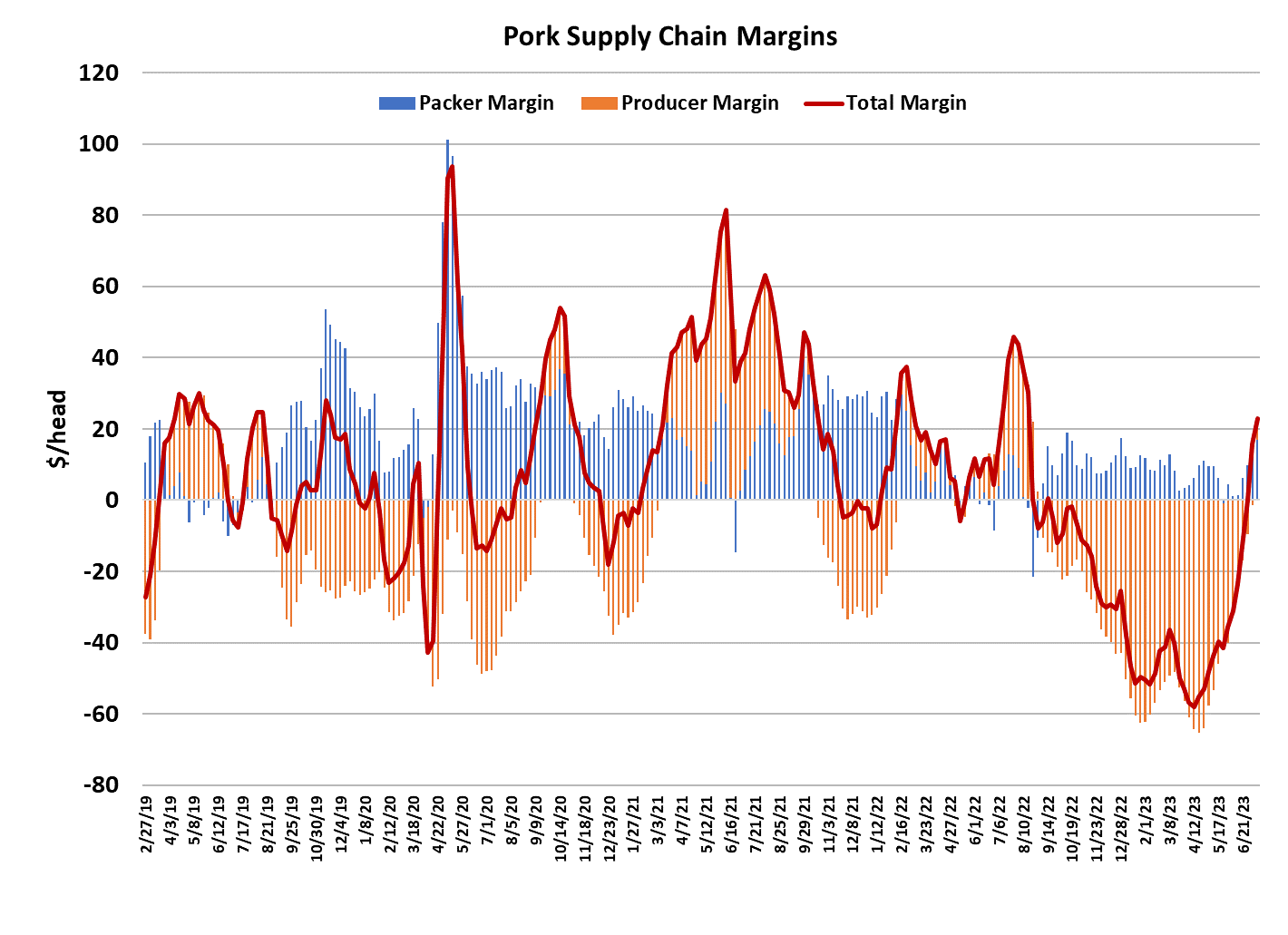

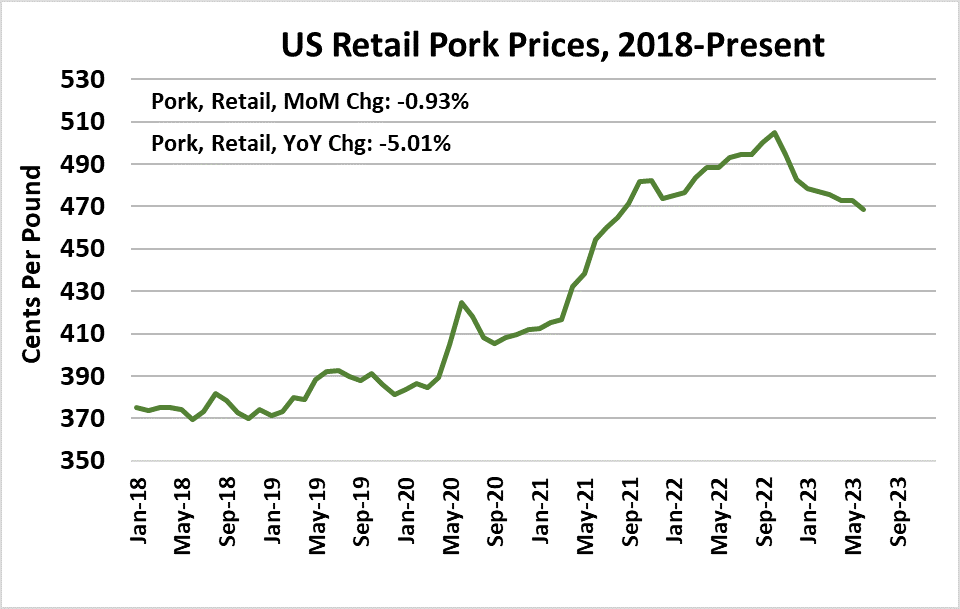

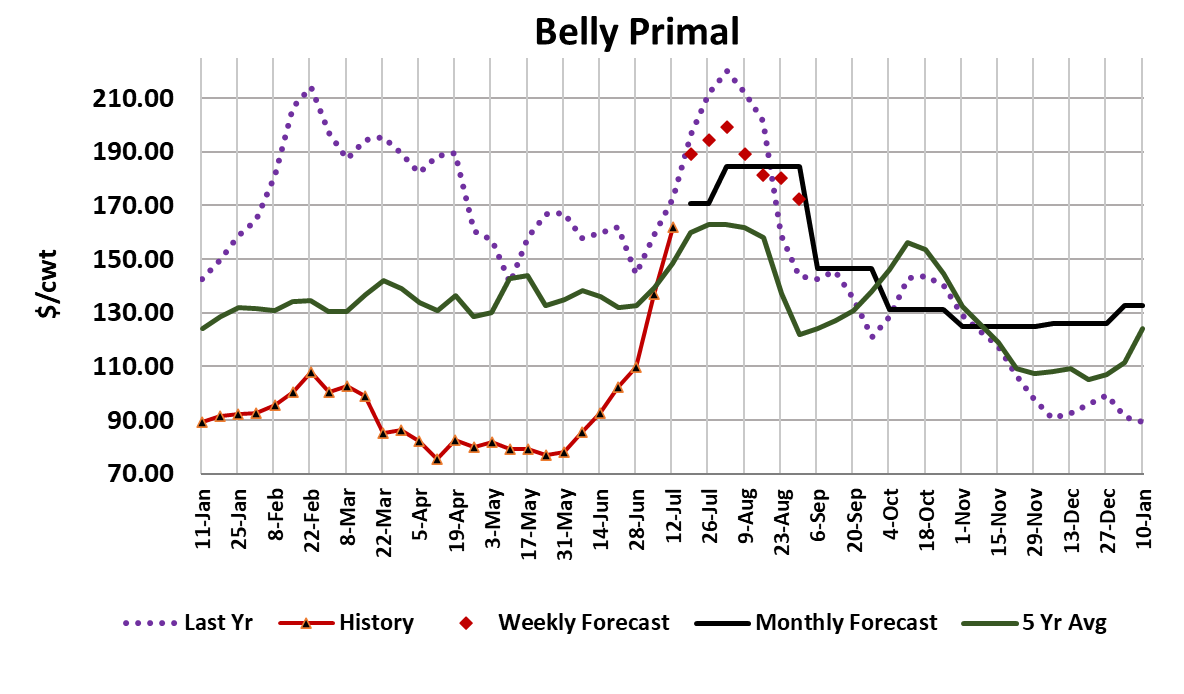

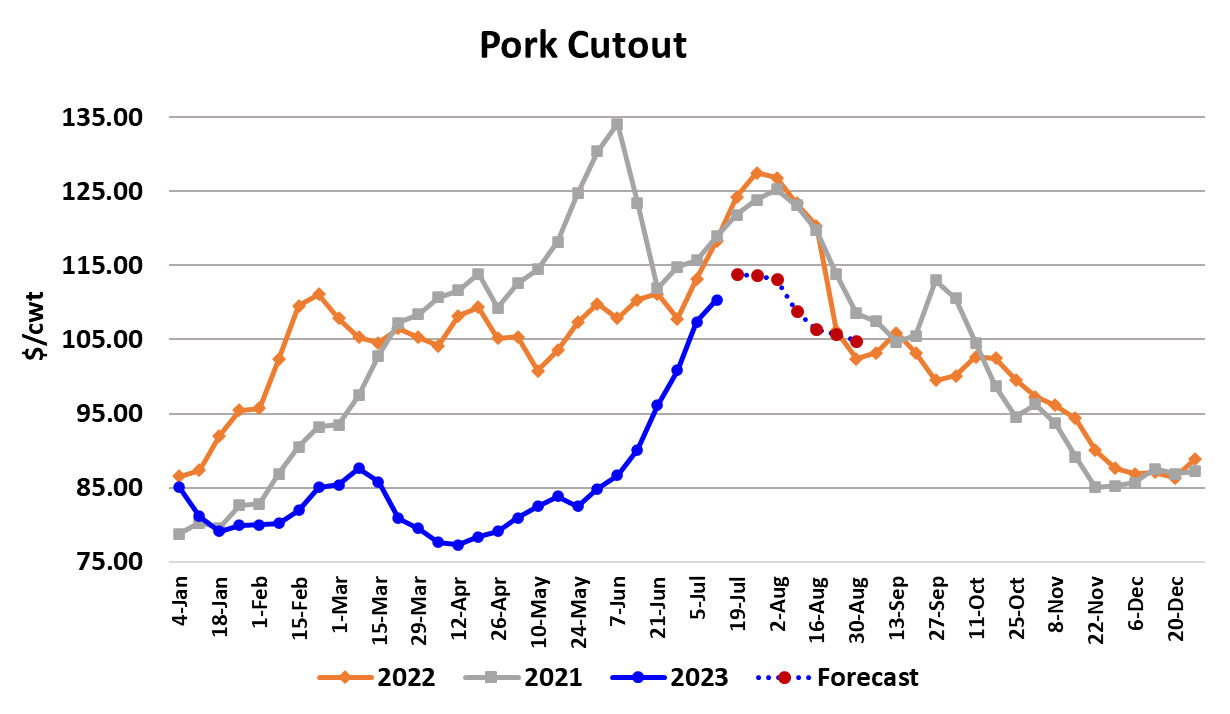

Prices in the hog and pork complex continued on their upward trajectory this week, with the cutout adding almost $3/cwt through Thursday on a weekly average basis, and the WCB negotiated market gaining a little over $2/cwt. This week we saw several instances of triple digit cash hog prices, with the peak reported price at $102.28/cwt. By my calculation, that should be enough to cover all production costs and leave producers with an average margin near $6/head. That is quite a victory considering how dismal things looked back in April/May. Packers are also doing quite well as their margin held near $17/head for the second week in a row. Thus, the combined margin continued moving higher and you can see from the attached chart that it has moved back into a more normal zone after the dreadful spring drawdown. Bellies and hams continue to be the driving force behind the recent gains in the cutout, but that is being partially offset by significant price declines in the butt primal. Futures traders appeared to be caught off-guard earlier this week when a noon cutout printed over $112/cwt and that led to a flurry of buying activity in the soon-to-expire July contract. It now looks like that contract is on track to expire somewhere in the $102-103 range. You may recall that just before Memorial Day the July contract traded down to $74, so this has been an incredible reversal of fortune over the past 6 weeks. The current demand upcycle began in mid-April and has been running for 13 weeks. That makes it a little long in the tooth, since we normally see these demand cycles run in one direction for only about 8 weeks. However, we could argue that an exceptionally deep demand downcycle might be followed by a longer, and stronger, upcycle than would normally be the case. It is easy to tell that some futures traders want to start betting on demand to turn lower and that is evidenced by the almost $6 discount that the August contract is currently carrying to the July contract. Further gains in the cutout are almost certainly contingent on how much more strength the bellies and hams can muster because the retail cuts look like they may soon be running out of gas. The sharp downtrend that the butts have entered into probably has at least a couple more weeks to run. Loins are slowly working higher and that could continue for the balance of July, but I don’t get the impression that they are going to post very large gains at this point, and once kills begin to increase in August then we should see loin prices turn lower. So, it all seems to ride on the bellies and hams. The good news for bulls is that the bellies could have a lot more room to run. It looks as though this week’s average for the belly primal will be in the low $160s and the fundamental forecast has it continuing higher toward a top near $200 before easing lower in August. This week marks the first time the belly primal has traded over its 5-year average since September 2022. Hams could also continue to firm up, but probably don’t have near the upside potential that bellies have. I would give them maybe one or two more weeks of strengthening before they start to work lower. There are some interesting dynamics going on inside the ham complex. Boneless hams seem to be struggling much more than the bone-in items and that is a big reversal from the pandemic when tight labor supplies limited boning capability and thus we saw the boneless trading at very sharp premiums to the bone-in. Mexico is a big buyer of bone-in hams and that may be what is driving the price strength in 23/27 lb hams, which were quoted on Thursday at $107.52/cwt. One would think that as the bone-in hams get more expensive, the boneless would too, but so far that doesn’t seem to be the case. When I put all of the primal forecasts together, I get a cutout forecast that tops around $115 in 2-3 weeks and then slowly works lower to about $104 at the end of August. It won’t all be demand weakness however, because slaughter levels should start to increase from about 2.35 million head per week at present to 2.5 million head per week at the end of August. USDA reported FI carcass weights down another pound today and they probably will decline another 2-3 pounds before they bottom near the end of July. The DTDS weights continue at record low levels, which makes me think that producers are current on their marketings and will likely be able to keep cash hog prices moving higher for a few more weeks. It is a bit of a mystery to me how the hog supply can be so current, yet packer margins are $17/head in the middle of July. Maybe it is attributable to the dramatic move in belly prices combined with packer discipline in not trying to push the kill too hard at this time of year. One other piece of good news is that USDA reported retail pork prices were lower again in June, further helping pork’s competitive position in the meat case. Next week, expect further modest gains in the cutout and negotiated hog market. Keep and eye on those belly and ham prices because they are the key to continued improvement in the cutout.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}