Pork Wrap July 12

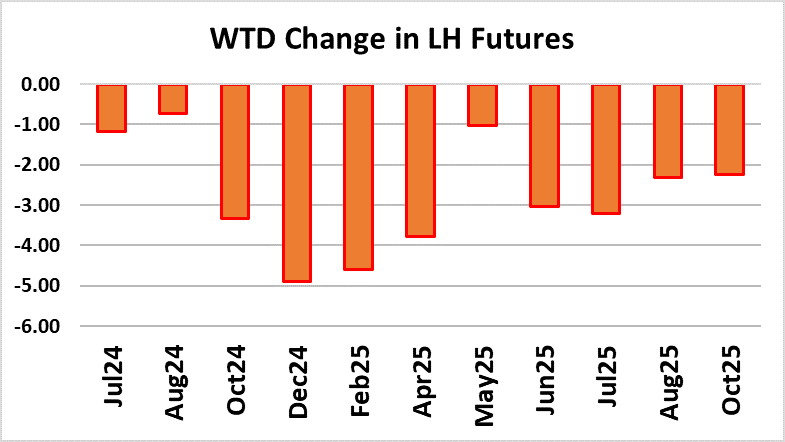

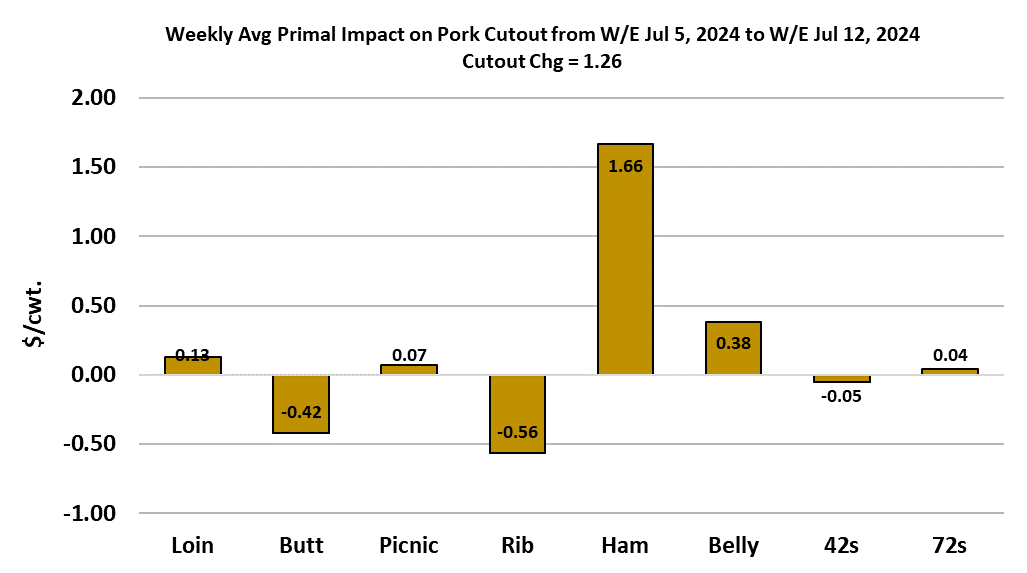

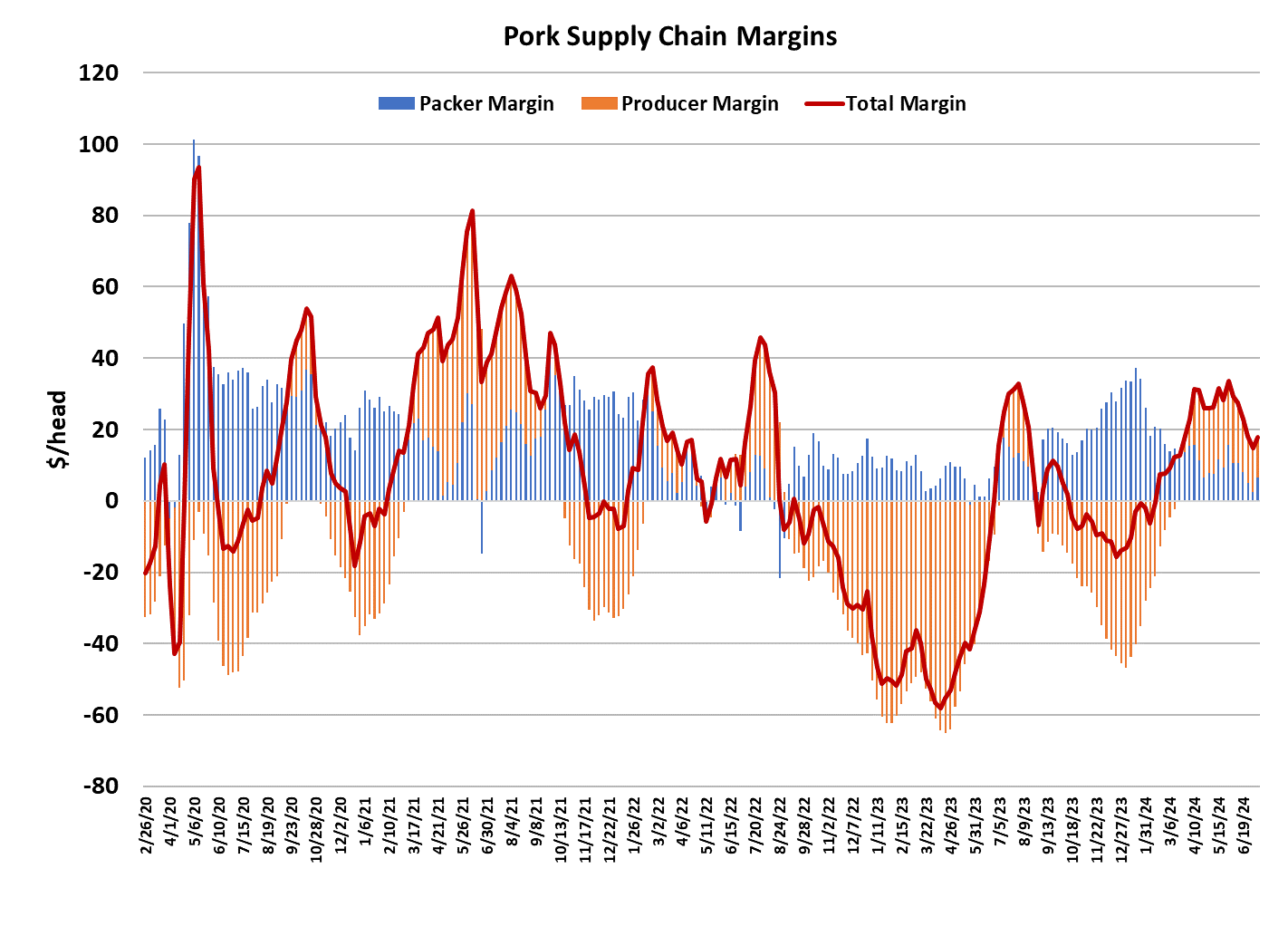

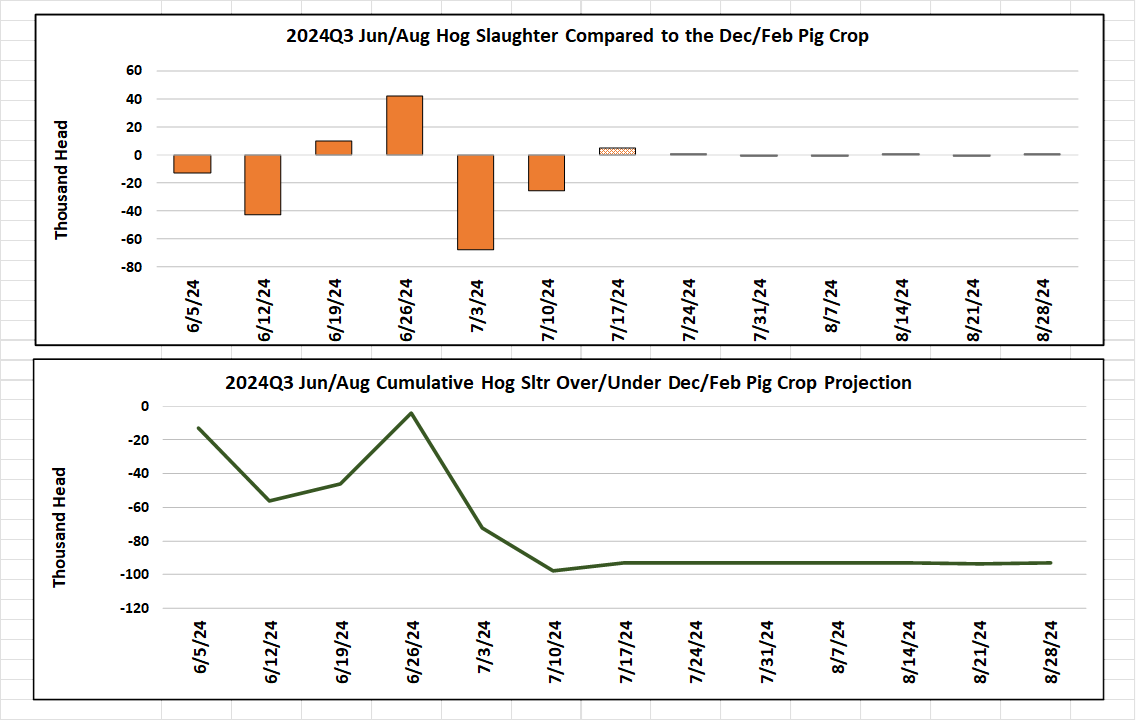

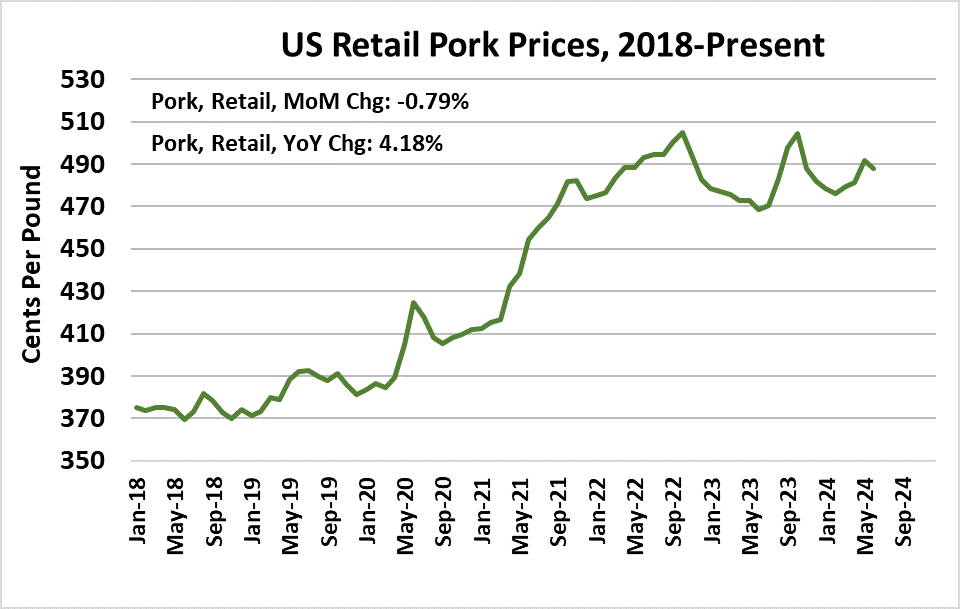

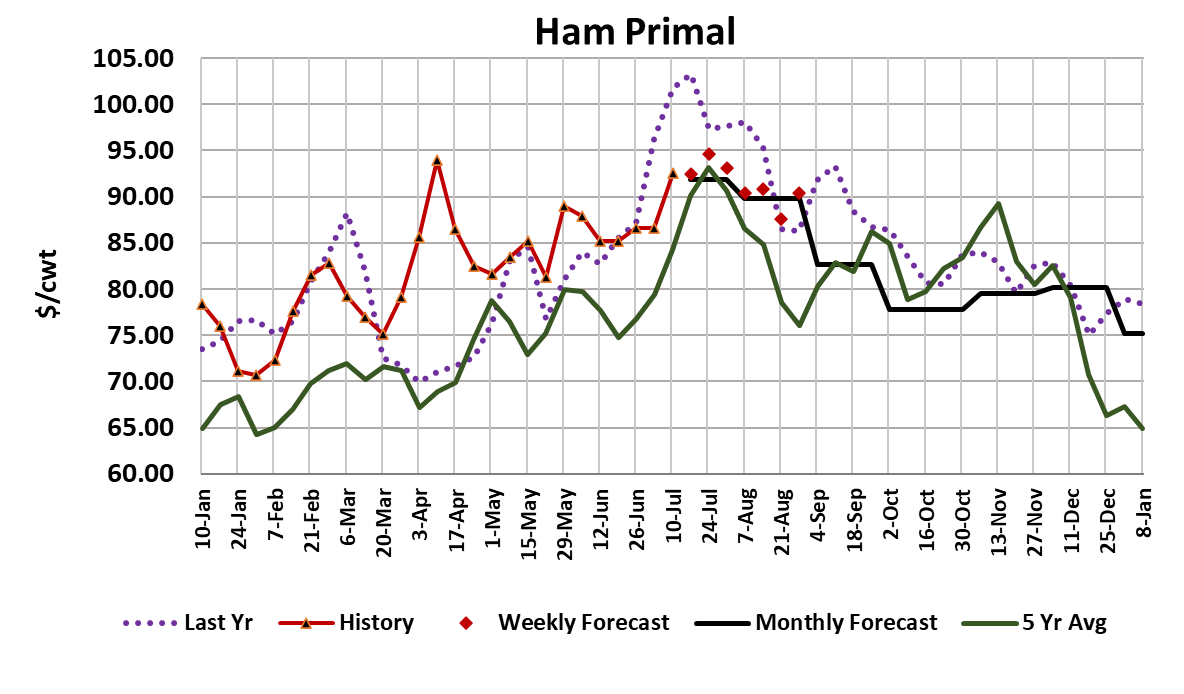

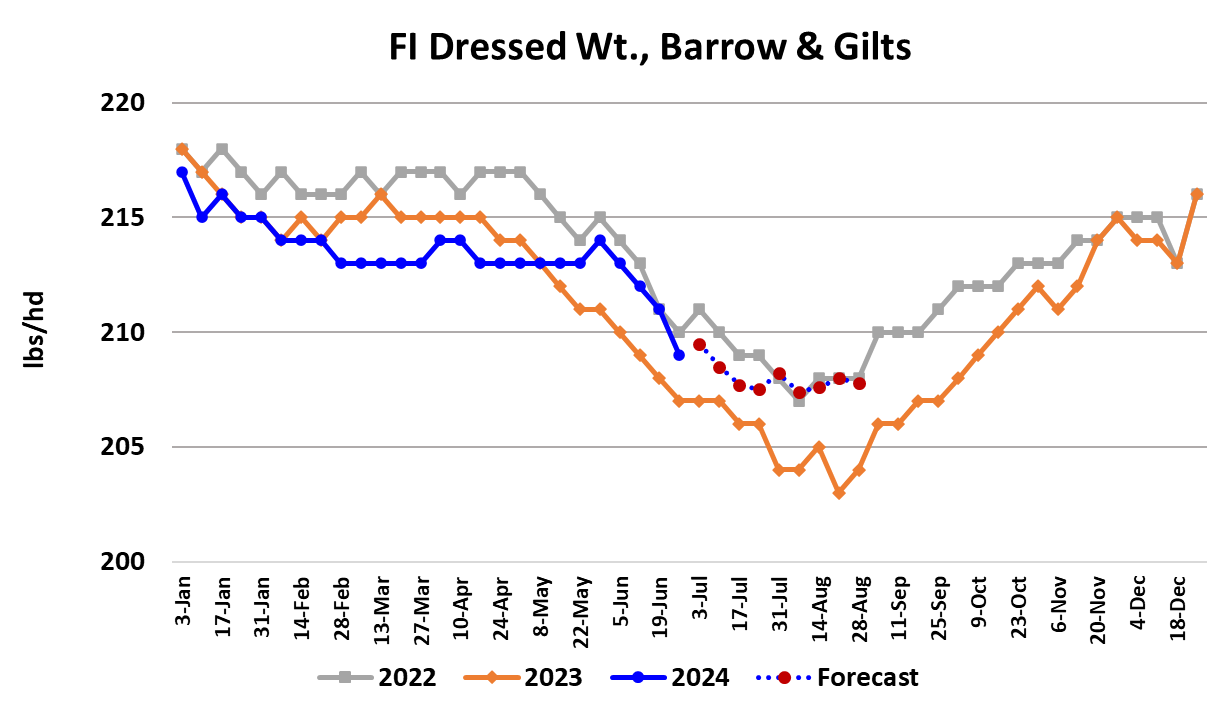

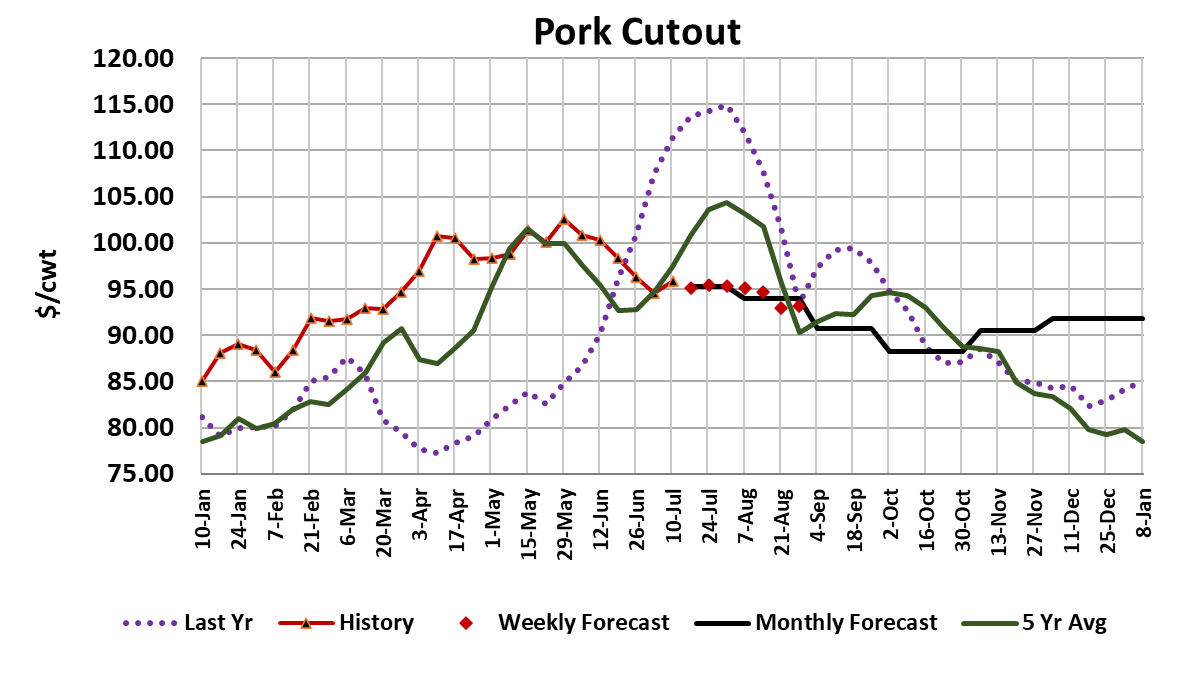

After watching their margin compress over the past few weeks, pork packers finally got some good news as cash hog prices eased while the cutout moved higher. I estimate this week’s margin near $6.50/head, up about $4 from the week before. The cutout added $1.26 on a weekly average basis as it moved to $95.83. The increase was facilitated by sharply higher pricing in the ham complex, with a little additional help from the bellies. The ham primal has a strong tendency to make its annual top near mid-July, so the increase isn’t all that surprising. But beware, it also has a strong tendency to drop hard once the top has been made. This week’s sharp gains were probably also helped along by the holiday-reduced kill in the previous week as processors may have been short on raw materials. With the hams on the go, all eyes are now on the belly primal, which added a little over $2 this week, but still remains at very depressed levels. Bellies also have a strong seasonal tendency to move higher at this time of year. Unfortunately for the bulls, the retail primals didn’t do much this week and, with kills expected to slowly work higher from here, there is risk that they will fail to advance much from current levels, and may be at risk of continuing their slide lower. While the cutout surprised with a modest gain this week, the negotiated hog market surprised as prices softened. The WCB spot market averaged $87.57 this week, down $3.73 from the week before. Perhaps some hogs were backed up after the short kill week and needed to be cleared, or maybe supplies are already starting to expand seasonally. Whatever the cause, it is a bit concerning to see cash hog prices turning lower this early in July. Hog prices often respond positively to the cutout, so if the cutout can hold its gains early next week, perhaps the cash hog market will mount a recovery. Monday is the final day of trading for the July LH futures and it looks like the LHI will be near $88.50 at expiration. The July contract will expire lower than the Apr, May or Jun contracts did, which is pretty unusual. With that kind of trend in place, it is hard to be too optimistic about the Aug expiration. This week’s slaughter came in at 2.39 million head, just a tad below the 2.42 million kill that we saw prior to the holiday week. Kills so far this summer have been generally consistent with what USDA estimated the Dec/Feb pig crop to be, so there isn’t much concern about suddenly finding a lot of additional hogs that need to be killed. However, that Dec/Feb pig crop was rather large and so it is unlikely that non-holiday kills will dip much below this week’s level as we move through July. By early August, kills should be expanding at a strong clip. Barrow and gilt weights dropped two pounds this week to 209, but that is part of the normal seasonal, so it doesn’t generate much concern at this point. We are still watching the weather closely and it looks like the hog producing regions in the Midwest could be in for some above-average temperatures next week, but the forecast isn’t calling for a heat dome to form over the area so it probably won’t turn into a big problem the hogs in the near-term. Overall pork production is expected to average 4-5% stronger than last year through the balance of summer and that creates a pretty big supply-side headwind. Exports have looked a little better in the weekly data and we are hearing that hog prices in Mexico are on the rise, so perhaps that will help availability manageable over the next few weeks. The combined margin ticked a little higher this week, but that isn’t enough to declare the downtrend over. We often see small changes of direction that get reversed in following weeks. My thought is that the combined margin will continue to ease until it reaches the zero line and it is more likely that producers are the ones that will be giving up margin rather than packers as animal numbers start expand seasonally. When the combined margin goes into decline, that is often a sign that near-term demand is softening and thus there is less margin available to be shared between the two segments. Overall pork demand isn’t all that great to start with, so if further softening occurs over the next few weeks that could take the industry to a pretty dark place. Of course, many would assert that the industry is already in a dark place when we have July futures expiring at $88. One piece of good news was that retail pork prices for June were reported down slightly from the month before, which is a bit of a relief given the big increase that was reported for May. Retail pork prices are now 4.2% stronger than last year. Next week, the hams will command a lot of attention as we try to ascertain if that primal can add to the gains it posted this week. Bellies too will be in focus on hopes that perhaps they will give us at least one modest rally before summer evaporates. Cash hogs are likely to improve if the cutout can manage to add to its gains, but otherwise sideways might be a better call there.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}