Pork Wrap July 1

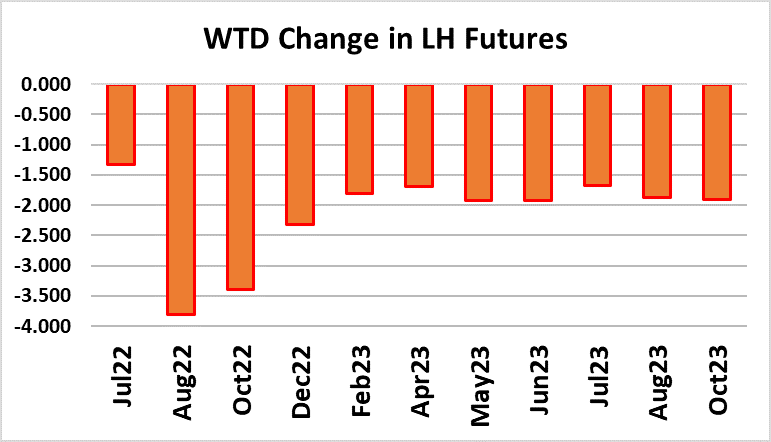

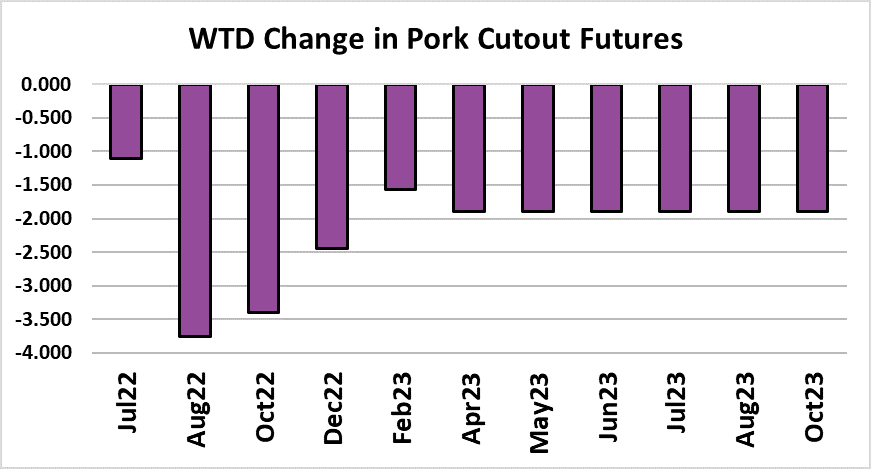

The hog and pork complex eased a bit this week as the cutout

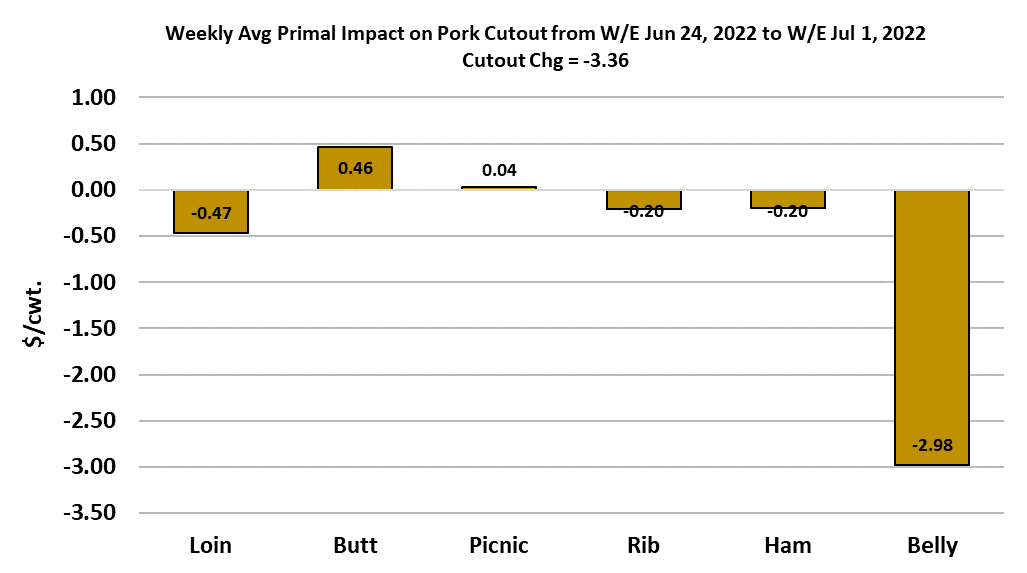

dropped $3.36/cwt on a weekly average basis and the WCB

negotiated hog market was down $1.15/cwt. The LHI, which lags

the other markets, was actually up about $0.30/cwt on the week.

I think most of the easing in the negotiated markets can be

attributed to packers having less demand for hogs due to the

holiday, which should be transitory. The softening in the cutout

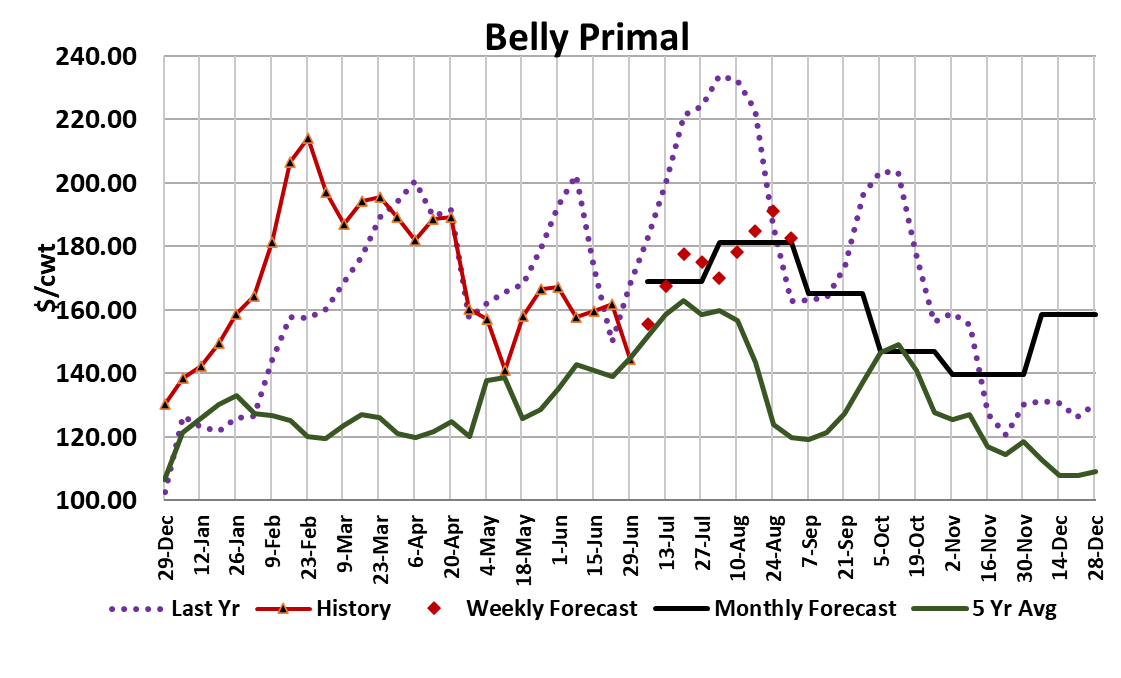

can almost entirely be traced to the belly primal, where a very low

print on Tuesday afternoon set the tone for a lower average for the

week. The belly primal averaged $145 this week and there have

only been 4 other weeks so far in 2022 where the average has

been lower. Given that we are currently at the tightest production

of the year, it makes sense to me that bellies have more upside

opportunity than downside risk at this point. On the other side of

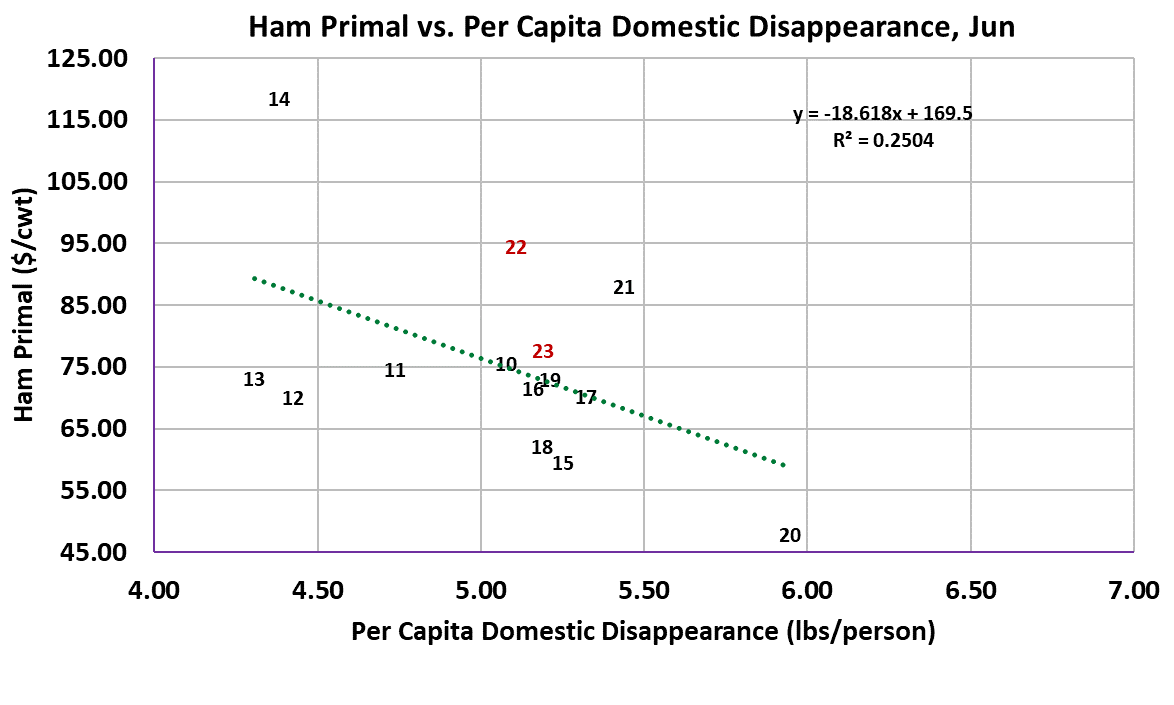

the spectrum, we have hams, which held up valiantly this week and

are very close to their highest point so far in 2022.

The small production around Independence Day may keep these

from showing too much weakness in the near term, but as we get

further out into July, I expect that hams are going to retreat. The

butts, which I’ve highlighted recently due to extraordinarily strong

pricing, averaged a little higher again this week but near the end of

the week they were trading lower and the weekly chart seems to

be suggesting that the butts are making a top and will soon move

lower. It seems likely that the other retail primals such as loins and

ribs are going to ease over the next few weeks as kills start to

slowly increase and pork demand has to contend with the dog days

of summer. That keeps the cutout on a downward trajectory even

if the bellies do manage a rally as expected. I’m not looking for

rapid collapse in the cutout just a slow easing in the average of

$1-2 per week

Futures traders don’t seem to agree with that in the near-term, as

they are pricing the Jul cutout futures close to $111, which would

be about $3 higher than this week’s average cutout. Perhaps they

are anticipating a bump in the cutout due to the short kills and I

have to concede that is a distinct possibility for next week, but by

the time we get into settlement week for the Jul contract production

will have expanded back to normal and the cutout should be

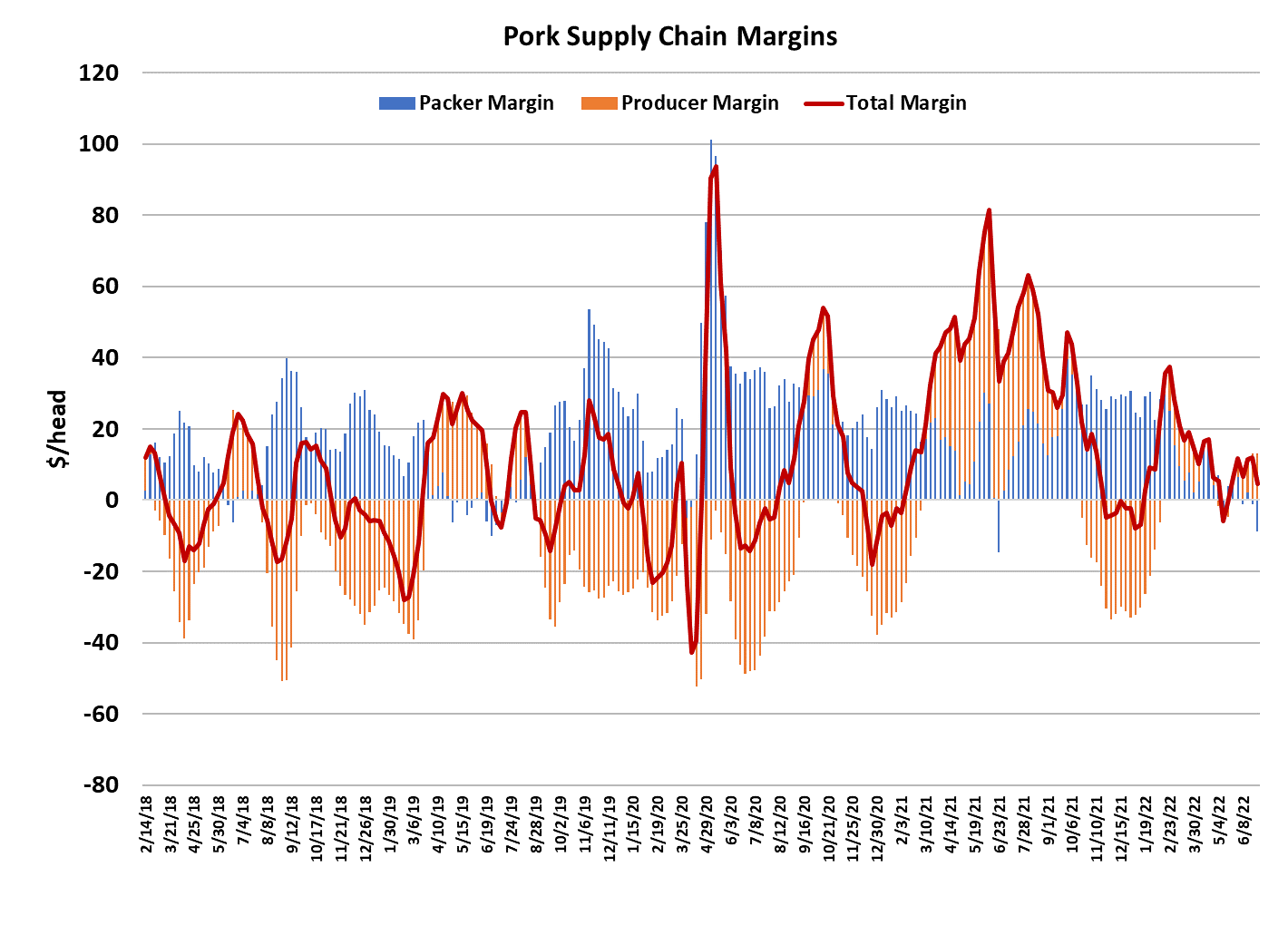

moving lower again. The combined margin appears to be making

a top now, which could be a signal that softer pork demand is on

tap for the balance of the summer months. This week’s slaughter

registered 2.29 million head as packers pulled back on the Friday

kill and reduced the Saturday kill to a paltry 9000 head. It is a long

weekend for a lot of pork plant workers. Monday’s kill should be

almost zero, but look for packers to push next Saturday’s slaughter

above 100k in order to help offset some of Monday’s lost

production.

Even so, we are likely to see next week’s kill fall below 2 million head.

When that happened last year for the Fourth of July, both the ham

and belly primals posted impressive gains. Processors likely let

inventories run a bit low ahead of the holiday and thus will need to refill

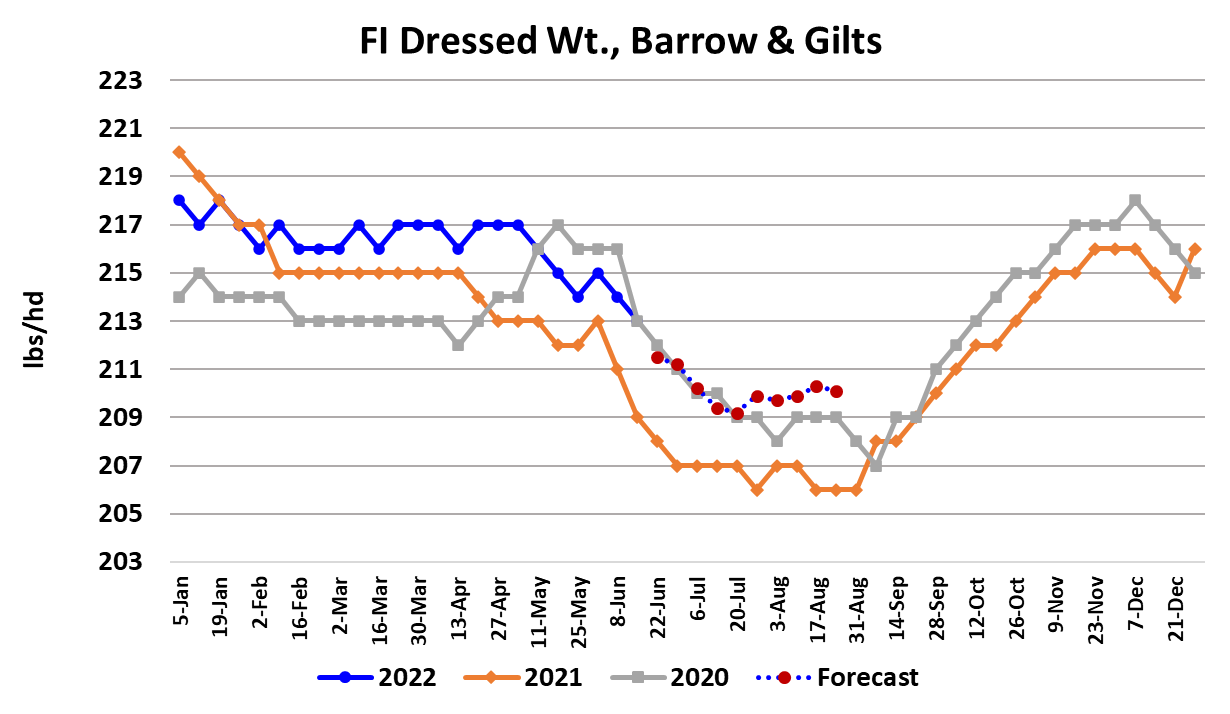

right when production is at its lowest. Barrow and gilt carcass weights

were reported another pound lower this week and are likely to post a

1-2 pound decrease in next week’s data. This is all part of the normal

drawdown in weights that happens during the summer. The weather

forecast for the Midwestern production regions seems rather benign

until about the middle of July, when the chance for above normal

temperatures increases. That is worth keeping an eye on, but the

reliability of weather forecasts much beyond 7-10 days is low. There is

not much new happening on the trade front. Pork exports appear

to be holding in a mostly sideways pattern and now we are getting to

the point in the calendar where we saw big export declines last

year, so the YOY comparables are not as stark as they were earlier

this year.

Hog and pork prices are slowly rising in China, but I really don’t think

they are near the point where it would generate a material increase in

purchases from the US. The bigger risk is that relatively high summer

pork pricing will cause a modest decline in Mexican purchases. This

week’s Hogs and Pigs report showed that producers added 70,000

breeding animals between March 1 and June 1, which is a bit

surprising given the high feed cost environment that was in place

during that period. That was more than I had been expecting prior to

the report, so adopting USDA’s numbers caused some modest

declines in my distant pork price forecasts. The March/May pig crop

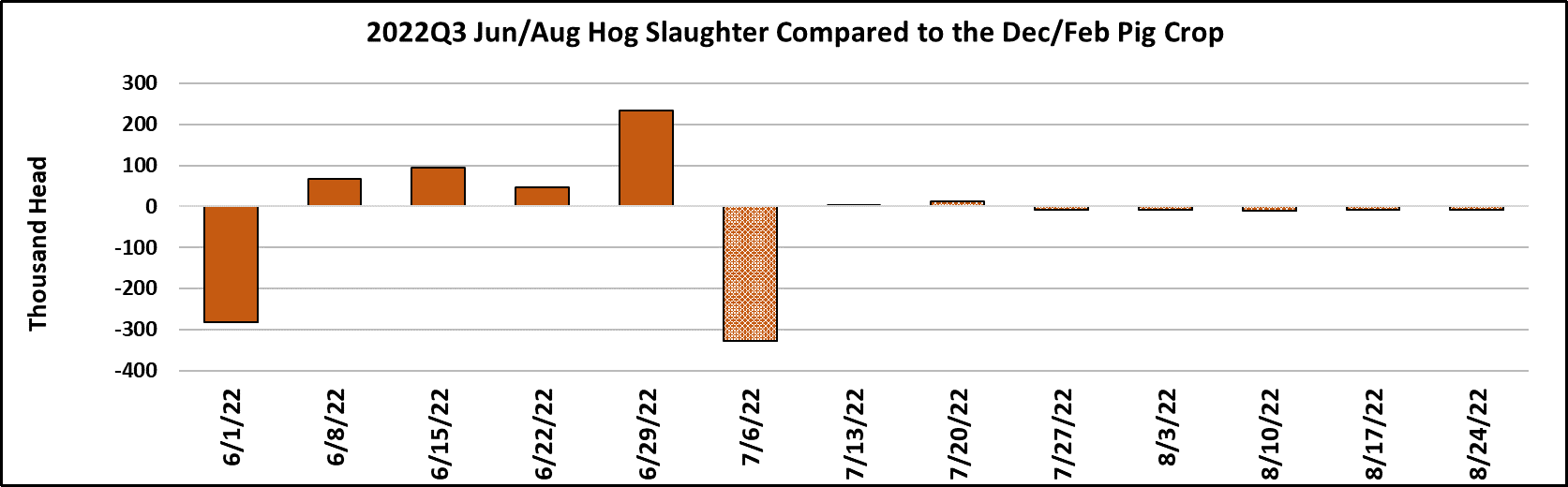

was reported down 1% YOY and those will be the animals that

come to slaughter during the Sep/Nov quarter this fall. The Dec/

Feb pig crop had been reported down 1% also earlier this year and

so the market has adjusted to working with a slightly smaller hog supply

and the new report confirms this is likely to continue through the

balance of 2022.

So, there doesn’t seem to be much in the way of supply side

surprises for the hog and pork complex over the next six months or so.

Disease problems are often confined to the winter and spring quarters,

so they don’t create a lot of uncertainty in summer and fall either. I

think it will be the demand side that holds the most potential to surprise

us in coming months and if I had to guess, that surprise could be that

demand is softer than most expect given all that is going on in the

macroeconomy. Next week, watch for a belly rebound on holidayshortened production and also keep an eye out for a rebound in the

negotiated hog markets as packers look to get back to a full kill

schedule after Monday

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}