Pork Wrap January 9

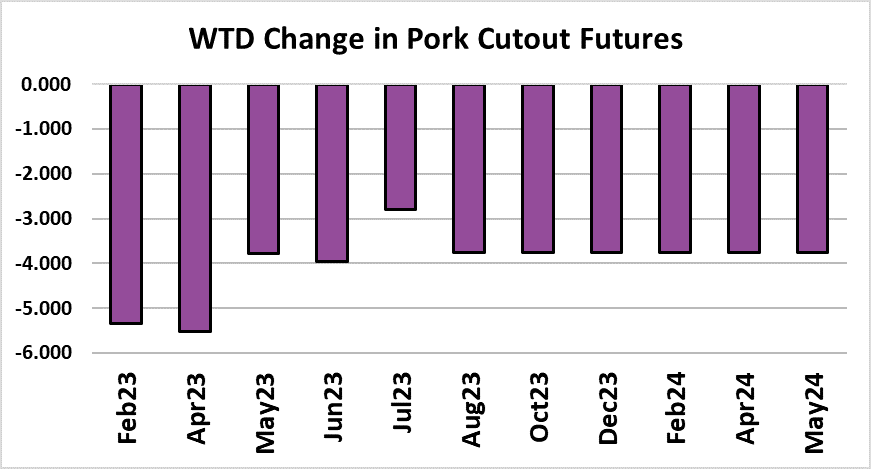

The pork cutout lost another $3.81/cwt. this week as both bellies and

hams failed to gain any traction following the holidays. If the cutout is

losing $4 this week after three short kill weeks, it is somewhat scary to

think what might happen when kills balloon back to normal next week.

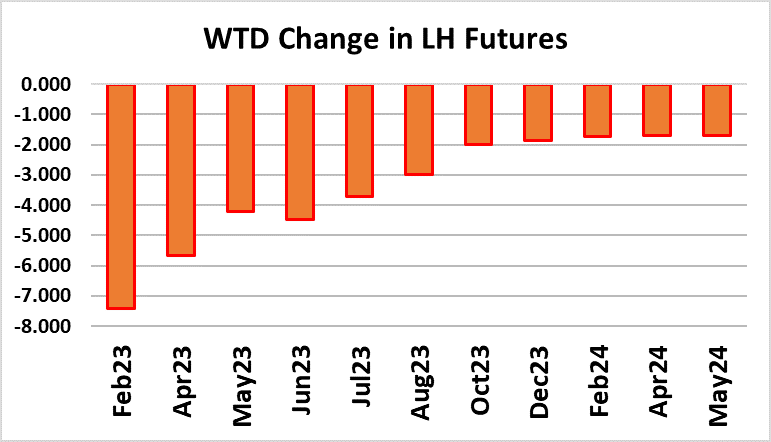

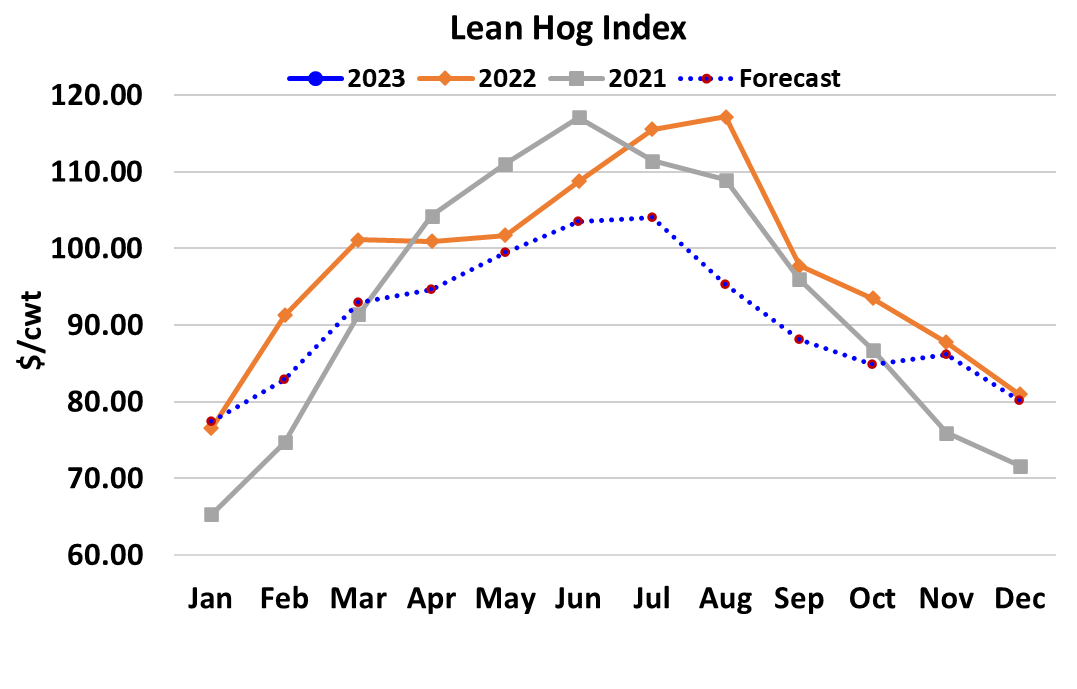

Futures traders acted like they had that fear when they pushed the spot Feb contract down over $7/cwt. this week. Further, because kills

have been so light, cash hogs haven’t been in high demand and prices there have been moving lower also. The NDD negotiated market lost

$1.77/cwt. on a weekly average basis. So, cutout down and negotiated hogs down guarantees that the LHI will go down also, and

it lost $2 this week, with more to come next week. It appears as though, as of Friday afternoon, something close to $76.50 is already

baked into the LHI for early next week. And that is before the pork from this Saturday’s huge 420k kill starts looking for a home. No

wonder futures traders are not very interested in buying this market.

For the last three price cycles, the bulls have stood ready to buy Feb

aggressively after a sell off and it has never really worked out for them.

Now the bulls are either worn out or broke, and the daily chart can’t

buy a green bar. I think part of the problem here is that expectations

were set too high by what happened to the LHI last year when it gained almost $20/cwt. between Dec expiration and Feb expiration.

But early 2022 saw a phenomenal surge in pork demand that just isn’t part of the picture this year. Prior to the extraordinary years of 2021 and 2022, the LHI only averaged a gain of about $3 between Dec

expiration and Feb expiration.

Too many traders were expecting a repeat of last year that just isn’t

going to happen. In fact, it now looks like the LHI at Feb expiration

might be below Dec. Demand for spot pork is soft right now. Bellies,

which really helped the cause last January, are hampered by large

cold storage stocks that processors need to draw down. Hams, which

have been the star performer all through the second half of last year,

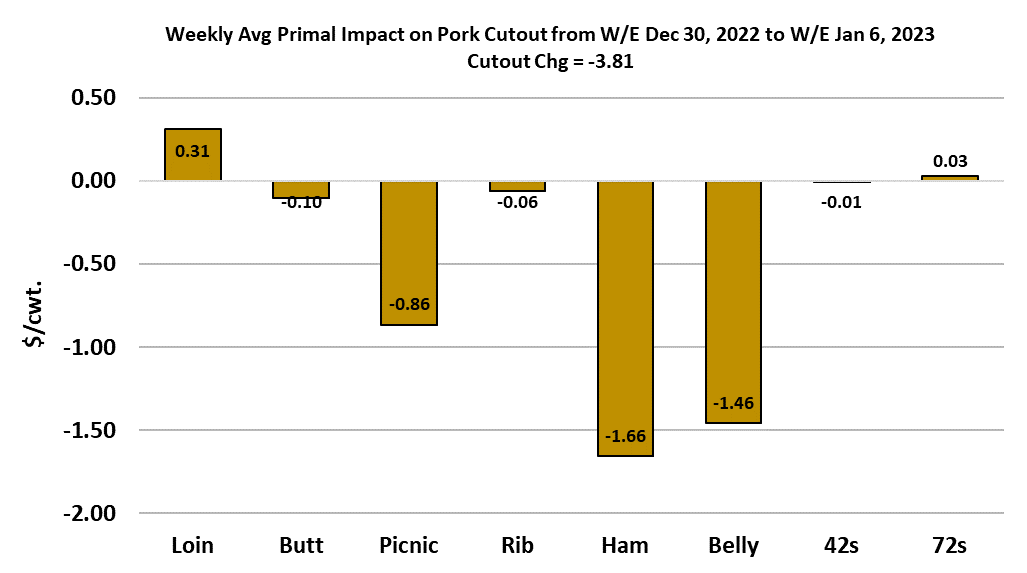

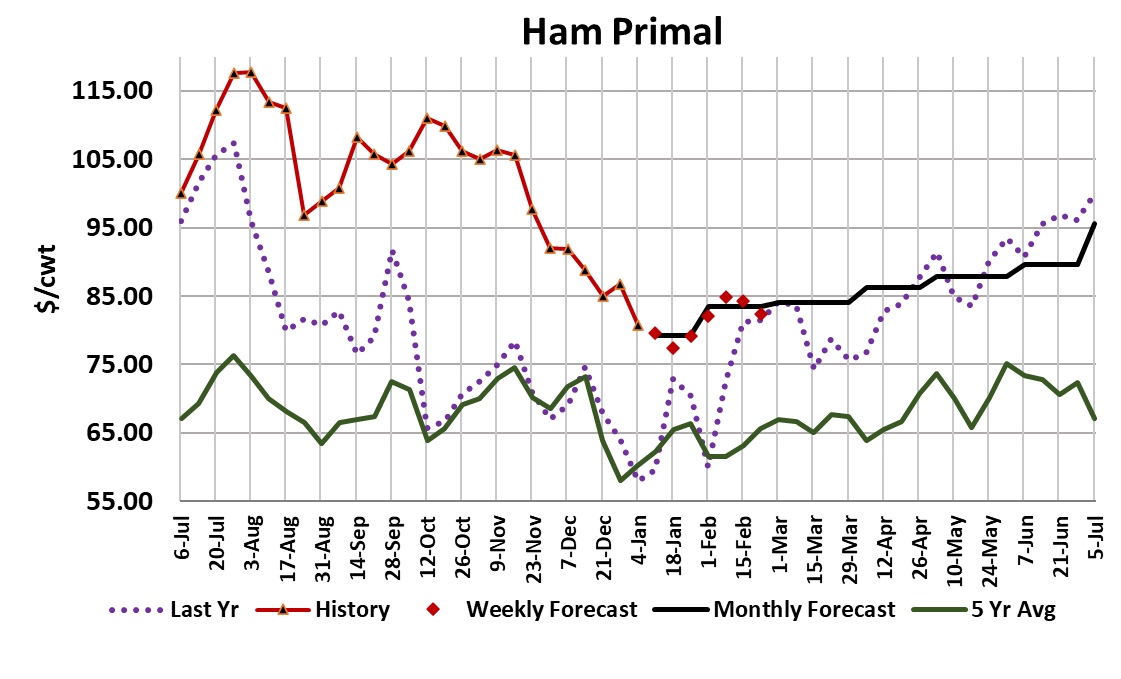

are starting to lose their luster. Notice on the attached chart how the

ham primal has moved much closer to last year and the five-year

average in recent weeks. Packers have been moving large quantities

of hams in recent days, so perhaps the bottom is near unless next

week’s full production schedule takes them even lower. This week’s

kill came in at almost 2.3 million head—not bad for a week that had

almost no kill on Monday. However, packers are really gearing up for next week. At this juncture, I’m estimating next week’s slaughter to

top 2.6 million head, with another very large Saturday kill. If there was

any shortage of fresh pork, that will take care of the problem.

I expect that in order to be able to put together such a large kill, packers

will need to be much more active in the negotiated hog market next week.

Perhaps that will stop the slide in cash hog prices. While 2.6 million

seems very large for January, we need to consider that the way the

holidays fell this year it messed up the normal weekly kill pattern. That is obvious in the over/under-kill chart relative to the pig crop. Packers under-killed this week, so they will over-kill next week and thus the

negative and positive bars mostly offset one another so that the

cumulative kill so far in this quarter is only about 50k over what the pig

crop implied. Thus, it’s not accurate to blame the recent price weakness

on more hogs that expected. I think that blame lies squarely at the feet of the demand side.

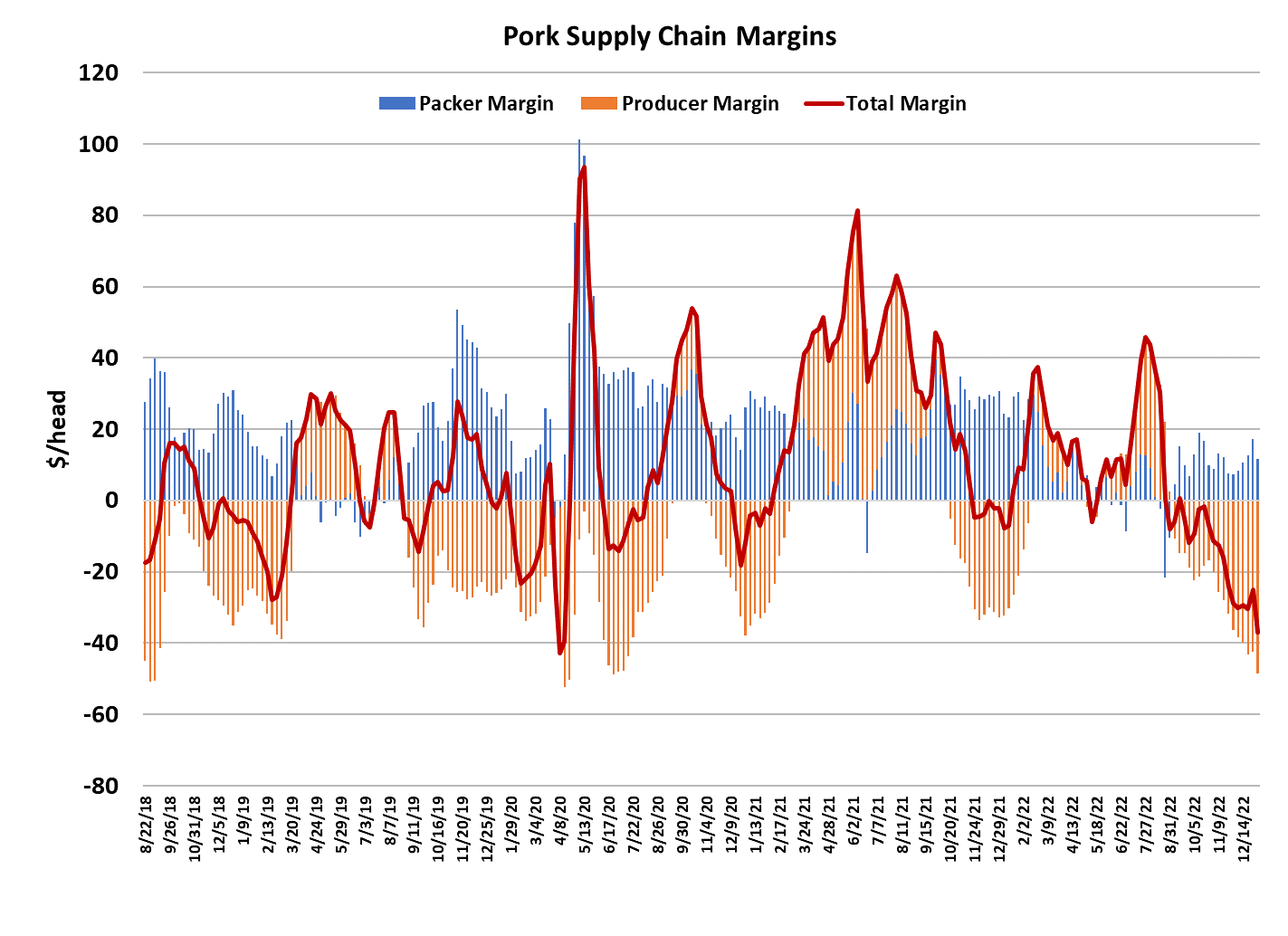

The combined margin chart is about as ugly as it gets. Right now, I

estimate producer margins are about -$45/head and high corn prices are largely to blame. Back in the summer when the LHI was routinely over

$100/cwt., producers did pretty well, but now that the LHI is heading for

the $75 level, they are taking a pretty big financial hit. Cash corn prices in Iowa are a little lower now than they were back in the summer, but not by

enough to offset the huge difference in hog prices. The five-year average

for producer margins in the first week of January is -$27/head, so that

gives an idea of how much worse the financial situation is this year. This certainly won’t encourage expansion in the hog herd, and may quicken the contraction. Barrow and gilt weights dropped two pounds this week

and that data was for the week that the polar vortex descended upon the Midwest. I expect weights to bounce back in short order and maybe

increase another couple of pounds before they make their seasonal top.

Unseasonably warm weather is in the forecast for the next couple of

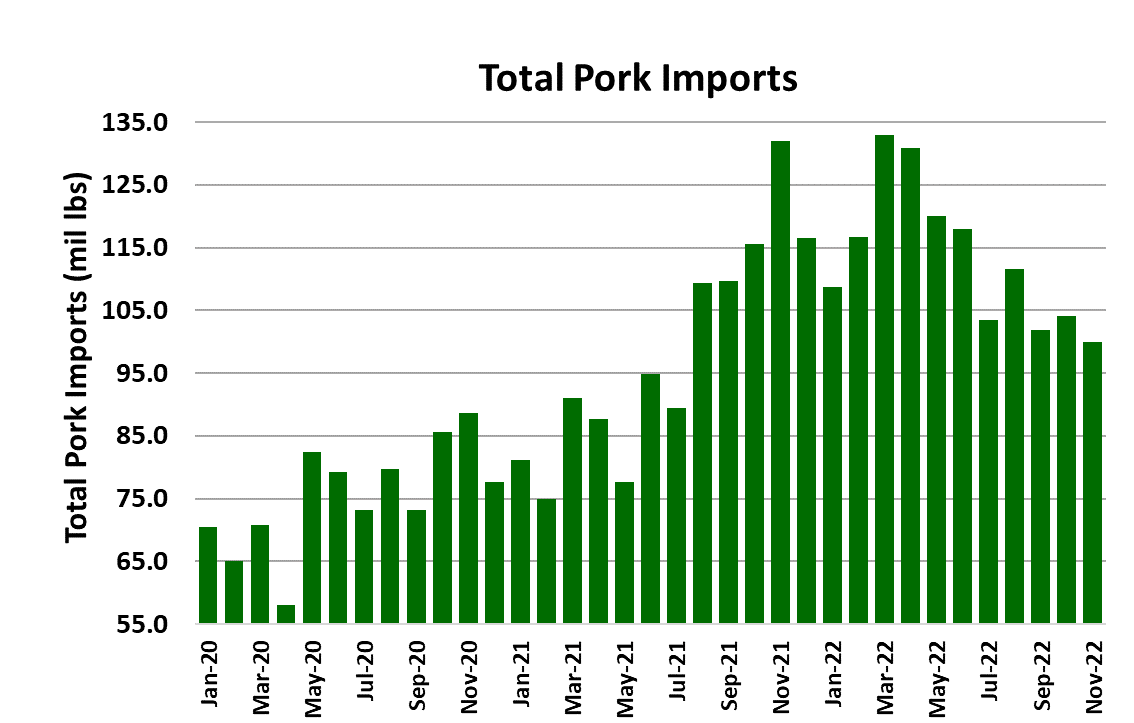

weeks, so that should help move weights higher. USDA provided the trade data for November this week and it showed pork exports almost

dead-on with last year for the second month in a row. The good news is

that pork imports were down 24% YOY. Per capita availability was down 3.8% YOY in November. I have no doubt that the spring rally in hog and

pork prices is coming this year, but I have a hard time seeing it starting

next week, with such large production looming. Pork is having to compete with some really cheap chicken for retail ad space at this time of

year when consumers typically become more value conscious. That is

likely keeping pork demand on the defensive. At some point it will

rebound and the bulls will have their day, but it doesn’t look like that is

likely to develop in the near term. Next week, watch for the hams to find a bottom. That is a key step in halting the slide in the cutout.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}