Pork Wrap January 7

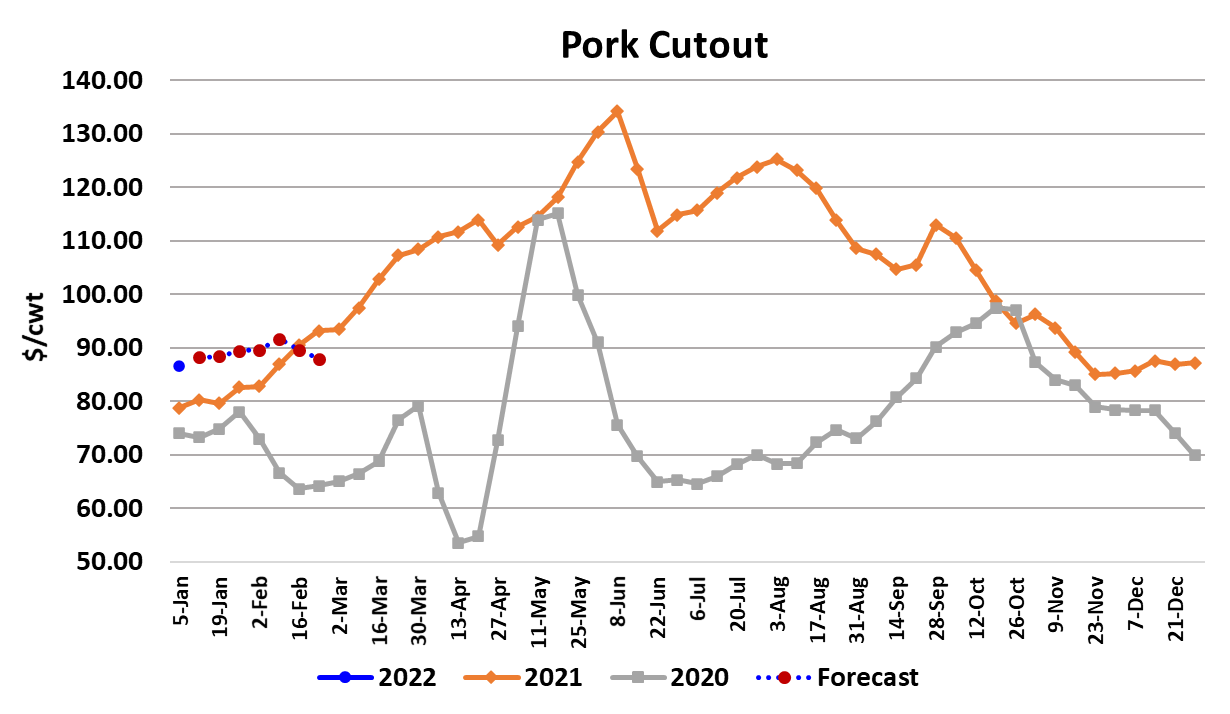

It was yet another week with the pork cutout going nowhere. It averaged

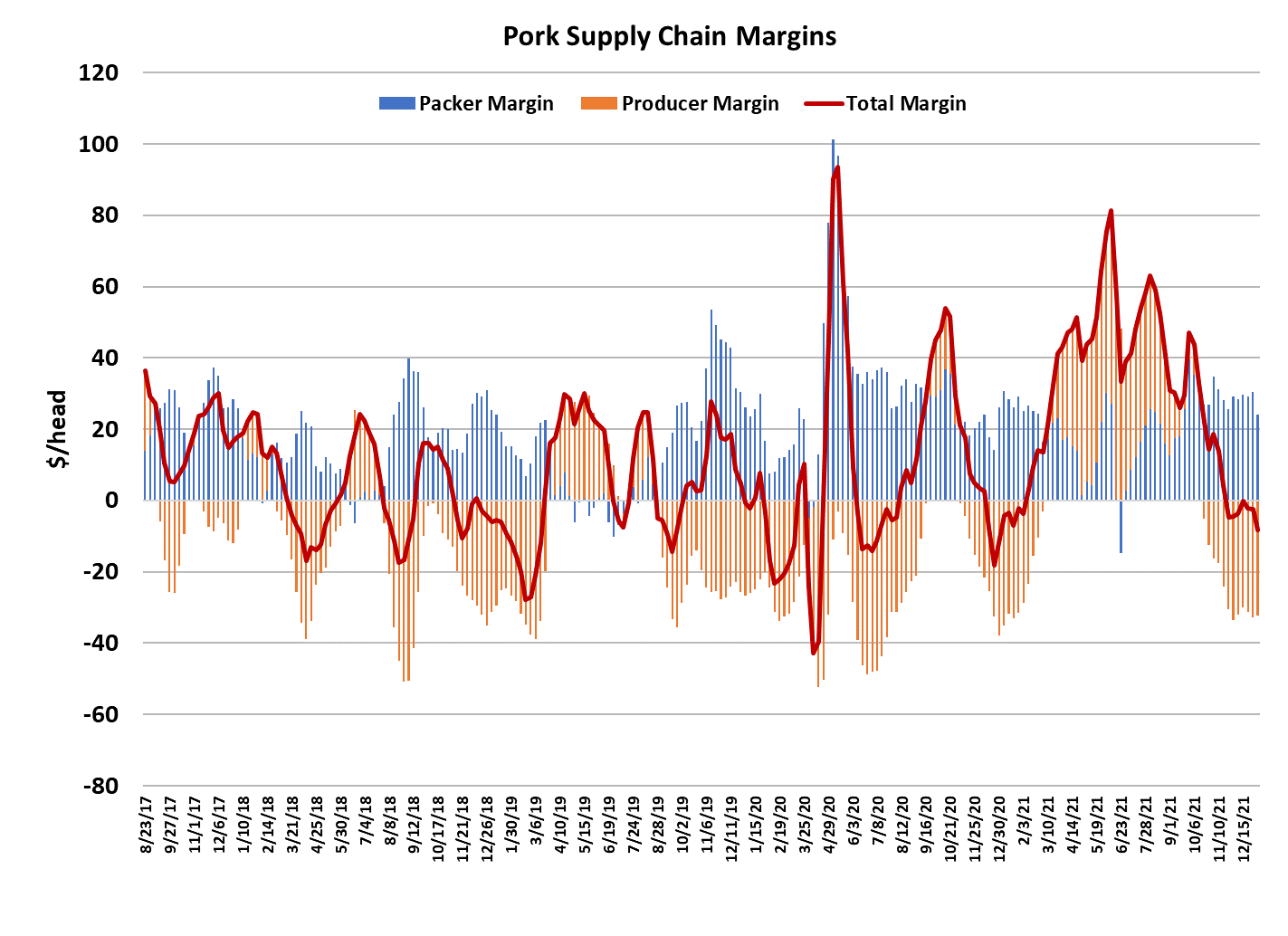

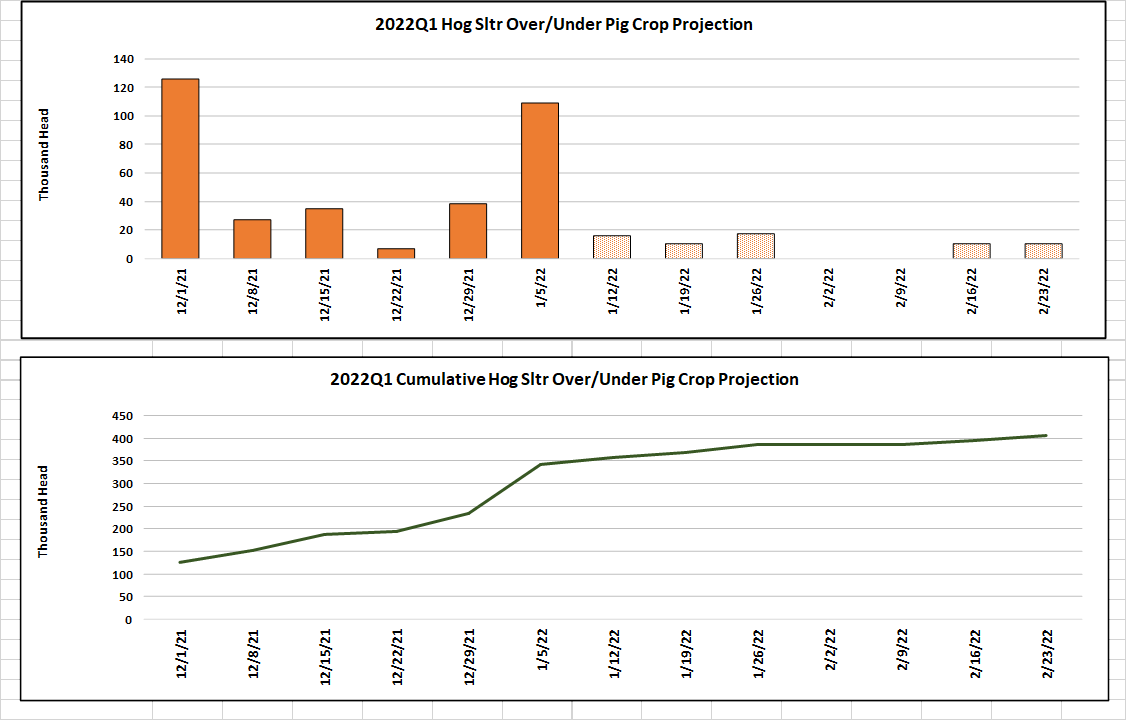

$86.57, down $0.64 from last week’s average. One thing that did change this week was the price of cash hogs. The WCB negotiated market was up almost $6 and the NDD market gained a little over $4.50. It was somewhat curious that the cash hog market moved upward after two short kill weeks. Normally, a short kills lead to some backing up that has to be cleared, but apparently not this time. With the cutout flat and cash hogs rising, packer margins were pressured. I calculate the margin at close to $24/head, down about $6 from last week. Similar to last week, hams exerted pressure on the cutout while bellies supported it. All of the other primals were nearly unchanged. With omicron infections soaring in the US, there was a lot of concern about packers having enough labor available to process a full slaughter schedule. The managed to pull it off, although there were a few days where the estimated kill was revised downward. To make up for that, they came on with a strong Saturday slaughter that pushed the weekly total to 2.58 million head. That was over 100k above what the pig crop suggested.

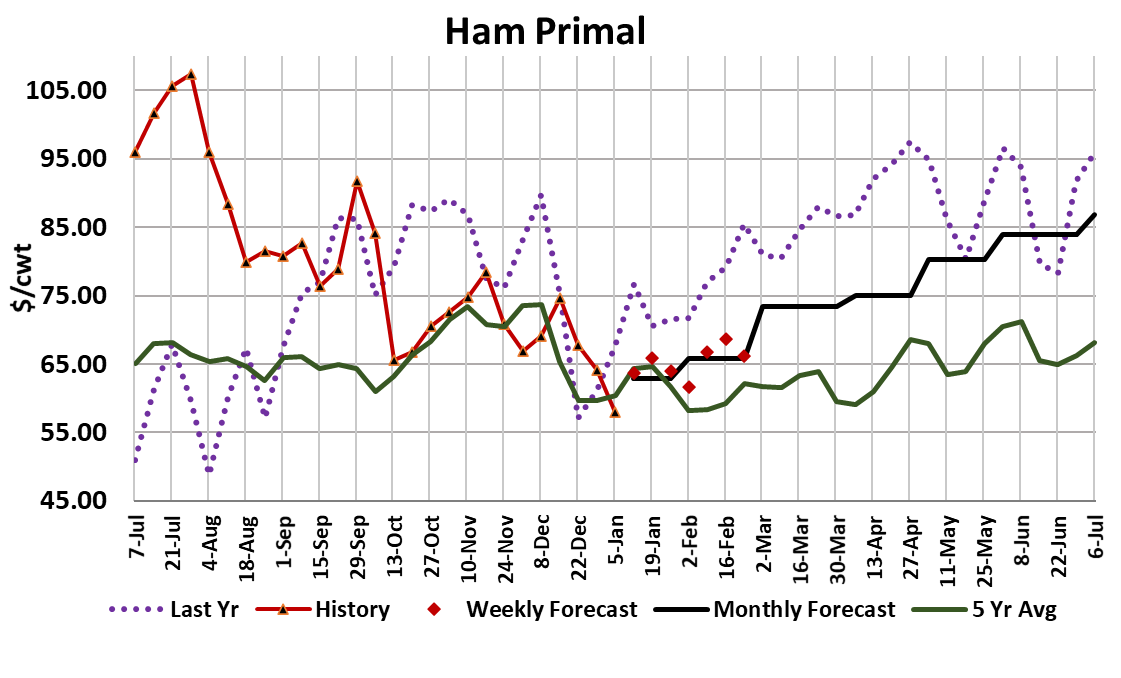

We are almost halfway through the Dec/Feb quarter now and the cumulative over-kill has been about 350k. I think it is safe to assume that USDA underestimated the summer pig crop and will have to revise it upward in the next Hogs & Pigs report. However, that leaves us with a mystery as to why the cash hog markets are strengthening when there are more hogs available than advertised. Perhaps one or more packers found themselves out of position and had to bid the hogs up in a particular region. If that is the case, then the cash strength is likely to dissipate quickly. For now though, if packers want to improve their margin they will need to find a way to put more money on the pork. That might not be an easy task heading into next week with this week’s big kill in the coolers. However, it does seem to me like the hams are getting cheap enough now that they ought to attract buying interest, both from domestic buyers prepping for Easter and from international buyers who might

be price sensitive. Over the past five years, the ham primal has tended to add about $5 on average during the month of January. The primal is now $10 below where it was in the first week of January during the past two years, so buyers should see today’s pricing as a value. Part of the problem might be the lack of deboning labor forcing more product to be sold as bone-in rather than boneless. That value-added boning business helps to prop up the primal value and in the current situation it is very difficult to do much de-boning. USDA did revise the yields and labor cost assumptions in their cutout calculation at the first of the year. The yield changes are mostly insignificant but they raised the labor credit substantially, and rightfully so.

Theoretically, that should better account for boneless product in the cutout and hopefully smooth out some of the wild primal value gyrations that have become common on days when a high percentage of the volume is in boneless product. That might not be immediately noticeable because of the strain that omicron is currently putting on the workforce, but once absenteeism subsides then I think pricing in the boneless products will ease and thus lessen the volatility impact on the primals. Omicron is probably also straining the labor force at belly slicers and that may be hindering buying interest in that primal. The belly seems overdue for a move higher and did manage some small gains over the past two weeks, but “small” is not a word that I typically associate with belly price changes and therefore think there must be some external force temporarily limiting belly demand at wholesale.

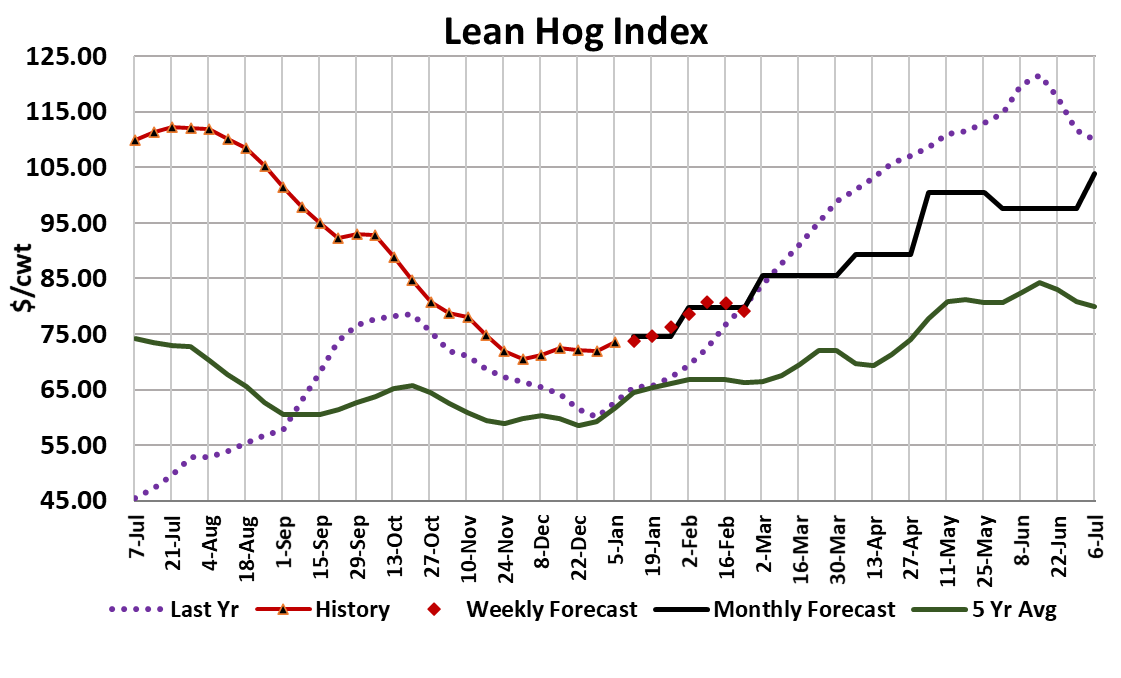

I’m forecasting the bellies to move higher in bigger chunks over the next few weeks under the assumption that omicron infections will subside quickly and thus the labor situation will improve. One consequence of labor tightness is that fewer knife cuts are made on an item and thus less trim is generated. We have seen the price of 72% trim gain about $15/cwt over the past two weeks and 42s are also on the rise. Sausage and hot dog makers had a golden opportunity to freeze trim from about mid-November until the end of the year, but now price levels make that an unattractive option. With hams and bellies due to rally and trims already moving higher, I expect that the cutout will show some gains over the next few weeks. Nothing dramatic, but some upward pressure nonetheless. A rising cutout along with a rising cash hog market makes for a rising lean hog index. Futures traders had been wanting to price that contract in the low to mid $80s for the past several weeks, but grew tired of the stagnant cutout and today that contract pulled back under the $80 mark, losing $3.30 in the process.

Up until now, the nearby futures have been really optimistic, but after today I think traders have shifted to more of a “show me” attitude. The back of the futures curve and been posting gains on a regular basis and those contracts were higher again this week. I think a lot of that has to do with the stubbornly high price of feedstuffs and the idea that in the long-run hog prices must equal the cost of production. I agree with that economic concept, but the six months from now to summer is hardly ‘long run’. One very important headwind facing buyers of those deferred futures is the fact that pork exports could be very disappointing in the next few months. USDA released the official trade data for November today and it showed YOY pork exports down 8.3%, with the volumes to China down 72% from last November. At the same time that exports are struggling, pork imports were reported up 49% YOY. In fact, the 132 million pounds of pork imported in November was an all-time high. It not any particular country that is responsible for the import surge, but rather growth in all of the major originating countries. So while domestic supply is down due to smaller pig crops, that is tempered somewhat by fewer exports and more imports. The combined margin has been signaling that it is time for pork demand to enter another upcycle, but this week it made an unexpected move lower. Maybe the downcycle has a little longer to run, but once hams catch a bid then I think the combined margin will start to march higher.

From a longer-run perspective, pork demand should slowly deflate as we

move through 2022. The conditions that created the supercharged demand environment in 2021 are not likely to be present in the same way this year. Doctors say that once the omicron surge has run its course that the acute phase of the pandemic may be over and it will then enter the chronic stage where it won’t be so disruptive to markets and everyday life. Everyone is ready for that. Next week, keep an eye on daily kills for signs that packers are struggling with absenteeism and watch that ham primal for stronger pricing because that likely holds the key to a stronger cutout and further gains in the LHI.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}