Pork Wrap January 28

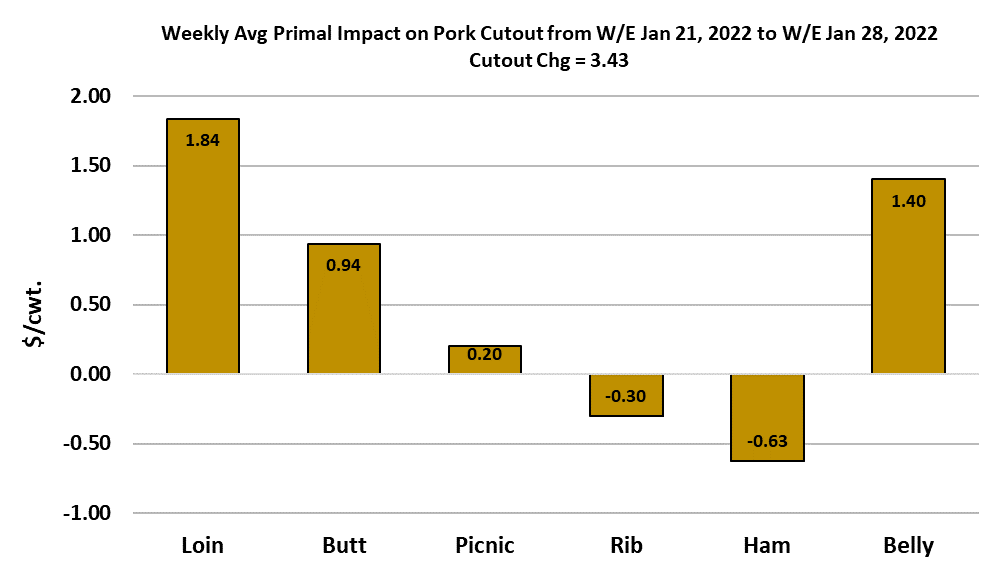

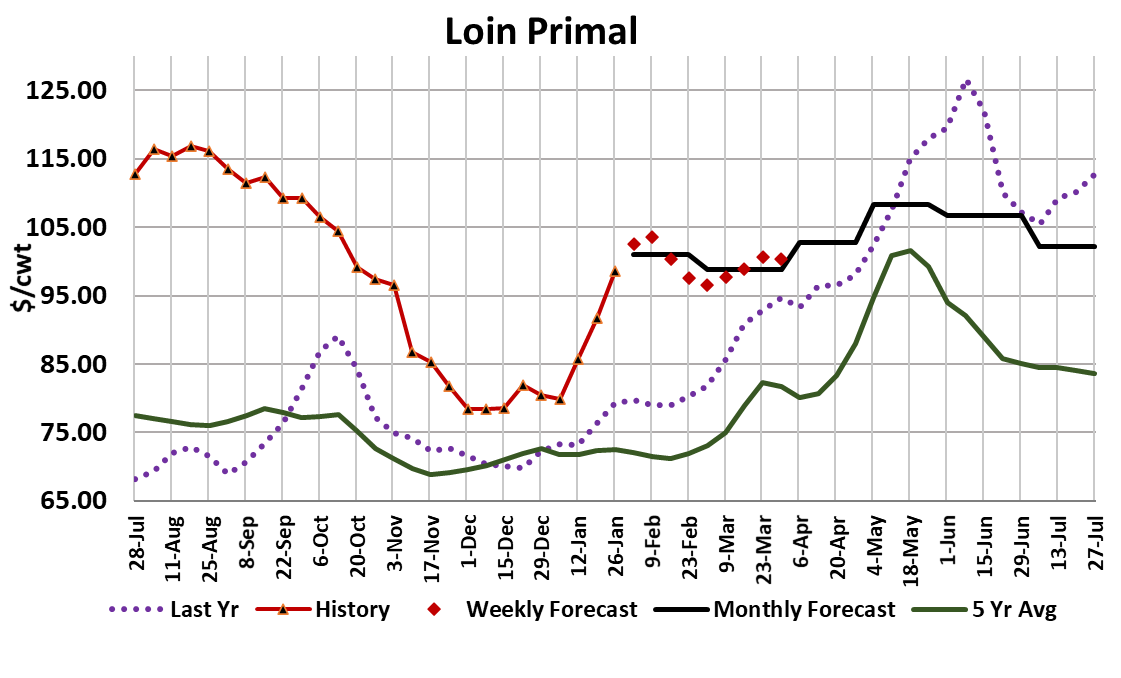

The pork cutout continued its upward momentum this week, adding

$3.43 to average $95.46. Retail items, and in particular the loins,

were the big driver of this week’s gains, along with some help from

the bellies. That fits with the idea that surging covid infections

would force consumers back into stay-at-home mode and drive

strong demand at retail. For once, the hams were not the main

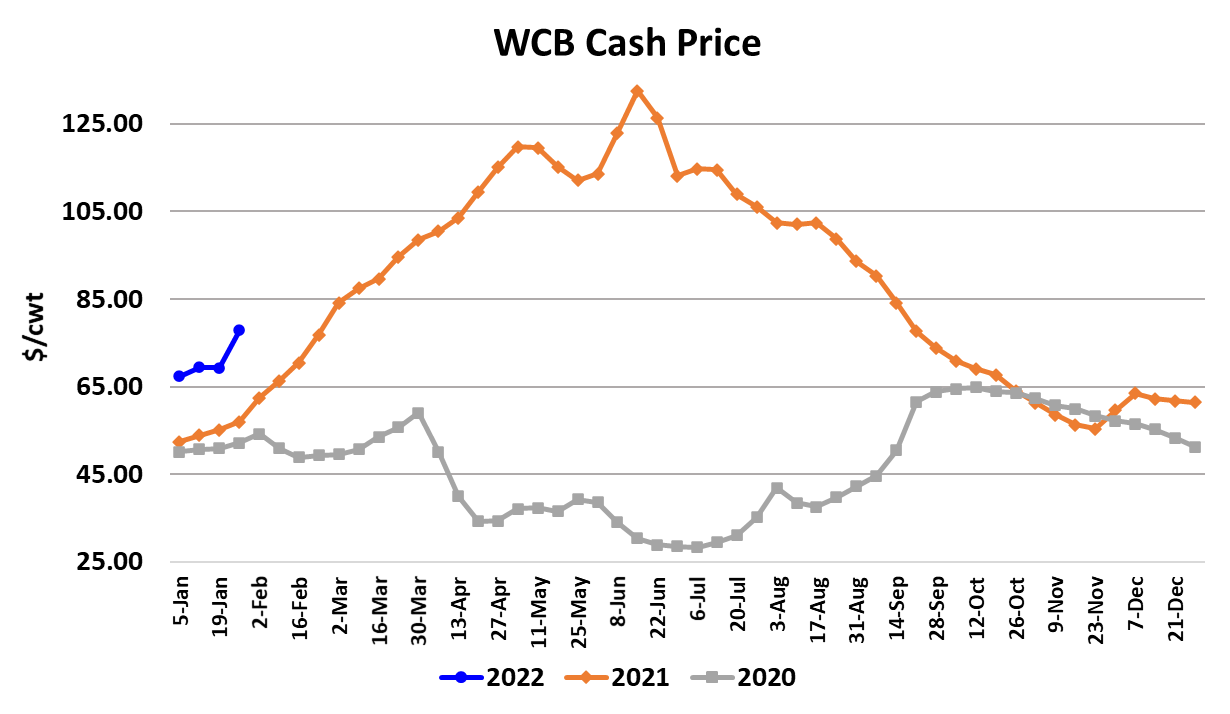

focus. The big story this week was the rapid rise in cash hog

prices. Negotiated prices in the WCB rose $8.55 this week and the

NDD price was up $5.44 on a weekly average basis. This caught a

lot of people off guard because the narrative had been that labor

problems in the plants were slowing kills and thus hogs should have

been backing up to some degree. Well, apparently not. First of all,

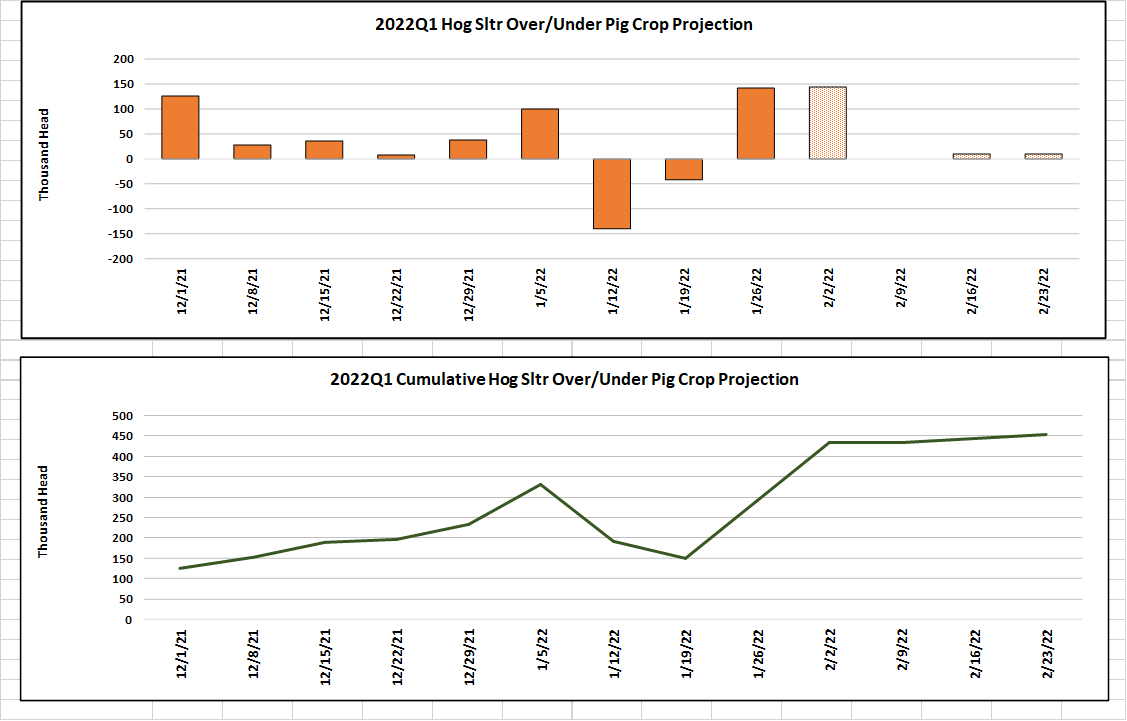

the hog kills never really got that small. The chart below compares

each week’s kill to what the Jun/Aug pig crop implied. From Dec 1

through New Year’s week, the industry actually over-killed the pig

crop.

Then there were two weeks of mild under-killing that I would

attribute to absenteeism in the plants. This week’s kill came in at

2.55 million head, which was about 145k over the pig crop

projection. So now we are back to over-killing the reported hog

supply again and I’m forecasting an over-kill again next week. That

makes it look like hogs are abundant. However, that doesn’t

square with the rapid rise in cash hog prices that we saw this week.

It is pretty clear now that labor is sufficient to kill all of the hogs that

are available. The rise in cash hog prices makes me think that

something else is going on. Perhaps producers are having disease

issues that are limiting hog availability. Since packers must buy

some negotiated hogs each day in order for their formulas to work,

they may be running up against producers who are reluctant to sell

in the negotiated market because disease has reduced their hog

supply below what they need to fulfill their formula commitments.

Thus, sharply higher cash prices are needed to bring forth a small

volume of negotiated hogs. This is pure speculation at this point,

but disease issues might also explain why there has been so much

buying interest in the summer contracts recently. Is PEDv rearing

its head once again? It feels a bit like that. I recall back in 2014

when the hog supply started to tighten up unexpectedly and for

several weeks no one knew quite how to explain it. Eventually, the

truth became widely known, but the futures market had already

leapt higher

Whatever it is, the negotiated markets should be watched

carefully. If they keep rising in big chunks then that is a sign to

pork buyers that they had better take coverage quickly because

availability is about to tighten. The rise in cash hog prices has

yet to be fully reflected in the LHI, which could easily reach $85

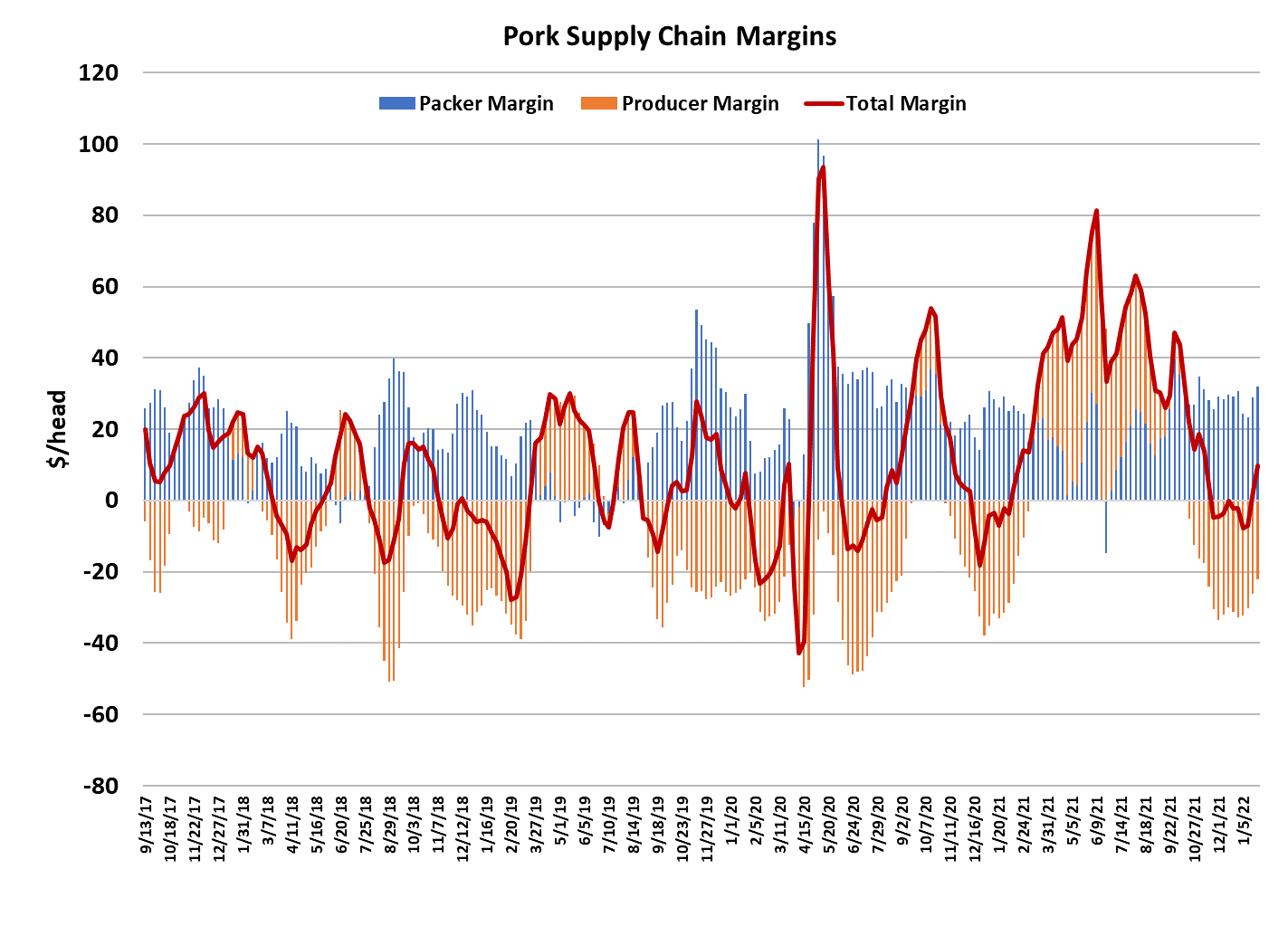

by the middle of next week. Packer margins expanded this week

as the cutout outpaced the LHI, but next week they are likely to

contract as the LHI catches up. Margins this week were near

$31/head—record large for this time of year. That might explain

why packers are pulling harder than they should on the hog

supply. All of the uncertainty around the hog supply makes price

forecasting rather difficult.

Right now, I’m forecasting the cutout to hold in the high $90s for a

couple of weeks and then come back down into the low 90s.

However, if there is a significant disease problem in the herd,

then all bets are off and it would be very likely that the cutout

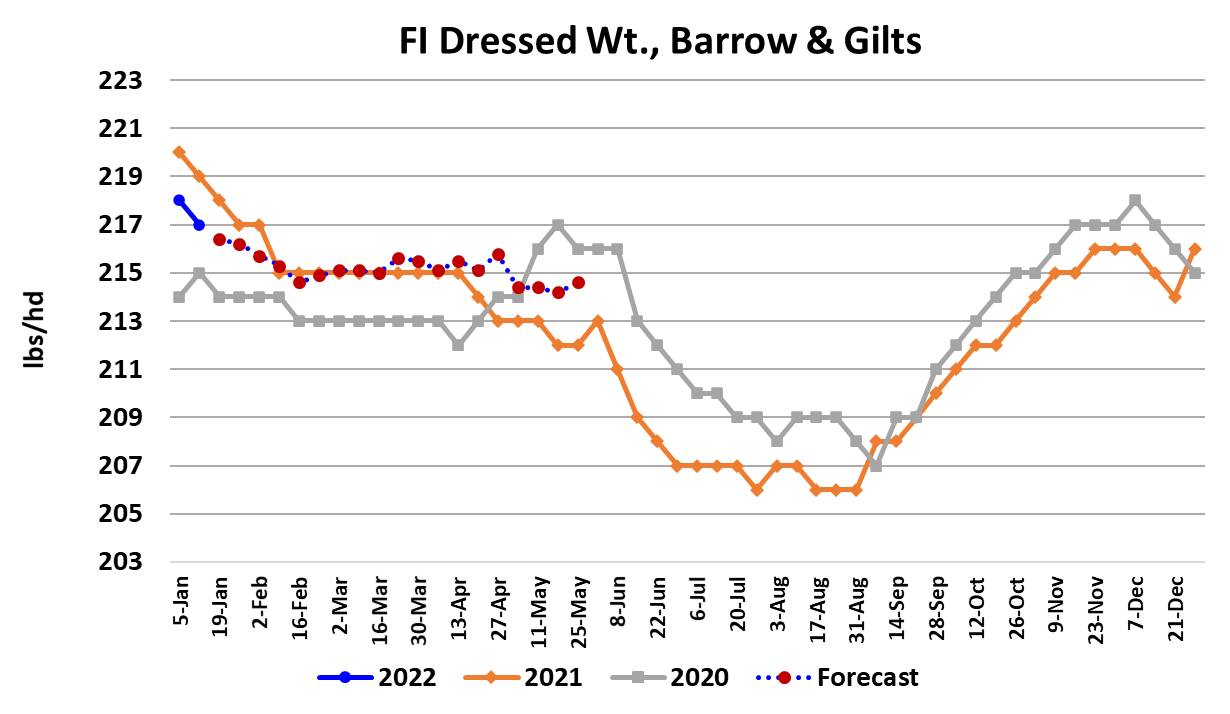

would advance well above the $100 mark. Hog weights are not

really showing any signs of the supply being stretched, with

barrow and gilt weights last reported 2 pounds under last year

and working lower. The DTDS weights are almost at the zero

mark, which suggests that producers are a little behind in their

marketings. However, that weight data is two weeks old and it

might tell a different story a few weeks down the road. On the

pork side, export demand is not very good at present either.

China will be hosting the winter Olympics next week, but not

allowing international spectators, so the event didn’t generate

additional demand for imported pork the way it did for the

summer games back in 2008. Mexico is our best customer right

now, but one has to wonder if they will remain a strong buyer with

cutout values hovering near $100. After many weeks of holding

in a sideways pattern, there is now some excitement back in the

hog and pork complex. Next week watch those negotiated prices

like a hawk because if they keep up their rapid advance, the odds

of tightening availability rise considerably.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}