Pork Wrap January 27

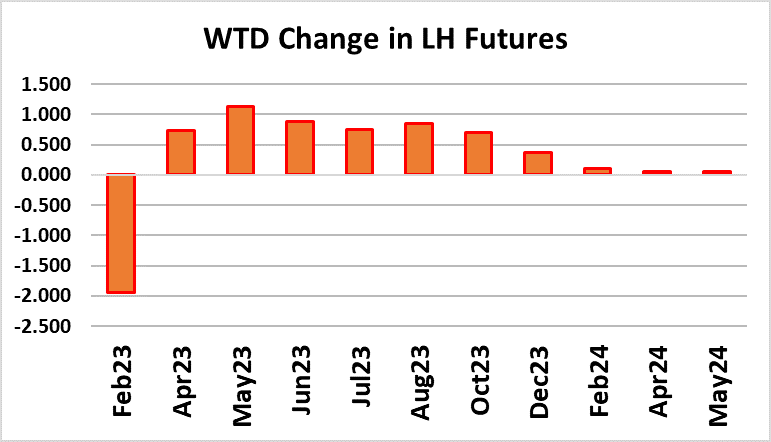

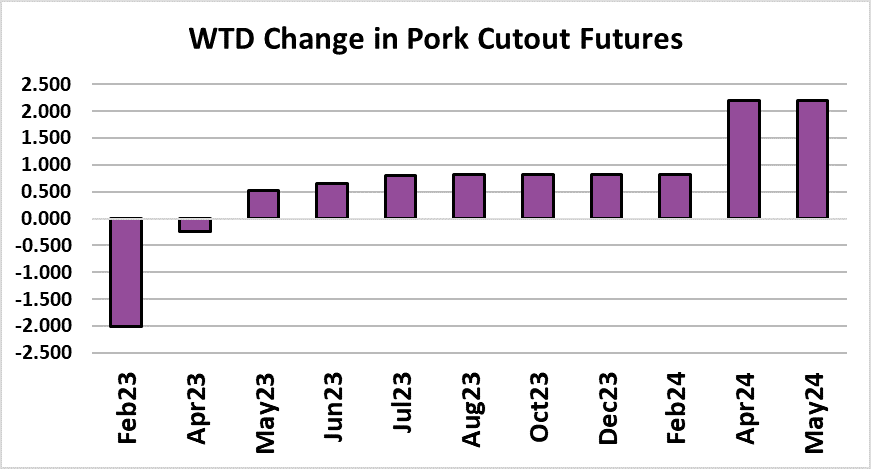

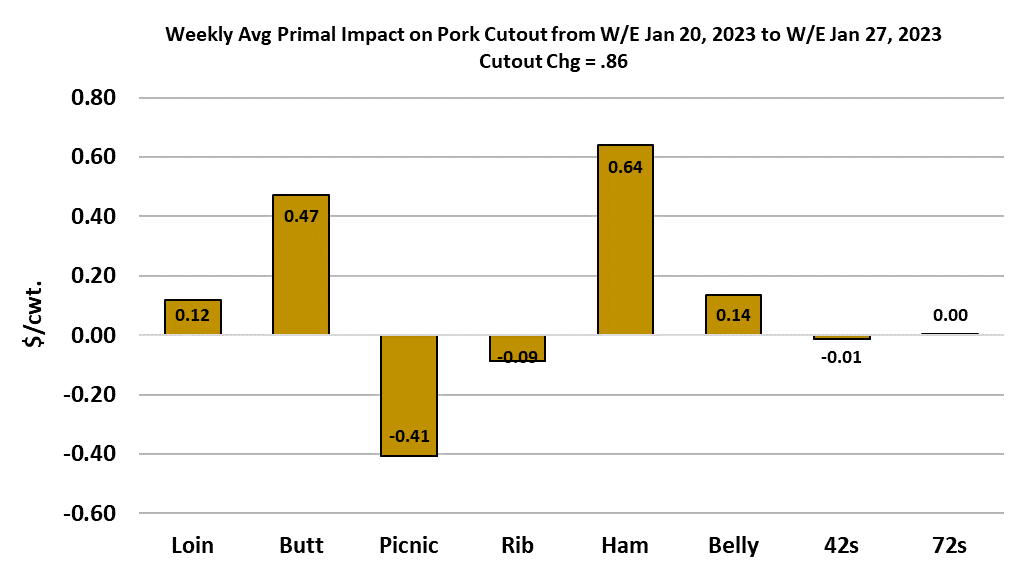

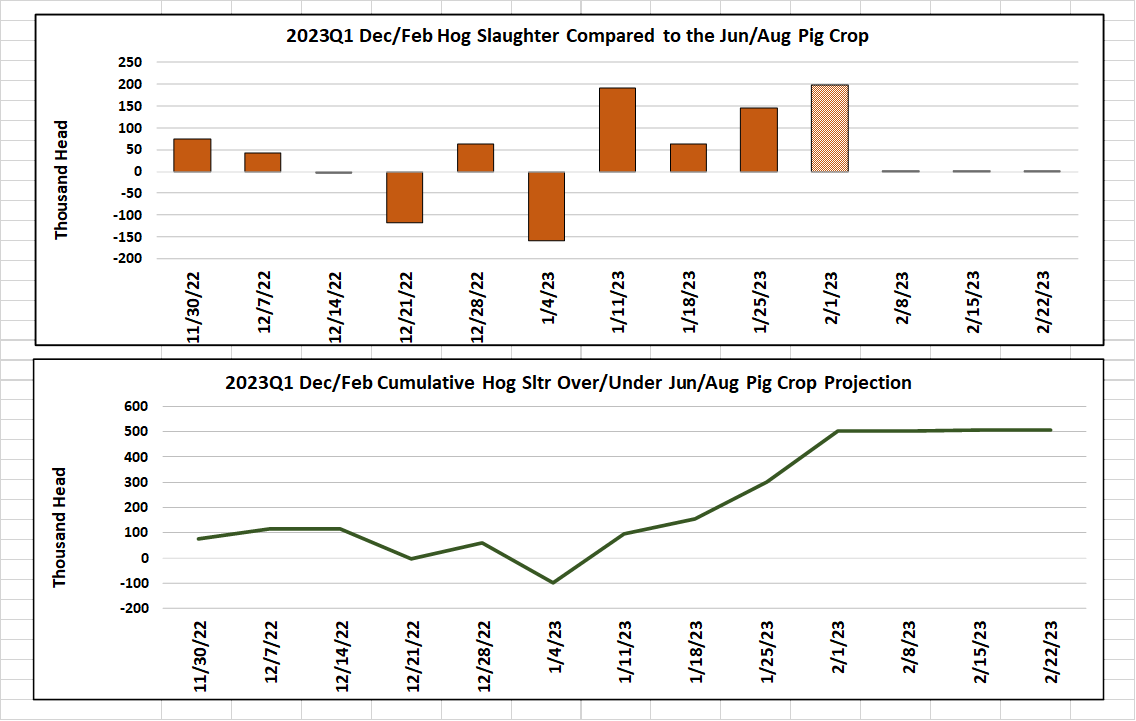

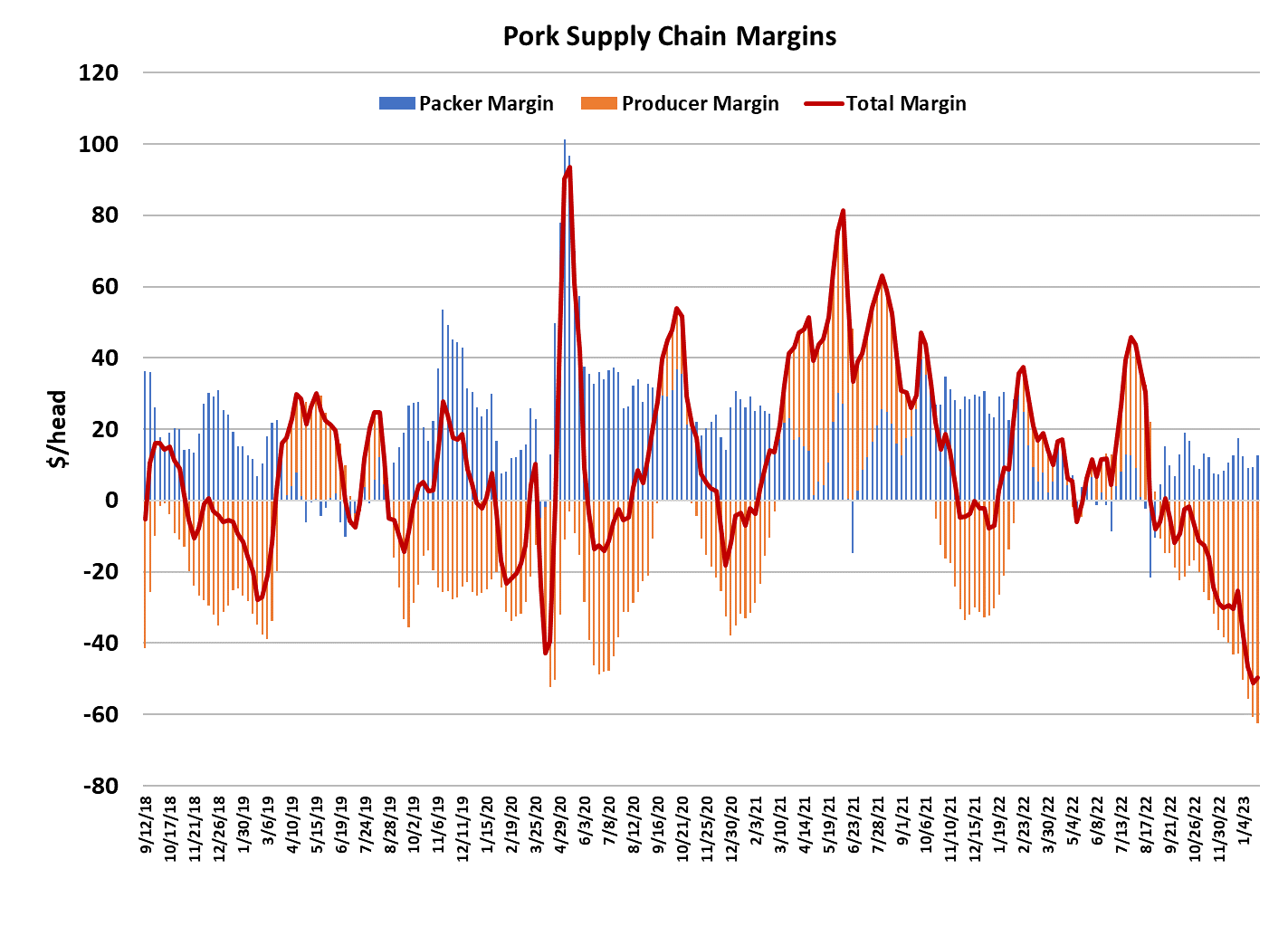

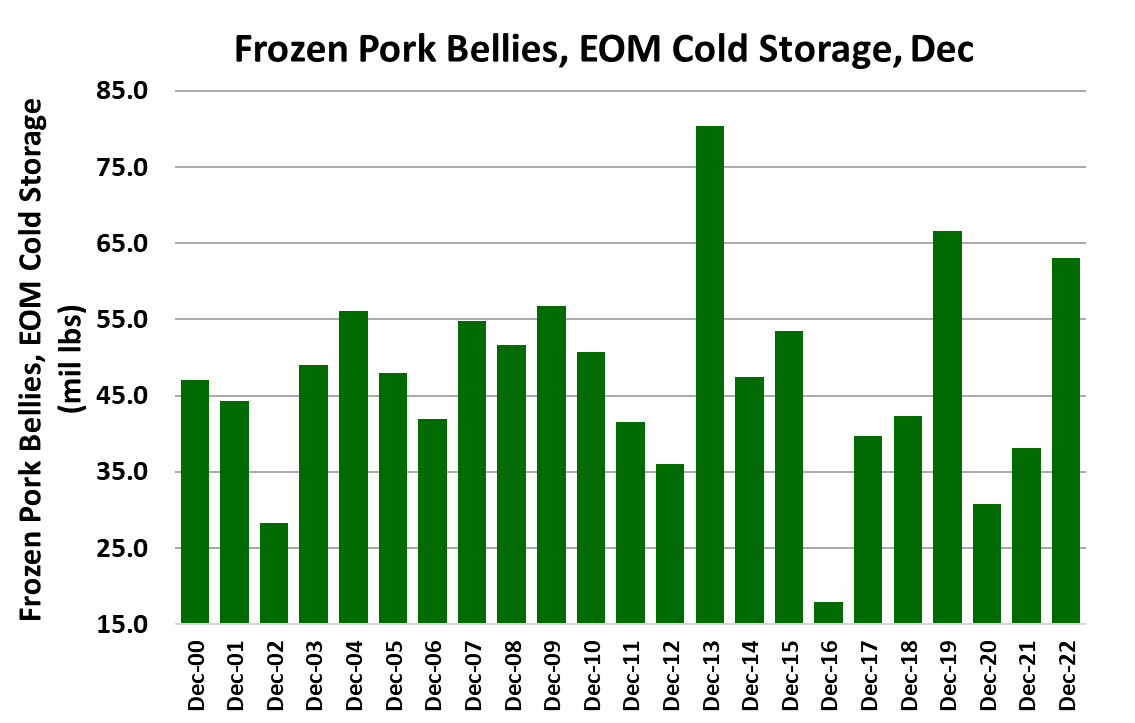

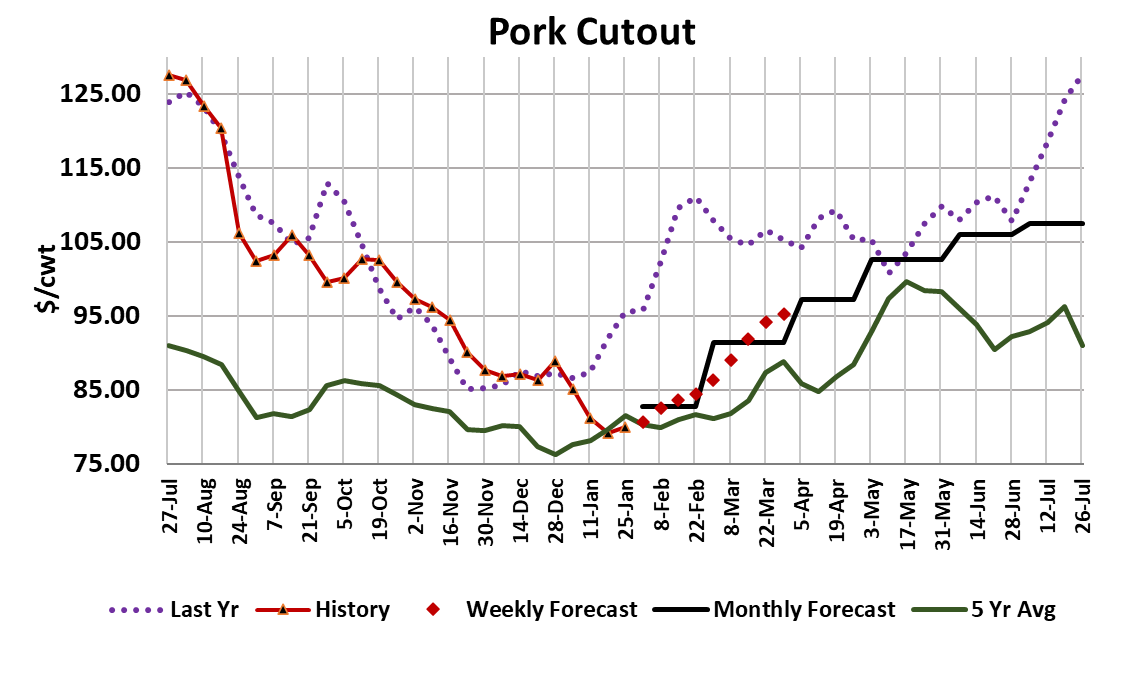

A glimmer of hope came to the hog and pork complex this week as both the cutout and negotiated hog markets posted a tiny increase. The cutout added $0.86/cwt. on a weekly average basis and the WCB negotiated price gained $0.47/cwt. Market participants are trying to discern if this is the true bottom in prices or just another head fake. My guess is that a bottom is being carved out, but it probably won’t be a V-bottom and the price gains over the next few weeks are likely to be small. It is interesting to note that this week’s cutout was actually below its 5-year average. That hasn’t happened since well before the pandemic. It is just another reminder of how much different the market is now than it has been in the past few years. The ham market clawed its way higher this week and that was the biggest contributor to the cutout’s gain. Other than that, there just wasn’t much price movement in any part of the carcass this week. It is that lethargy in prices that makes the Feb contract vulnerable from its current perch near $76/cwt. The LHI is currently at $72.64, but it is stalled there unless further increases in the cutout or negotiated markets occur. With the cutout going in slow motion these days, there is some question as to whether or not the LHI can get to $76 in the remaining 12 trading days of its life. It probably won’t get much help from reduced kills. This week’s slaughter came in at 2.54 million head, up slightly from last week. Next week, packers are planning a larger Saturday kill and that could result in a weekly total near 2.6 million head. Pork fatigue is starting to set in. However, an artic air blast is set to hit the upper Midwest next week and that has the potential to trim back one or two daily kills, but the shortfall could easily be made up on Saturday. I am now fully convinced that there are more hogs ready for slaughter than what USDA’s estimate of the Jun/Aug pig crop indicated. The attached chart highlights the obvious over-kills in recent weeks, with more to come. At this point it looks like the industry will over-kill that pig crop estimate by about 500k, but that number could easily expand during the final weeks of the quarter. This will cast doubt on the Sep/Nov pig crop, which will be slaughtered from March through May. So far, the Apr futures have opted to keep a very large premium over the Feb contract, but if it turns out that the next pig crop is bigger-than-advertised also, that premium might not be justified. The slow movement in pork prices that I highlighted earlier also makes it risky for Apr to trade at such a large premium. On average, the LHI only advances about $3-5/cwt. from Feb expiration to Apr expiration, but the futures are currently looking for a $10.50 gain. There is a tendency for traders to anticipate that when price levels are exceptionally low or high and eventually turn, they will move rapidly in the opposite direction. That certainly happened last August when the market broke lower from a very high price level, but it isn’t a given that it will happen in the current environment where there are more hogs than expected, cold storage stocks are large, and demand is relatively soft. Speaking of cold storage, USDA found that the total amount of pork in cold storage at the end of December was almost 16% higher than last year. Bellies in cold storage were up 66% YOY, increasing 16% from November’s total. Those big stocks will likely make it difficult for belly prices to gain much traction in the near-term. Total ham stocks were down 13% YOY, but the drawdown during December was smaller than normal. Ham buyers should now be working on their needs for Easter and should find wholesale pricing very close to last year, allowing them to hit the same retail price points as last year. The weekly export data is showing shipments to Mexico very close to last year, which doesn’t suggest that Mexican buyers are rushing in to scoop up US hams at today’s price levels. In fact, pork exports in total aren’t much to write home about and thus far in 2023, interest from Japan and S. Korea has been especially muted. Shipments to China are running about 24% over last year, but much of that is offal and won’t have a direct impact on the cutout. Domestic demand has been exceptionally weak so far in 2023 and the combined margin makes that very evident. We did see a tiny tick upward in the combined margin this week, but I’d want to see another advance before declaring that the bottom is in. Producer profitability is worse than at any point in the past five years (orange bars). Back in 2021 when feed costs shot through the roof, producer margins were buffered by extremely strong demand, but now that demand has faded, producers are just left with high costs and no way to cover them. One of the main functions of the market is to send signals for future production to those that raise hogs. I’d say that right now the market is sending a clear signal that less hogs are needed. As the industry continues to downsize, plants will have to chase harder for hog supplies, thus raising prices to a level that should restore profitability. That economic process can take months, or even years, to play out and the futures market has a big role in the process. If traders keep unrealistically high prices on the deferred futures, then producers can hedge their output and avoid having to downsize, which just makes it tougher to get the herd right-sized with demand. Next week, watch for further advances in ham prices, but don’t expect them to rocket higher since production will continue to be large. Also, keep an eye on the weather in the upper Midwest as that might cause some slaughter delays.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}