Pork Wrap January 26

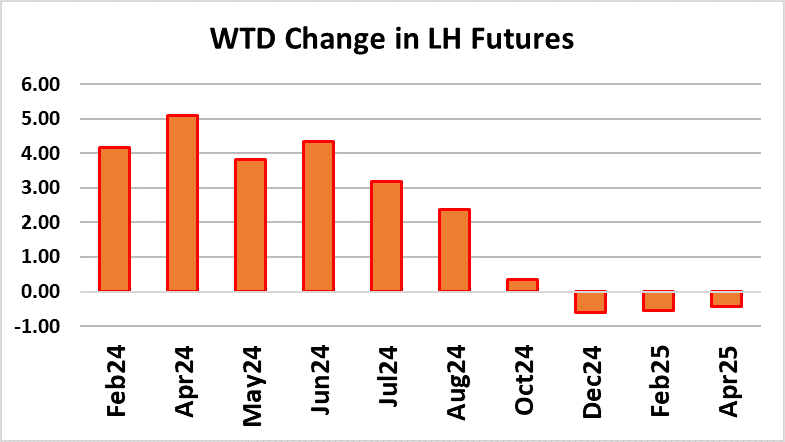

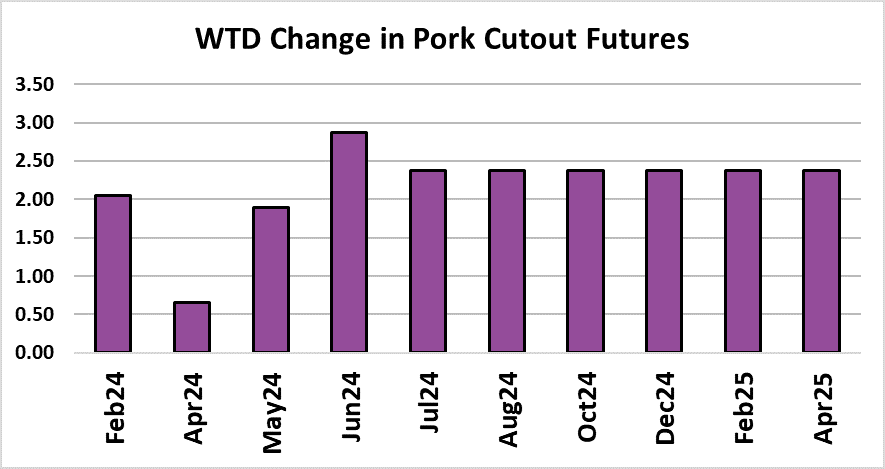

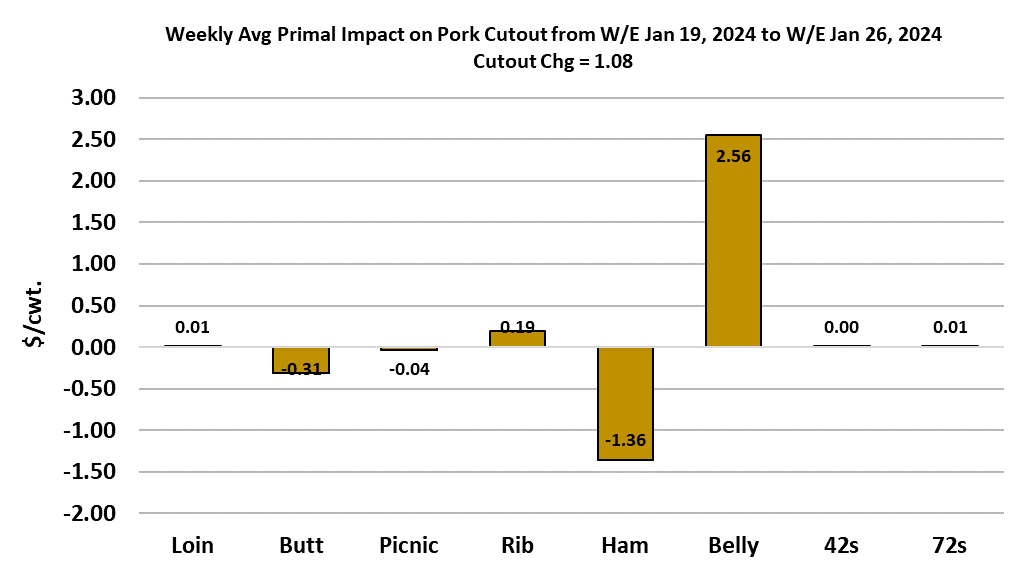

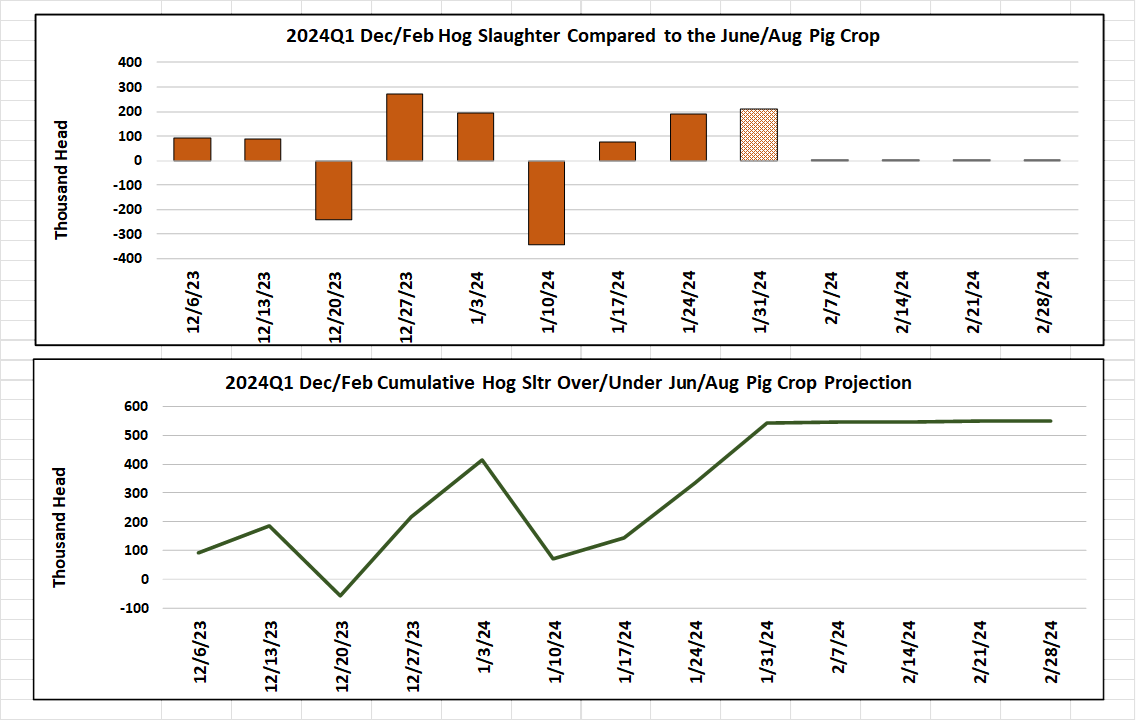

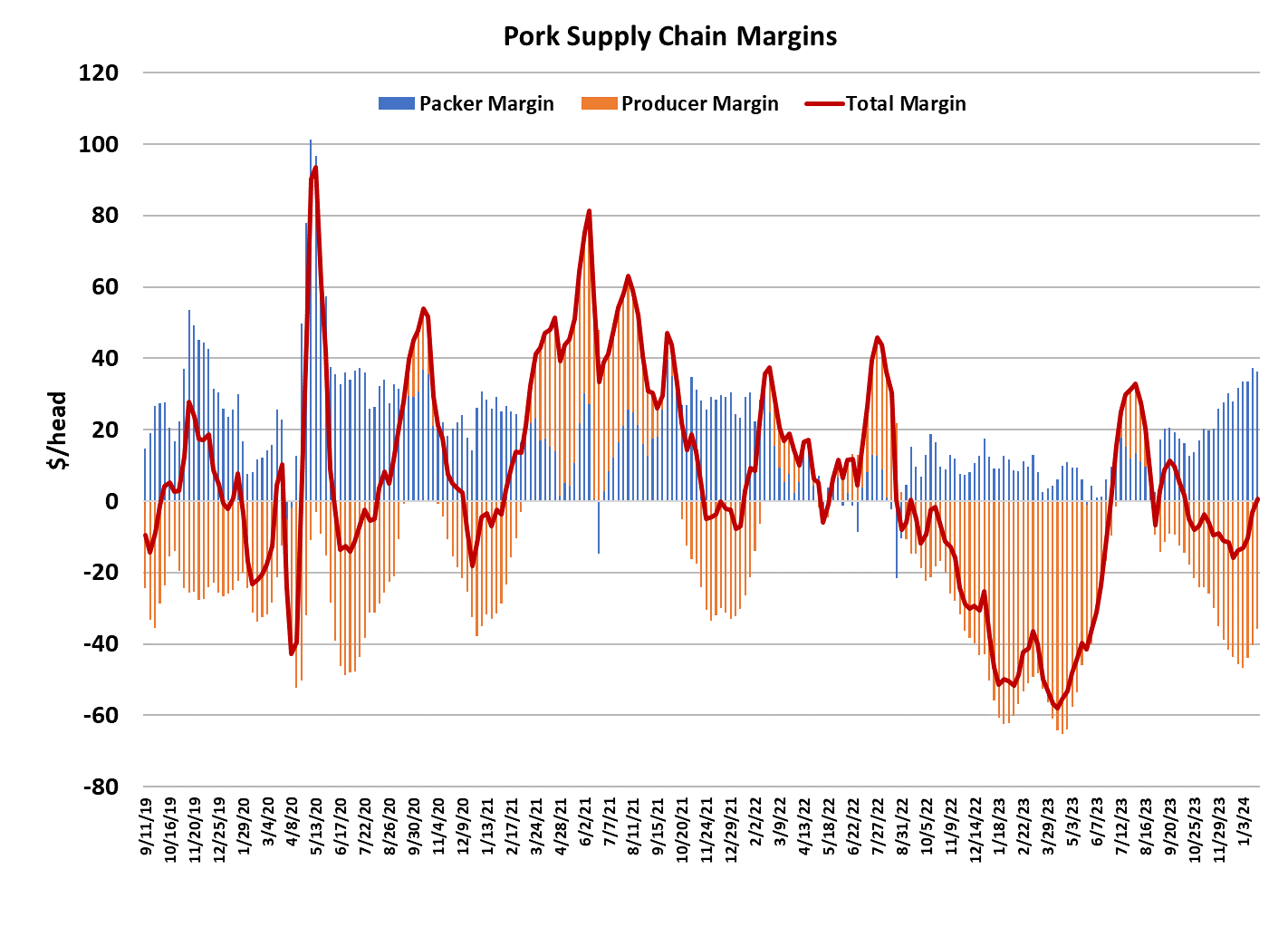

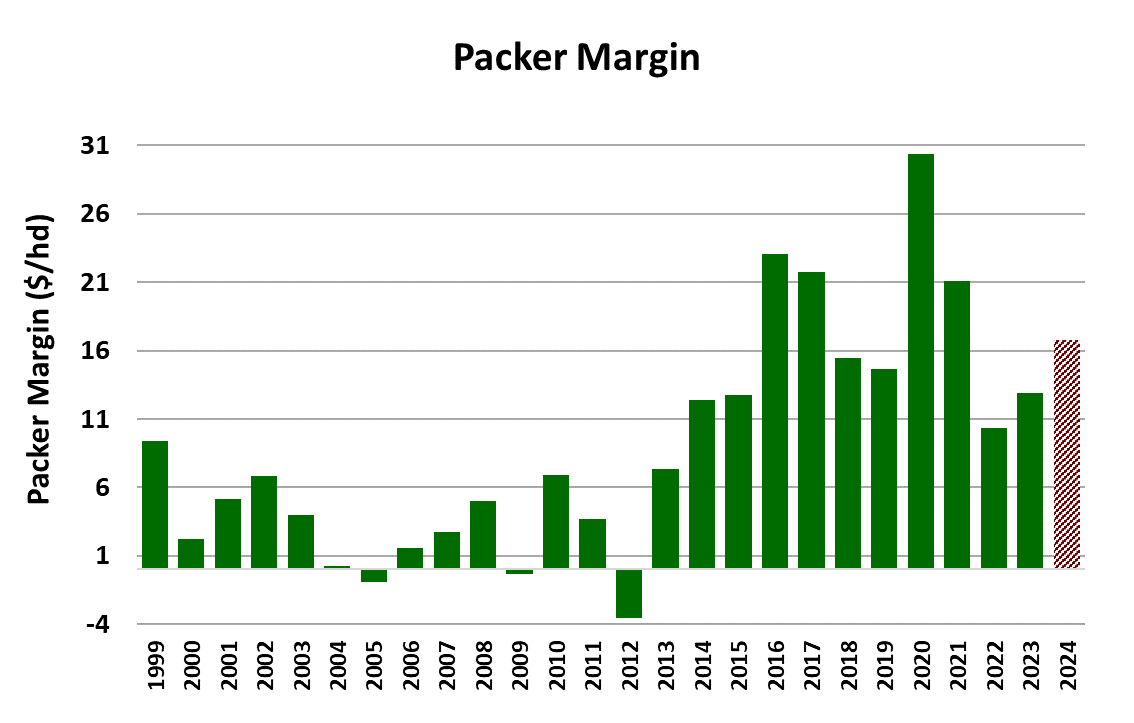

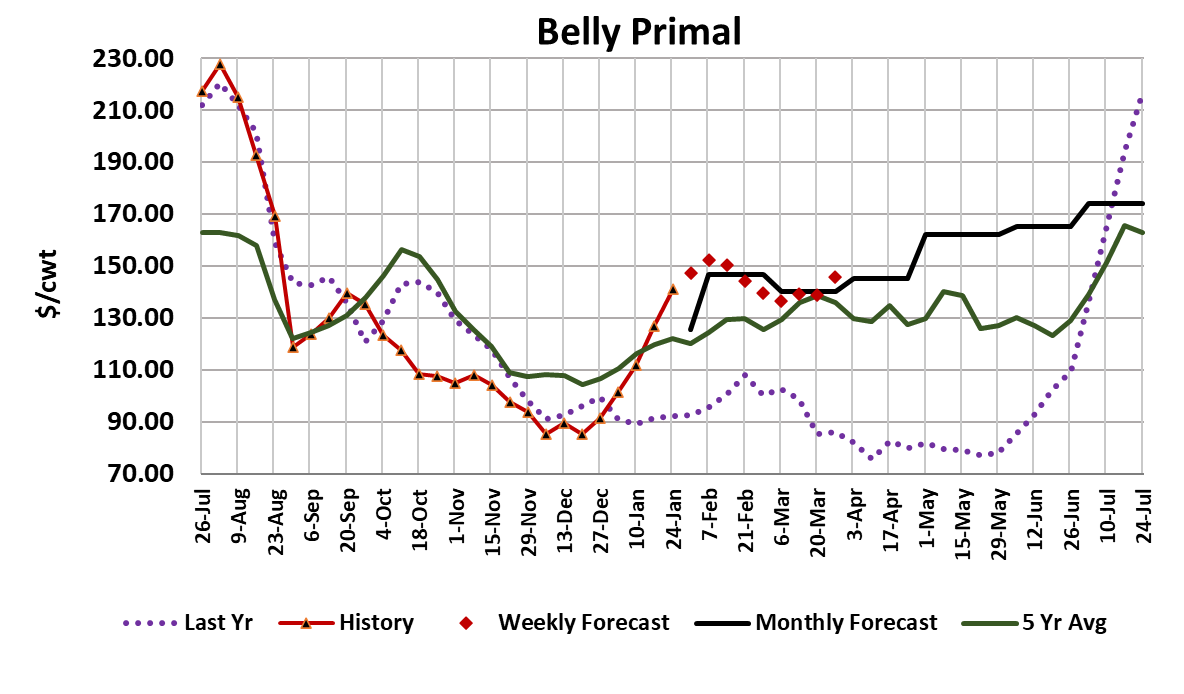

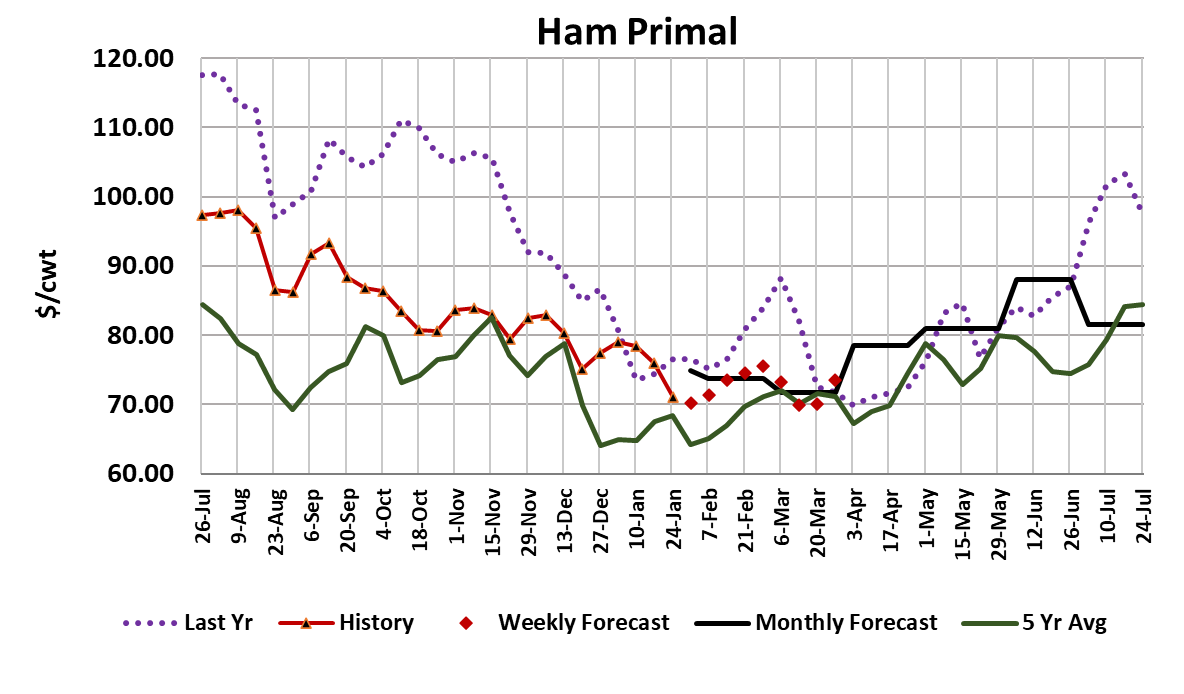

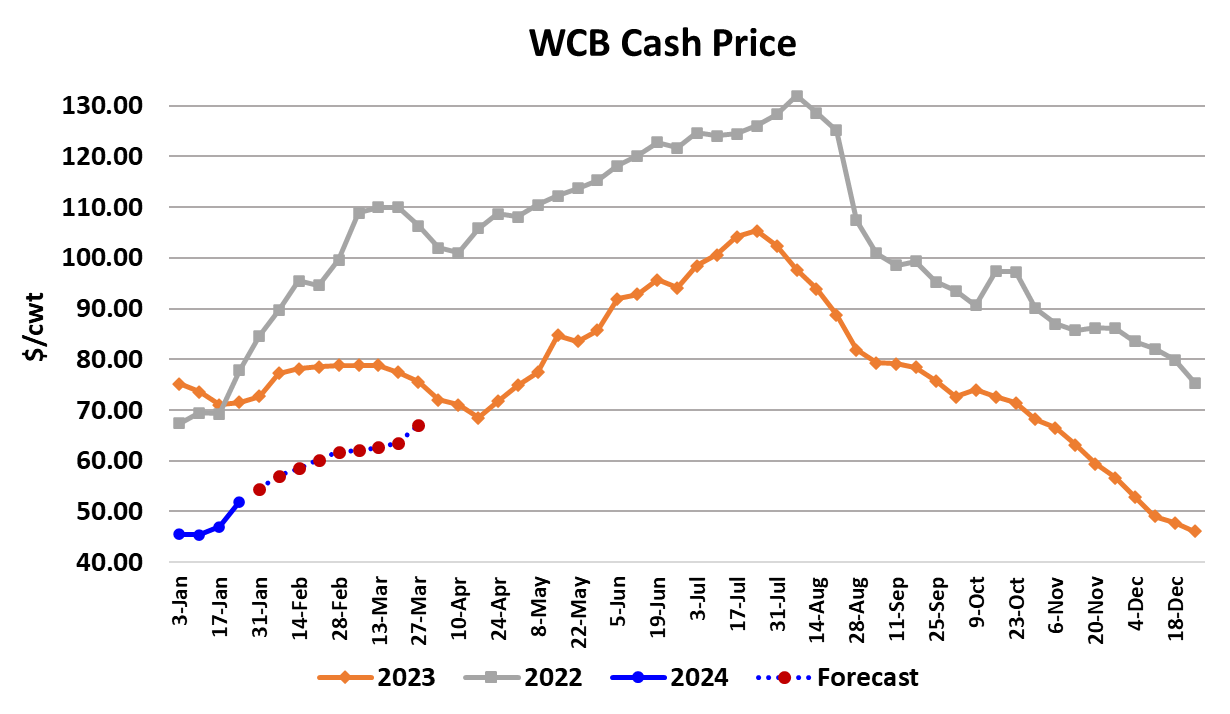

After a very dismal December and early January, optimism has returned to the hog and pork complex. Interestingly, this new optimism wasn’t generated by a soaring cutout because the cutout only added its usual $1 this week. Nope, the excitement was generated by the negotiated hog market where prices in the NDD market gained a little over $6 on to average $51.57/cwt. As of Friday afternoon prices in the WCB region were close to $56/cwt. and the previous Friday they were near $46/cwt. How is it possible for negotiated hog prices to rise so rapidly when hogs were supposedly backed up due to small kills during the weather event of early January? I said last week that I didn’t think the backlog from the weather problems was very big at all and that is looking more likely now. However, I’m also of the opinion that the negotiated hog market is fairly easily manipulated, particularly by packers, due to the very tiny percentage of overall slaughter that is transacted through that market. The positive correlation between the cutout and the negotiated market is rather strong. When the cutout is falling (as it was in late 2023) packers push the negotiated price down. When the cutout is rising, packers allow the negotiated market to rise to some degree. When packers sense that producers have had enough financial pain, they can “donate” some of their margin to producers by letting negotiated prices rise. The degree of control by packers over the negotiated price is much stronger in the hog market than in the cattle market where a much higher percentage of slaughter is priced via arms-length negotiation. Further, many formula pricing programs in the hog market reference the cutout, with hogs priced at some discount to the cutout. Those formulas give packers a guaranteed margin on a year-round basis and it is usually a pretty healthy margin—on the order of $20-25 per head. For these reasons, we see much more consistent profitability in the pork packing industry. My packer margin estimates only show three years between 2000 and 2023 where packer margins averaged in negative territory. The point is that with packer margins currently over $35/head, they could comfortably bid up negotiated prices without much threat of putting margins at risk. Or maybe their margins were just so good that they wanted to run bigger kills and that forced them to bid up the negotiated market to get those extra hogs. Packers certainly put together an impressive kill this week that totaled 2.71 million head. There are early indications that next week’s kill will be above 2.65 million head. Both of those are way above what the pig crop implied for this time of year, so the evidence is starting to mount that USDA’s survey under-estimated the size of the pig crop last summer. By the time next week’s kill is in the books, the over-kill could be close to 550,000 head. With the return to big kills, one would think that the cutout would come under pressure, but so far it hasn’t. The cutout gained $1.08 to average $89.10 this week. Once again, the bellies were by far the biggest positive contributor to the cutout’s rise. Ham prices went in the other direction, while price changes for the retail primals were small and mixed. More and more, the fate of the cutout rests on the direction of hams and bellies. This week, the bellies dominated and so we saw a small increase in the cutout, but at some point the gains in the bellies may cool or reverse and that would likely spell trouble for the cutout. It is very interesting that the higher pricing in the belly market is coinciding with small volumes of reported spot belly transactions, even as the kills have moved higher. That suggests that a big quantity of bellies are avoiding the spot market. Perhaps they were sold for export or sold on a forward contract basis and so don’t show up in the spot report. This week’s Cold Storage report showed belly stocks at the end of December down about 11% YOY, which was similar to what we saw in November. The inventory build during December was a little smaller than normal, perhaps pointing to a little stronger demand for fresh bellies. It is always a bit concerning when the cutout seems to be carried by a single primal, particularly one as fickle as the bellies. On any given day two million pounds might show up in the spot market, driving prices lower and cratering the cutout. That is the risk that bulls need to consider in their newfound enthusiasm for long positions in the Feb and Apr futures. The Feb contract moved higher every day this week and finished on Friday just a hair under $75. At the beginning of January, that contract was trading near $65. So the there has been a strong bullish shift in trader’s attitudes. There are only 13 trading days left until the Feb contract expires and the LHI is still below $70. Traders must be expecting the steady diet of daily price gains to continue. All that said, I do think that we are seeing some modest improvement in pork demand. The combined margin has been moving higher for several weeks now and we’ve seen some very large production that hasn’t seemed to make a dent in price levels, so that is strong evidence of better demand. Of course, much of that demand improvement may concentrated in the belly primal, which is less impressive than if it was spread evenly across the carcass. The weekly export numbers continue to look strong, so that is probably helping to keep availability in the domestic spot market manageable. Carcass weights were reported down 2 pounds week-on-week and they are also running 2 pounds below last year, so that doesn’t point to a backup in the pipeline. Next week, watch the retail items to see how prices there respond to this week’s big production. Also, keep an eye on those negotiated markets for signs that the rally there might be fizzling out.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}