Pork Wrap January 21

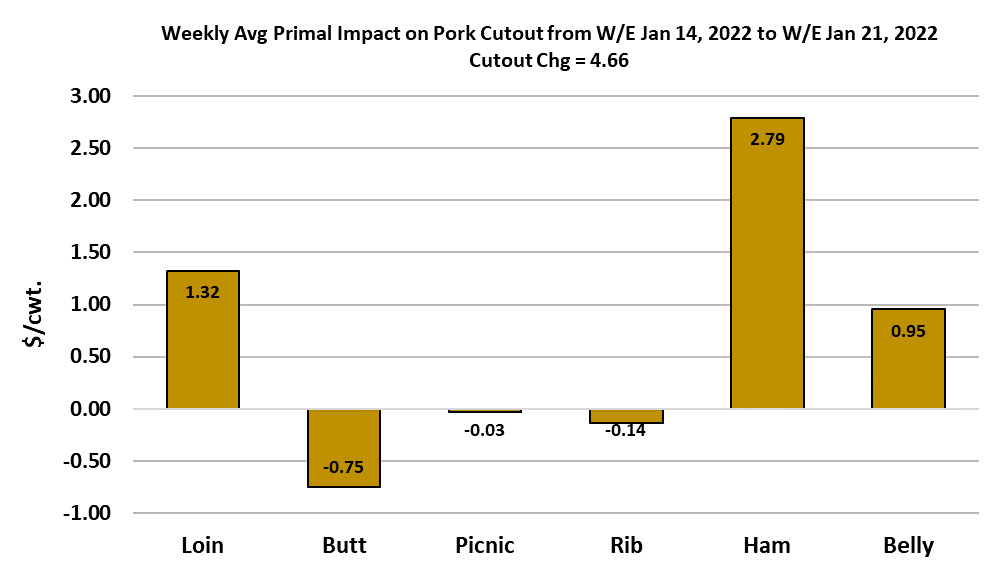

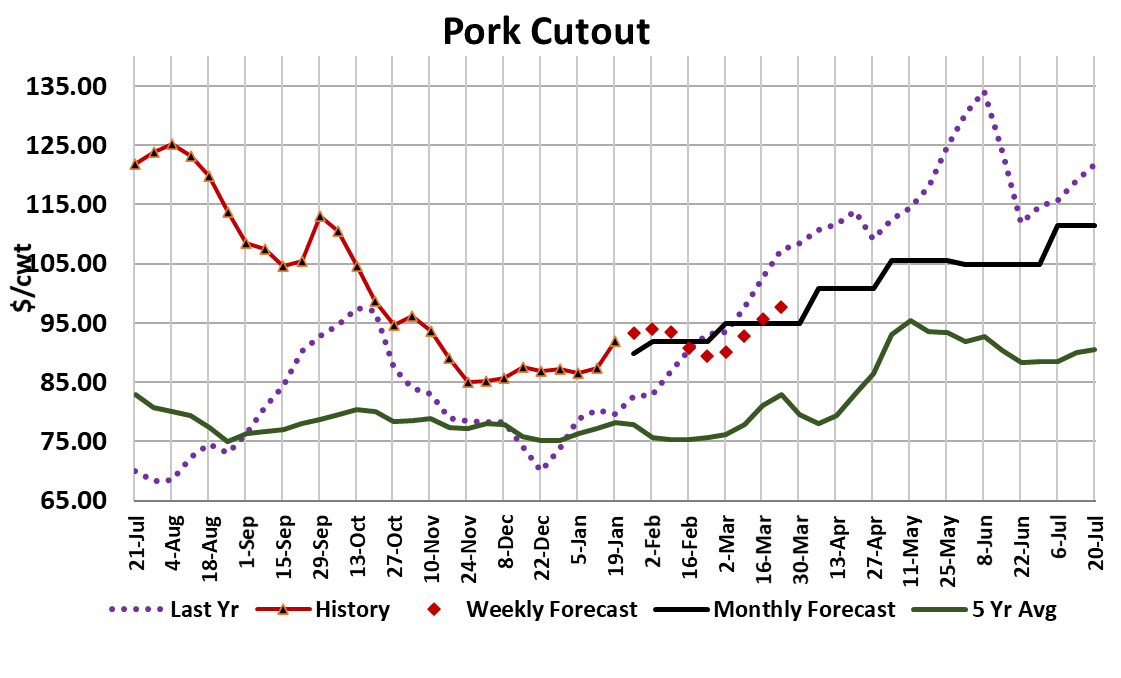

This week the pork cutout finally got enough traction to move above

the $90 mark. For the week, it was up $4.66 to average $92.03.

Hams were the primary drivers, with a little assistance from the loins

and bellies. Last week I noted that the hams had gotten ridiculously

cheap and would likely attract some buying attention. That seemed

to happen this week, but they also found support from light kills.

Packers did a good job of cleaning up ham inventories coming into

the week, so the light kill and low price levels made for an

environment conducive to price gains. Bellies also showed some life

this week and that may be a sign that processors are getting more

labor back on line.

Currently, bellies aren’t super cheap the way that hams were, but

they are cheap enough that some users may be building freezer

inventories ahead of tight fresh supplies this spring and summer.

Pork loins are making their way into retail ads as an attractive

alternative to expensive beef, especially now that holiday bills are

landing in consumer’s mailboxes. So there are good demand-side

reasons why the cutout is pushing higher, but we have also seen kills

constrained by omicron-related absenteeism and thus there is a

supply-side component to the recent price strength as well. Packers

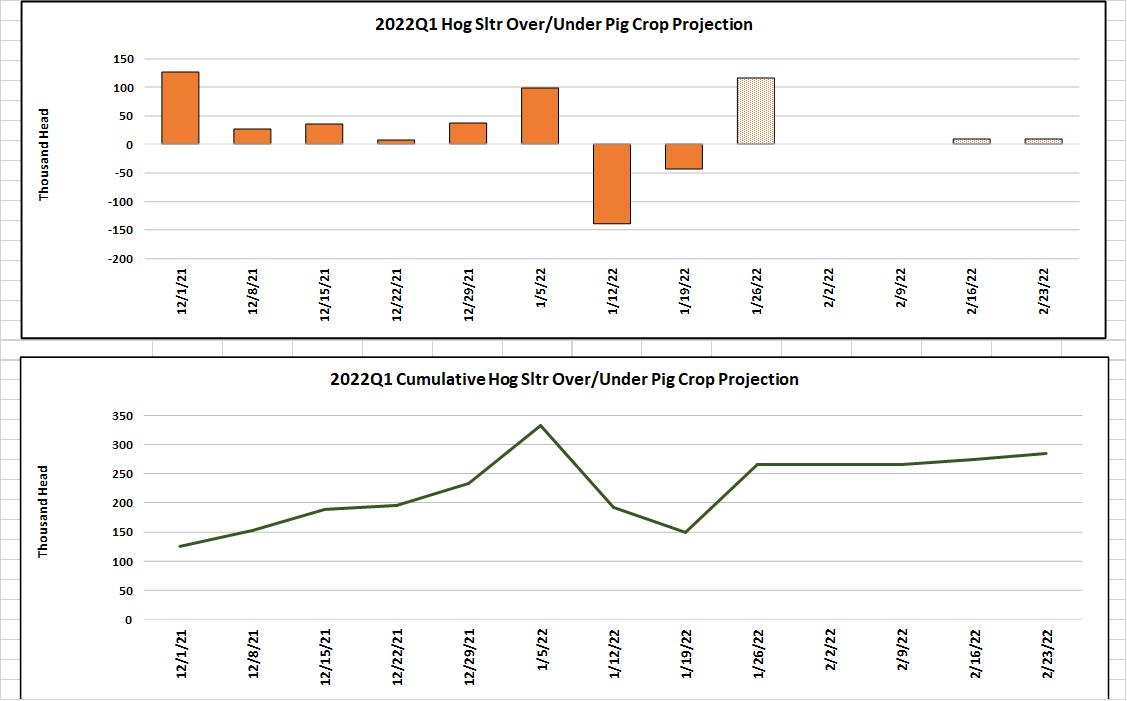

managed to kill 2.44 million head this week with the help of a fairly

strong Saturday kill, but the graph below indicates that was still about

50k less that what the pig crop indicated. Back in December, kills

were running larger that the pig crop implied and that makes me think

that USDA under-estimated the Jun/Aug pig crop moderately. So, if

we hadn’t had high absenteeism in the plants over the last couple of

week, by guess is that the kills would have been larger than the pig

crop implied by about 75-100k. Given that we underkilled by about

175k in those two weeks, it implies that we likely backed up about

250-275k hogs. That’s not a huge backlog, but it also isn’t

insignificant.

The weight data is also starting to point to some backing up in the

pipeline. Negotiated hog prices have been very volatile lately,

moving up then down in big chunks, but on a weekly average basis,

negotiated prices were a tiny bit lower this week. That also fits with

the idea that there are some extra hogs in the system. With each

passing week, packers should find it easier to get back on a full kill

schedule. If they can keep hog prices contained, they may even opt

to kill off some of the backlog in the next several weeks. That is the

thought behind my forecast next week for a kill around 100k over

what the pig crop suggested. A couple of weeks like that and the

backlog problem will be solved. The wild swings in daily hog prices

has made it difficult for futures traders to identify the trend in those

markets, so instead they have just focused on the cutout which has

been mostly up.

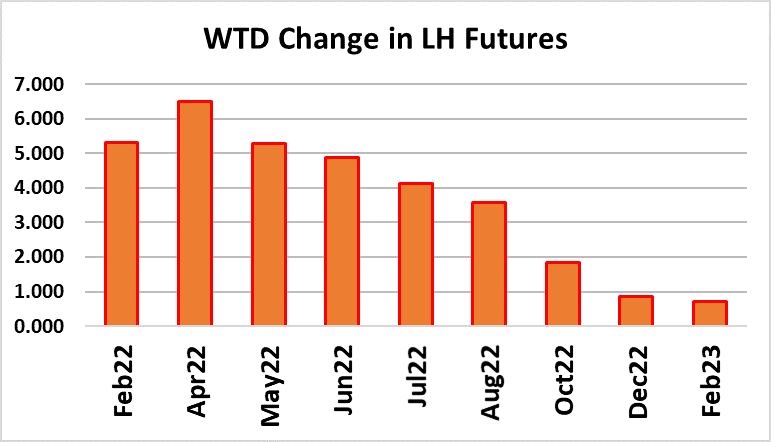

The Feb futures gained over $5 this week and the Apr were up

more than $6 as a rising cutout brought the bulls back out. But even

the cutout is difficult to decipher, often swinging $5-10 from

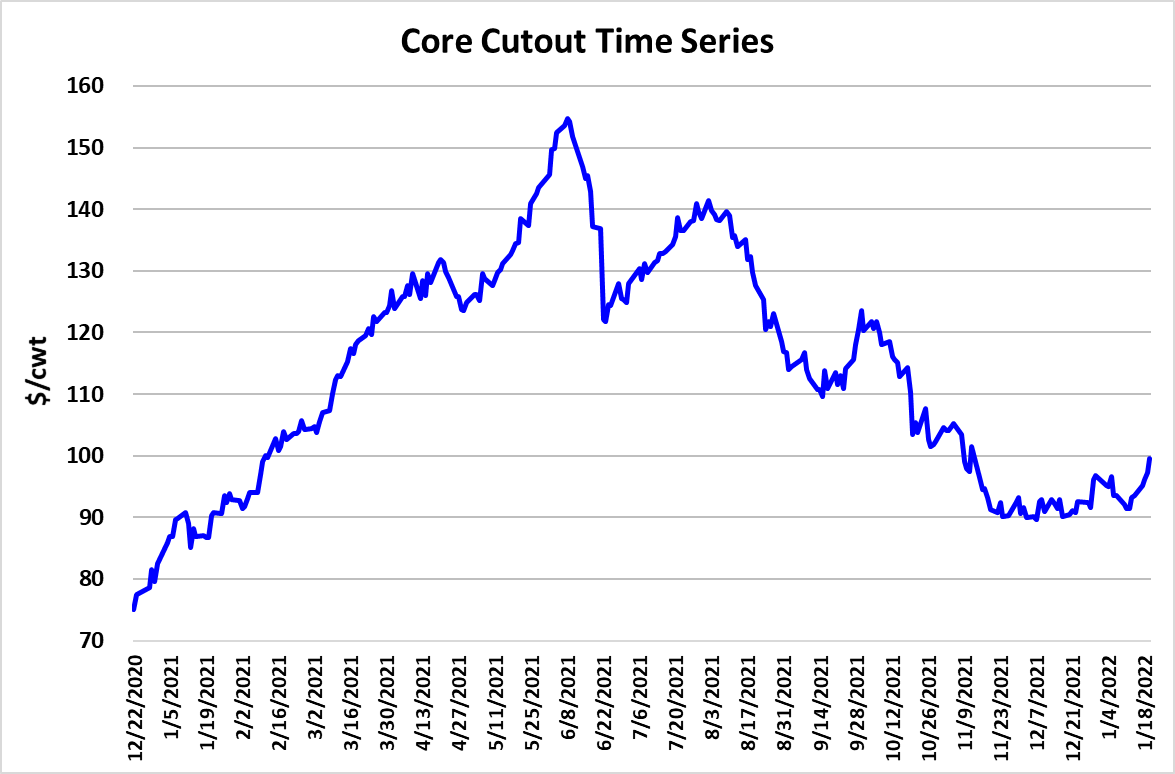

morning to afternoon. To help bring some clarify that problem

somewhat, I created a “core” cutout that is comprised of one item

from each primal that is minimally processed (so that labor is not a

big factor) and weighted those items according to the percentage

each primal contributes to the cutout. Trim is also included. The

chart below indicates a strong move higher in the core cutout

recently, going from around $90 to near $100 at the close today.

So we have evidence that this recent move is solid and not just

based on a shifting mix of products.

My guess is that improvements in labor availability over the next

several weeks will cause the core cutout to track more steady than

uptrending. With the cutout rising and the cash hog markets

steady, packer margins added about $6/head and are now close to

$29/head. That makes it the largest margin ever for this point in the

calendar. Normally margins soften in January and February in

response to seasonally softer demand, and I expect that will be the

case this year as well. The forecast has packer margins averaging

around $26/head in January and $19/head in February. In fact,

margins should continue to work lower from now until mid-July in

response to a seasonal downtrend in hog numbers. It is worth

noting that international demand for US pork is looking pretty weak

right now, compared to recent years. Fortunately pork production

is also smaller, so that has helped to offset the impact of having to

move a greater percentage of production in the domestic market.

Demand in the domestic market seems okay, but not great.

The combined margin did turn higher this week, so maybe we are

finally going to get that demand upcycle that has been anticipated.

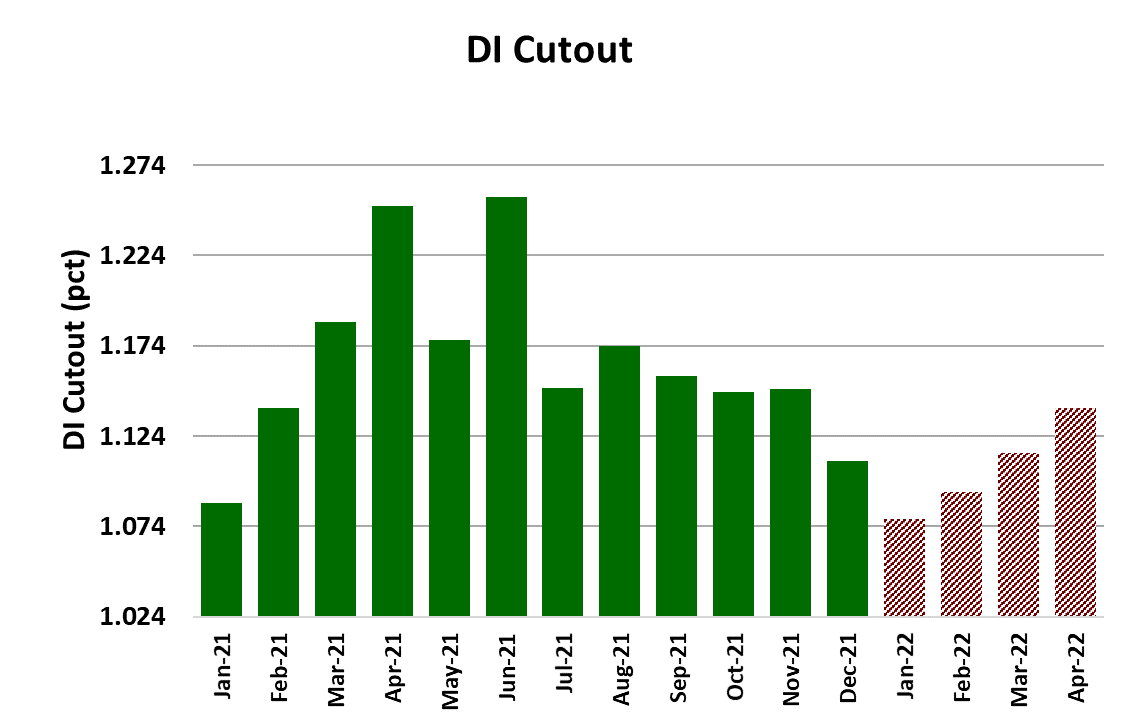

However, the bar chart below plots the cutout demand index by

month and you can see that demand here in January is at almost

the same level it was last January. Thus, the YOY difference in

pork prices is being driven more by constrained supply than

exceptional domestic demand. At this time last year demand was

mediocre but “great pork demand surge of 2021” was about to

begin in February. Now it looks like demand is back close to presurge levels. The combined margin chart gives that impression

also. Next week, keep an eye on the daily kills for signs that the

labor problem is easing. Also, watch the weekly weights for signs

that hogs are backed up.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}