Pork Wrap January 20

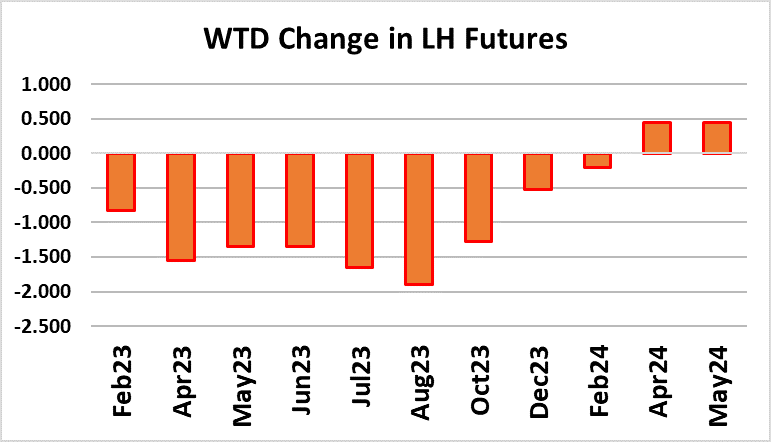

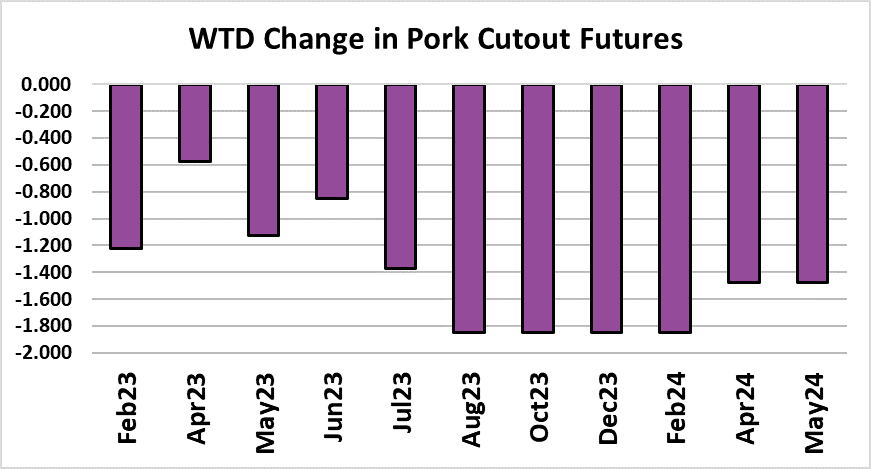

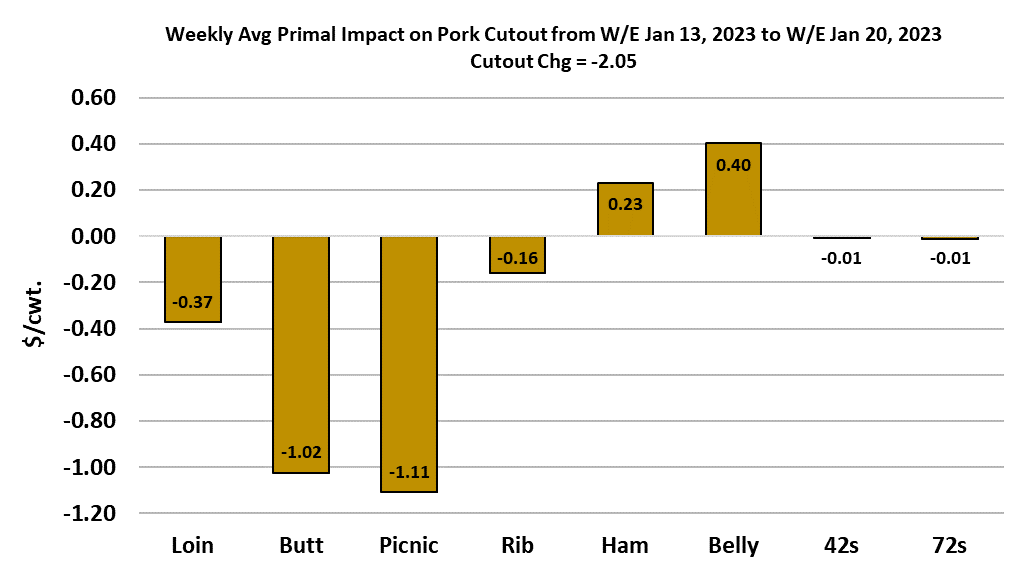

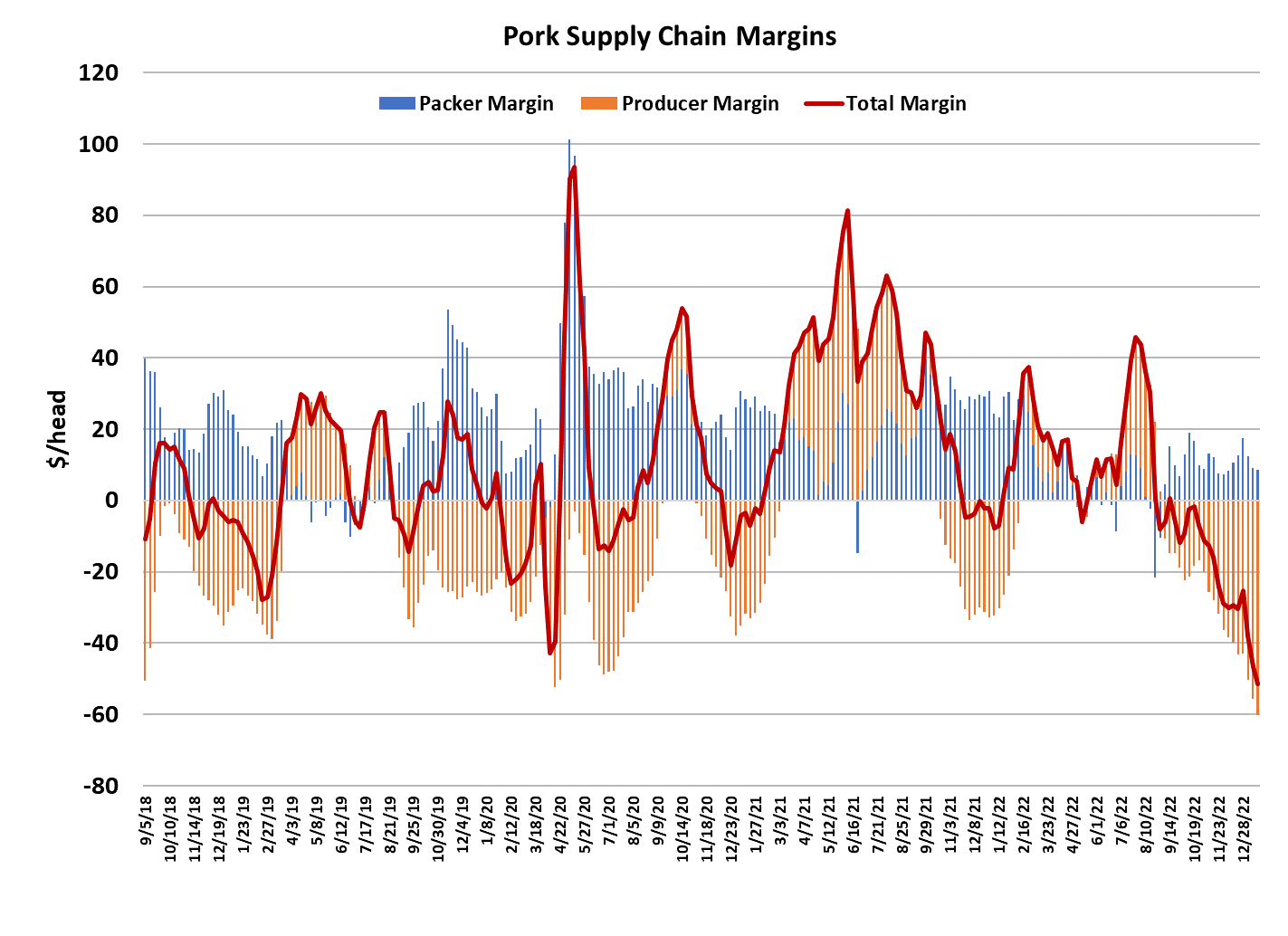

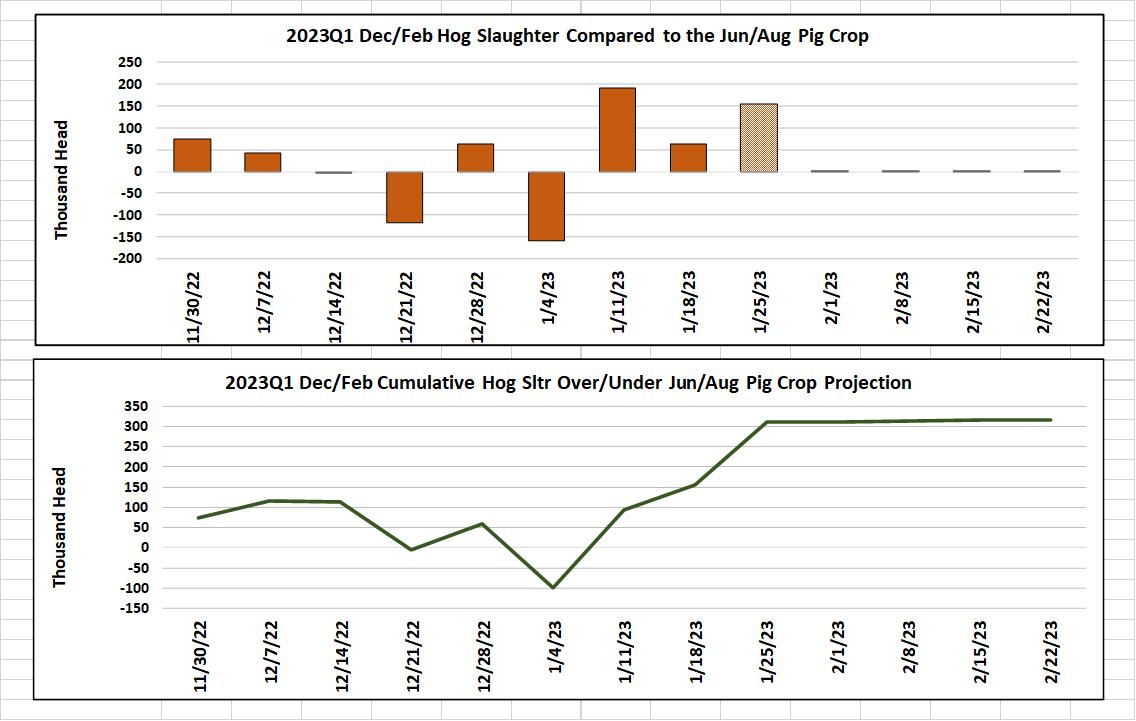

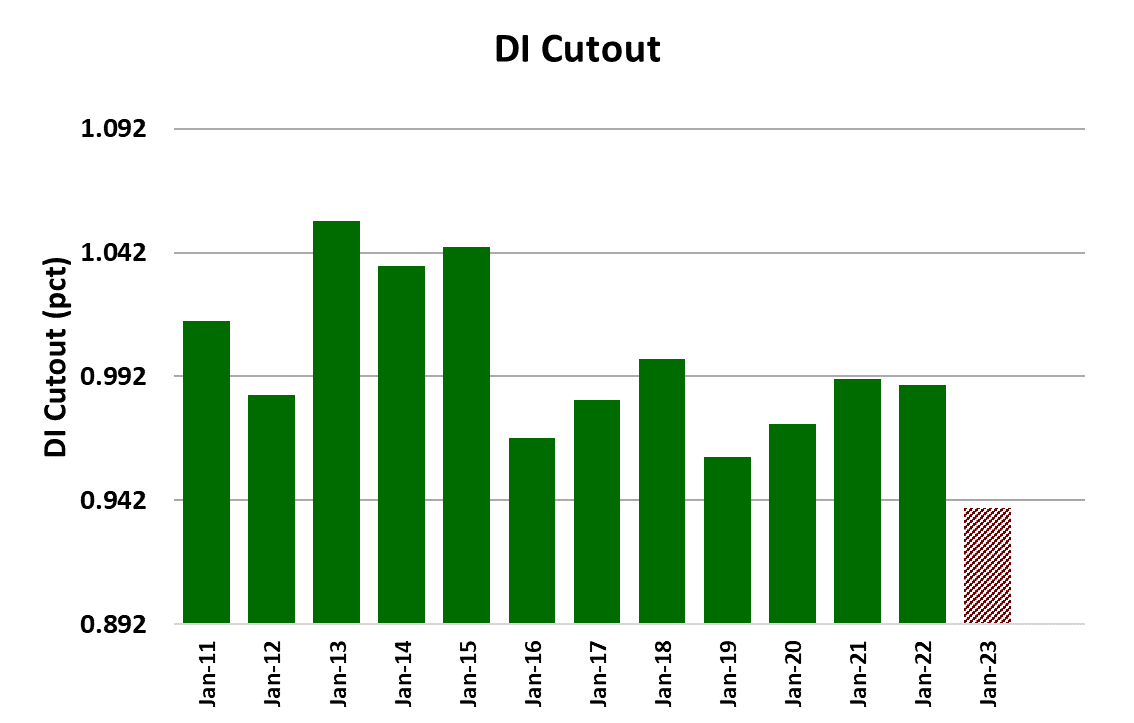

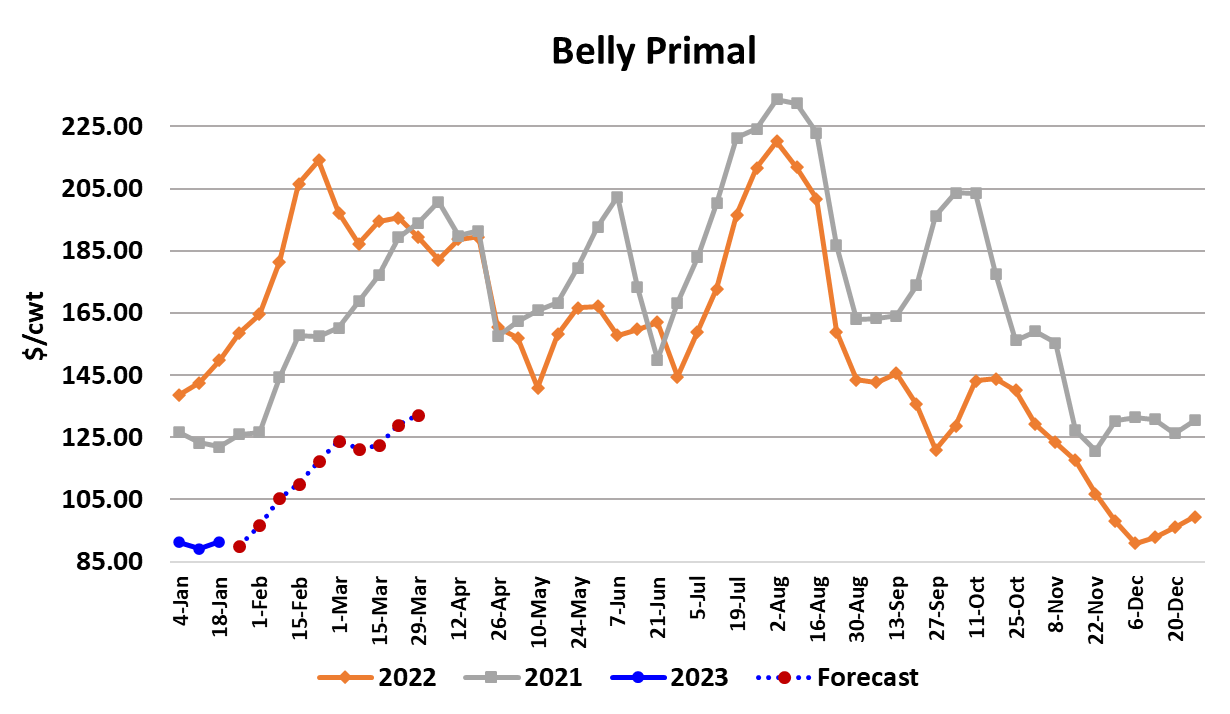

Pricing in the hog and pork complex was softer yet again this week, with the cutout dropping $2.05/cwt. and the WCB cash market down $2.54/cwt. It is not surprising that the market buckled a bit under the weight of last week’s huge 2.68 million head kill. This week the kill registered 2.53 million head, but may have been hampered a bit by a snowstorm that crossed Iowa. Even so, that total was still above what the Jun/Aug pig crop projected and the cumulative over-kill for the quarter is now about 300k. Next week’s kill is expected to add to that, so with a little over a month to go in the current quarter, it is looking like the summer Hogs and Pigs report understated the pig crop modestly. That, combined with holiday and periodic weather disruptions probably backed up some hogs that are now getting cleaned up with big kills. One indicator of that is the barrow and gilt FI carcass weights, which have surged five pounds in the past two weeks. The DTDS weights also shot higher this week. Another indicator is pricing in the negotiated markets, which continues to slide lower. The WCB printed below $70/cwt. on Thursday and Friday and is now tracking below national negotiated price. It is a world of difference between now and the summer months that saw the WCB hit $135/cwt and consistently run several dollars premium to the national price. Not to worry though, producers will have their day in the sun again during the spring and summer months when hog supplies tighten back up. The cutout continued to drop this week as the retail items came under pressure from heavy production. Loins, butts, pics and ribs were all lower on the week. The processing items were a little higher, but not by enough to offset the weakness in the retail items. For the fourth week in a row, the Monday print on the cutout was the highest of the week and it deteriorated from there. There was a little upturn in the cutout on Thursday and Friday this week, but close analysis of what was driving that makes me think that it might not have staying power. Going forward, weekly kills should get a tiny bit smaller every week, so perhaps that will provide a floor under the cutout and help it to move back over the $80 mark. Picnics are in the midst of a big seasonal downdraft that should be just about complete. Look for those to trade mostly sideways through February. Butts should track similarly. Loins normally see improving retail interest in late winter and the forecast there points higher. But, if there is going to be any significant improvement in the cutout, the hams and bellies will need to be involved. The ham primal gained a smidge this week, but it is still near its lowest level in almost nine months. Packers really need Mexico to come to the rescue and scoop up some of these cheap hams. Hog and pork prices in Mexico are much higher than in the US, so the value proposition for exporting hams to the south is there, it just hasn’t kicked in with the same strength that we saw in the second half of last year. Bellies have been languishing in a sideways pattern at very low levels since early December. It seems like there should be nowhere for those prices to go but up. However, the bellies are plagued by heavy stocks in cold storage. The last data available shows bellies in cold storage at the end of November over double the previous year and December normally sees further increases, so when the next cold storage report is released on Wednesday, it could show further gains in belly stocks. The last time we had belly stocks this large was in late 2019 heading into 2020 and in that year belly prices stayed weak through April, and actually declined from January to April. So maybe I’m expecting to much by calling for a rebound in the bellies over the next few weeks. That leaves hams and loins as the best hope for stopping the slide in the cutout. Watch those closely. Sow prices appear to be bottoming now, right on schedule with the normal seasonal pattern, but there is very little correlation between sow prices and the cutout. The combined margin chart is so depressing it is difficult to even talk about it. High feed grain prices combined with soft pork prices produces this type of situation where there isn’t much margin for either packers or producers. Producers, in particular, are having a hard go of it and I calculate their margin at something close to -$60/head this week. Packer margins were close to $8/head, which is far less than what they are used to making in January. I think the hog and pork complex is in the midst of a big reset where prices are transition back toward pre-pandemic levels. Traders that got used to hog prices in the $120s during the summer are likely to be sorely disappointed this summer if prices barely break into triple digits. The highs will be lower and the lows will be lower. We are experiencing a lower low right now. Maybe not all the way back to pre-pandemic levels because there has been some macroeconomic price inflation, but likely well below pandemic levels. The past two years have made us forget that the cutout used to rarely visit triple digits and hog prices often dipped into the $60s and even $50s. All that said, this current downdraft in demand is exceptional. The attached chart shows the demand index for January across a large number of years. Keep in mind that these demand indexes are inflation-removed. Prior to the pandemic we used to see periodic demand “air pockets” for pork. It looks like that feature may have returned. Throughout the pandemic pork demand generally led beef demand by a month or two. Maybe pork is now giving us a peek at what may happen to beef demand this spring. The only ones happy about this situation are pork buyers and those short the futures. Next week, watch the hams and loins—they have the most potential to move higher. The cold storage report will also be a must-read.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}