Pork Wrap January 19

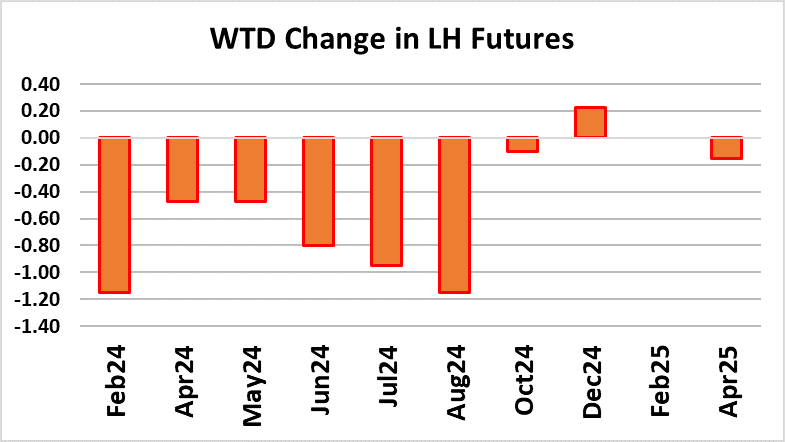

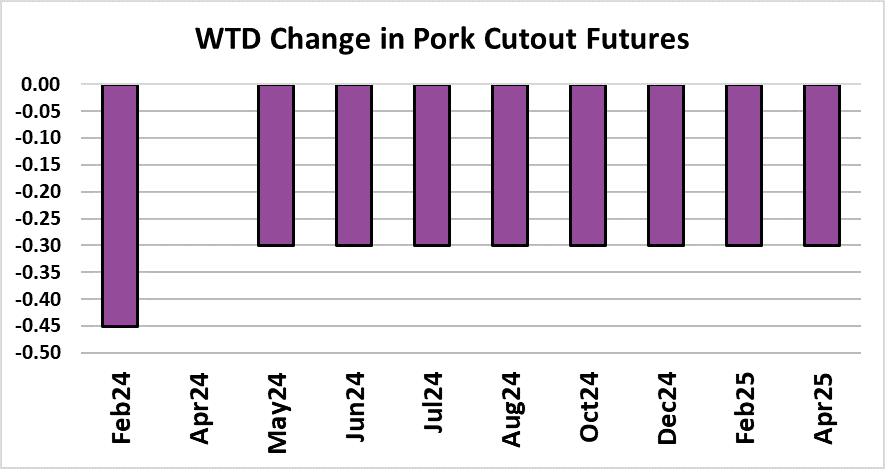

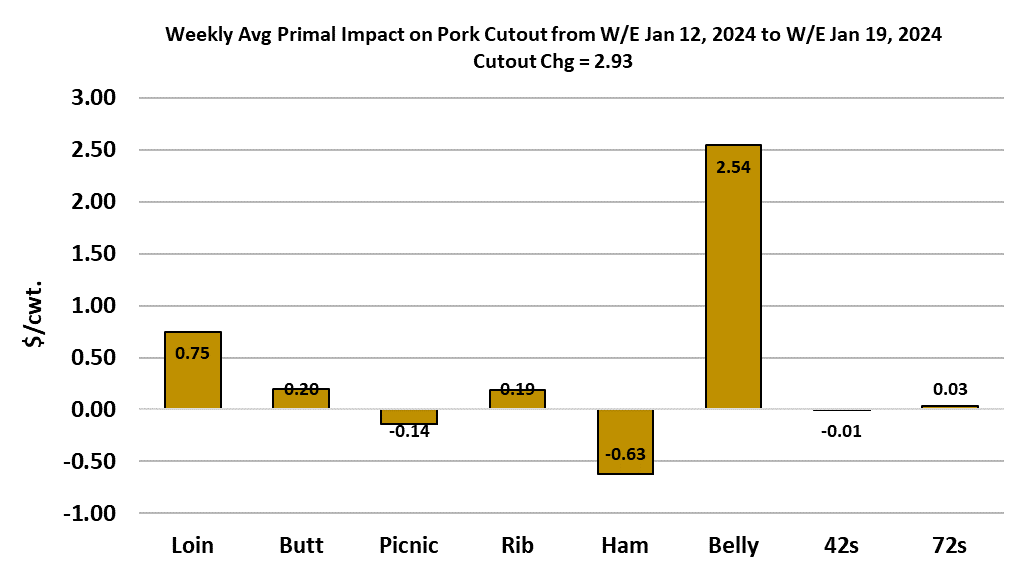

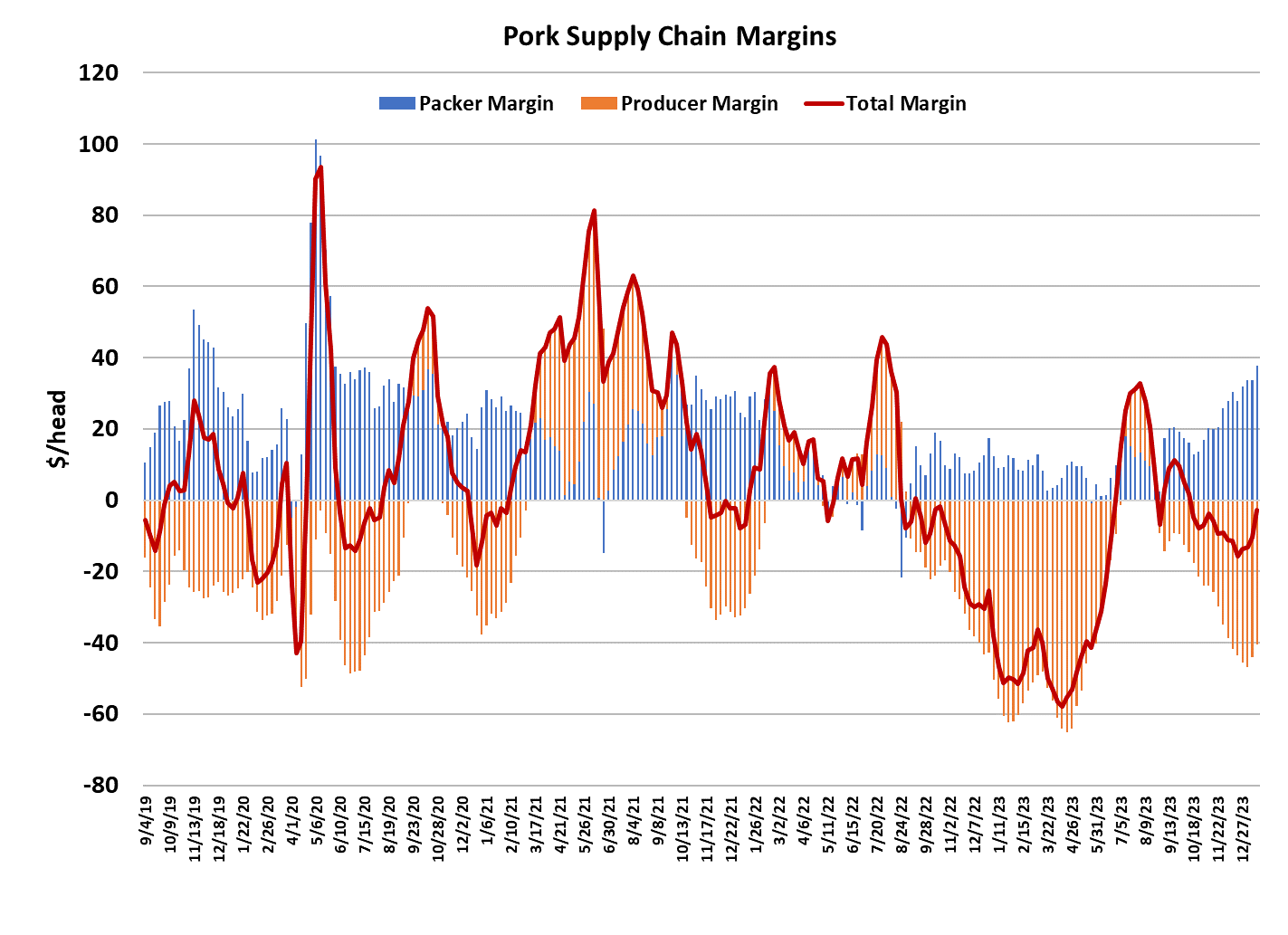

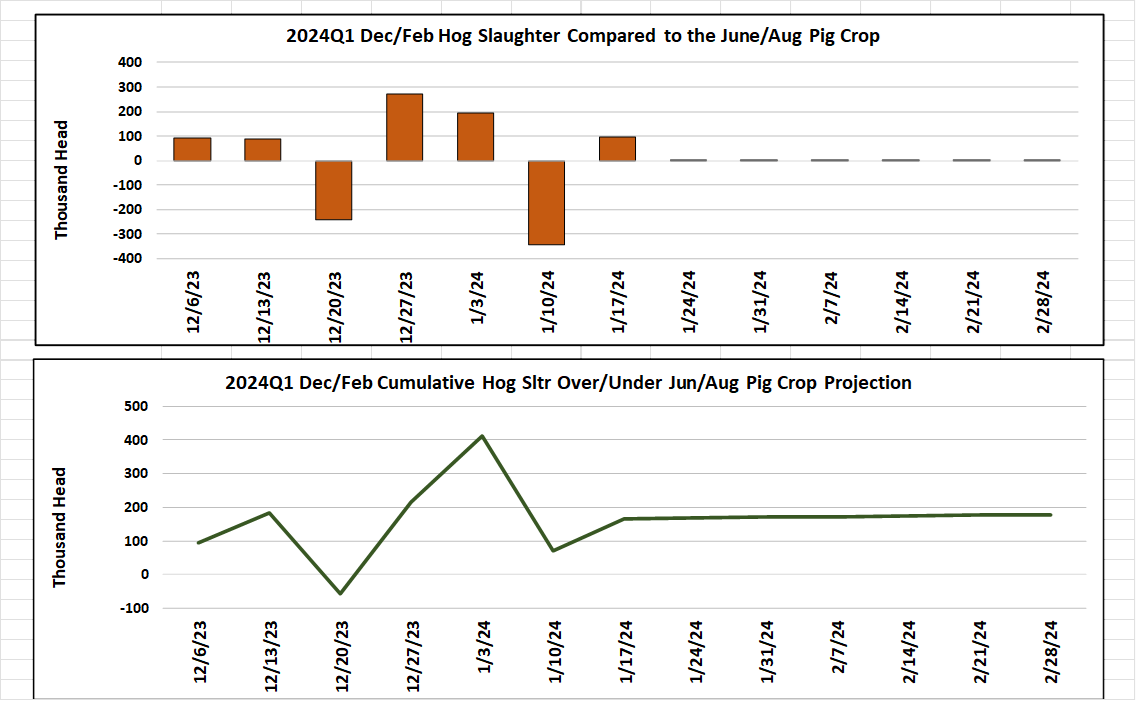

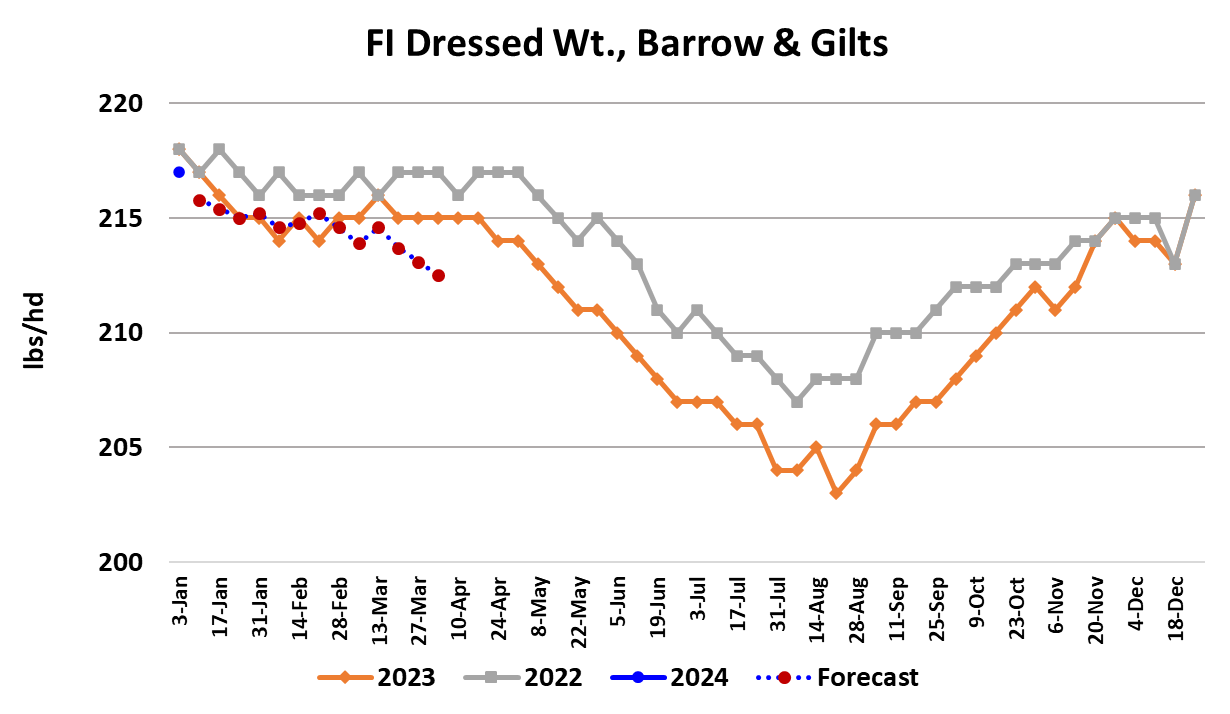

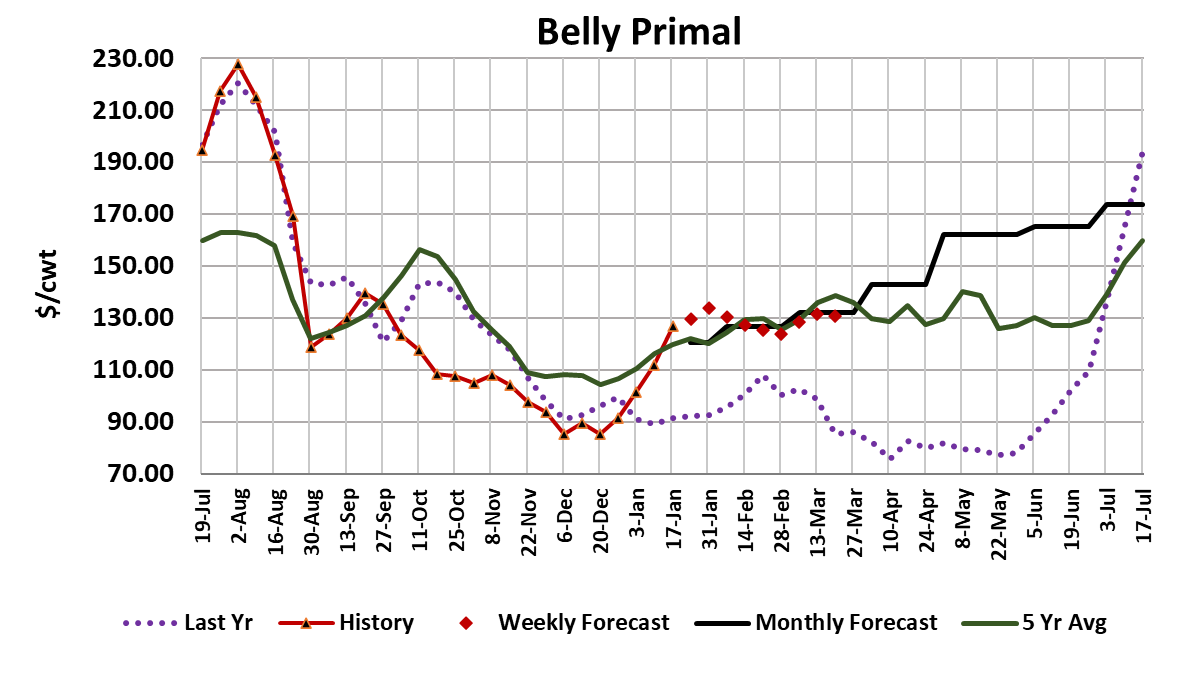

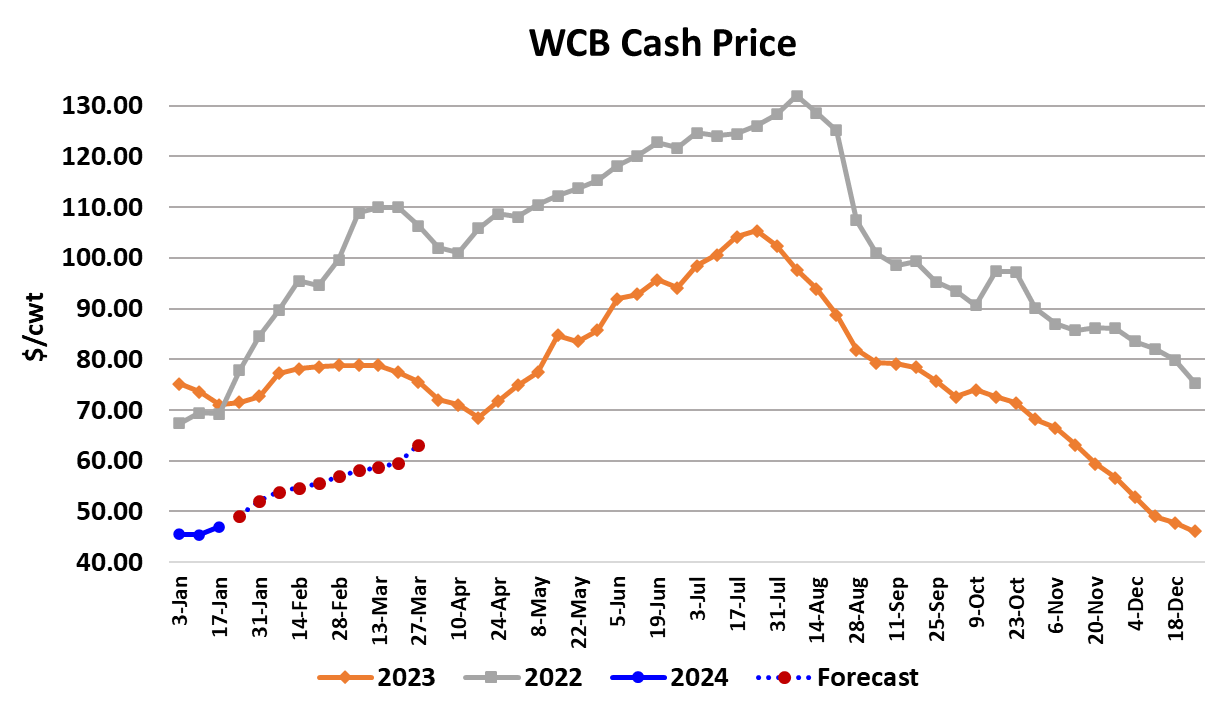

This week, the pork cutout posted its largest weekly gain since Labor Day, up $2.93/cwt. on a weekly average basis to $88.02. That rally was led by the bellies and it happened in a week where production returned to near-normal. As a result, it easy to conclude that the strength in bellies recently is a result of improved demand and not just a function of low product availability brought on by recent holidays and weather events. The belly primal averaged close to $127 this week and that represents a 48% price increase in the past 30 days. Of course, it isn’t likely that the belly primal will see that type of gain over the next 30 days, but I do think it will continue to firm, only at a slower pace. Loins were the second biggest contributor to the cutout gain this week but I’m more inclined to think that one was more a function of unexpectedly tight availability hitting right at the time when retailers were poised to feature loin items to cash-strapped consumers post holidays. Let’s see if they can hold these gains next week when the kill could hit 2.7 million head. On the other side of the ledger, the hams appear to be struggling a bit, with the primal losing $2.34 on a weekly average basis. I don’t expect the hams to move sharply lower since there always seems to be willing buyers at only a slight discount, and that leaves me thinking that they will trade mostly sideways to slightly lower over the next few weeks. The combined margin moved decidedly higher this week after several weeks of lukewarm gains. Perhaps that means that a new demand upcycle has begun—something the industry needs very badly. Some demand improvement will be necessary in the next couple of weeks simply to offset the price-negative influence of the very large kills which packers most likely will generate in an effort to capitalize on very strong margins. There should be plenty of hogs available to generate those high slaughter levels because some hogs may have been delayed in moving to slaughter by the weather last week and the holidays in the two weeks before that. How many hogs were backlogged by those three weeks of light kills? It is hard to know for sure, but if we look at the weekly slaughter chart relative to what the Jun/Aug pig crop implied, we see that the short kill due to weather in the week of Jan 10 was almost exactly offset by bigger-than-expected kills in the two holiday weeks so that Jan 10 reduced kill might not have backed up as many hogs as it appears. Halfway through the Dec/Feb quarter the over-kill is only 175k, even with that Jan 10 short week. Of course, USDA may still be way too low on the pig crop so the next few weeks could also be characterized by big overkills, but I don’t think the weather disruptions backlogged very many hogs at all. If there was a big backlog of un-slaughtered hogs, then I’d expect to see cash hog prices sliding lower and that just isn’t happening. Negotiated prices in the WCB region actually advanced $1.54 this week. All of that said, it does look like packers could be planning a 2.7 million head kill next week so we definitely aren’t running out of hogs in the near-term. It is worth noting that prices in the hog and pork complex are often very trend-prone and the trend seems to have shifted from lower in late 2023 toward higher prices here in early 2024. The cutout and the LHI have both worked higher recently and the normal seasonal is for prices to rise a bit heading into February expiration. Bellies trending higher is a big driver. I don’t want to argue that the cutout is going to roar higher, because the fundamentals are not that bullish, but it may not have a lot of downside risk here. Instead, a sideways to slightly higher pattern for the cutout over the next few weeks seems like a reasonable expectation. Of course, we know that pork demand is still terrible from a historical perspective, but what are the odds that it gets worse from here? Not very high. Eventually, kills will moderate seasonally and that should help price levels higher. Packer margins are now near $37/head, which is up about $4 from last week and producer margins are near -$40/head, also up about $4 from last week. Hence, the strong increase in the combined margin. Going forward, I’d look for producer margins to slowly improve and packer margins to slowly shrink. Barrow and gilt carcass weights increased another pound to 217, but the data was for the second week of the holidays, so not unexpected. We will need to watch carcass weights closely over the next couple of weeks because that can provide more information on the risk of hogs being backlogged. So far, I don’t see much there. Next week, I think the storyline is going to center around the size of the kill and how much ground, if any, the cutout gives up. If we do get a kill in the area of 2.7 million head and yet the cutout can post even a very small gain, then that would provide a high degree of confidence that the upward trend in prices is likely to continue.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}