Pork Wrap January 14

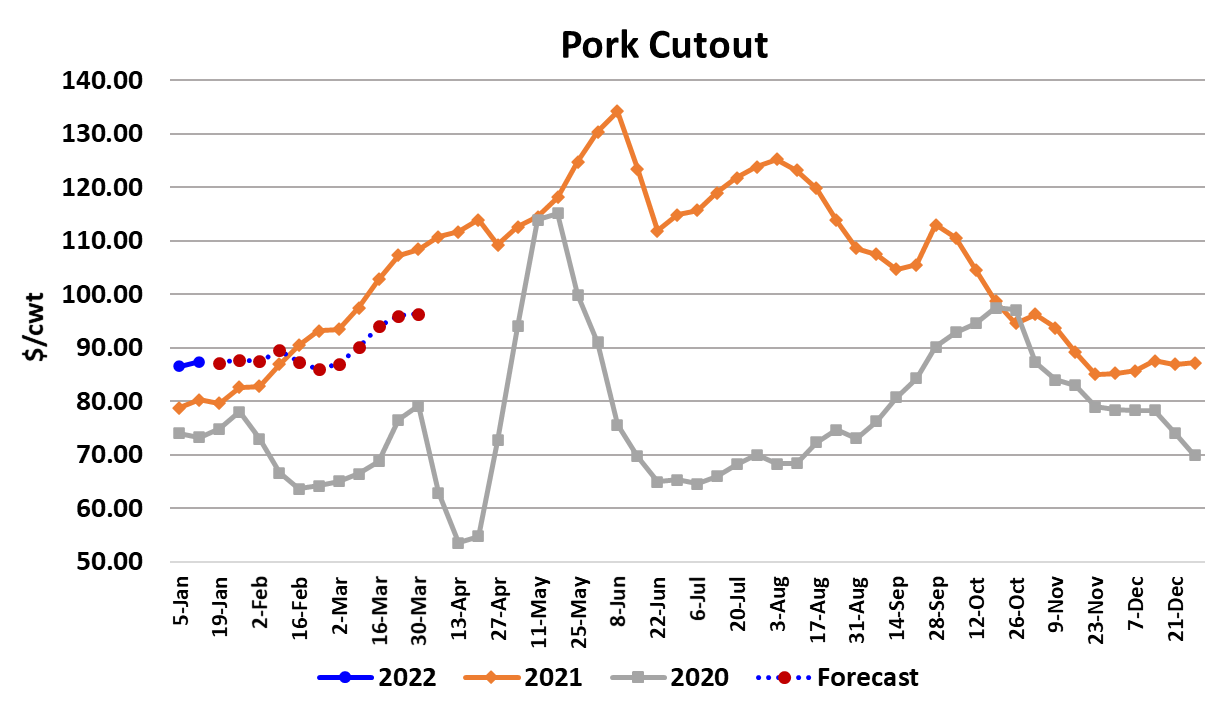

I could say that this was yet another week where the pork cutout went

nowhere since it averaged $87.37, only $0.80 higher than last week’s

average. However, that would ignore the wild day-to-day volatility we

saw. On Tuesday, the cutout finished at $81.62 and on Thursday it

closed at $95.28. Needless to say, Thursday was a big day for

boneless hams. This was the first week in a while where the hams

and bellies weren’t the biggest influencers on the cutout. This week,

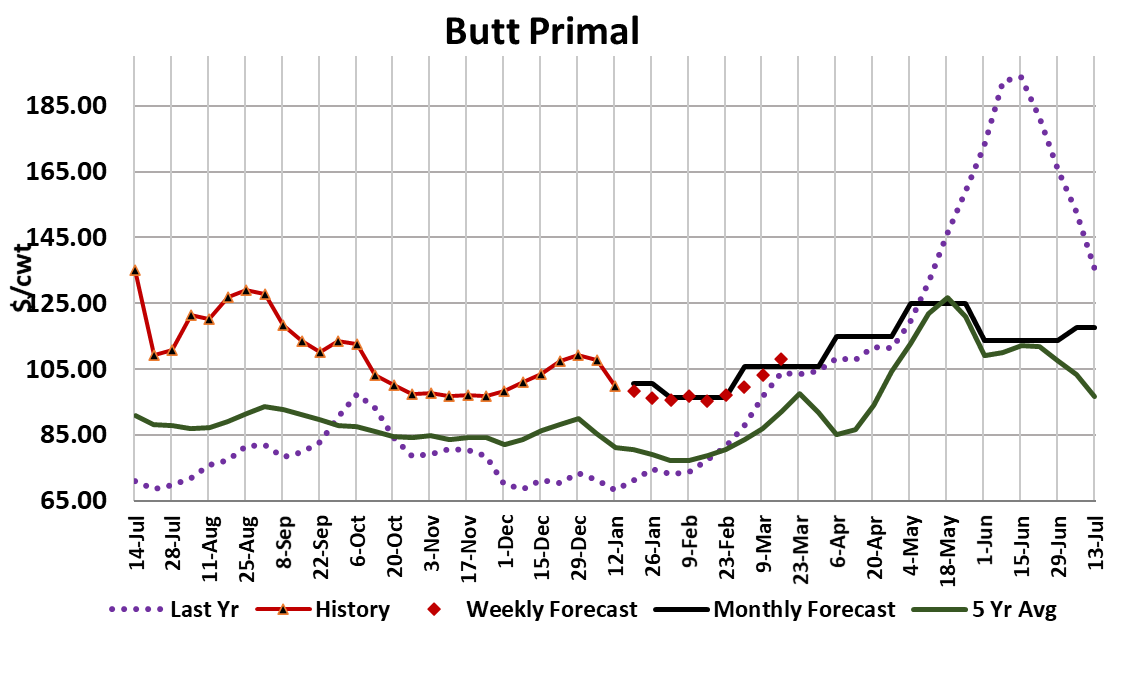

the loins came to life toward the end of the week. Butts and picnics

were a drag on the cutout this week and I’m more than just a little

concerned about those going forward. Both are typically soft in Jan/

Feb and it looks like this year they are going to follow the normal

seasonal pattern after bucking it last year. I think the other primals

will have to overcome the weakness in butts and picnics over the next

couple of weeks if the cutout is to gain any real traction.

Last week I talked about how COVID absenteeism was adversely

affecting packers’ ability to process hams and that was causing bonein hams to get dumped on the market at low prices. At one point this

week, the 23/27 lb hams were quoted below $40/cwt—the lowest in

almost seven years. Volumes on the bone-in hams were huge. A

good portion of those are likely headed for the freezer and will be

processed later when labor is more available. The bone-in hams did

eek out some small gains late in the week, but there is considerable

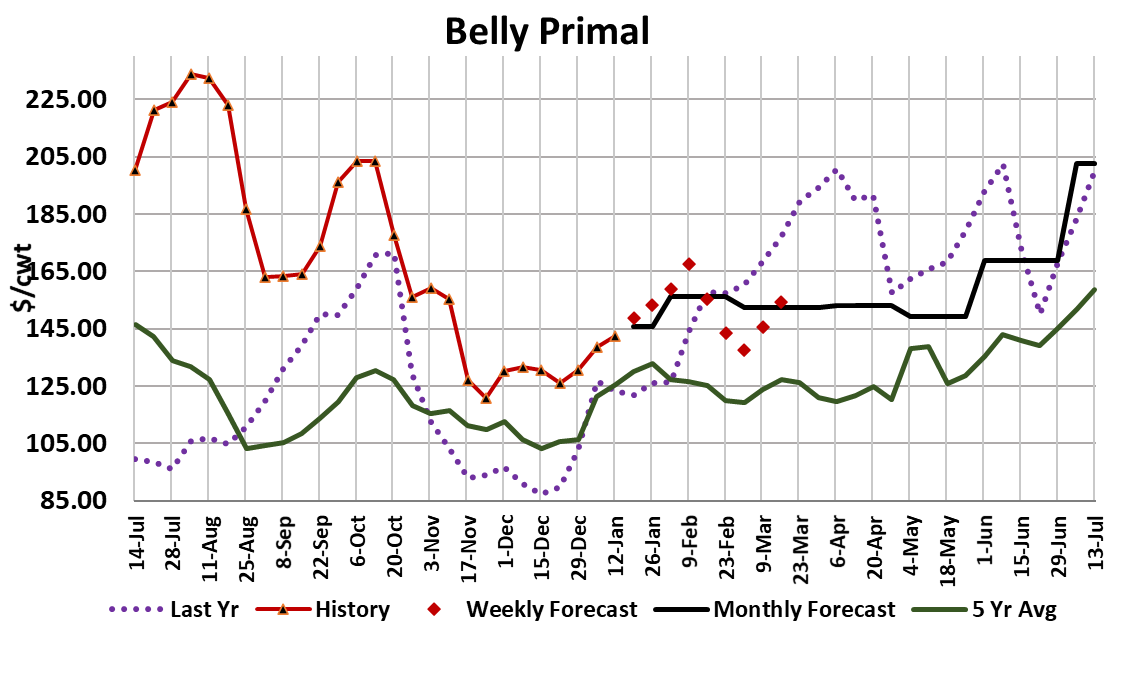

risk that those gains don’t stick. The bellies fared better this week,

posting their third weekly increase in a row. I see those continuing

higher and even at current price levels some users might opt to move

bellies into cold storage ahead of a stronger pricing environment this

spring and summer. The forecast has the cutout holding in the midto-high $80s for the next several weeks with bellies and loins helping

and butts and picnics hurting the cutout.

Hams are the wild card that could cause the cutout to be stronger or

weaker than currently forecast. Packers are still struggling with

absenteeism in the plants and that fact was evident in this week’s

kills. The daily kills were revised a lot this week and mostly

downward. The average weekday kill was right at 446k, compared to

about 480k per day back before Christmas. Further, packers did a

Saturday kill that was almost 100k less than last week, putting the

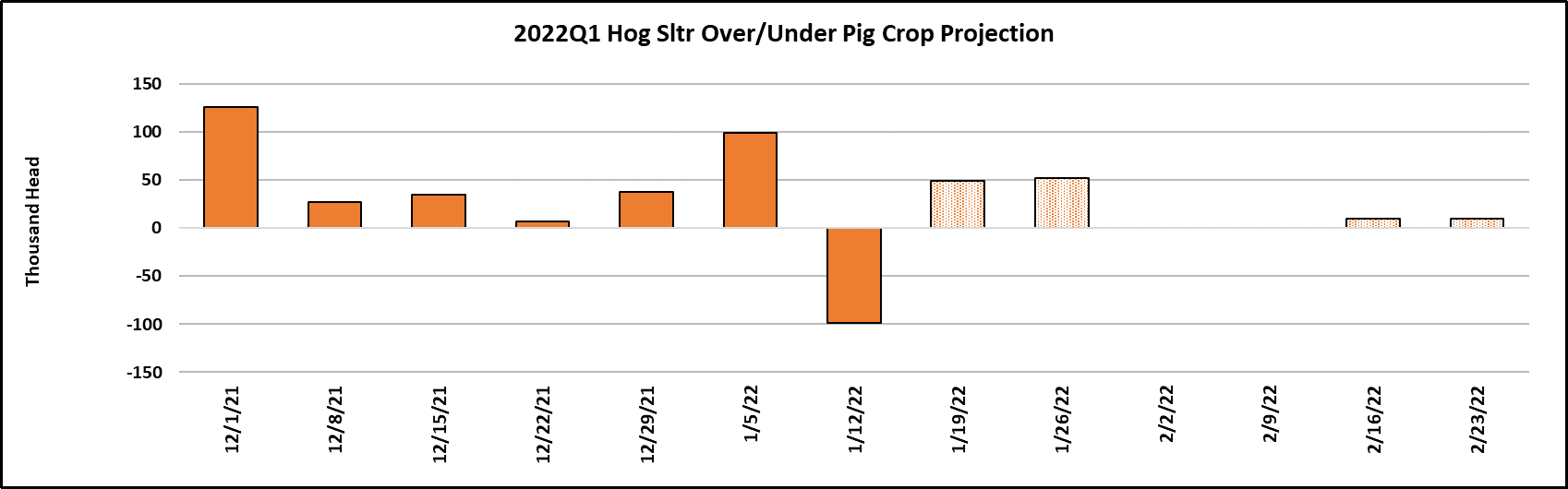

weekly total at a paltry 2.41 million head. This was the first week in

the Dec/Feb quarter where the kill failed to live up to the pig crop

projection. It was about 100k short of it. That will probably back up

some hogs in the pipeline, especially if packers struggle again next

week. Fortunately for producers, hog weights are not excessive at the

moment and they may be able to dial back the energy component of

rations for a couple of weeks and manage this problem without too

much price concession.

Nationally, negotiated cash hog prices were steady this week, but

the WCB region saw a $2 price increase. The LHI gained about a

dollar on the back of a little stronger cutout and now sits at $74.32.

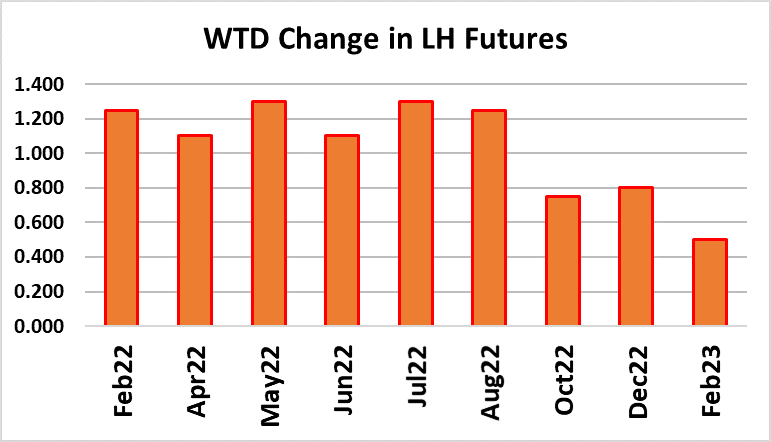

Nearby futures moved lower early in the week as traders continued

to be disappointed by the lack of upward movement in the LHI.

However, Thursday’s $95 cutout print sent the Feb futures soaring

on Friday and pushed the contract into positive territory for the

week. I expect that it will probably take a couple more weeks

before the omicron train has run its course and plants are able to

operate at normal capacity again. This week packer margins

averaged close to $23/head, down about $1 from the week before.

I’m more than a little surprised that margins haven’t ballooned out

in response to the constriction in processing capacity

Normally we would expect pork prices to shoot higher as less is

produced and hog prices to move lower as the pipeline backs up.

Neither has happened so far. Margins are rapidly increasing for

beef, but not so for pork. It is possible that soft exports are

keeping more product at home and thus tempering the price impact

of smaller kills. There is also the Prop 12 issue, whereby all pork

sold in the state of California has to be produced from sows that are

given more space than is common in the industry. Theoretically,

Prop 12 compliant pork should sell for more than commodity pork

and as a result we should see less pork consumption in California.

That would leave more to be consumed in the other 49 states and

have a downward influence on the pork prices that go into USDA’s

cutout calculation.

From what I understand, the high-priced Prop 12 pork is not going

into the cutout. USDA is treating that more like specialty pork. Still,

no one really seems to know how Prop 12 is actually affecting the

market, if at all. This issue has been pushed into the background

by the omicron-induced labor problems, but it has the potential to

be a significant factor in the weeks and months ahead. My guess

is that it will have a moderately negative effect on the cutout and

thus on hog prices, but until we hear more from California retailers

on how the new law is working, there will be a lot of uncertainty and

speculation around this topic. Next week, watch the daily kills for

signs that the plant labor problem is improving. Expect the cutout

to average in the high $80s, with a strong likelihood of big daily

price swings.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}