Pork Wrap January 13

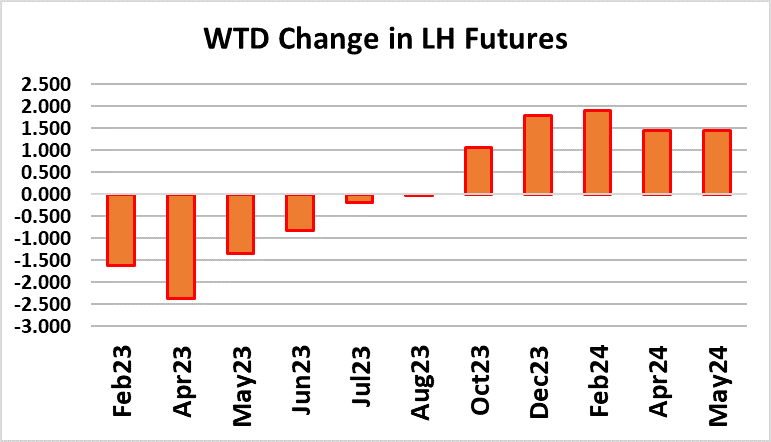

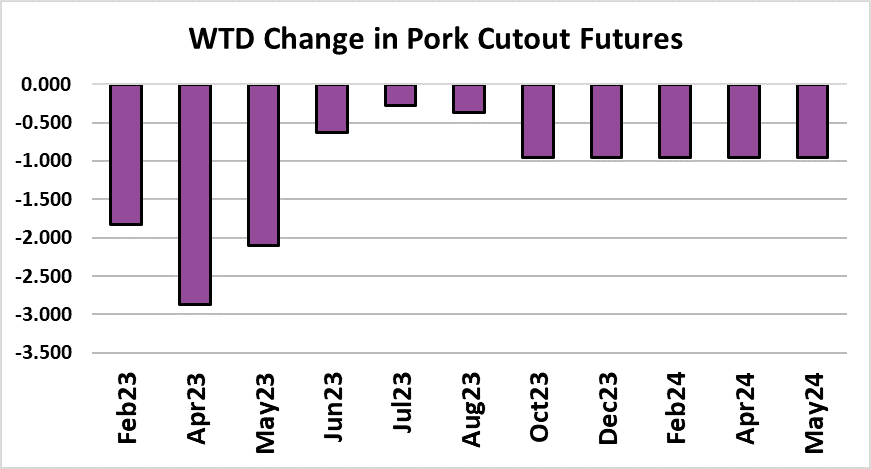

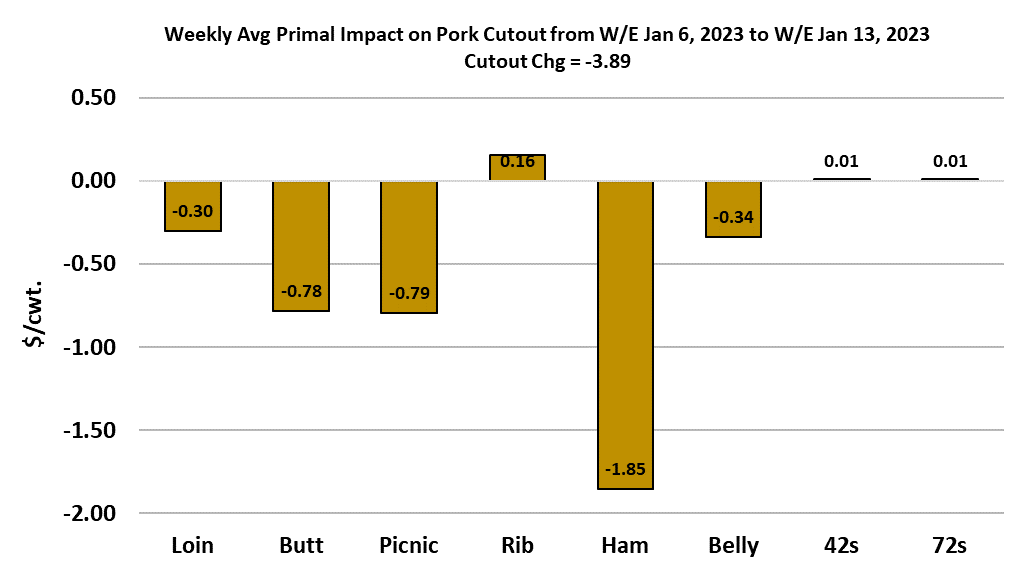

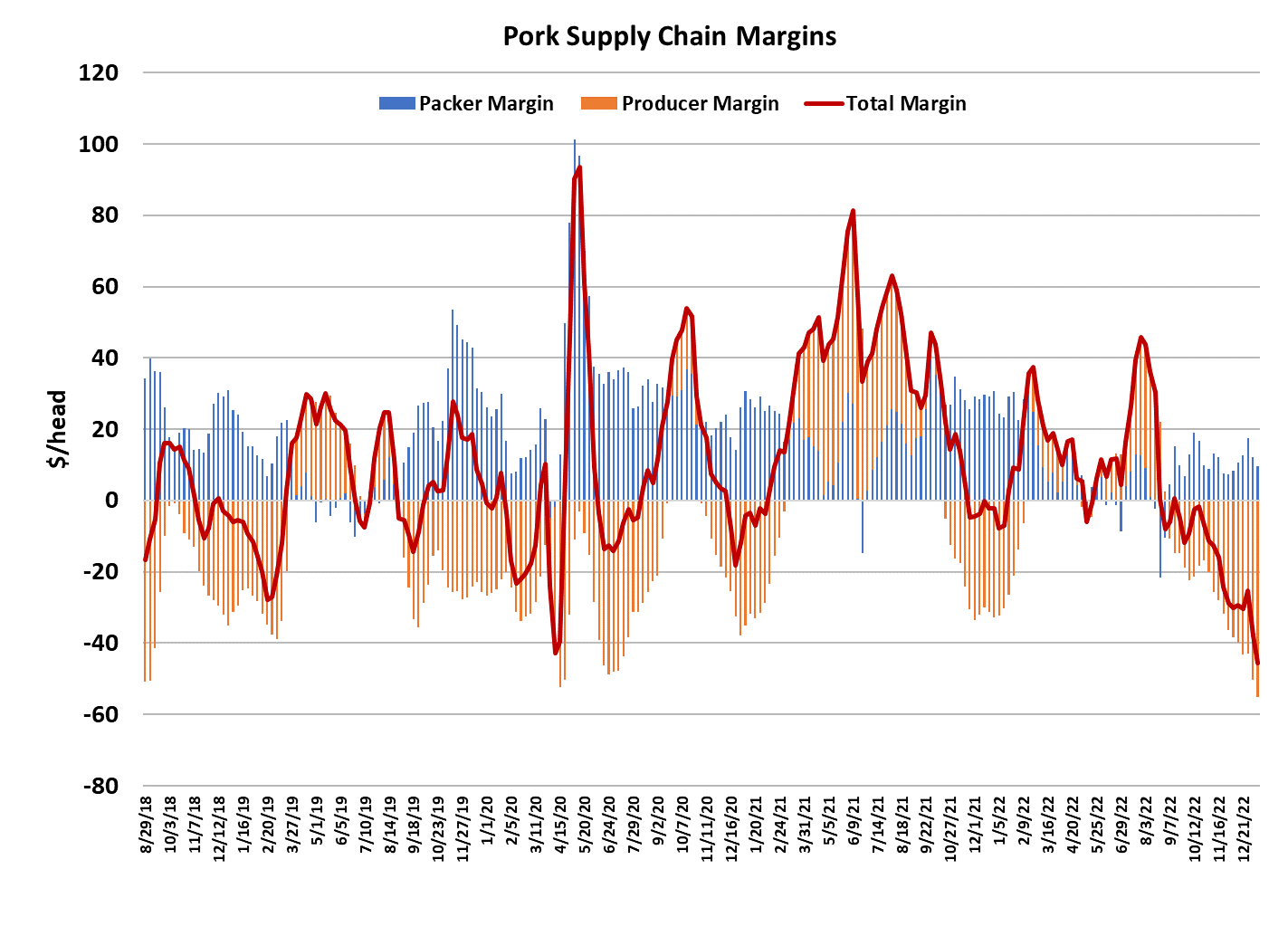

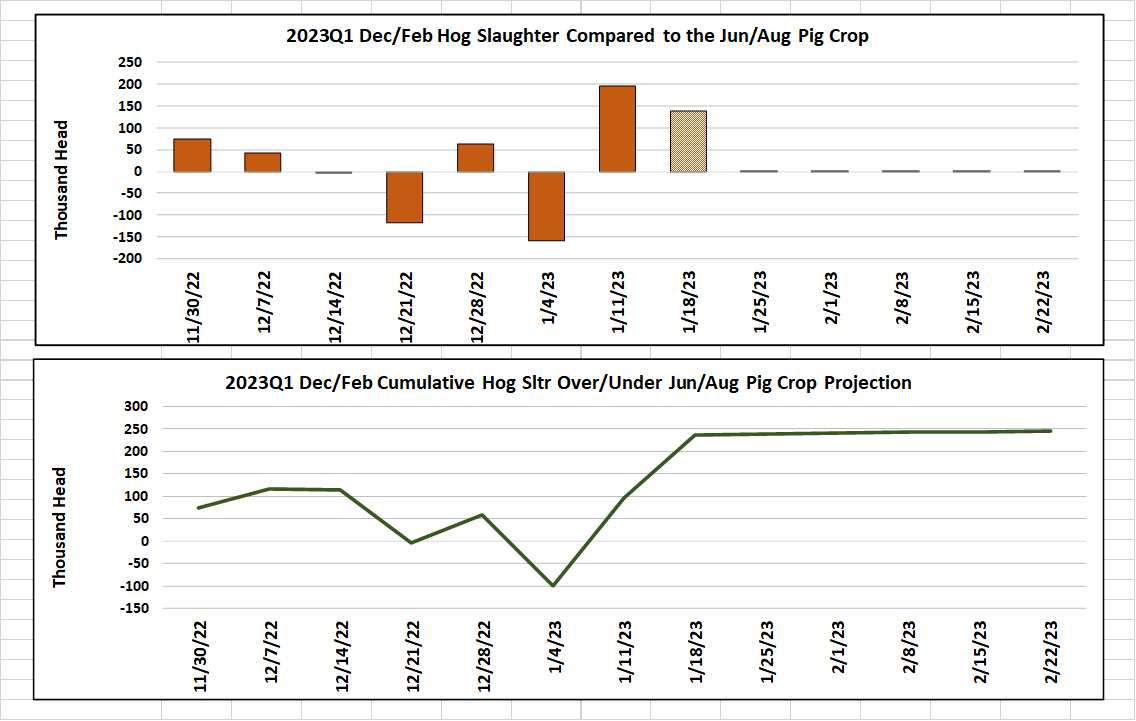

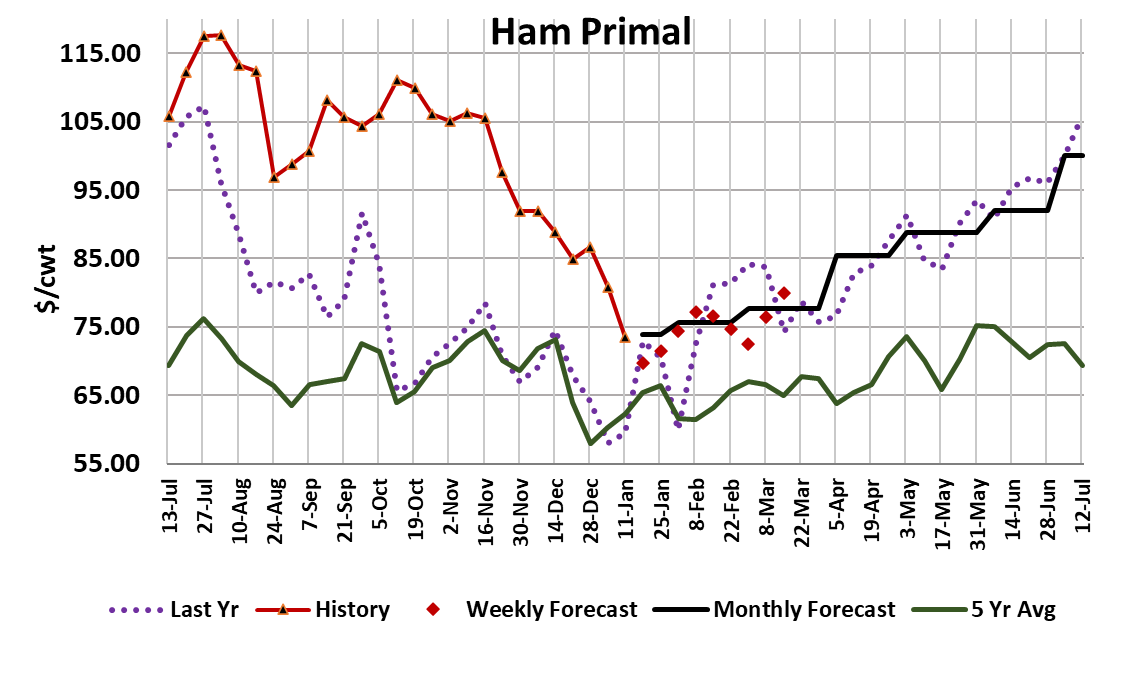

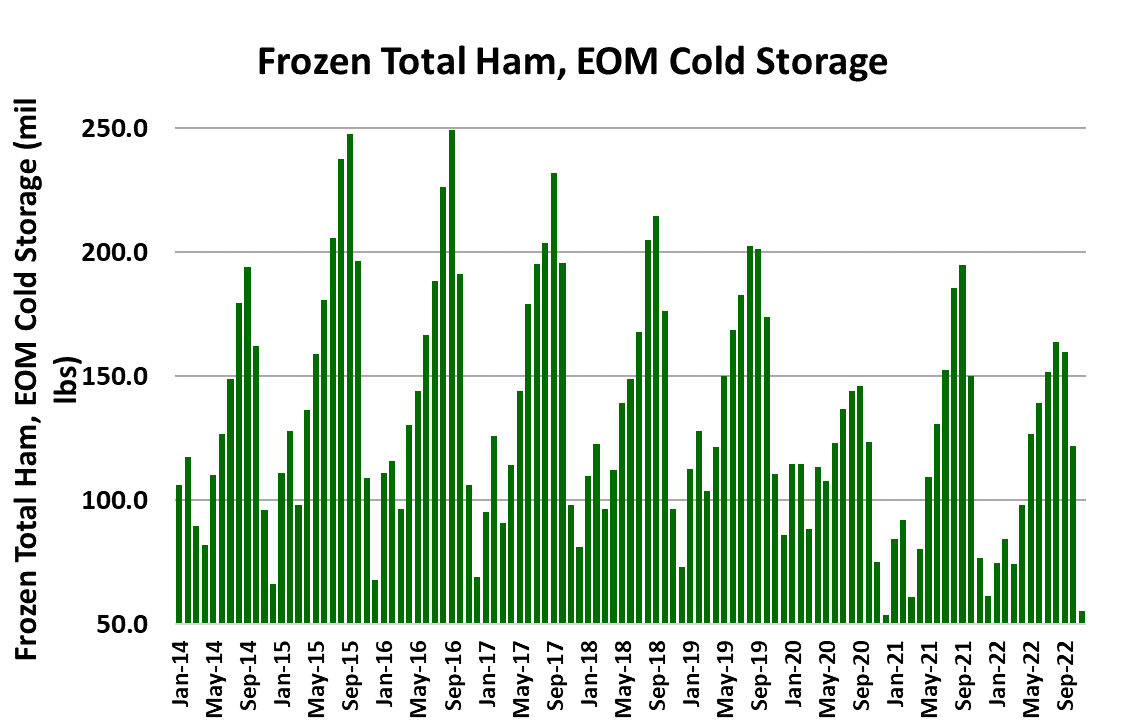

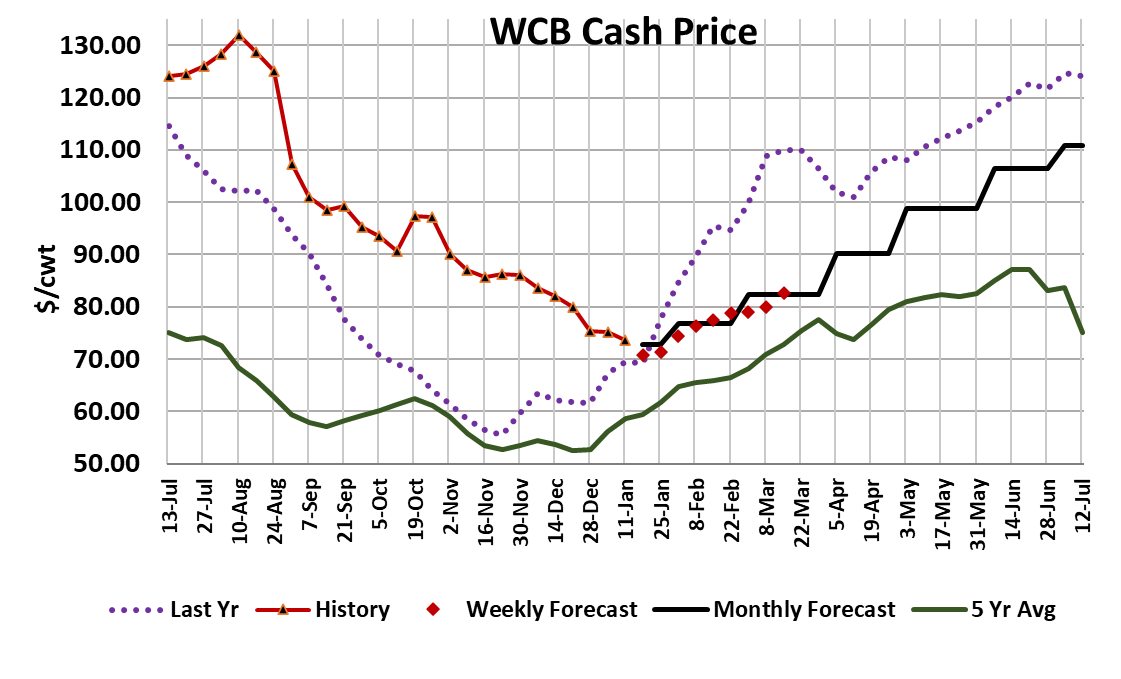

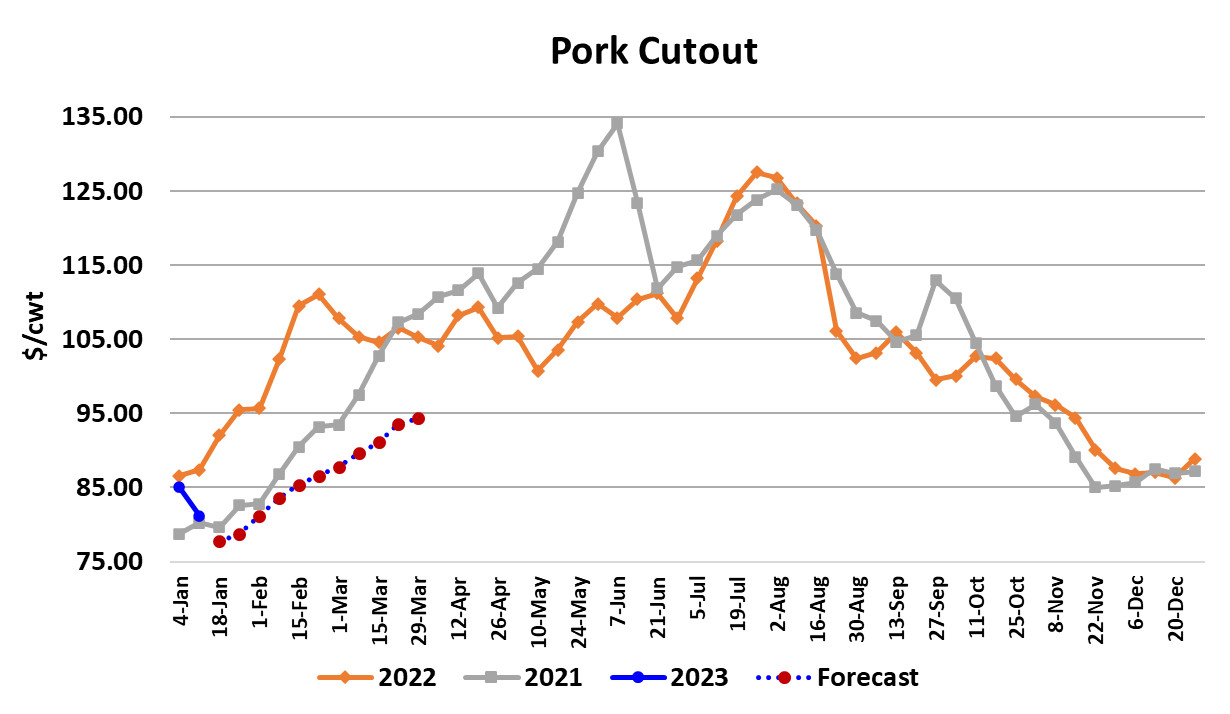

Packers ramped things up in a big way this week, producing a huge kill that caused the cutout to struggle. On a weekly average basis, the cutout was down $3.89/cwt. to $81.15. The cutout has now lost almost $8/cwt. over the first two weeks of January. Cash hogs came under pressure as well, with the WCB negotiated price dropping $1.58/cwt. on a weekly average basis. Since the cutout fell much more than hog prices, packer margins were compressed back down to $8.60/head. That is about half of what margins were in the last week of December. The moral of that story is light kills help margins. If that is the case, then packer margins are in trouble for the next couple of weeks because the kill has been huge. This week’s total was 2.67 million head, which was bigger than any kill we saw during 2022, even in November. What’s more, packers seem to be gearing up to kill close to 2.6 million head next week. Suddenly there is a lot of pork that needs a home and the only way to accomplish that is through lower prices. This week the retail cuts came under pressure more that what we’ve seen recently. Hams also continued to loose value. Fortunately, packers did seem to move good volumes at the lower prices, but they may need to extend that strategy into next week in order to keep inventories from building. It seems like it may be very difficult to keep the cutout from moving into the upper $70s during this big production period. It doesn’t help matters that simultaneously pork demand seems to have hit an air pocket. The combined margin looks awful. Production will eventually taper down, but this week’s slaughter was well above what the Jun/Aug pig crop implied. If we assume that I’m close on next week’s kill, that would also be over the pig crop implied and put the cumulative over-kill for this quarter (Dec/Feb) at about +250k. I realize that the holidays can do goofy things to production schedules so I’m not ready to definitively say the USDA under-estimated the summer pig crop, but the evidence is starting to point in that direction. It might not be a big miss, but we might want to get used to the idea that kills are going to come in a little larger than expected over the next few weeks. Looking back on the data for the Jun/Aug period, it does look like the number of sows farrowing as a percentage of the breeding stock was the lowest it has been in the last 19 years for that quarter, so maybe they under-estimated how many sows farrowed this summer. The pigs per litter number in that quarter showed no YOY gain, which is somewhat unusual also. Maybe that was under-estimated. Whatever the cause, if there are more hogs out there than advertised, we should probably lower price expectations. That is exactly what I did this week as I went through the price forecasts. The bigger reductions were applied to the near-term price forecasts, but I even extended some more moderate downward adjustments into summer. The past two summers have been characterized by rip-roaring pork demand and I think that has created a tendency to expect $120+ lean hog indexes in summer, but as we are seeing right now, this year is way different from last year on the demand side. Triple digits are still possible for the LHI in summer, but maybe just barely. Perhaps tops will come in the $105-110 range. The YOY decline in the cutouts should be larger than what we see in the LHI over the summer as margins are likely to be tighter than they have been due to packers chasing an ever shrinking hog supply. To add to the supply side woes, carcass weights have been moving higher lately. USDA reported federally-inspected (FI) weights up three pounds for the last week of December. Some of that was probably a re-bound from lower weights in the week of the cold snap before Christmas. Still, when we combine that with the week-over-week gains that have been reported in the more timely 201 report, it seem to reflect that producers may be falling behind in their marketings some. The DTDS weights have moved higher recently and are projected to surge as the FI data comes in for early January. Of course, the big kill this week and the big one coming next week should help to clear out any backlogged hogs that may exist. Normally cash hog prices turn higher in early December, but this year they are still on the way down. Perhaps these big kills will be what causes them to bottom. Another thing that is raising concern for me is the continued softness in the ham market. The attached chart shows how the ham primal has moved from a strong premium over the five-year average to the point where now it is very close to the five-year average. Those hams have provided a lot of benefit to the cutout over the past six months and if that phenomenon is over, then there is another reason to adjust price expectations lower. I can understand why bellies are remaining soft because freezer stocks there are large, but hams in cold storage are very tight. Rumors had it that Mexico was going to be a big buyer of US hams in January, but so far we haven’t seen much evidence of that. Futures traders have been more generous with this market than I would have been. Feb is still carrying a $5 premium to a rapidly declining LHI. I don’t think that futures necessarily should trade below the index, but it seems like there is enough uncertainty about how long this downcycle will last that the futures ought to move closer to the index and stick close until the uncertainty is cleared up. At some point, the cutout and hog prices will turn higher, but it isn’t a given that it will happen next week, or even the week after, so by the time prices do turn upward, the runway might be quite short for Feb. Next week, watch to see how the retail items handle continued big production and keep an eye on the hams for any sign that buyer interest is improving.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}