Pork Wrap January 12

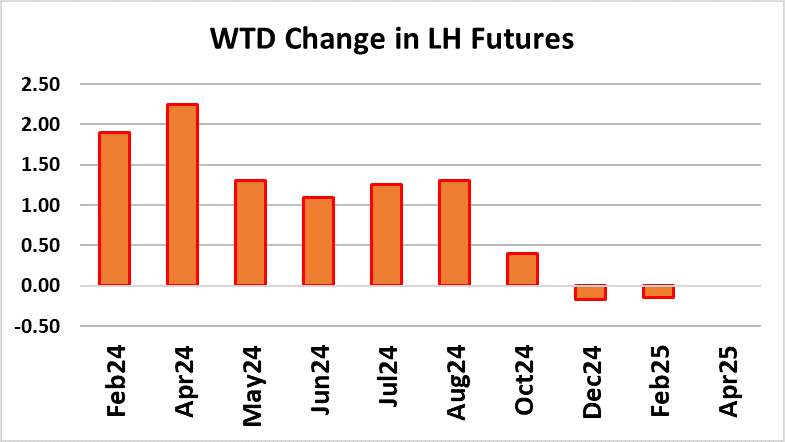

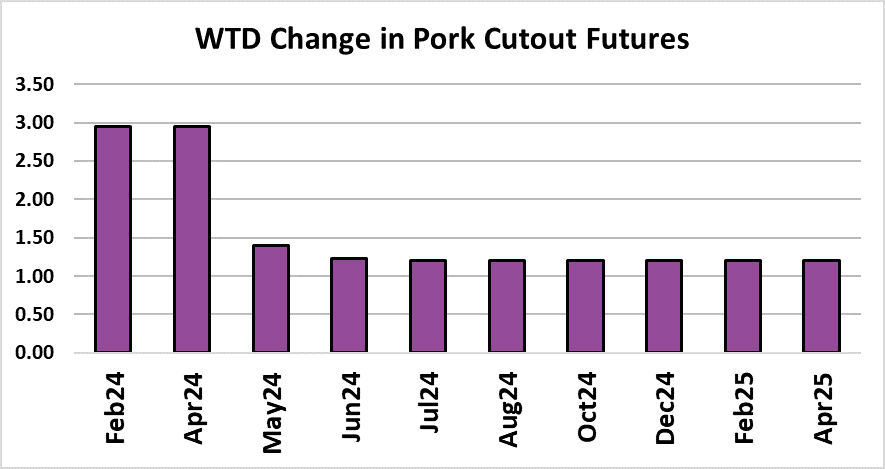

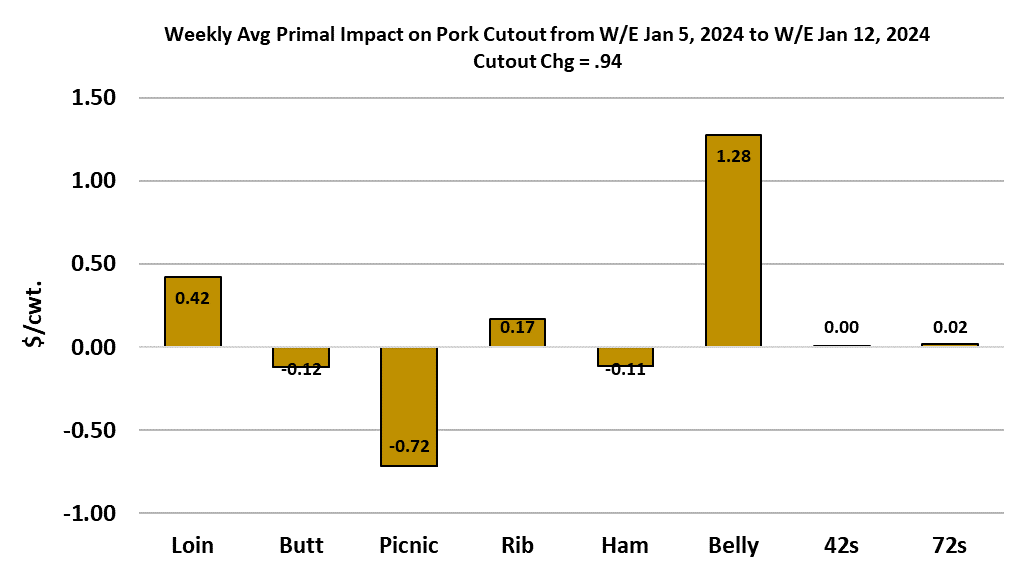

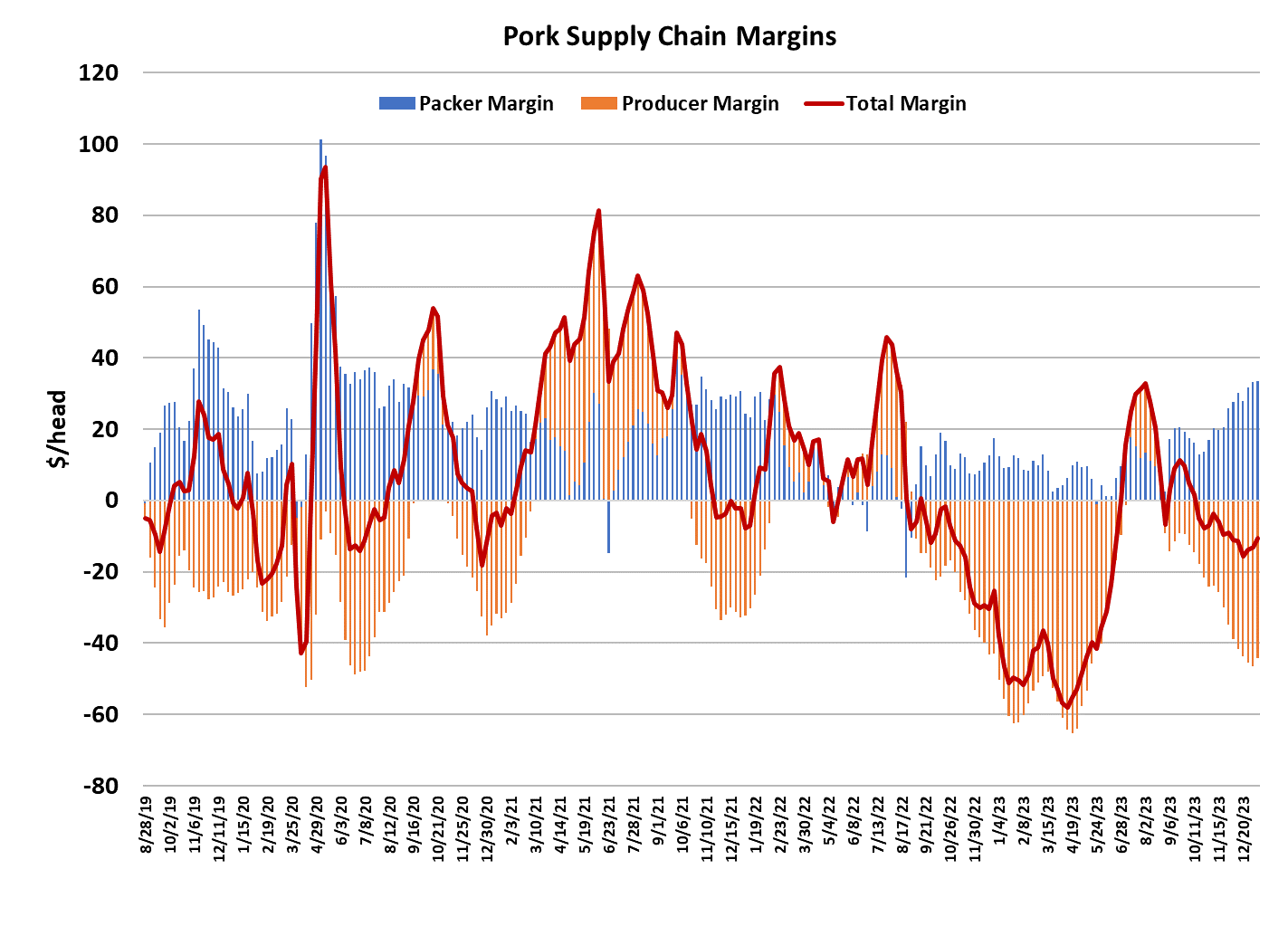

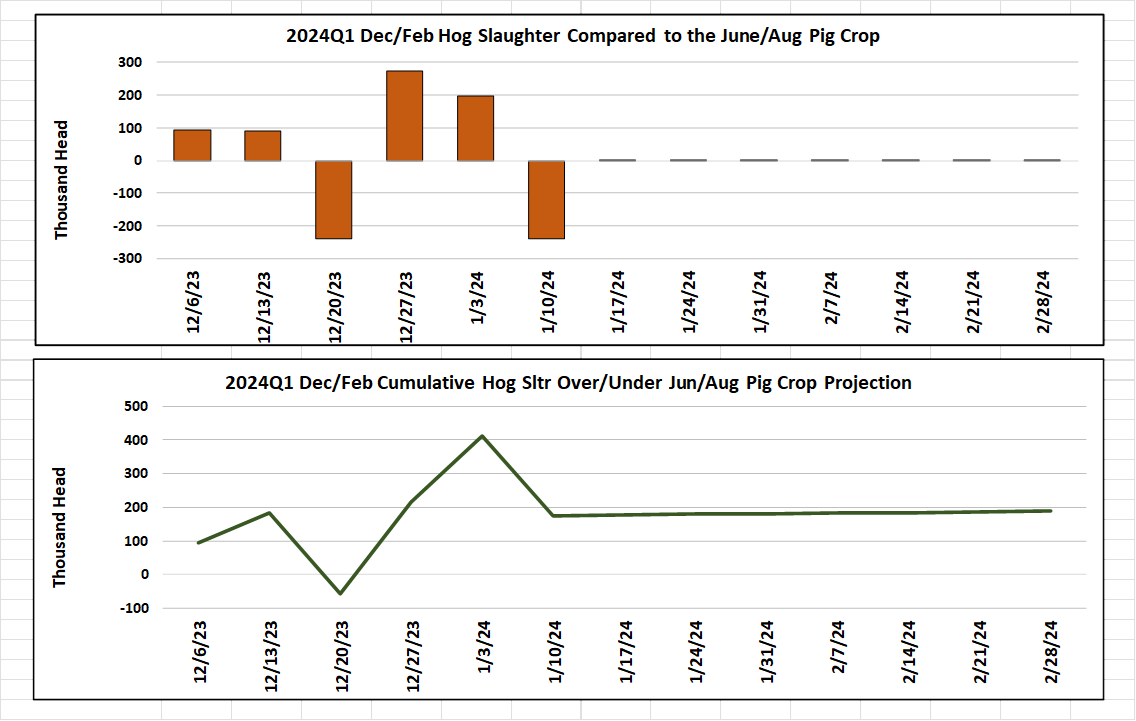

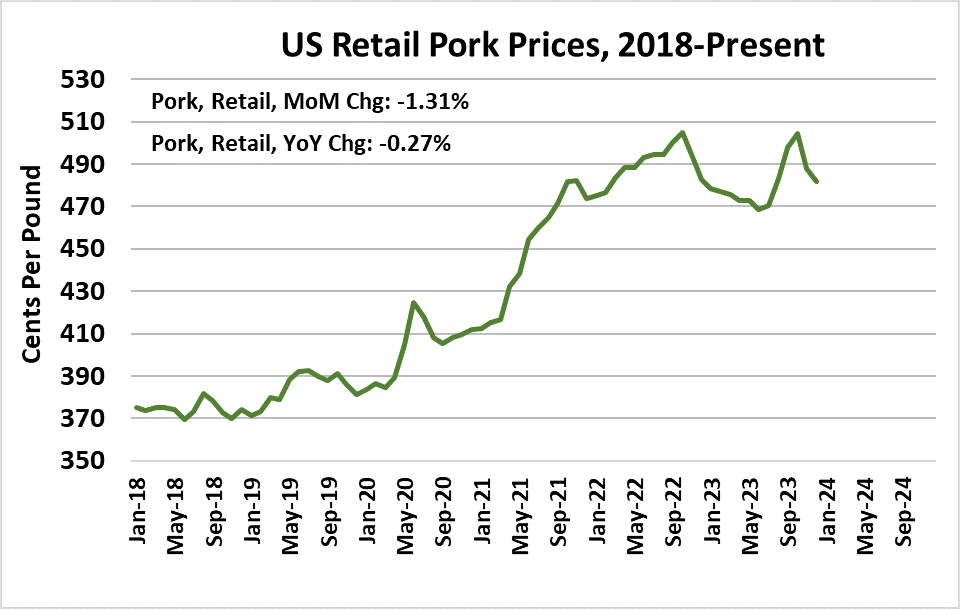

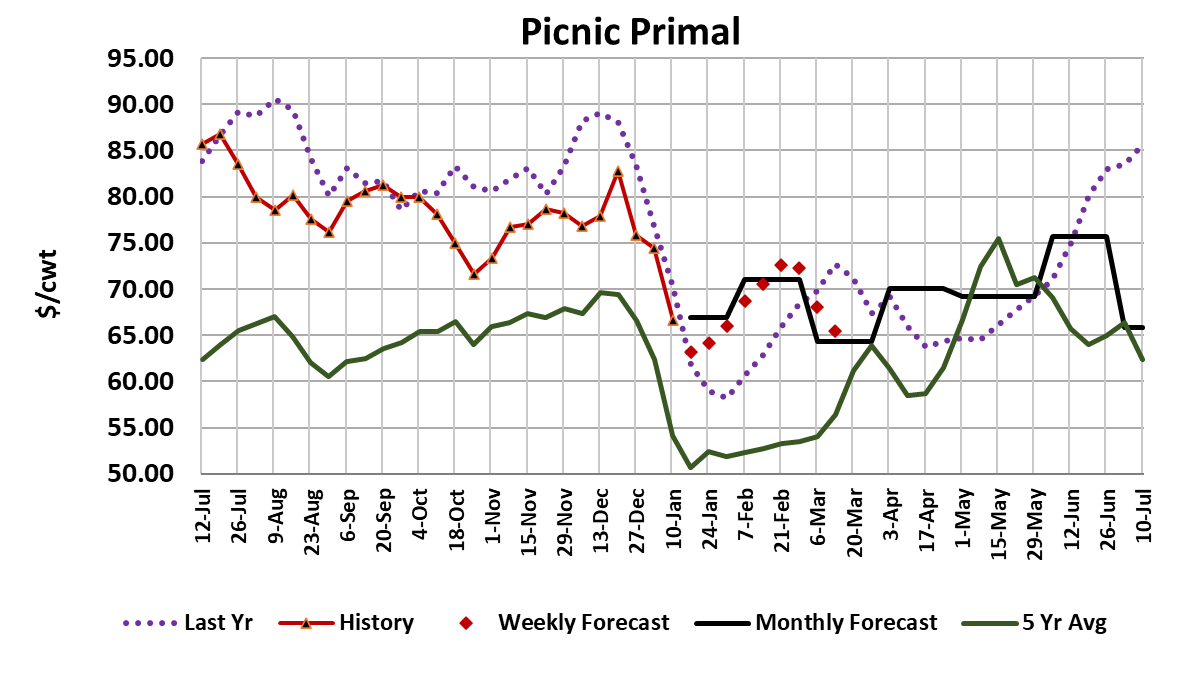

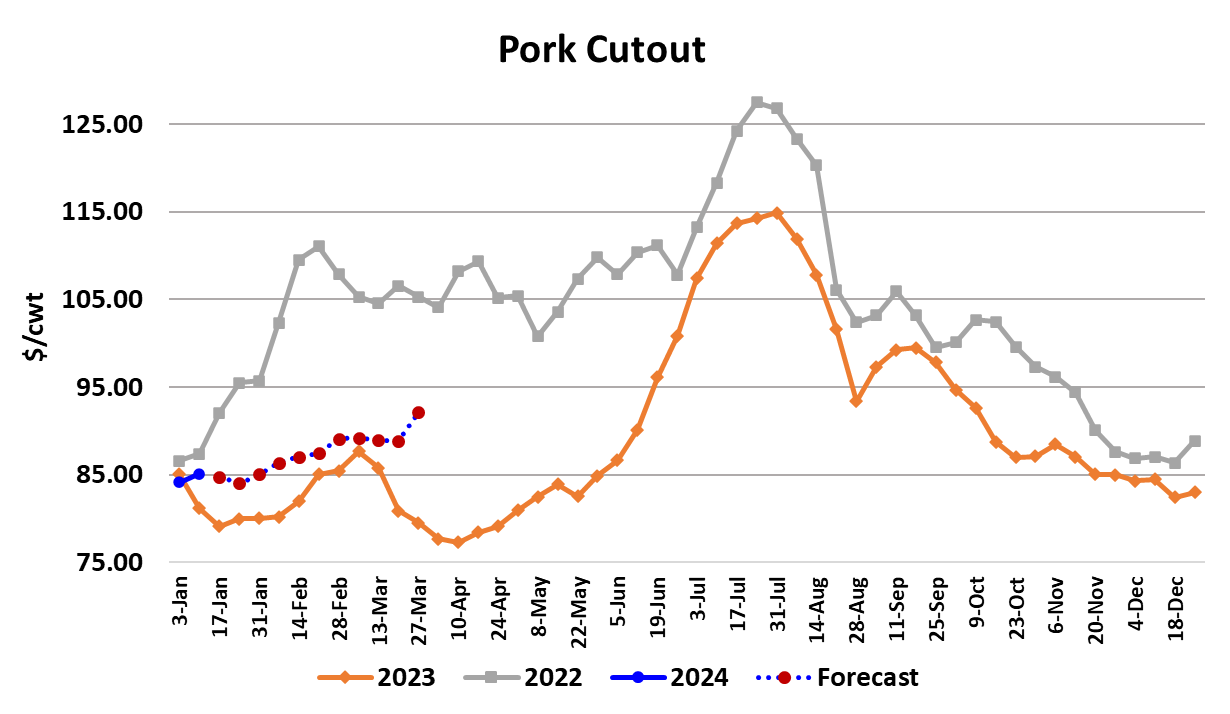

Last week, I noted that belly prices had firmed, but I wanted to see how they held up under a full production week. Unfortunately, that hasn’t yet been tested because this week was another short kill week due to weather issues. Snow across the Midwest and an impending polar vortex had packers cutting slaughter schedules as travel was difficult for hogs and humans alike. This week’s slaughter only tallied 2.28 million head, which was 100k less than the holiday week that we just came through. So, we have essentially had three short kills in a row now and there is some risk that next week’s kill will also be curtailed a bit by the weather. With production suddenly falling well below expectations, one might expect pork buyers to scramble to procure product and drive up prices in the process. There may have been a little of that in certain items, but by and large the pork market took it in stride. The cutout advanced $0.94/cwt. on a weekly average basis to $85.09. The belly primal provided the most support, while the picnic primal was the biggest drag on the cutout. The fact that the cutout could only muster a gain of less than a dollar in a week where production was sharply below normal doesn’t speak very highly about pork demand. Of course, we have known for some time that pork demand was struggling and I guess this event just provides further confirmation of that. Negotiated hog prices were almost unchanged on the week and something seems a little fishy about that. After three short kill weeks, the NDD negotiated price is only about $2 below the level seen before the holidays. Surely there must be some hogs backing up in the pipeline and I would expect that to manifest in lower negotiated prices, but that didn’t happen this week. Perhaps packers are comfortable enough with their $30+ margins that they don’t feel the need to put additional financial pressure on producers, who are already deep underwater margin-wise. The combined margin has inched a little higher over the past few weeks, primarily as a result of packer margins expanding a little while producer margins were mostly flat. If the negotiated price is carving out a bottom here in early January, then we might reasonably expect the LHI to start slowly working higher alongside the gains in the cutout. The fundamental forecast has the cutout holding in the $84-86 area for a couple of more weeks and then slowly climbing to $90 by late February. If that scenario plays out, then the LHI should be around $72 at Feb expiration, which is very close to where it settled this week. However, a lot could go wrong that would derail that plan, most notably if pork demand softens further. That is what happened last year in late January and set the stage for a weaker-than-expected expiration on the Feb futures. One concerning aspect in this week’s pork market was some softening of ham prices. It isn’t yet clear what is driving the lower prices, but it was a bit surprising to see that coming on the heels of to light production weeks. If the hams stagnate or continue to work lower, then it is going to be very difficult to achieve the near-term fundamental forecast. The retail items still look pretty shaky and picnics are clearly in a seasonal downdraft, so that doesn’t help either. Further, all of those hogs that didn’t get slaughtered this week won’t disappear and thus will eventually cause some big production increases down the road when they come to market. With demand obviously still very weak, that creates some additional downside price risk. Barrow and gilt carcass weights jumped three pounds in the most recent FI data release. That data was for the week that included Christmas, so some increase was expected, but three pounds was a surprise. That may be the seasonal top in weights and from here they likely move sideways for 2-3 months. As wholesale pork prices have eased over the past few months, retailers have become more comfortable with lowering the prices that consumers see. USDA reported the December retail price down 1.3% from November and it now sits just a hair under last year’s level. With hog productivity soaring and more hogs on the ground than expected, the industry really needs retailers to rapidly lower prices in order to help spur consumption. The drop in December was a step in the right direction, but further downward adjustments are needed. Overall, the biggest change this week came from the weather. Hog supplies are still ample, and demand is still very weak. Prices might get a short-term boost from the weather-related slaughter disruptions, but once production returns to normal and packers get busy trying to harvest all of the delayed hogs, then problems with demand will come back into focus. Next week, watch the daily kills for further slaughter reductions and expect a huge Saturday kill next week as packers try to get caught up.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}