Pork Wrap January 5

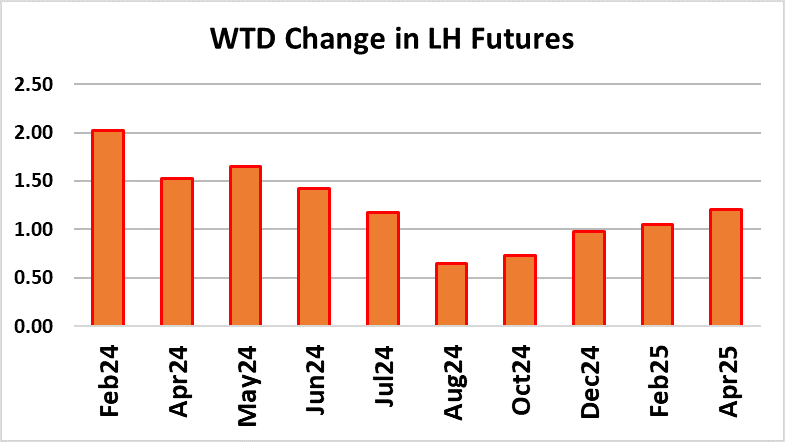

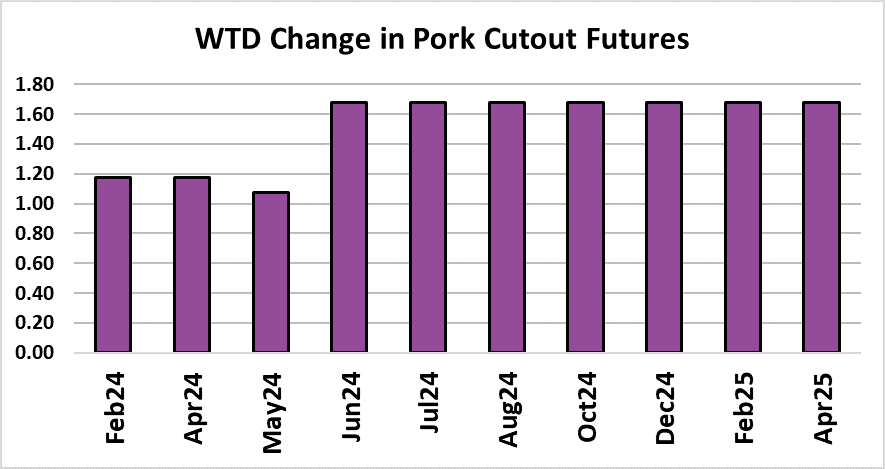

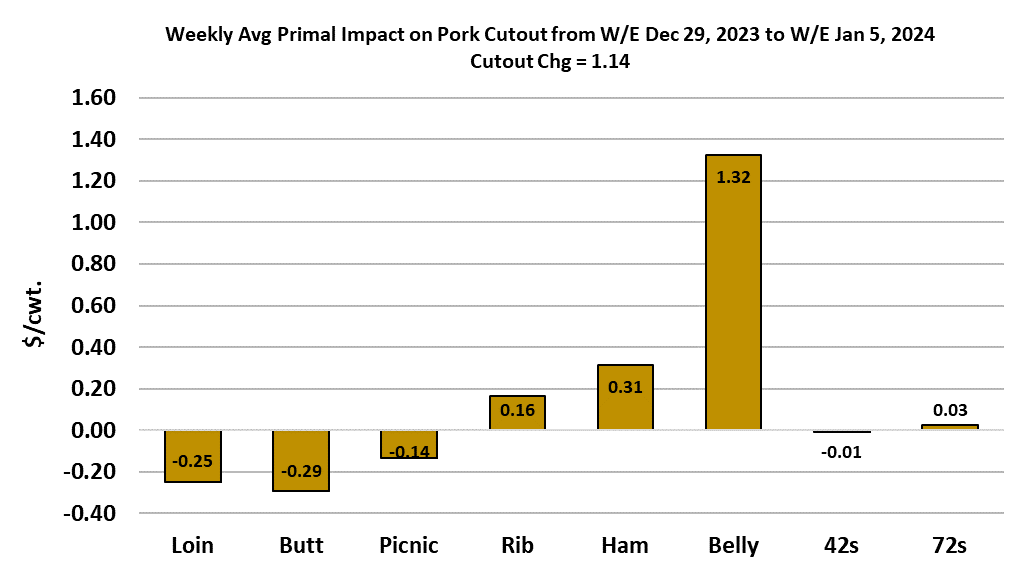

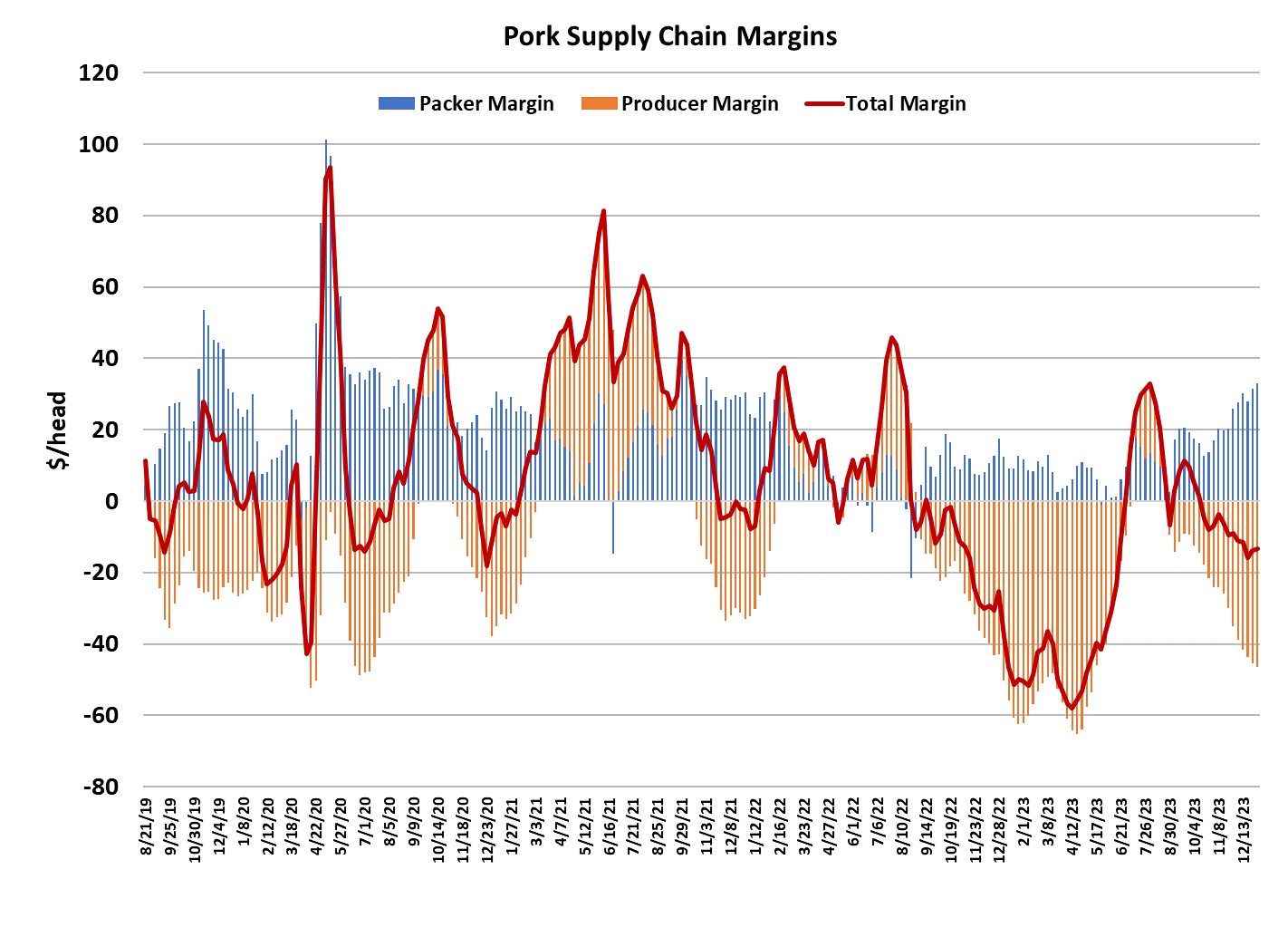

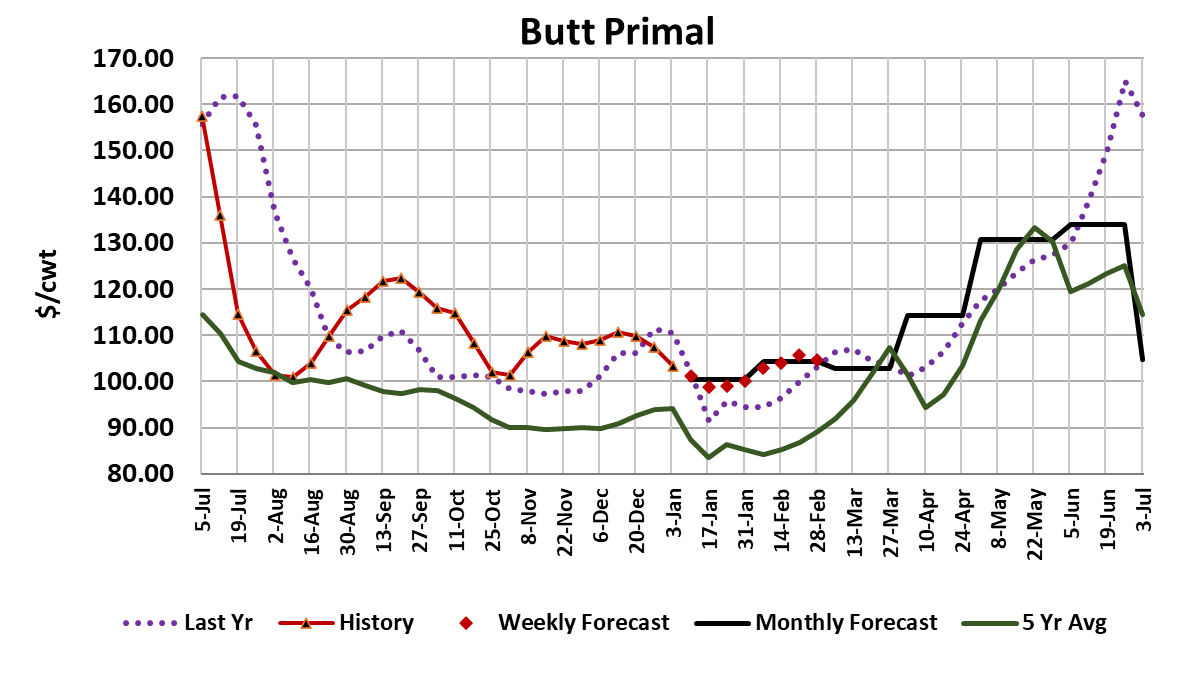

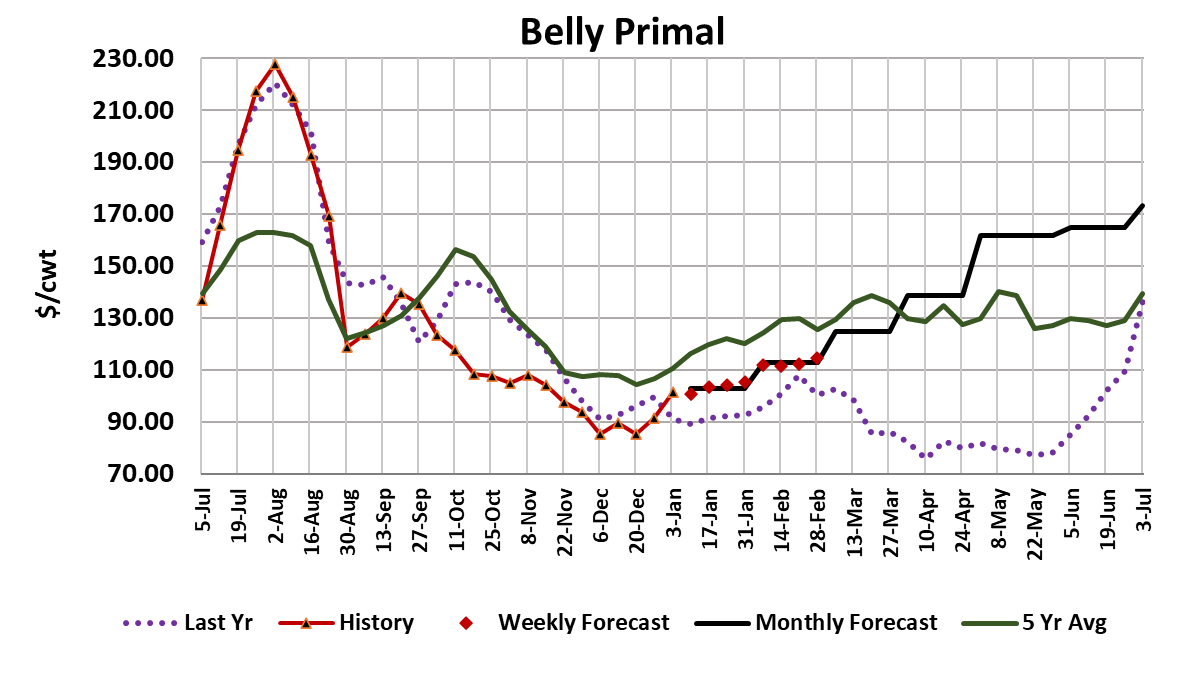

Lean hog futures went on a rollercoaster ride this week, as the nearby Feb contract inexplicably sold off hard on Tuesday, spent Wednesday ruminating on that move, then shot limit up on Thursday, followed by additional gains on Friday. After all was said and done, Feb added a little over $2 on the week. The big drop on Tuesday made little sense because it pushed the futures below the cash index, which is very atypical at this time of year. There wasn’t any significant news that would have justified such a big move, so I just have to chalk it up to traders finding it a little harder to read the fundamental tea leaves after two holiday weeks where the data flow is light and thus potentially misleading. Last year during New Year’s week, the Feb futures averaged $5.10 over the LHI, and it had been as much as $10 over the LHI during the last week of December. So, it was a big surprise to see traders take the Feb contract discount to cash in one big swoop on Tuesday. What made it even more surprising is that there were indications that the cutout was slowly improving during the last week of December, so the bias should have been to boost the futures coming out of New Year’s, not crater it. Perhaps it was computers run amok or technicians seeing something scary in past prices that drove the sell off, but the improving cutout didn’t go away and by Thursday traders realized their mistake and Feb gained the limit of $3.75 on the day. For the week, the cutout averaged $84.15, up $1.15 from the week before. The lion’s share of the gain was driven by the bellies, with a little help from the hams. However, it is difficult to know whether or not the rise in the cutout was simply a function of tight availability over the holiday weeks or true improvement in demand. We need to see how the cutout performs next week as production levels return to normal in order to answer that question. At least the Feb futures are now back at a more-normal $5 premium to the LHI, so perhaps they will be better behaved next week. This week produced a dichotomy in the cutout, with the retail cuts working mostly lower and the processing items gaining ground. To be honest, the softening in the retail items has me more concerned than the gains in the belly primal. Belly prices can swing around a lot, particularly when volume is light but the loins, butts and picnics are less inclined to move on a whim and so the fact that they declined during a short production week is a bit concerning. It is pretty common for processing plants to run reduced hours through the holidays and that lessens the need for fresh pork as an input. However, as the holidays draw to a close those plants often need to replenish inventory and that can lead to some temporary price gains like what we saw in the hams and bellies this week (trim too to some degree). I want to see the processing items build on that strength next week as slaughter returns to normal before I declare the bull run to be on. That said, the fundamental forecast doesn’t have the cutout moving much lower from here, perhaps a dollar or two at most, before it starts to increase heading into February. So, I see the downside price risk as limited from here, but the price gains, when they come, are likely to be slow and measured. Negotiated hog prices were down slightly this week with the WCB market dropping $0.53 on a weekly average basis to $45.52. Packer margins are in great shape at a little over $33/head and producer margins are miserable at a little under -$46/head. The combined margin has been mostly sideways for the past couple of weeks, so that isn’t indicating much in the way of improving demand. This week’s kill came in at 2.38 million head, up 160k from Christmas week. Packers will be putting in a huge Saturday kill tomorrow, estimated at 440k. Next week, look for slaughter to return to 2.65 million head or perhaps even a little higher. We are still over-killing the summer pig crop, even after USDA revised it upward by 370k in the most recent Hogs & Pigs report. That means kills could possibly run larger-than-expected for the next several weeks and possibly for months. Hog weights are nearing a top, but likely will move sideways from now until March, so there won’t be much supply-side relief coming from weights. Some hogs that should have been marketed during the holidays probably got pushed back into early January and could be driving next week’s strong projected kill. It is unlikely that cash hog prices will be able to advance under those conditions. As a result, I see packer margins holding above the $30/head level for at least another couple of weeks before hog availability starts to slowly pull back and thus creates some modest reductions in packer margins. That same slow, seasonal tightening in hog supplies should also help producer margins slowly climb higher, although there is little chance that they will go positive before April or May. In general however, the supply side continues to look pretty bearish, with all of these unanticipated hogs coming to market. The demand side could be improving, but we need to see more evidence of that next week under a full kill schedule to be sure. To that end, it will be important to keep an eye on those retail primals because if demand is softening there, it could negate any demand improvement that develops in the processing items.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}