Pork Wrap February 9

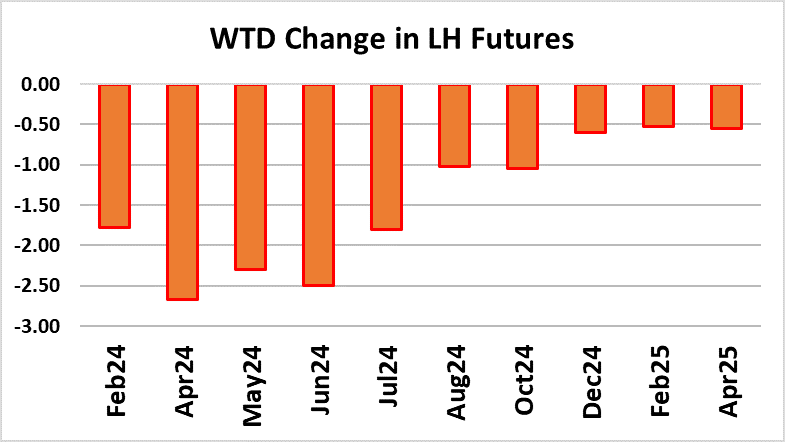

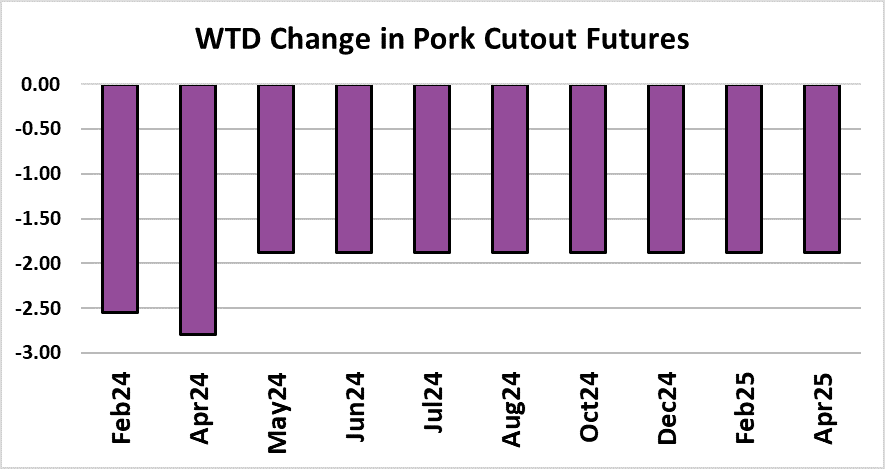

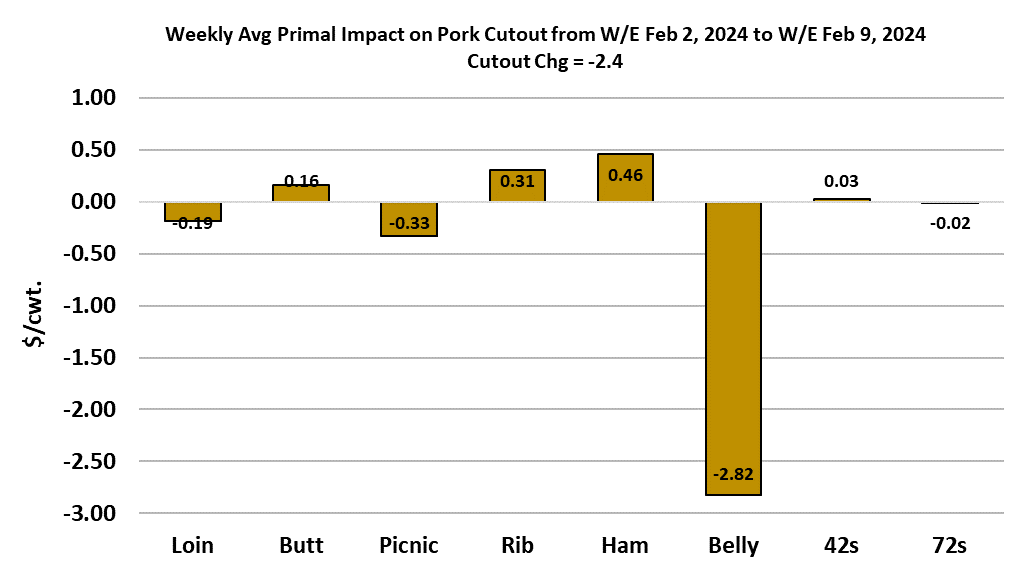

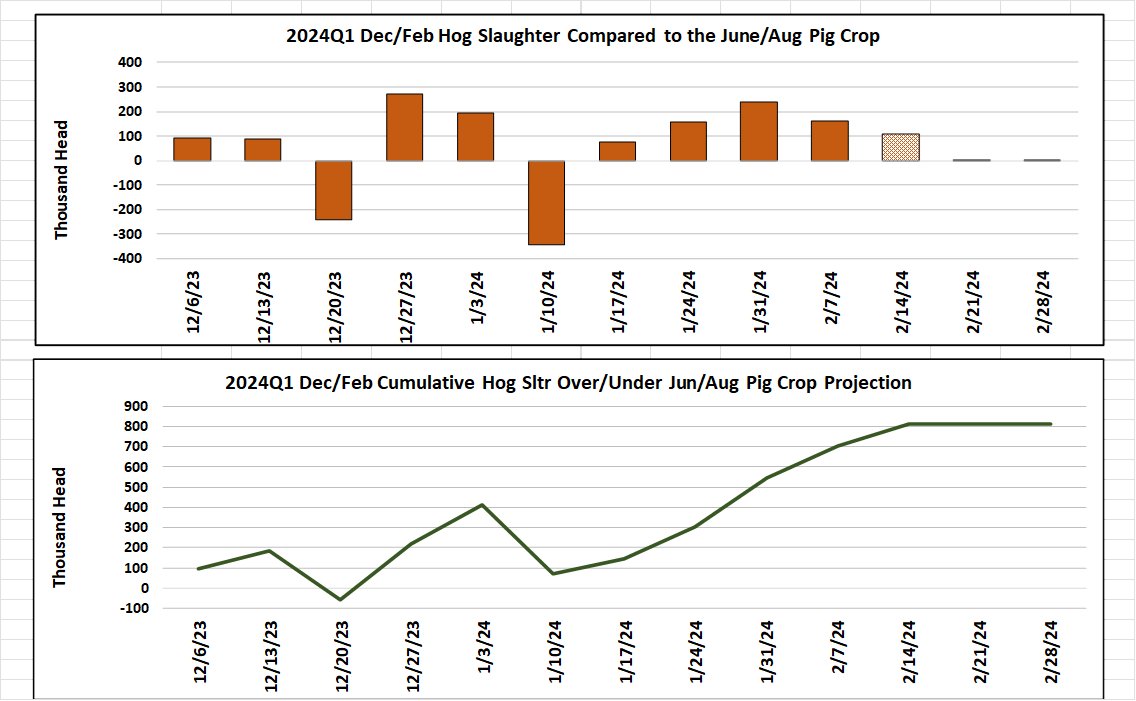

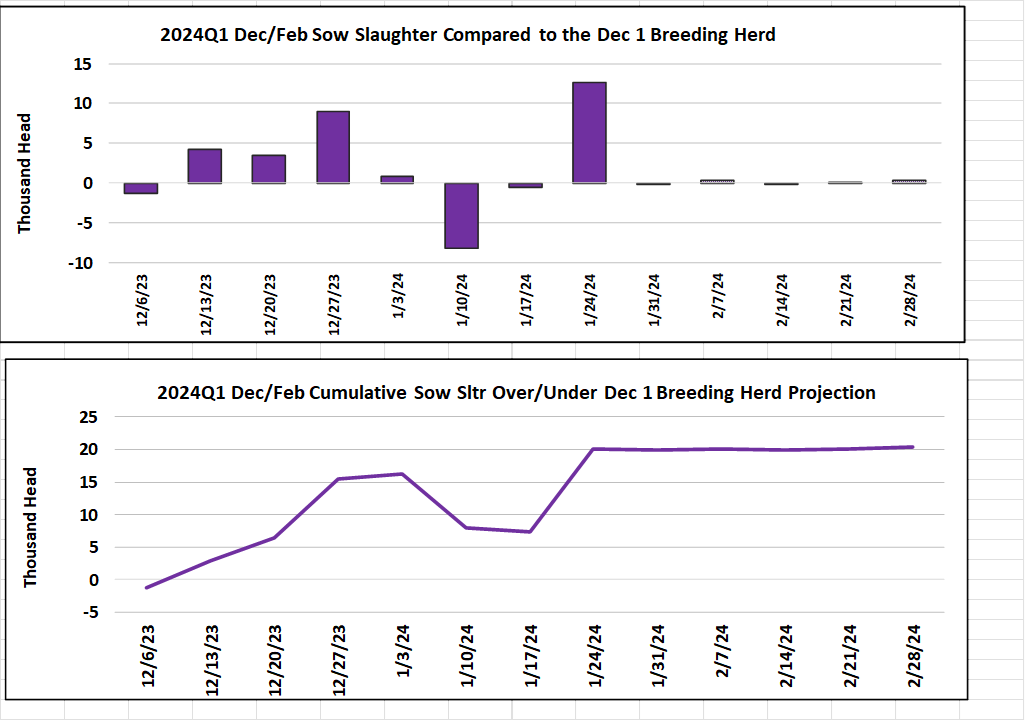

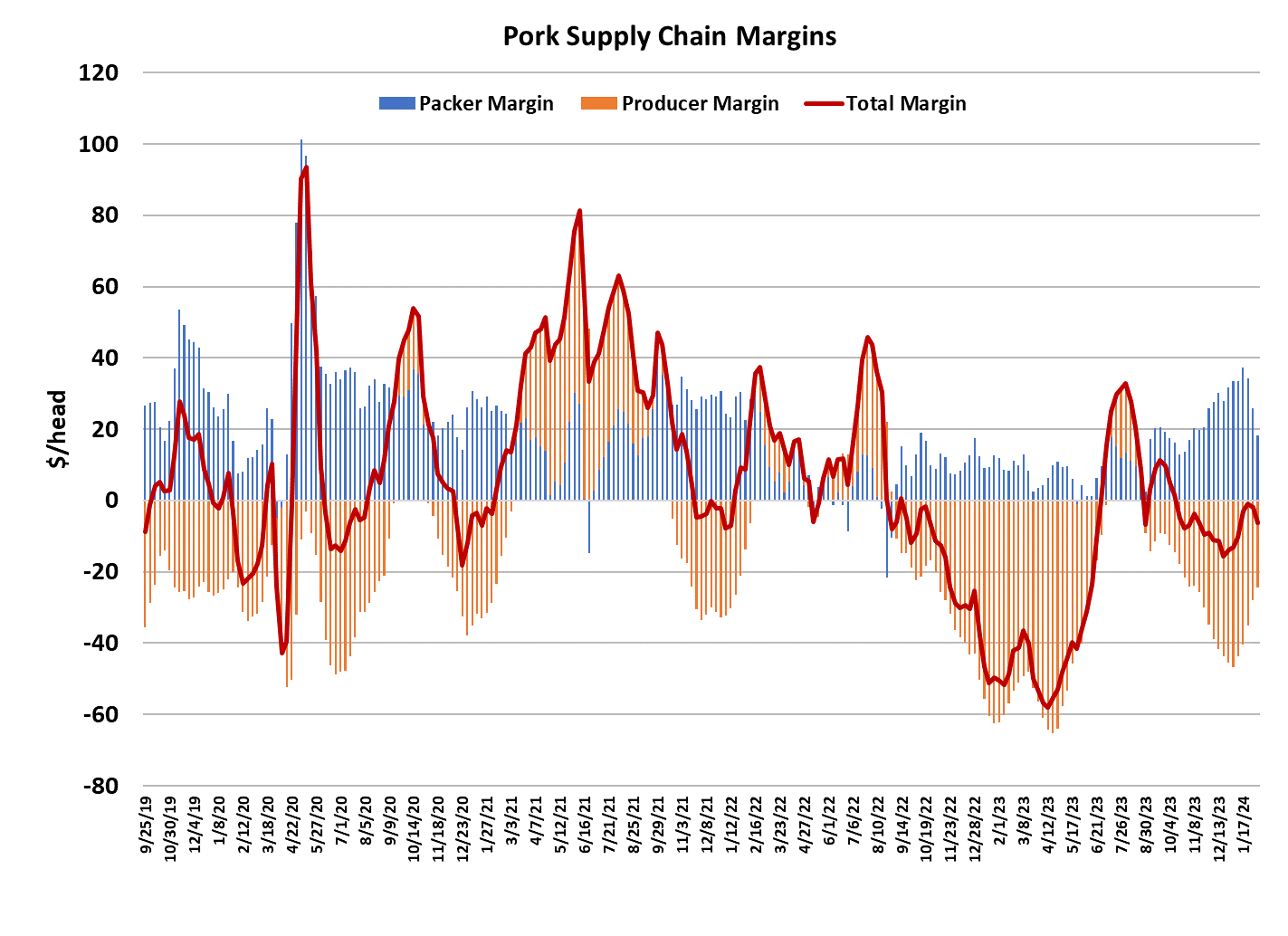

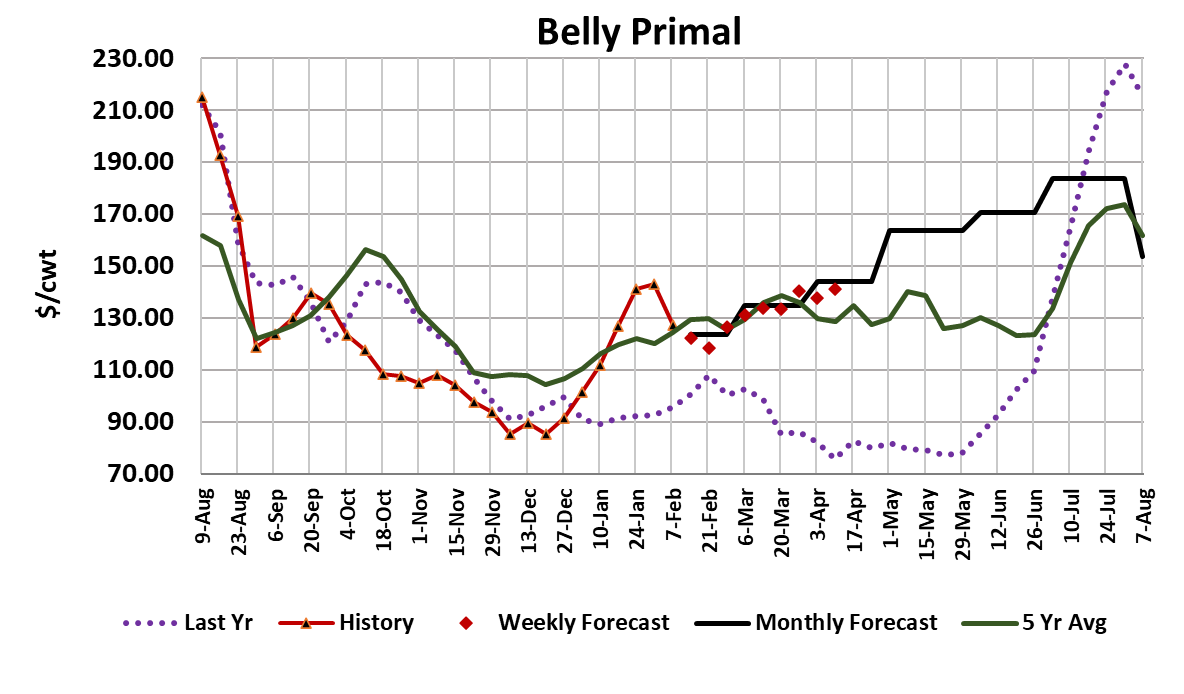

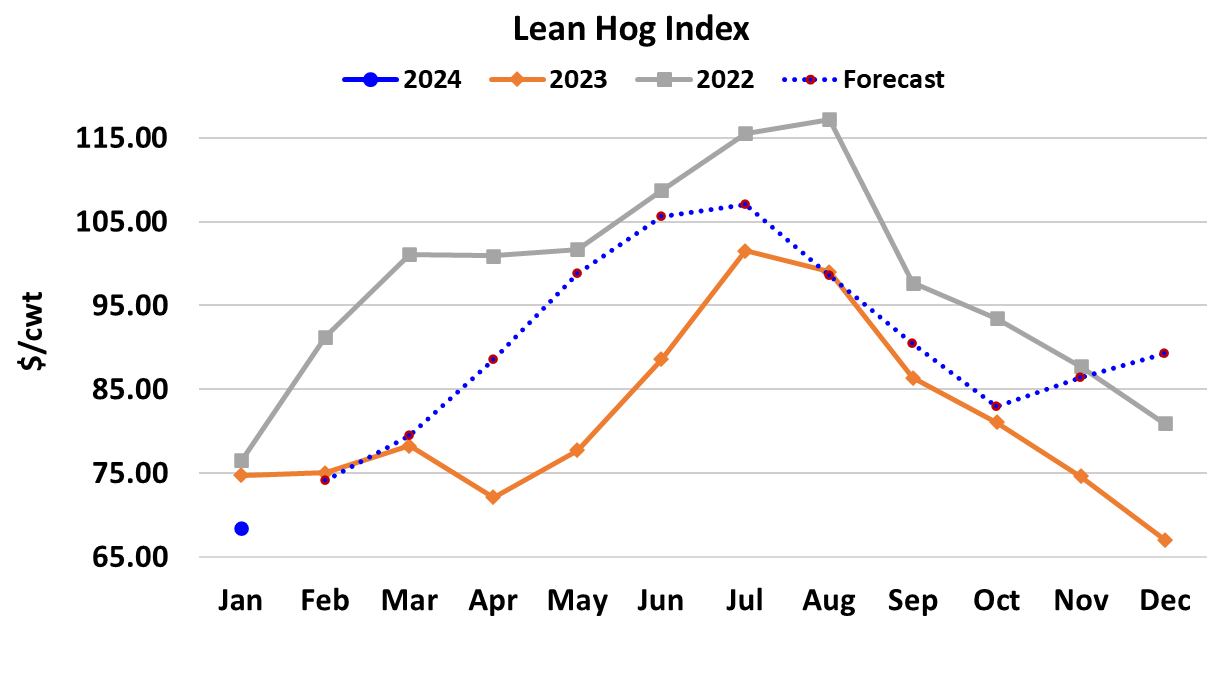

Bellies dragged the cutout lower again this week as the primal value fell almost $16/cwt. to average $127.09. That was a sharp reversal after six weeks of increases. Even though some other parts of the carcass posted gains, that wasn’t enough to keep the cutout from losing $2.40/cwt. on a weekly average basis. As a result, packer margins continued to compress, now estimated to be at $18/head and down $16 in just the last two weeks. The lower cutout flowed through to the LHI, causing it to stall in the $73-74 range with Feb expiration rapidly approaching. Traders are watching this belly weakness with interest because last year at this time it was an underperforming belly market that took the cutout and LHI down and caused the Apr contract to expire several dollars under where the Feb contract finished. At present, the Apr futures are carrying a nervous $7-8 premium to Feb. My guess is that the bellies will start to firm back up within a couple of weeks and we will end up seeing the Apr premium justified. It may actually be too small. The current fundamental forecast has the cutout in the high $90s in mid-April and the LHI in the high $80s. The ham market perked up a bit this week, with the primal adding about $2, and there could be further upside potential next week. I don’t expect the hams to go rocketing higher, but some strength there could offset softness in the belly and help to stabilize the cutout or perhaps even turn it upward again. One thing that is a bit concerning is the combined margin, which was lower again this week and now looks like it is beginning a new downcycle. The last upcycle was very short, so this downcycle is starting from a pretty low level and that is a bit ominous. Demand for the retail items seems to be holding up well, particularly given the strong production of late, so perhaps that will keep overall pork demand from softening too much in the short run. This week’s kill was reported at 2.62 million head, down 70k from the week before. That is a step in the right direction. Further, next week’s slaughter is likely to be below 2.6 million head, perhaps “only” 2.58 million. Finally, it looks like some relief is coming on the supply side. Even if next week’s slaughter is below 2.6 million, it will still likely be well above what the pig crop implied. It looks like slaughter for the Dec/Feb quarter is going to come in at least 800k over what the Jun/Aug pig crop implied, and we could very easily see at 1 million head surplus. USDA will likely need to revise that pig crop higher when it releases its next Hogs & Pigs report in March. It would probably be wise for market participants to assume that the Sep/Nov pig crop, which was reported down 0.2%, was also larger than advertised and should be prepared for slaughter to run stronger than expected in the upcoming March/May quarter. Hog producers need be more aggressive in liquidating breeding stock in order to better align production with pork demand at a price that will generate more margin in the supply chain. The FI sow slaughter data for the week of Jan 24, which was published this week, showed a big jump in sow slaughter and so far in the Dec/Feb quarter, the industry has killed about 20k more sows that would normally be expected given the size of the Dec 1 breeding herd. That is movement in the right direction, but the pace is too slow. Producer margins have been improving as hog prices have moved higher over the last few weeks, but they are still $25/head underwater and have little chance of turning a profit until late April or early May. USDA provided the international trade data for December this week and it was surprisingly strong. Exports were up 14.7% YOY in December and for 2023 as a whole, pork exports were 7.6% higher than in 2022. Strong export demand is encouraging, but it is unlikely to be strong enough to make 2024 a profitable year for producers. Packers, on the other hand, are likely to have another banner year as long as producers keep churning out large pig crops. Next week, it will be all eyes on the belly primal, because that seems to be what is driving the cutout currently. Pork buyers should start to prepare for declining pork production in the weeks ahead as kills subside and exports run strong.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}