Pork Wrap February 6

no pdf

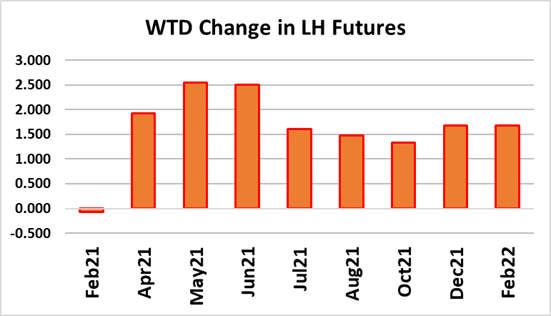

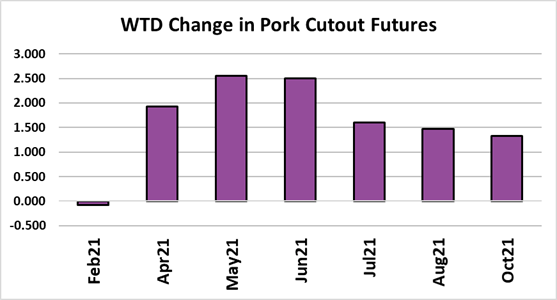

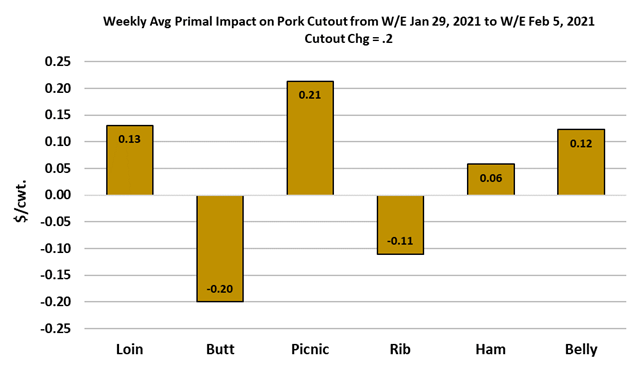

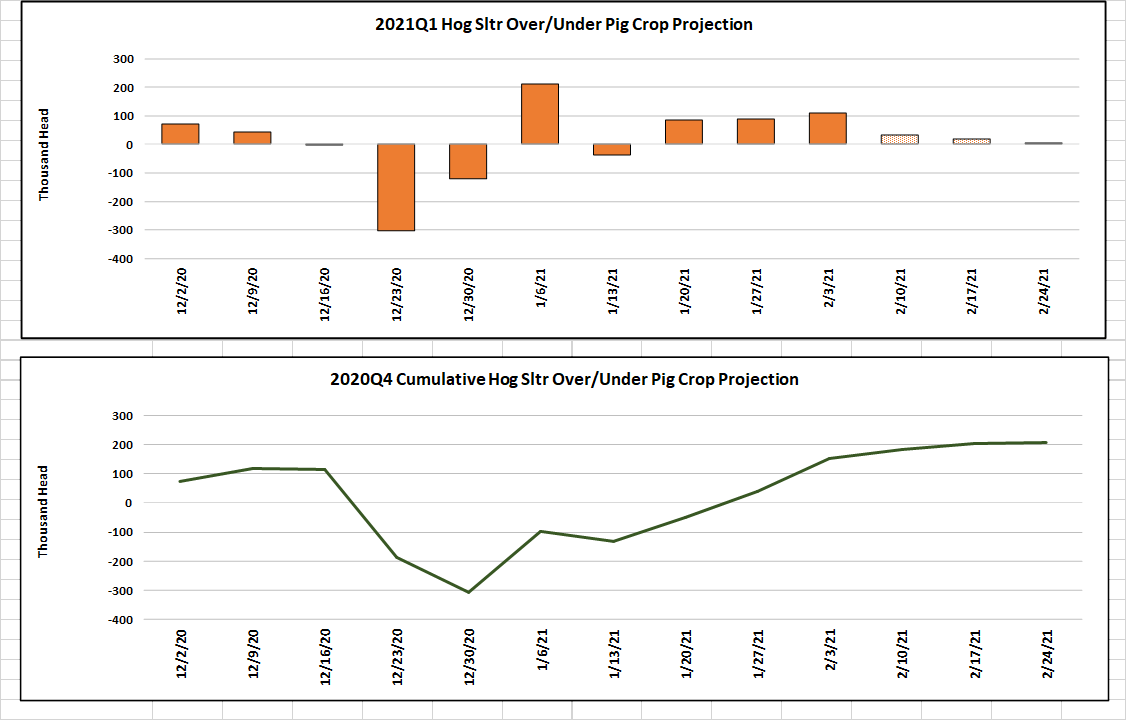

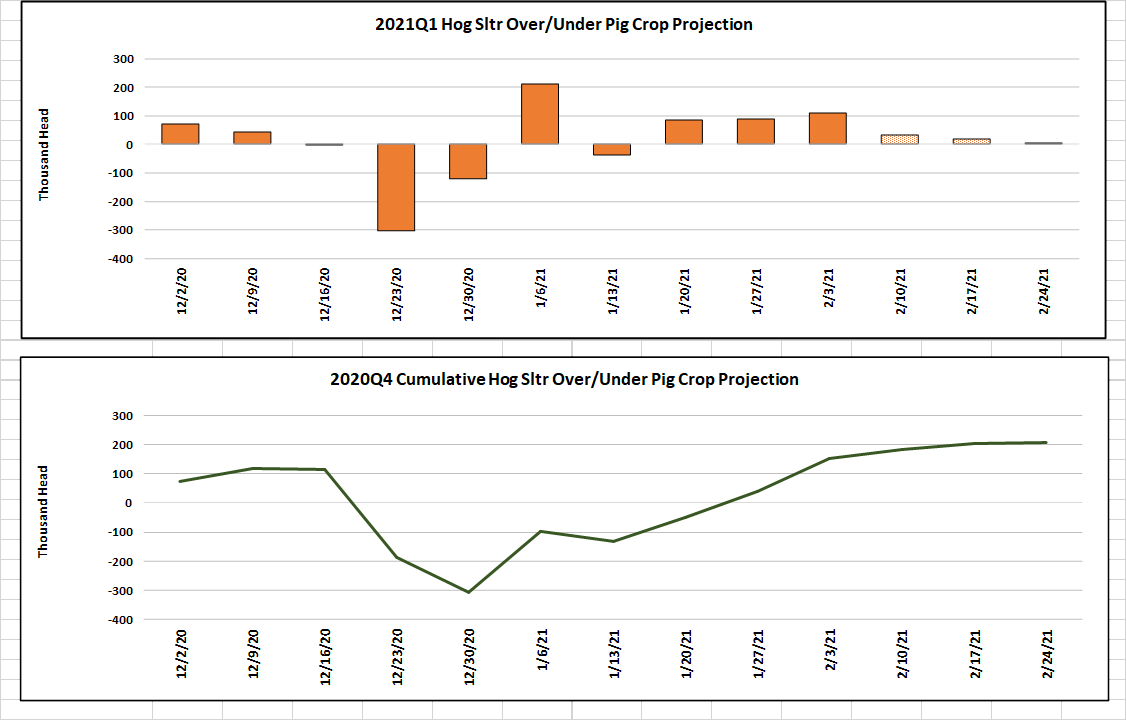

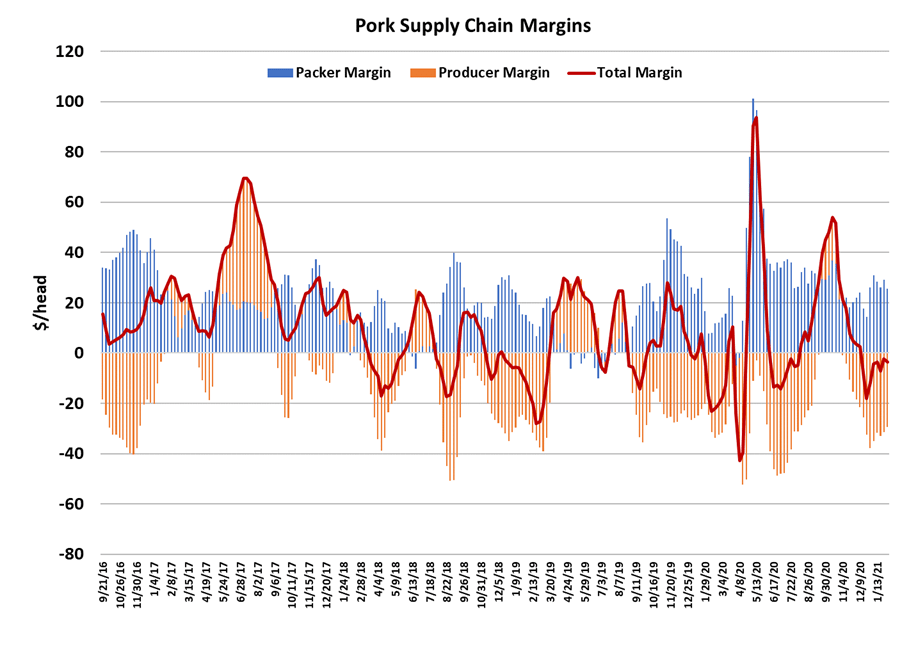

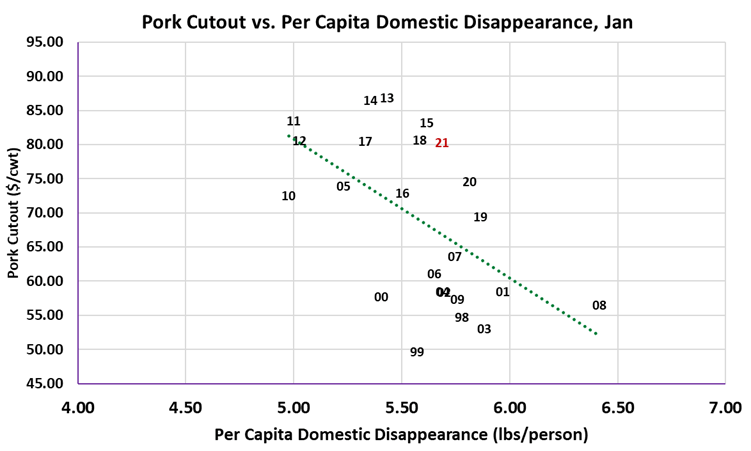

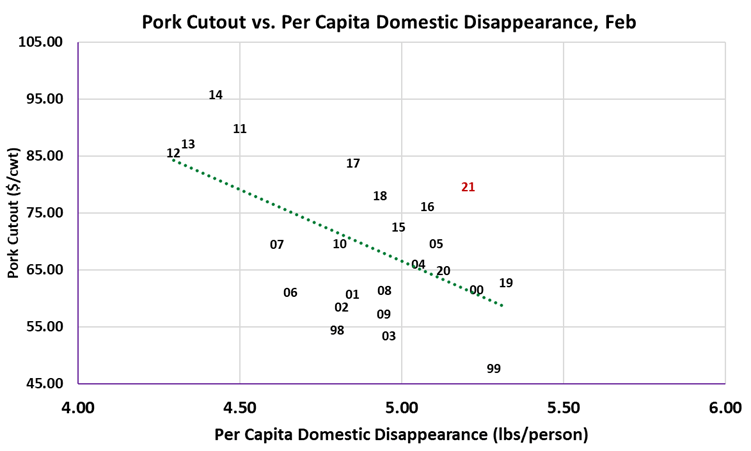

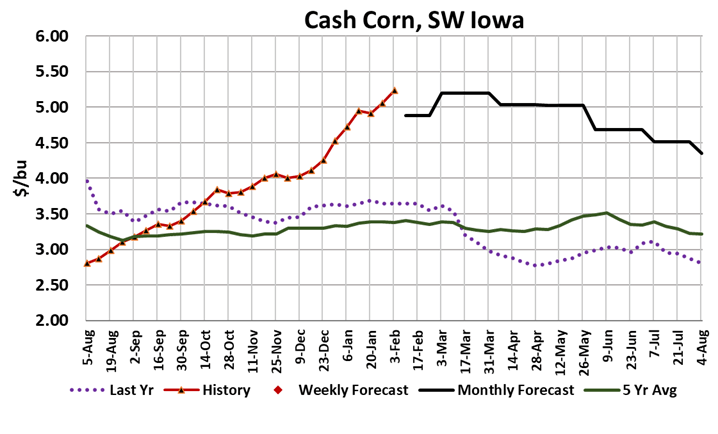

Last week I said that I was looking for the pork cutout to retreat modestly over the next two weeks. It didn¡¯t happen. On a weekly average basis, the cutout was up slightly ($0.20). What¡¯s more, the cutout actually improved as the week wore on, averaging $85 over Thursday and Friday. It is pretty clear that this rally still has some legs underneath it. Packers found themselves having to pay up in the negotiated markets this week too, with the NDD up almost $5 Friday-to-Friday. With a flat cutout and rising cash hog markets, packer margins compressed down to $25/hd from $29/hd the week before. Declining packer margins are a hallmark of February, so this is not too surprising. Even with the decline, this is the largest packer margins have ever been in the first week of February (2017 came close). So from a packer¡¯s perspective, everything is just fine in the markets right now. From a pork buyer¡¯s perspective however, it is painful to see the cutout $10-15 higher than its been in the past two years at this juncture. Likewise for independent hog producers who are still seeing cash market pricing below their breakevens when the pork market is so strong. Clearly, pork demand is very strong right now. Some of that may be coming from high beef prices, but I think it is probably also due to foodservice operators beginning to restock as they watch covid infections decline and anticipate more foodservice demand in coming weeks. A good part of it is probably just due to the fact that in Jan/Feb there has been little to do but stay home and stay safe and that drives up pork consumption through the retail channel and we know that is positive for overall demand. The combined margin chart below ticked lower again this week after head-faking us last week. It is not helpful at all when this margin does not show a consistent trend in one direction or the other. Where will it go next? Up? Down? I have to vote for down since I¡¯ve got a little dip in the cutout built in next week, but I’m also very uncertain about that after this week’s strong market. Export markets appear to be doing ok, but below last year¡¯s torrid pace. I¡¯m projecting Q1 exports down 4% YOY, but last year¡¯s number was very strong so even a 4% decline leaves the export picture pretty good from a historical perspective. There are 2 scatter diagrams below. One for January and another for February. The January 21 data point is approximately on the same level as the 2013 and 2015 data points, but look what happens to the 2013 and 2015 data points in the February scatter. Am I too strong on Feb pork demand? I¡¯ve got the cutout averaging about $80 in February¡ªsimilar to where it was in January. If I were to bring my Feb21 data point down to the level of 2015, that would imply an average cutout this month of $70. Right now, it sure doesn¡¯t feel like its headed that way and we¡¯ve already got a week¡¯s worth of $80+ cutouts in the Feb average, so we would need to take the cutout down to $70 very quickly if we are going to average that this time around. With the way demand has been running, I don¡¯t think I can justify that. Maybe a $76-77 cutout, but not a $70 cutout. That said, at some point demand will cycle lower and that will be the catalyst for pushing the cutout back into the low $70s. Its hard to say when the demand cycle will turn, but since the combined margin indicator has been in a sideways mode and prone to head fakes lately, we could shift back to the 8-week model for cycles in the cutout. The cutout bottomed its last cycle around Christmas, so the 8-week model would imply 2-3 more weeks before the cutout breaks lower. This week¡¯s kill clocked in at 2.69 million head. That exceeded the pig crop projection by 100k head. It doesn¡¯t appear that there is a shortage of market-ready hogs out there right now. Kills should work steadily lower in the weeks ahead and should hold pretty close to last year¡¯s level unless the pig crop remains under-estimated even after USDA¡¯s million-head increase from the last H&P report. In that case we might expect to see kills run over last year into March. We will soon transition to slaughtering the Sep/Nov pig crop, which USDA reported down 1.4%, so that should supply a modest amount of additional tightening this spring. Carcass weights came in a pound lower this week and so things are headed in the right direction there. The DTDS also pulled back from a really high level this week and that makes me feel more confident that the industry can kill this extra weight off of the hogs over the next month or so. Bitter cold weather in the upper Midwest next week should also help to trim weights down. In the futures market, traders are rightfully seeing the current demand situation as bullish and combining that with strong corn pricing to paint a very bullish situation for 2021. That has created a pretty serious over-pricing situation in my opinion. For one thing, we know that the current strong demand picture will fade at some point and there is no guarantee that corn pricing is going to remain high in the US. China could back away from its purchases and the weather in our Corn Belt could turn out to be better than expected. It is only early February¡ªway too soon to declare 2021 as a high corn price year. But alas, this market has pretty much decided to buy now and see what happens later. The cutout futures are now pricing in a $96 cutout in July, but the summer market hasn¡¯t come anywhere near that level in the past three years. Maybe this year will be different..

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}