Pork Wrap February 4

The pork cutout was essentially unchanged this week, averaging

$95.71. The cash hog markets were another story however, with the

NDD negotiated market gaining $8.71 on a weekly average basis.

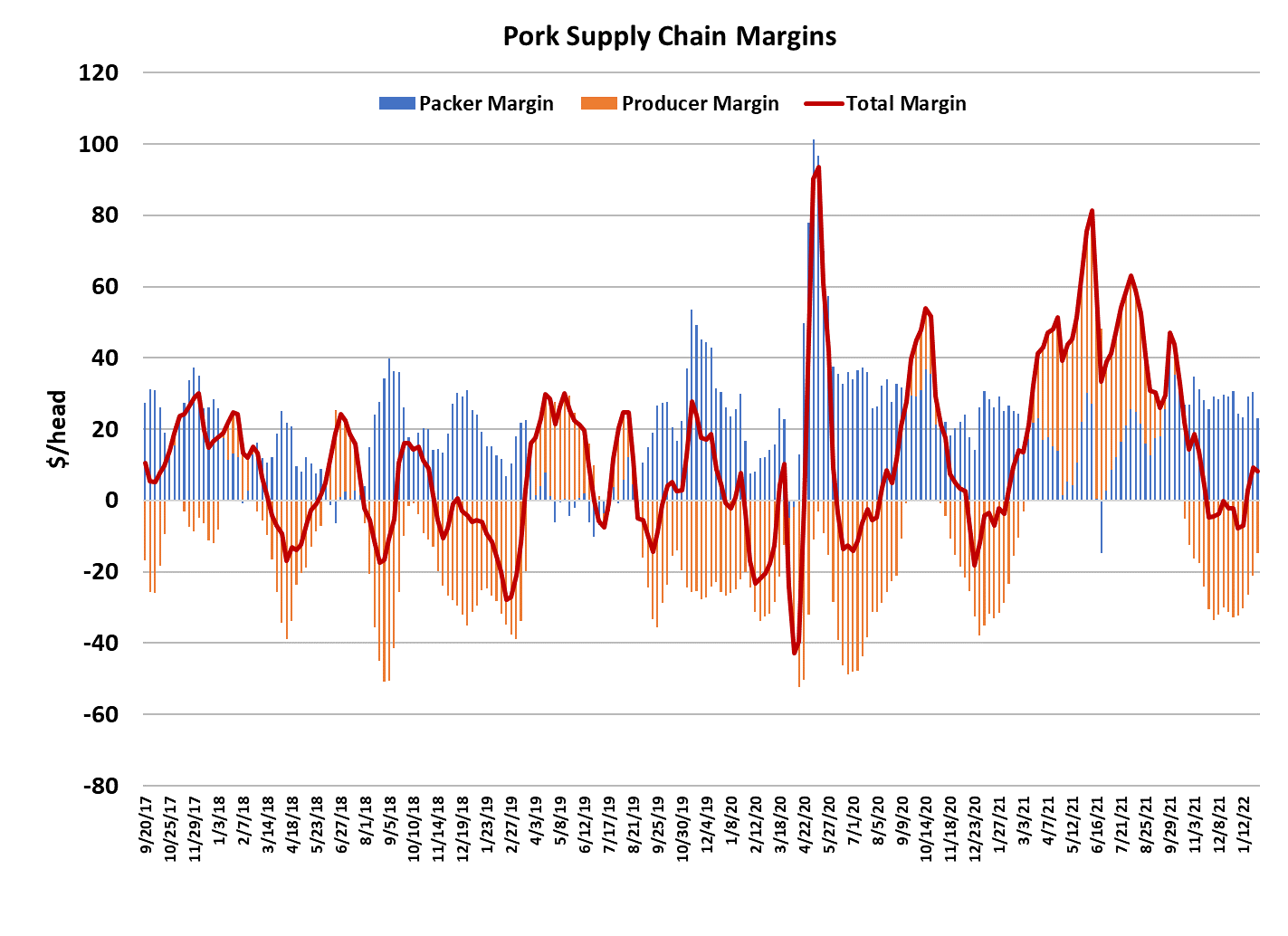

That meant more compression in packer margins, which lost about $7

on the week to $23/head. The buzz is all about what is going on in

the cash hog markets. The week before last, when negotiated hog

prices jumped $8/cwt, there was a thought that perhaps it was just an

anomaly, but after moving another $8 higher this week, it is pretty

clear that something seismic is going on. Spot hog supplies seem

unusually tight and that might very well be due to more problems with

PRRS this year compared to other years. We’ve also heard that hog

producers in Western Canada are seeing significant outbreaks of

PEDv. Those operations typically farrow piglets that are shipped into

the Upper Midwest for finishing.

Further, cross-border trucking is all messed up due to both the US

and Canada insisting on all truck drivers who want to cross the border

be vaccinated for COVID. That points to a potential gap in piglet

supplies here in Jan/Feb that would manifest as tighter-than-expected

hog supplies in June/July. But that is future tightness in the hog

supply. It is still a bit unclear what is causing the current tightness on

the supply side. It is possible that the summer pig crop might have

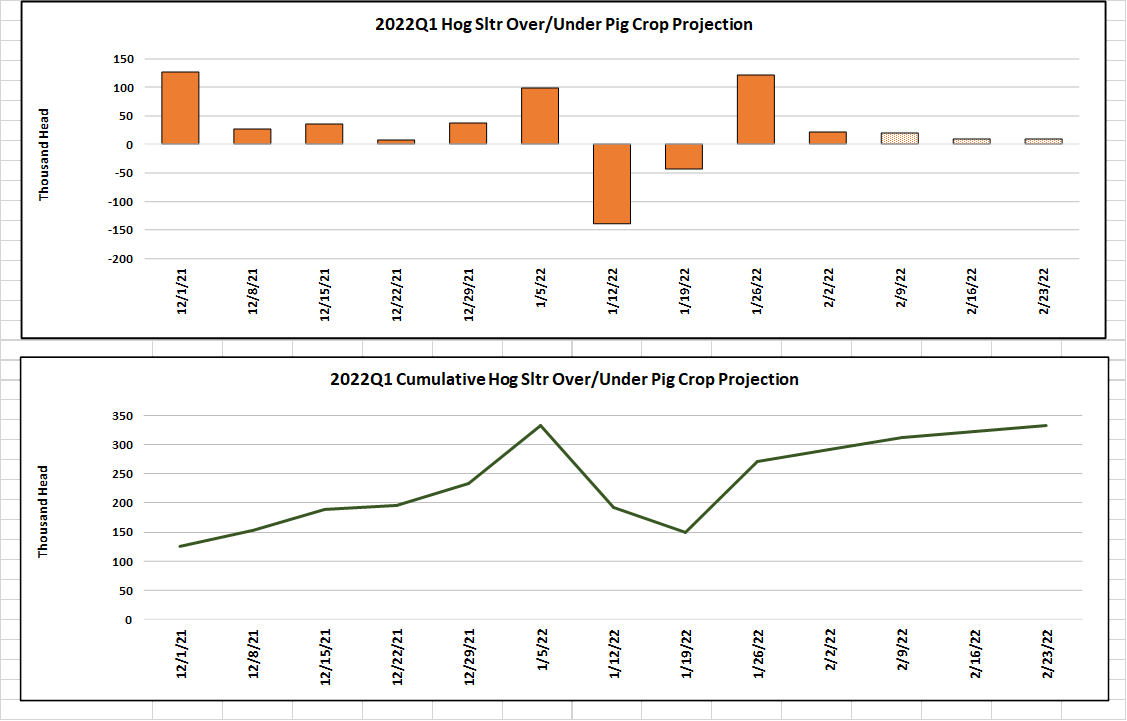

been more front-end loaded than expected. The chart below shows

that packers over-killed the pig crop through December and into early

January. Then, they under-killed it for a couple of weeks as omicron

was surging and labor availability became a major issue. This week’s

kill however, at 2.44 million head, was much more in-line with what

USDA estimated. The daily kills were really small this week,

averaging only 447k, compared to 466k the week before, but packers

did a relatively large Saturday kill of 203k to bring the weekly total

close to the pig crop estimate.

It is not clear what caused the small daily kills. It probably wasn’t

weather issues since most of the hog plants are located well north of

where this week’s storm began. Maybe it had something to do with

the rapidly rising cash hog market, but if that were the case then it

wouldn’t make much sense to do a big Saturday kill. Or, it could just

be normal downtime for maintenance and cleaning. The forecast

has next week’s kill holding at 2.44 million head, but with bigger

weekday kills and a smaller Saturday slaughter. Once February is

done, the industry will start working through the Sep/Nov pig crop,

which USDA estimated to be down 3.6%. If USDA is right about that,

then slaughter levels ought to hold in the 2.4-2.45 million head range

right through the end of March before they shrink further in late spring

Barrow and gilt carcass weights were reported one pound higher

this week and now stand at 218 pounds. That seems awfully heavy

if hog supply is truly tight. That is another piece of the puzzle that

doesn’t fit nicely. Normally weights will trend slightly lower through

February and then plateau in March before beginning their

seasonal descent toward a bottom in the middle of summer. The

DTDS weights looked high this week also. So, the weight data is

saying plentiful hogs, but the price data is saying not enough hogs.

My inclination is to go with the prices—they don’t usually lie. The

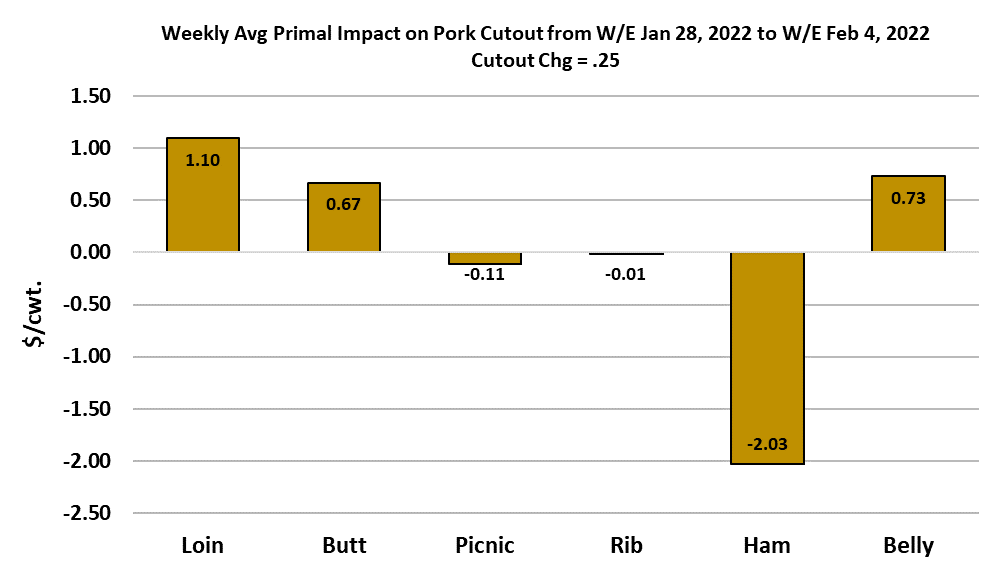

week the retail cuts—loins, butts—firmed up enough to keep the

cutout steady in the face of ham price weakness. Bone-in 23/27

hams dipped back to the $40 area after trading in the mid-$50s just

a week or so ago.

It also looks like the boneless hams are not commanding as much

of a premium as they have in the past. I see that as more of a

demand-side problem than growth in the supply of boneless hams

due to more boning labor. That is partly because the trimmings

keep marching higher and that is a pretty solid indicator that

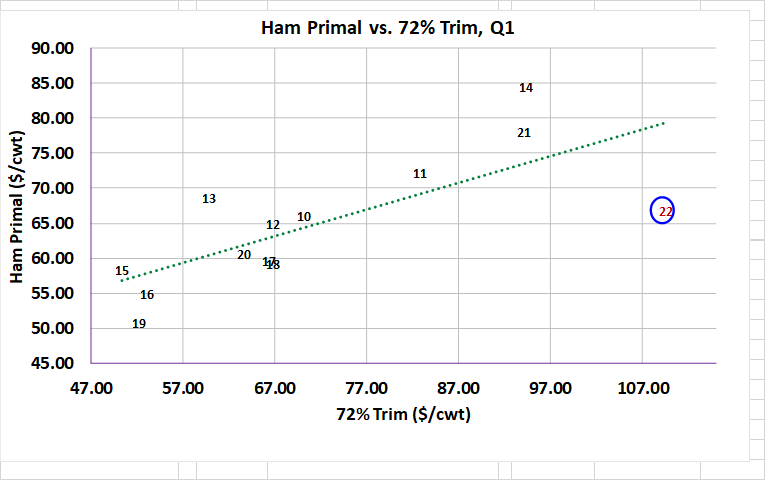

packers are not producing a lot more trim these days. In fact, ham

prices are pretty low relative to 72% trim (scatter below) and that

would normally justify throwing some hams into the grinder.

However, before that can happen, the bone has to come out.

Therein lies the problem. Still not enough boning labor. Bellies

continue to work higher in methodical fashion, and that could help

lift the cutout a bit next week. I had been thinking that pork demand

was in an upcycle, but the cutout stalled this week on smaller

production and the combined margin took a little tick lower. I’m not

ready to call this demand upcycle complete, but it certainly has

slowed down some.

Beef prices are now moving lower, so that may become a

headwind for pork in the next couple of weeks. Still, I think the

main determining factor on the cutout’s direction in the next month

or so will be the supply of hogs. If there really is a significant

disease problem that limits hog availability and drives up hog

prices, you can bet that it will also push pork prices higher. The

biggest negative in the complex remains export demand, which is

well below last year’s strong level. However, the supply of hogs

being down 6% or more here in Q1 has kept pork buyers from

seeing much benefit from the smaller exports. Hog producers

sensed the pullback in demand from China and they scaled back

the herd size appropriately. Next week, watch those negotiated

hog markets. They are trying to tell us something.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}