Pork Wrap February 26

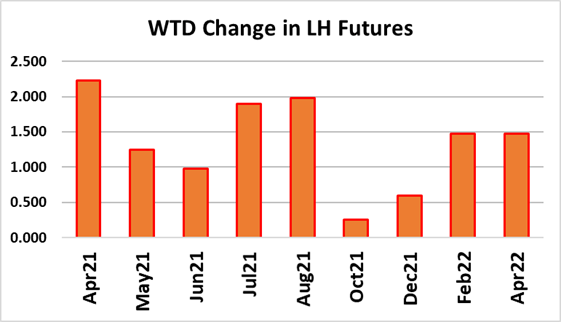

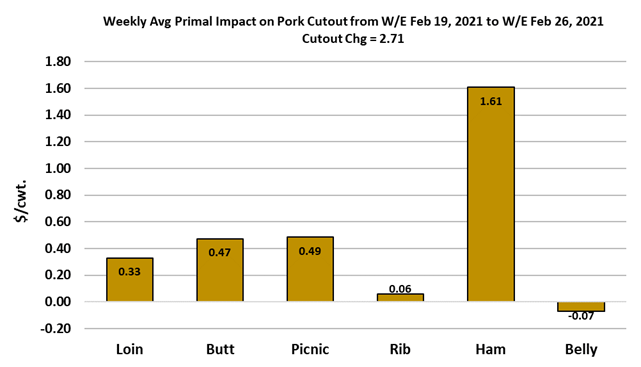

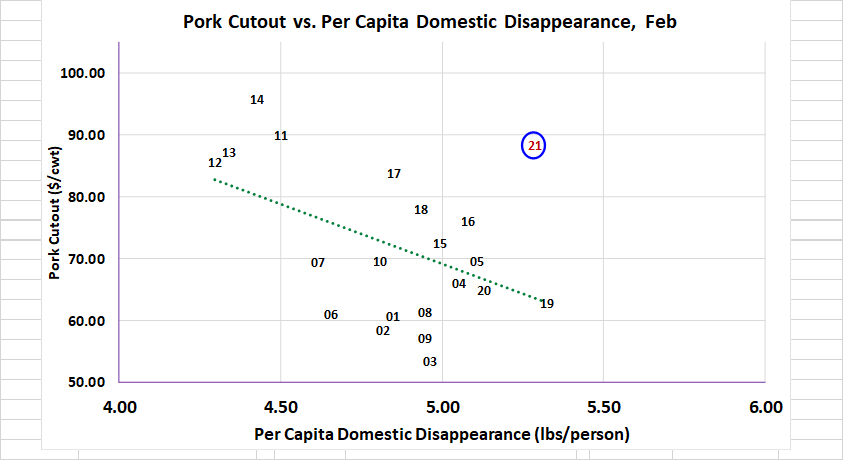

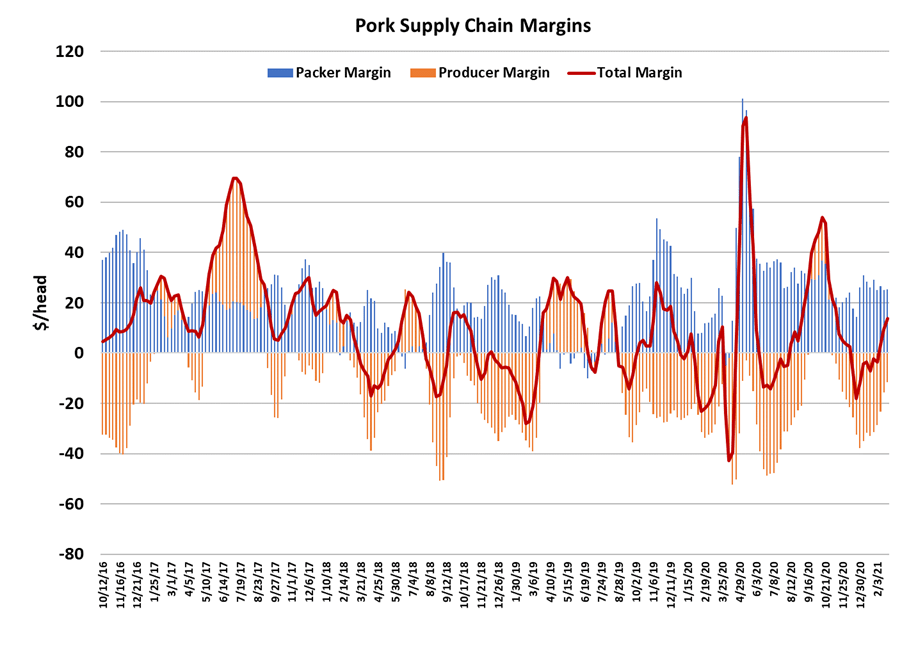

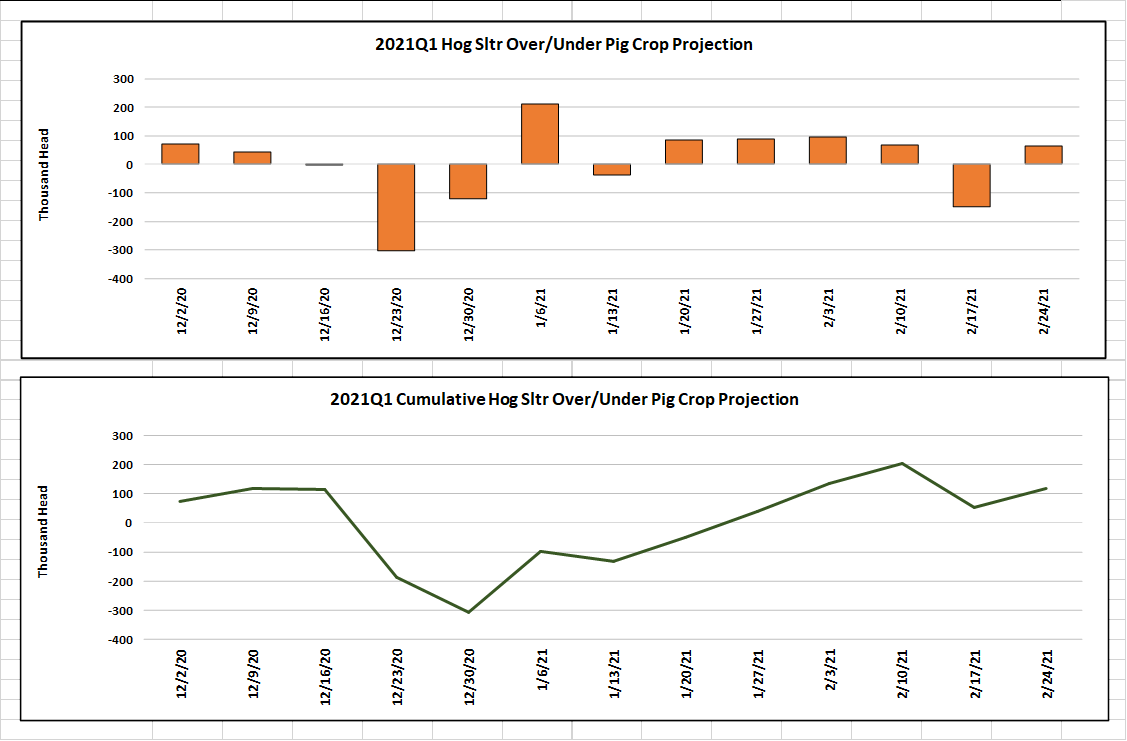

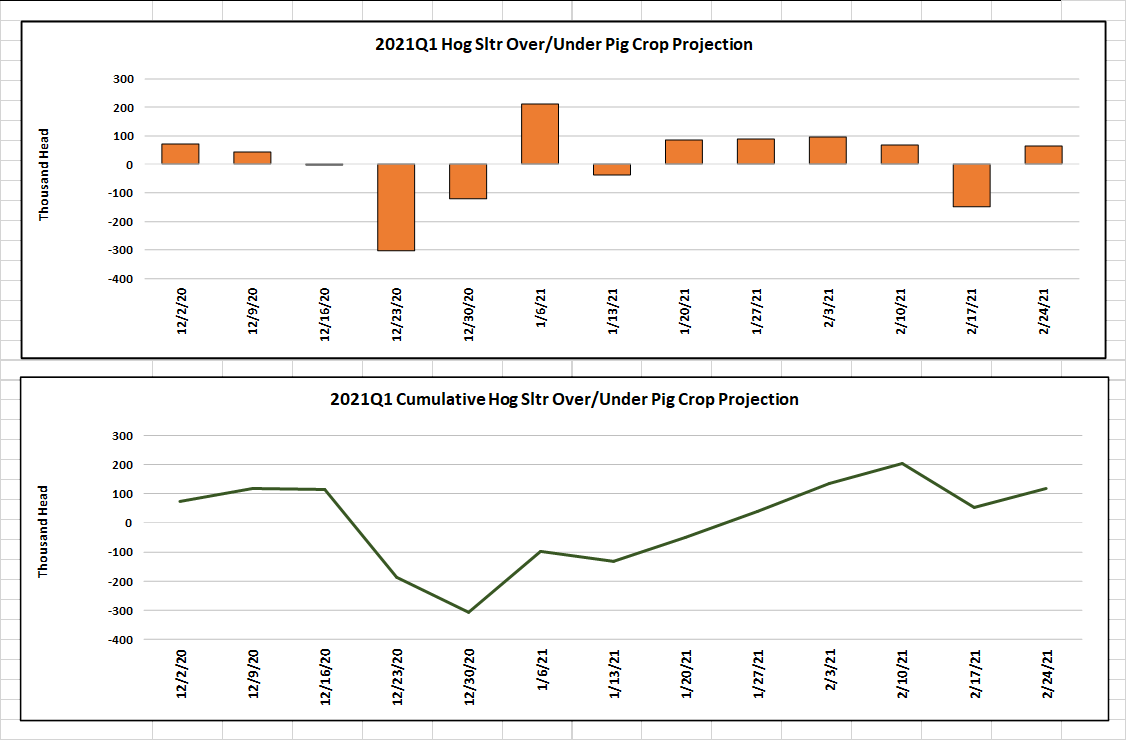

The cash hog market moved higher again, with the NDD negotiated market gaining a whopping $6.37 on a weekly average basis. The cutout averaged $2.71 higher than last week at the same time. Packer margins were mostly unchanged at $25/hd, but should shrink next week as the big gains in the negotiated market get fully reflected in the LHI. Last week, I questioned whether futures traders would be happy to let the Apr futures sit at $85 when the LHI was poised to reach $79 early this week. Turns out, they were not going to let that happen. After modest gains on Monday and Tuesday, traders went full bore on Wednesday forcing the Apr contract to settle limit-up. By Thursday, Apr was trading at $90, and sure enough the market sold off on Friday to settle back around $87. Now, just because the market had a big down day today, we shouldn’t assume that the strength in LH futures is going to fade. This was not a decline caused by some major change in the fundamentals, but rather a case of the market correcting after getting too excited in the middle of the week. The cutout is still hovering in the mid-$90s and the negotiated markets are still rising. If the cutout can continue working higher next week, then I think Apr will make another run at $90. After all, the LHI will likely be approaching $83 by midweek. If Apr were to stay at $87 that would only be a -$4 basis with a month and a half until expiration. That doesn’t seem like enough, unless the cutout is on the verge of falling apart, which it doesn’t seem to be. This big rally in the hog markets has caused some market participants to have visions of a triple-digit LHI this summer and cutouts above $120. I don’t think so. Keep in mind that the cutout went to $120 last spring, but we had to slash production in half to get there. I don’t think production is going to get cut like that this year. We are just in a very strong demand environment right now and that is what is driving the strength in the cash hogs, cutout and futures. These “bubbles” in demand happen from time to time in the hog market. The most recent example was last October. Keep in mind they can work in the other direction also, like when the market encounters a “demand air pocket” and prices move lower than most would have imagined. We haven’t had one of those in a while, but I’d be willing to bet that one surfaces before the end of 2021. When it does, it is going to make talk of triple digit hog prices look pretty silly. The supply side of the market looks pretty normal right now, outside of the short-term tightness in pork availability caused by a light kill last week when a deep freeze gripped the Midwest where many of the pork plants are located. Pork is caught up in the same impressive demand strength that is affecting beef and chicken. Domestic demand is very strong for all forms of animal protein at present. That will be exacerbated in the short run by the need to restock retail meat cases that were stripped bare before and during the weather event last week. The combined margin chart below shows that margin continuing higher and my thought is that it has 2-3 more weeks to go before it tops out. Also, the price-quantity scatter diagram for February illustrates just how strong pork demand has been this month. Look at where the 2021 data point is higher than in any other February, even the PEDv year of 2014. That is very impressive demand and it is domestic in nature because the per-capita disappearance variable on the X-axis takes into account imports and exports. Notice that per-capita disappearance is nearly the same this February as it was in February 2020, yet the cutout is almost $25 higher! No doubt that demand here in Q1 has been phenomenal so far. But, I caution readers not to think this kind of demand strength will continue indefinitely. It almost certainly will not. Further, the market will often suffer a significant demand “hangover” in the weeks and months following such a lofty showing. It might be a couple of weeks or a couple of months down the road, but softer, more normal, demand will return and prices will move back to more traditional levels. If there were something serious happening in the supply side of the market, say like PEDv, then I would have no problem seeing $90 or $100 prices this summer. But this looks like a purely demand-driven episode and that makes me think it will fade at some point. Speaking of the supply side, this week’s kill came in at 2.64 million head, which the chart below indicates was about 75k more than the Jun/Aug pig crop implied. We should now be done with that pig crop and next week will begin killing the Sep/Nov pig crop, which USDA estimated to be down 1.4% YOY, a little snugger hog supplies than last year, but certainly not enough to jack prices into triple digits. In the end, it looks like the industry over-killed the revised Jun/Aug pig crop by about 100k head. That is not a very big deviation for a 13-week period. Good thing USDA revised that pig crop upward by a million head back in December or else we would be screaming, “where are all these pigs coming from?” Barrow and gilt weights posted a big drop this week, down 2 pounds, and that caused the DTDS to plunge below the zero line. That makes it look like producers are in good shape with their marketings and thus may be able to keep the cash hog market moving higher in the near-term unless the cutout falters significantly. Next week, look for the futures to regain some of today’s losses and watch the cutout for any persistent weakness. A single down day does not make a trend, but string several down days together and it may be time to declare the party is over.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}