Pork Wrap February 25

Things slowed down a bit in the hog and pork complex this week. The

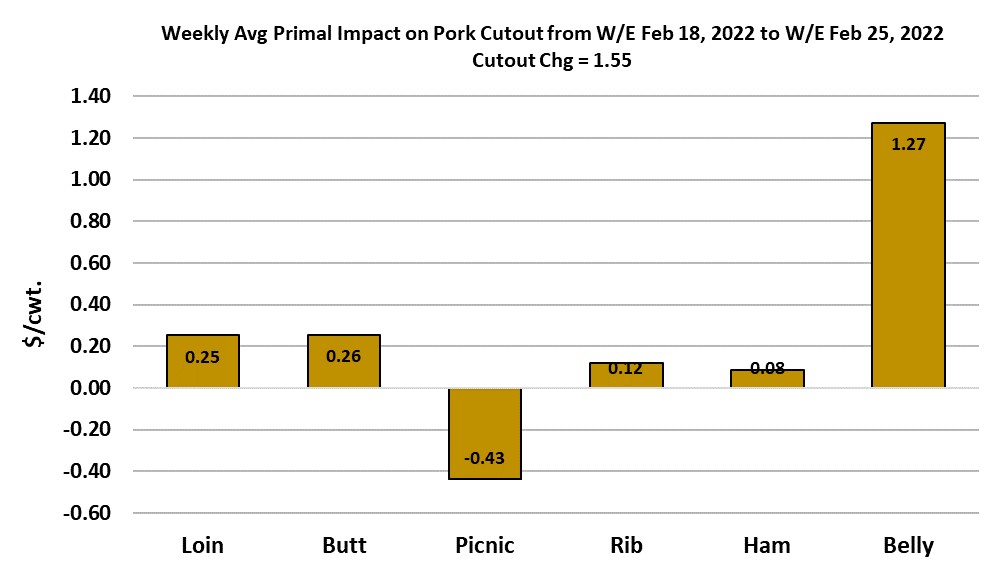

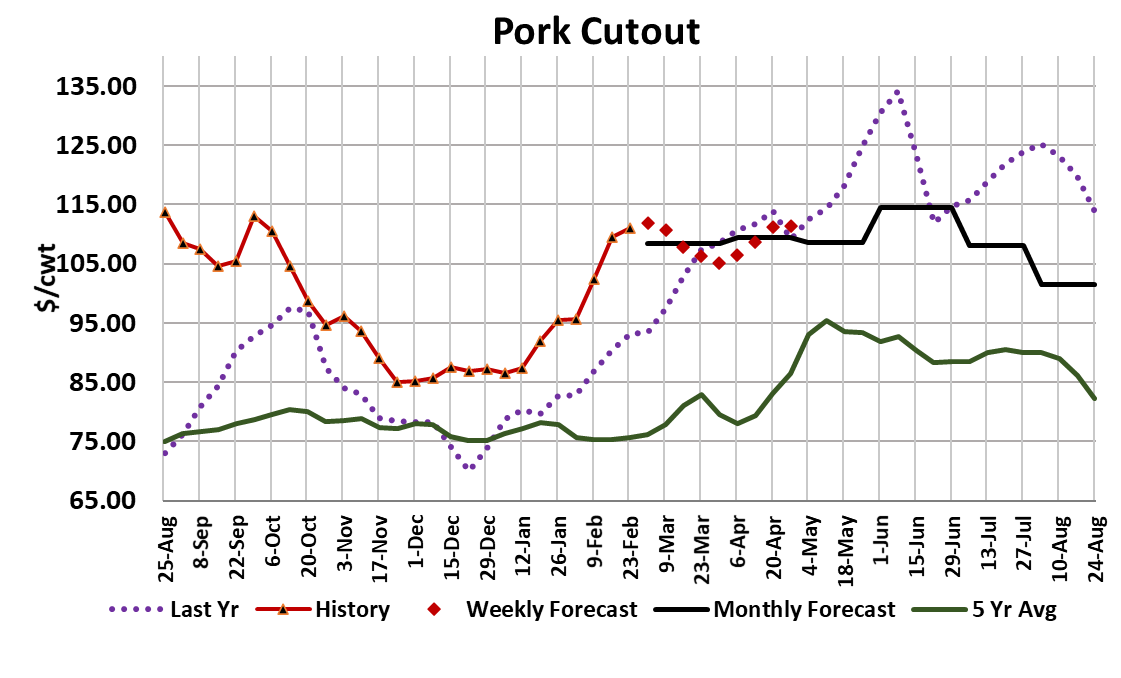

cutout was higher, but only up $1.55 on a weekly average basis. Cash

hogs were down slightly, with the NDD negotiated market dropping $0.75.

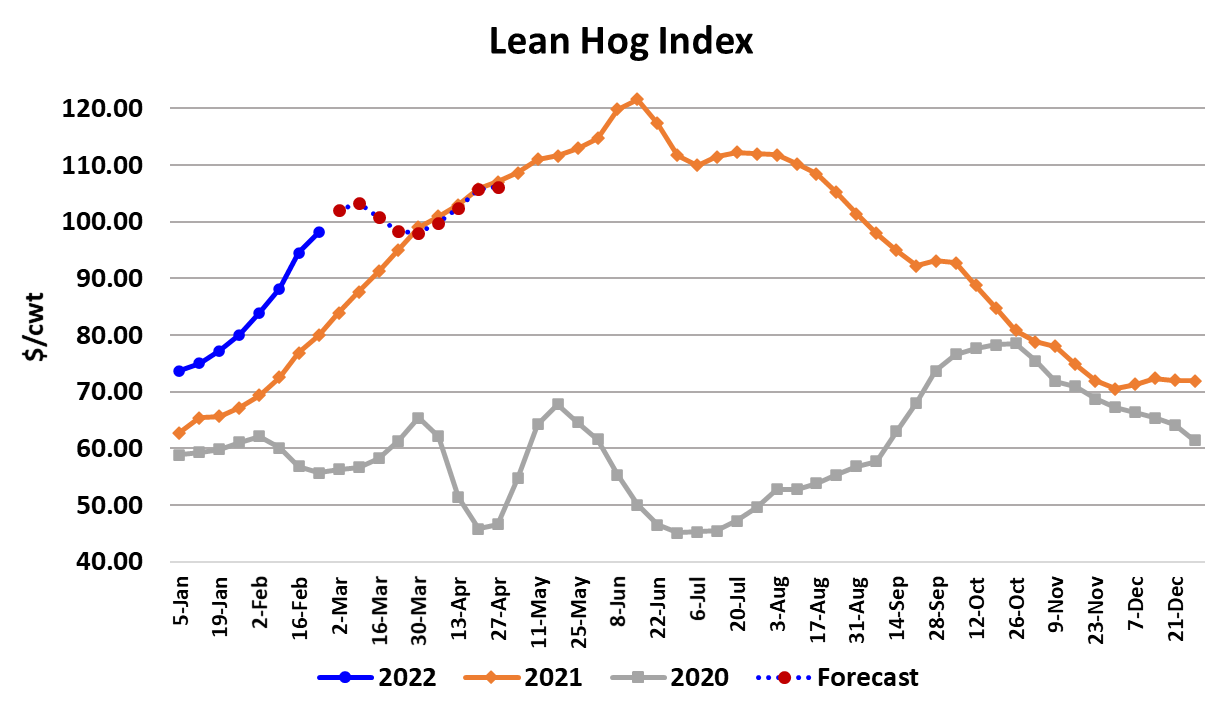

The LHI gained $3.67 because it had some catching up to do from the

prior week. The next release of the LHI is expected to be $99.27. The

sow market was on fire however, up nearly $7. Sows averaged $78 last

week. That used to be a good price for market hogs. Even though hog

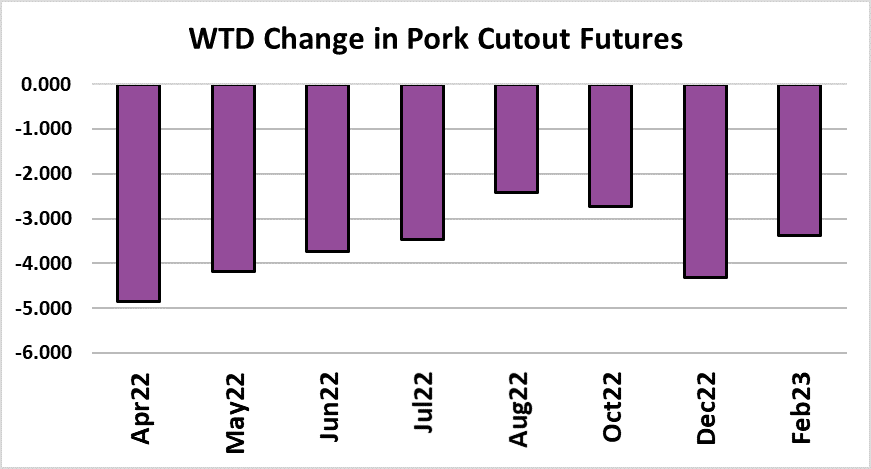

and pork prices were steady to a little higher, futures traders turned

decidedly bearish and punished nearby Apr with an almost $6 loss on the

week. To be fair, the futures had gotten overly optimistic and at one point

this week traded $112.85. That was close to $14 over the LHI at the time.

The market quickly realized the error in its ways and by the close on

Friday, Apr was back down to $103.67. Now Apr is less than $4 over the

LHI. That is quite a change. The news of Russia’s invasion into Ukraine

sent all markets into a tizzy and the normal reaction in those situations is

to sell first and figure out the implications later.

Hogs were easy for traders to sell because they had risen so much in the

past few weeks. Market participants are trying to determine if the cash

markets are near a top or if there is more room to run. The cutout was

really strong toward the end of the week, averaging close to $114 in the

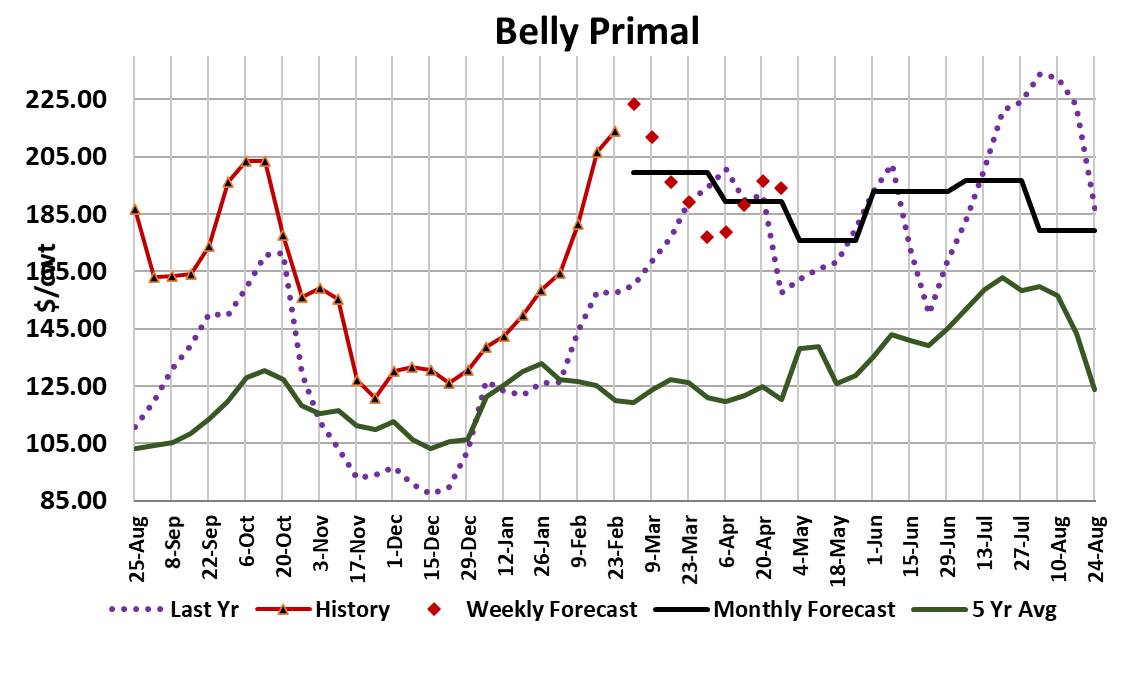

last two days. Bellies were providing much of the support for the cutout,

but there were positive contributions from other parts of the carcass. As I

look across the primals, bellies are the only one that appear to be in

significant danger of breaking lower in the near-term. The belly rally has

been going on since Christmas and has now seen 9 straight weeks of

price increases. That is way longer than most belly rallies last, but we did

have a belly rally last year that started at Christmas and didn’t end until

early April. Over the course of that rally, the belly primal went from $87 to

$200, a $113 increase. The current belly rally has added $88. The fear

is that when the bellies start to move lower from such high levels they

often do so very quickly and take the cutout lower in big chunks. I think

that the bellies can increase for another week or two, but am looking for a

sharp break after that

Hams appear to be on solid footing, with the bone-in hams currently

trending higher and we are seeing more boneless volume in the primal

mix these days, which has the effect of boosting the overall primal value.

Weekly exports to Mexico have been strong in the past few weeks and

that points to good demand for hams. All of the retail items should do

well for at least a few more weeks as consumers trade down from moreexpensive beef when they visit the grocery store. However, the Ukrainian

conflict is increasing the prospects of further price inflation in the general

economy and thus consumer budgets will likely get very stretched this

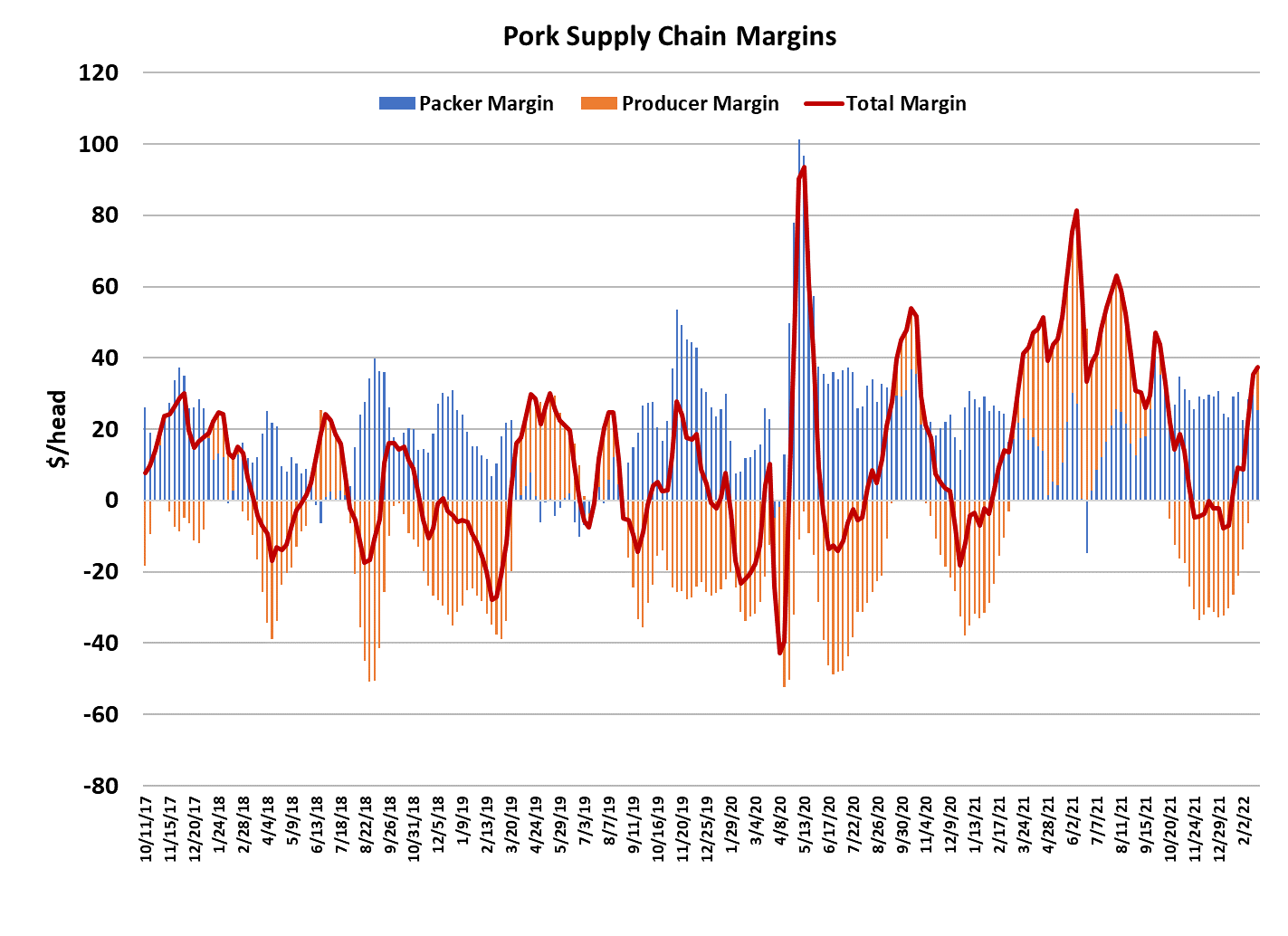

spring. The combined margin is still moving higher, but this week’s gain

wasn’t as strong as in recent weeks. Maybe it is going to top next week or

maybe it will just give a small head fake and continue higher. Over the

past few weeks, it has been strong domestic demand that has pulled the

cutout higher, but very soon we will start to see kills tighten up and thus

more of the influence may start to come from the supply side.

This week’s kill came in at 2.51 million head, up slightly from last week

and about 90k over the pig crop projection. This was the final week of

the Dec/Feb quarter and by my calculation the industry over-killed the

pig crop by about 550k. That isn’t a terrible miss, but it will likely cause

some upward revision in the Jun/Aug pig crop when USDA releases the

next Hogs and Pigs report on March 30. Next week we start working

on the Sep/Nov pig crop which should give us weekly kills in March

around 2.45 million head and by April that will be down to 2.35 million

head. So there is some hog supply tightening on the way. If the

disease problems are worse than normal, we could see kills even

smaller than that. That seems to be what the summer futures are

banking on. After the Jun contract traded close to $122 this week,

traders did an about face and Jun finished at $113.87 this afternoon.

The fundamental forecast has the cutout holding near this week’s level

for one more week and then starting to slowly ease, but not moving

back below the $100 mark. Hopefully the hand-off from demand-driven

support to supply-driven support will go smoothly and keep the cutout

relatively well supported.

A lot has been said lately about spot hog prices being near $100 in the

Western Corn Belt. The theory is that disease issues are worse there

than in the other regions. But, we need to remember that the cutout is

in the low $110s and that allows packers to pay $100 for cash hogs and

still have a decent margin. This week’s packer margin is estimated at a

little over $25/head, down $4 from last week. I don’t think many pork

packers would complain about a $25 margin at the end of February.

When the cutout starts to ease, then we will really find out how tight the

hogs are in the cash market. If packers can’t seem to move cash hog

prices lower, then we will have to surmise that the disease problems

are real and extra hogs are tight out in the country. The fact that they

were able to stabilize the cash market this week was a good sign.

Carcass weights look pretty normal for this time of year and the DTDS

isn’t pointing to any issues with either too many or too few hogs in the

pipeline. Right now, US pork prices are the highest in the world and

that is attracting imports from countries where domestic prices are a lot

lower.

At the same time, pork exports are way down from last year. That has

added to per capita availability, but it cannot completely offset the

impact of smaller domestic production stemming from a very small pig

crop last summer. I estimate that per capita availability will be down

about 4.5% YOY in both Q1 and Q2. Both of those pig crops are

already known, so hopefully those estimates are pretty close. I did

recently scale back my forecasts for the next few pig crops to take into

account greater disease prevalence and the impact of input cost

inflation. Next week, keep an eye on the bellies because they hold the

key to further gains in the cutout and watch prices in the negotiated

markets for indications that there are still pockets of tightness in the hog

supply.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}