Pork Wrap February 24

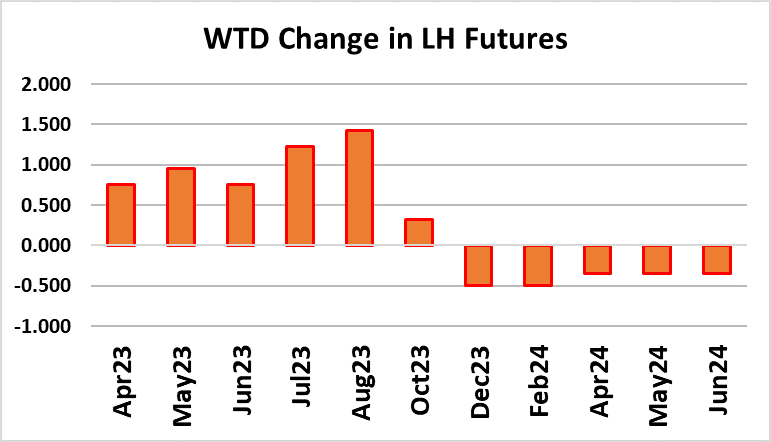

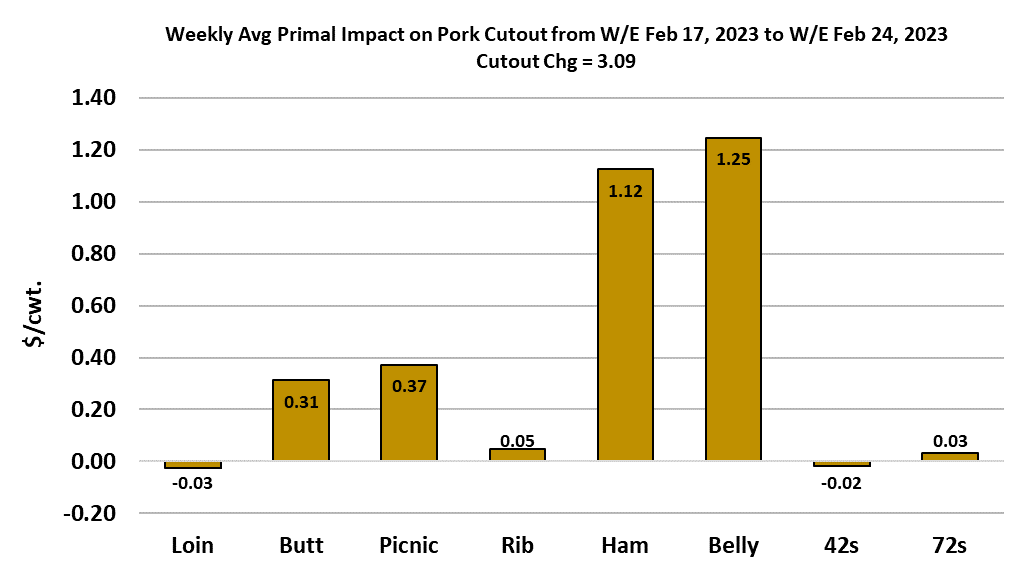

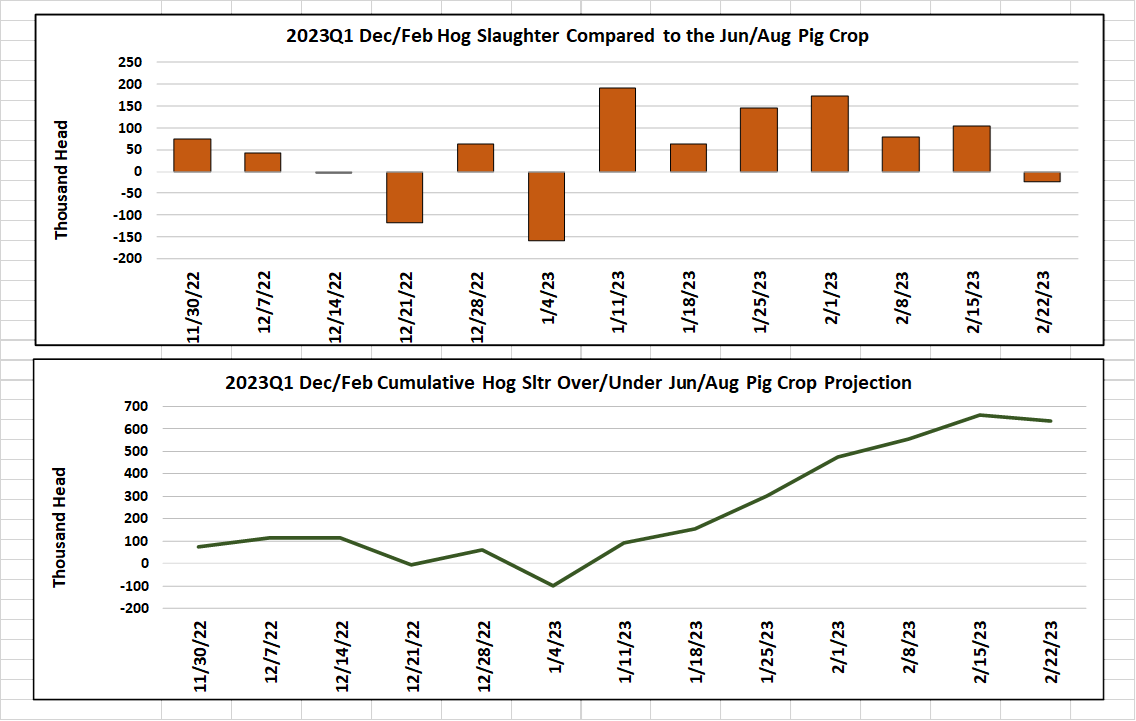

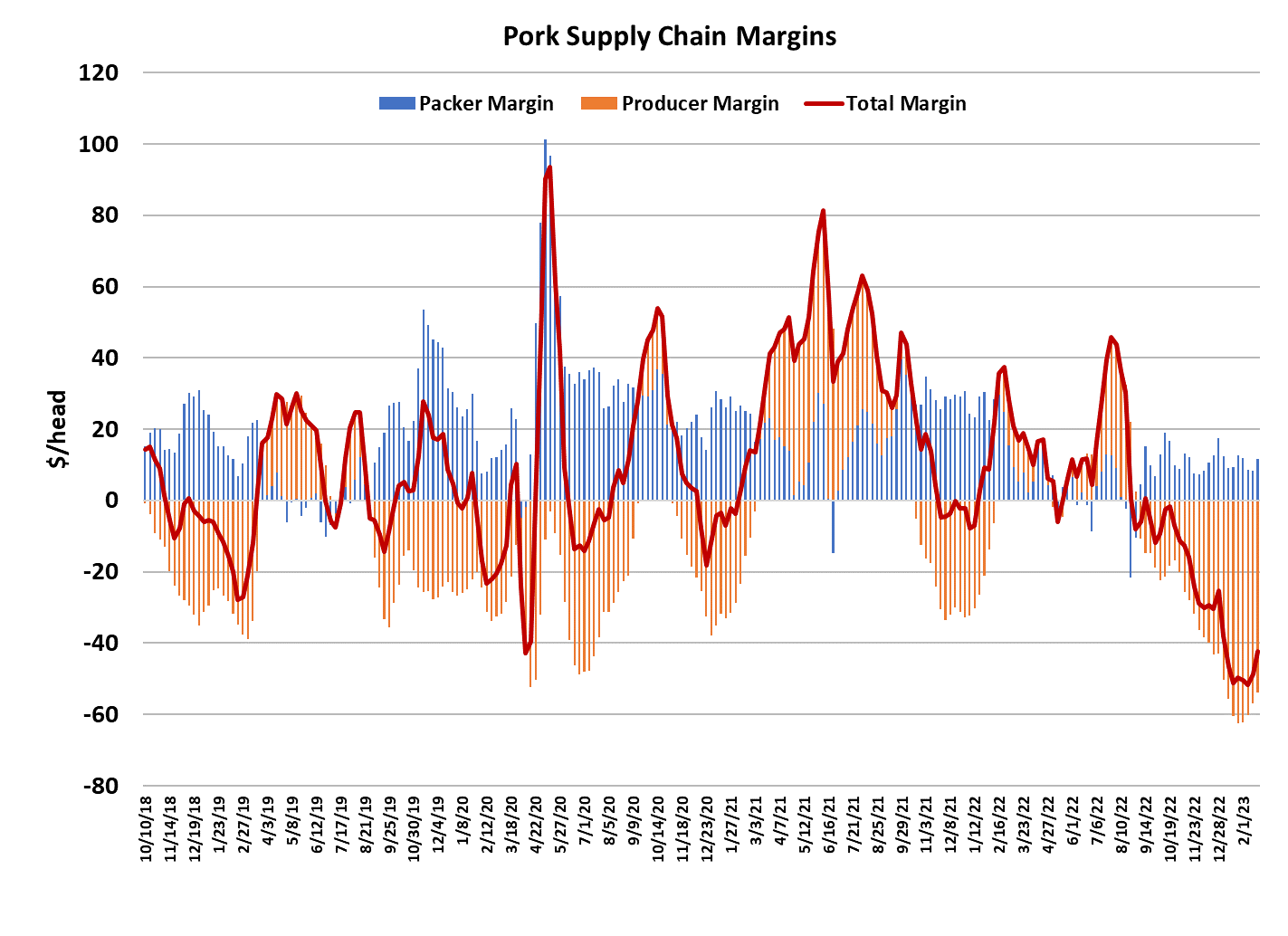

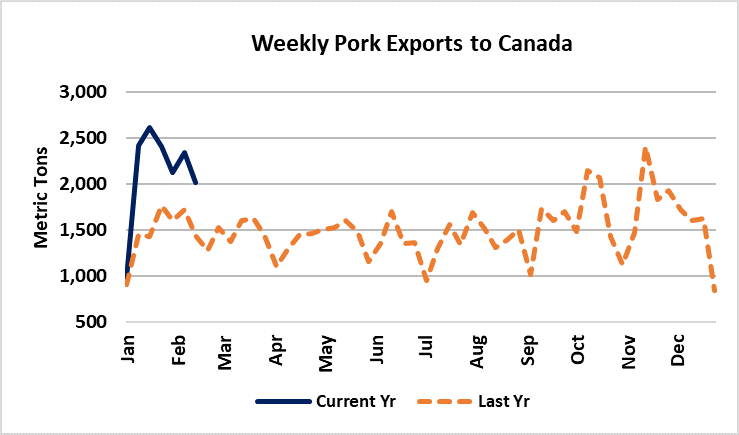

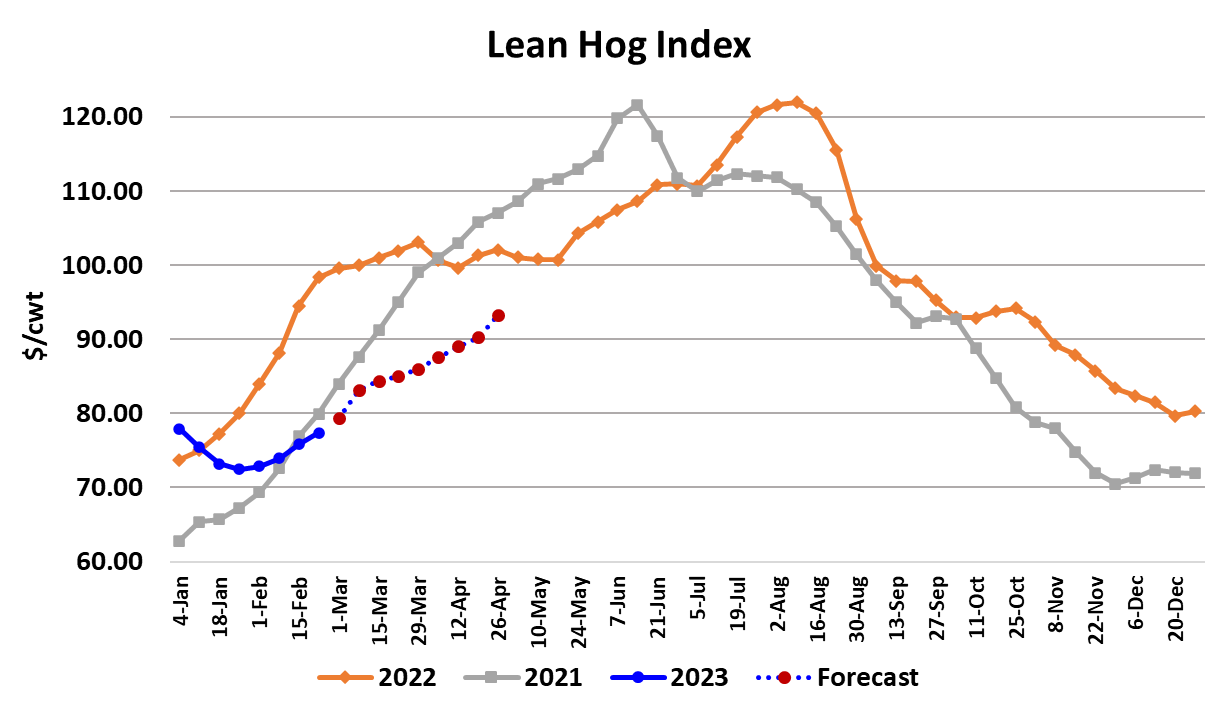

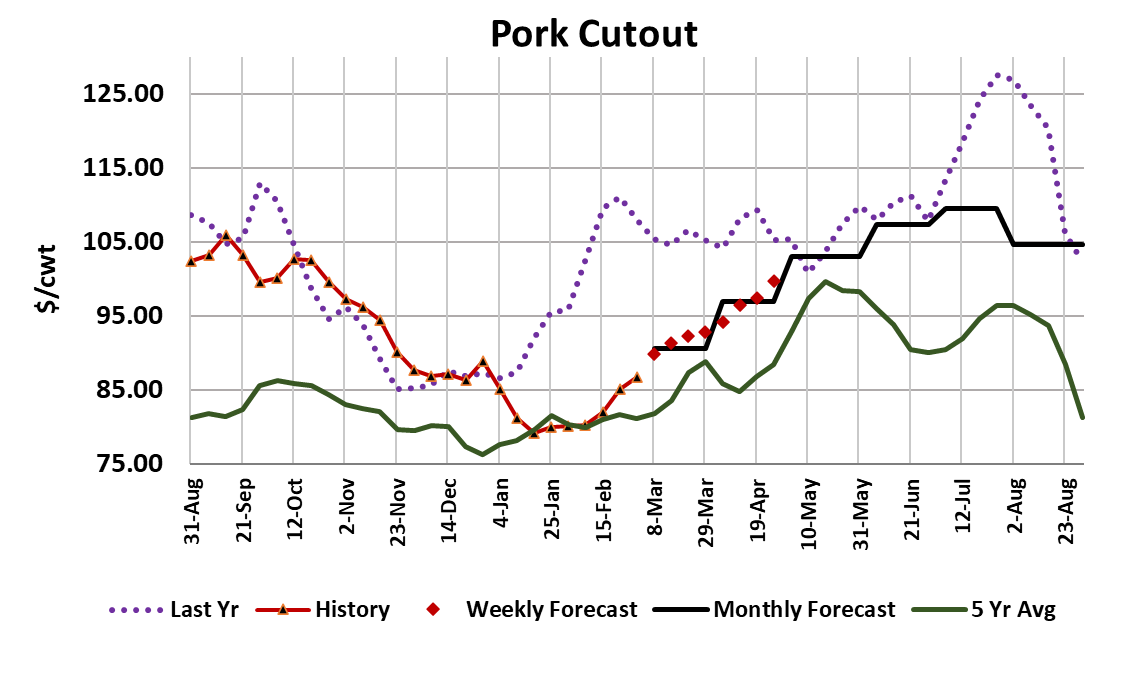

This week the pork cutout finally got some lift, rising $3.09 to average just a hair over $85/cwt. The boost was largely driven by gains in the hams and bellies, which could signal that processors are beginning to see better demand for their products. The cash hog market was a bit lethargic, with the WCB negotiated price gaining only $0.33/cwt while the NDD market was up $1.37. Intense winter weather across Northern Iowa and S. Minnesota caused some plants to close for a few shifts and thus limited packer’s need for spot market hogs. Packers tried to make some of that up by running more shifts on Saturday, but the weekly kill still only managed 2.38 million head. That probably means that some hogs that were destined to be slaughtered this week will be pushed into next week and as long as the weather cooperates I think we can expect the weekly total to climb back to at least 2.5 million in the week ahead. The cutout could see further gains early in the week as pork availability is restricted by last week’s smaller kill, however by the end of next week I would look for some cutout softening. The drop in this week’s kill produced the first week since early January where slaughter levels were lower than what the pig crop indicated. I’d take that as a fluke of the weather and not an indication that kills are now going to run at or below the pig crop estimate. Next week will mark the start of the March/May quarter and the industry will be working through the pig crop that was born in the Sep/Nov quarter. USDA’s survey indicated that pig crop was down 1.3% YOY, so we should expect slaughter during March/May to be down by a similar amount. Barrow and gilt carcass weights moved lower this week, now at 214 pounds and 3 pounds below last year at this time. This is normally the time of year when hog weights plateau until mid-to-late April when they start tracking seasonally lower again. FI pork production was down 2.7% YOY this week, but the weather played a big role in that. Next week, I’d look for production back close to last year and maybe even a little larger if packers work to get caught up on the hogs that went unharvested this week. That may also help improve negotiated hog prices. Packer margins this week were $11.65/head, up almost $3 from the week before. It seems likely that margins over the next few weeks will be a little tighter than what we saw this week. USDA reported total pork in cold storage up 19.2% YOY at the end of January. Cold storage stocks grew almost 50 million pounds from the end of December to the end of January. That means that the steady pricing that we witnessed throughout January required some product to be removed from the fresh market, otherwise the cutout would likely have moved lower. It does appear that the corner has been turned now and pork prices are heading higher, but the high level of stocks in cold storage will likely limit how fast, and how high, prices can rise this spring. The combined margin has now turned higher in a measurable way, so that makes me think that perhaps a new demand upcycle has begun. Futures traders don’t seem very impressed however, as the Apr contract gained less than $1/cwt this week. I find the gains in the hams to be the most encouraging factor right now. If the hams can maintain upward momentum, that should give enough support to the cutout to overcome some slight weakness that might emerge in the other primals. If bellies join the party, then maybe it will be possible for the cutout to reach the mid-$90 area by the time the Apr futures expire. However, I suspect that the odds favor a cutout at least a few dollars under that projection. There isn’t much to get excited about with respect to exports right now, as movement into China has really dropped off in the past few weeks. Canada has been the bright spot for export demand, but my guess is that won’t last more than a few more weeks. In all, this seems to be a pretty well-behaved market and the biggest surprises recently have come from the weather. Things to keep a close eye on going forward are the size of the weekly kill relative to the pig crop in the next few weeks and the negotiated hog market for signs that the underlying supply of hogs is finally beginning to tighten up.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}