Pork Wrap February 23

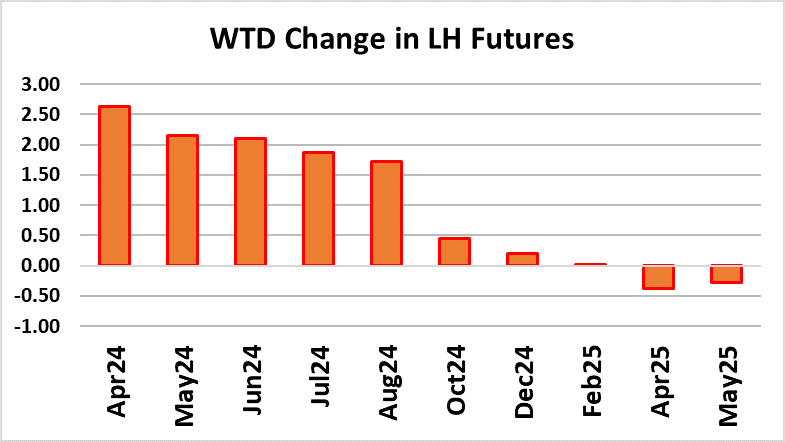

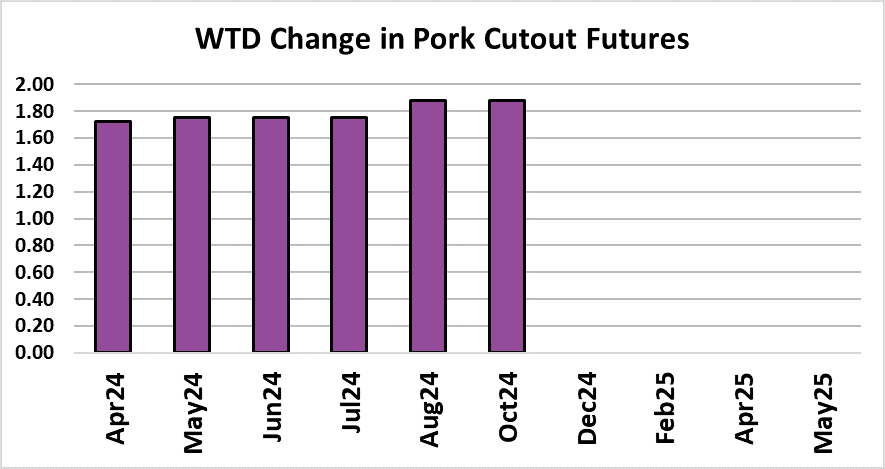

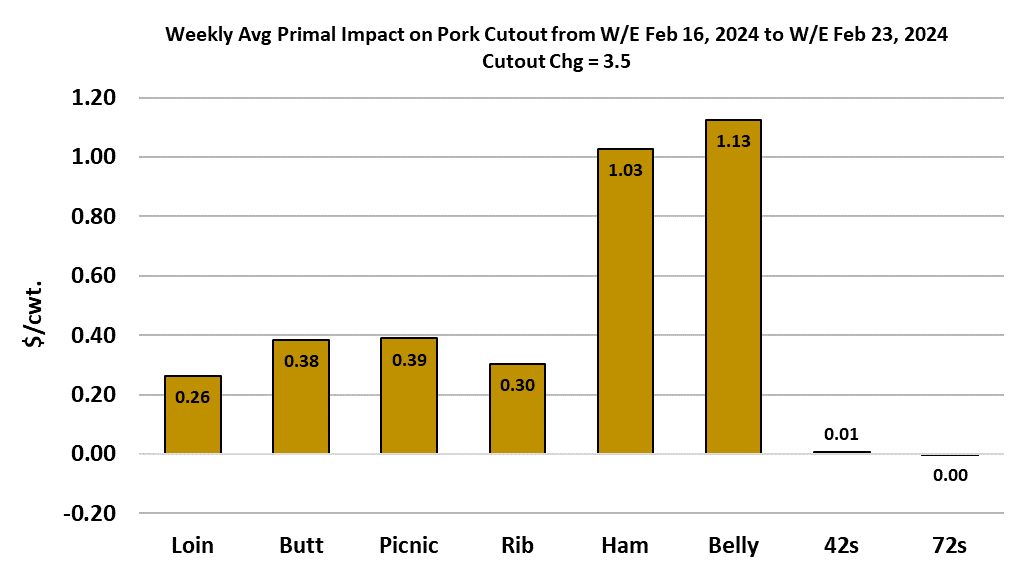

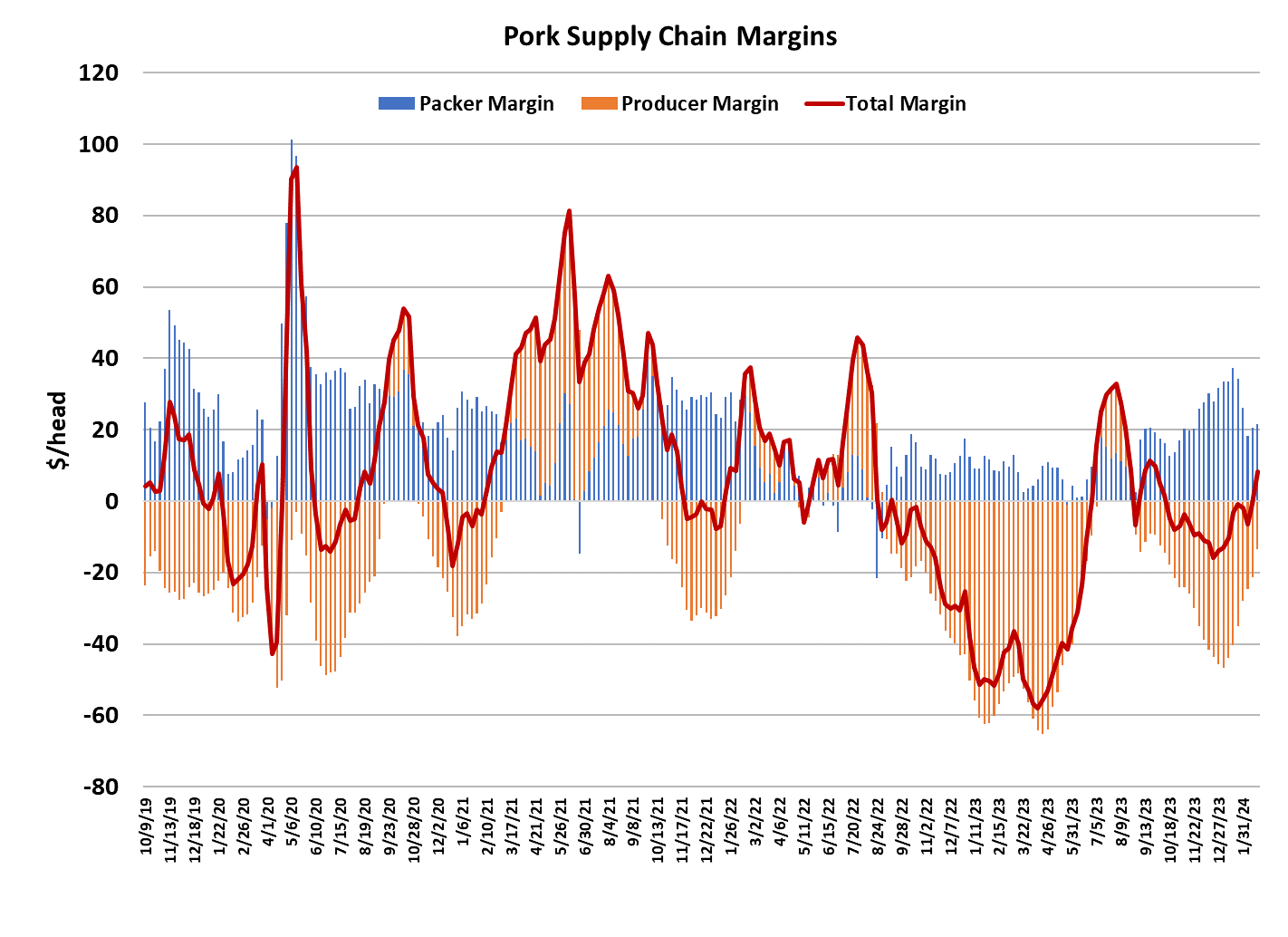

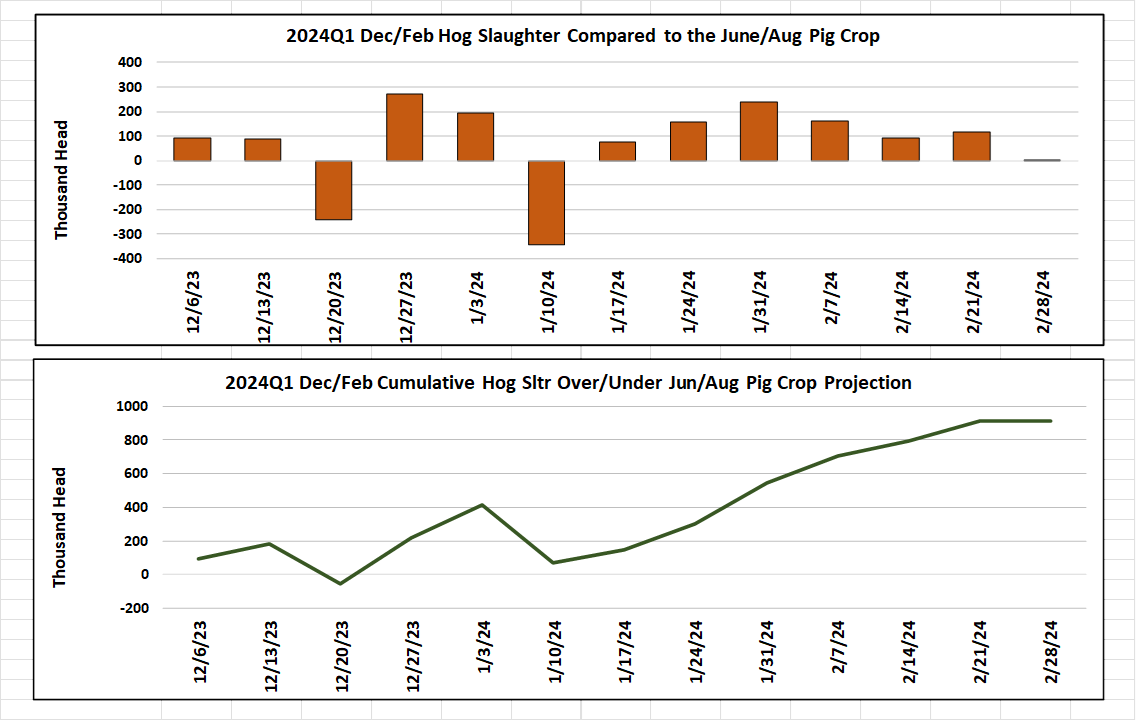

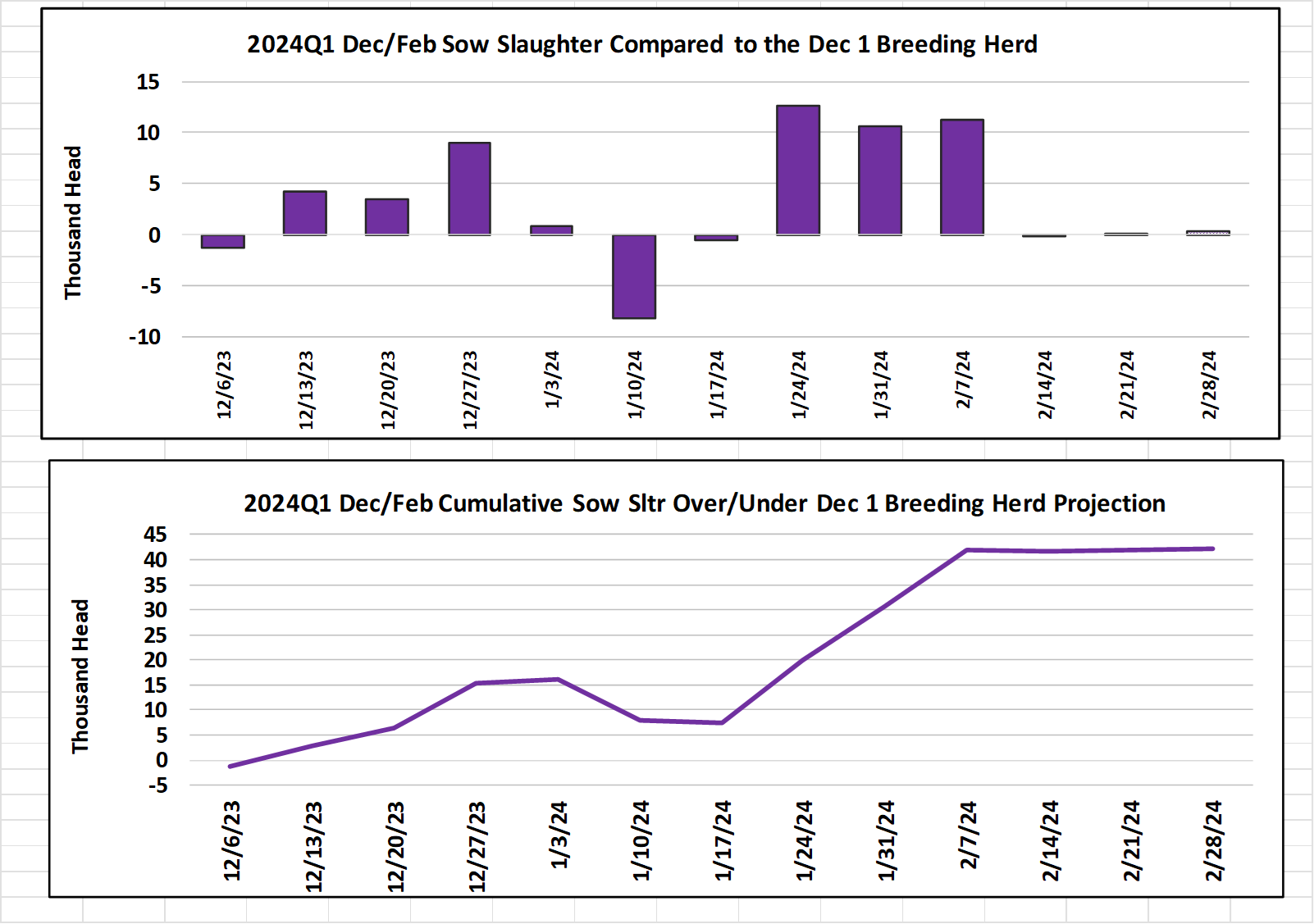

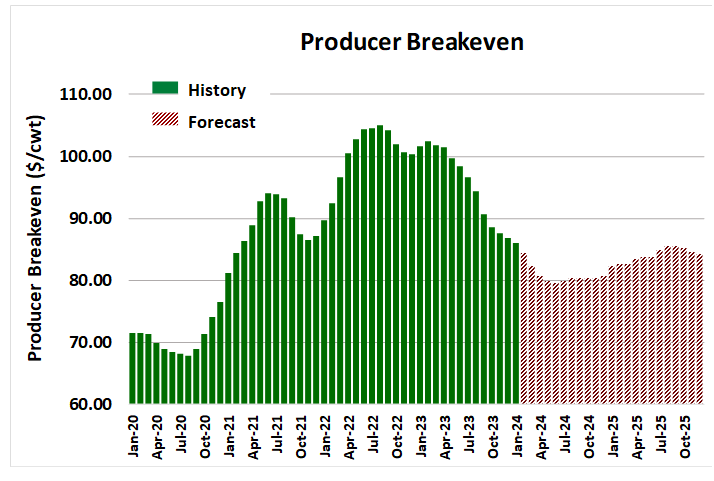

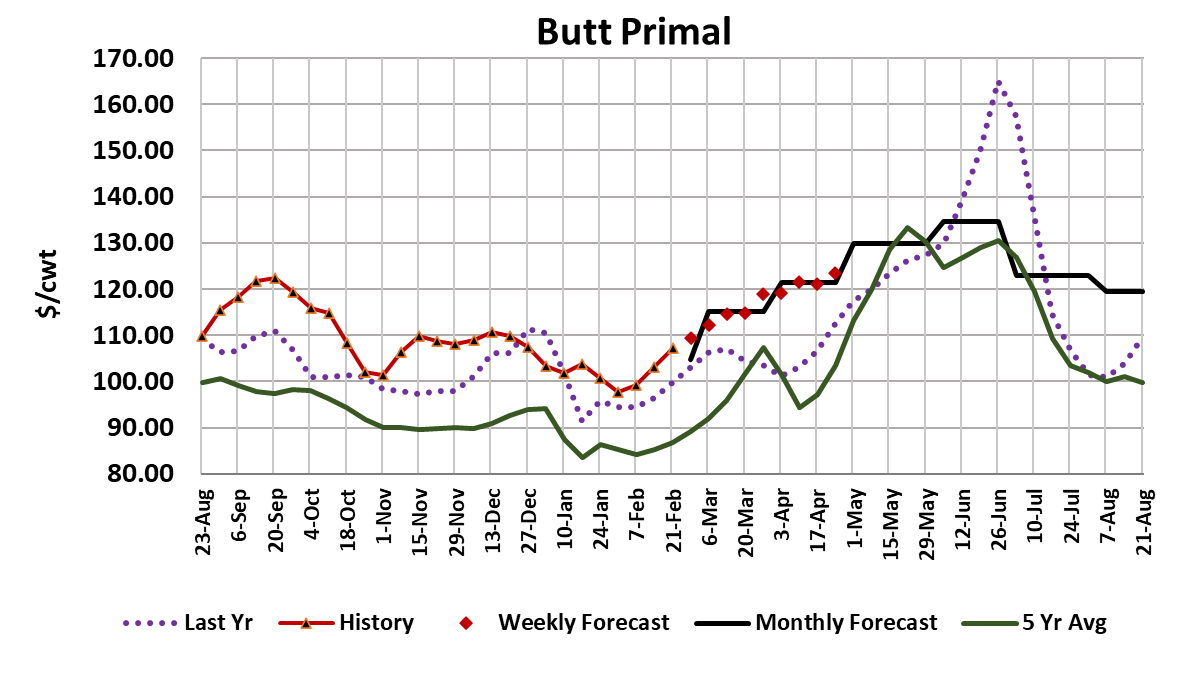

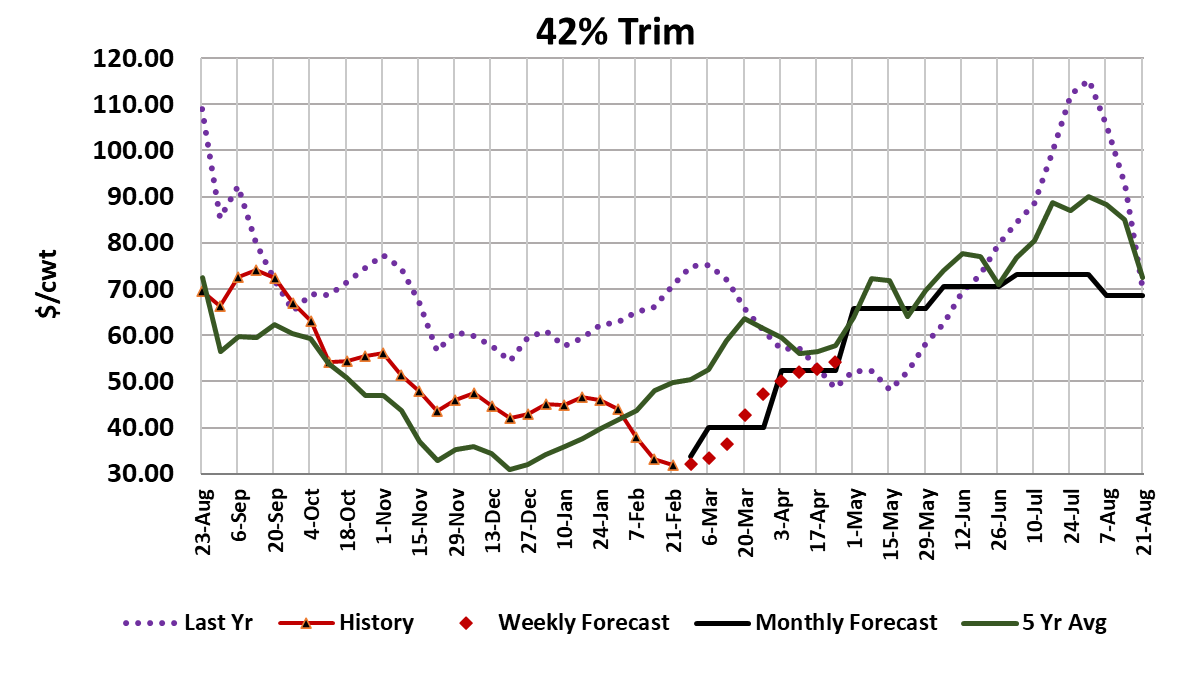

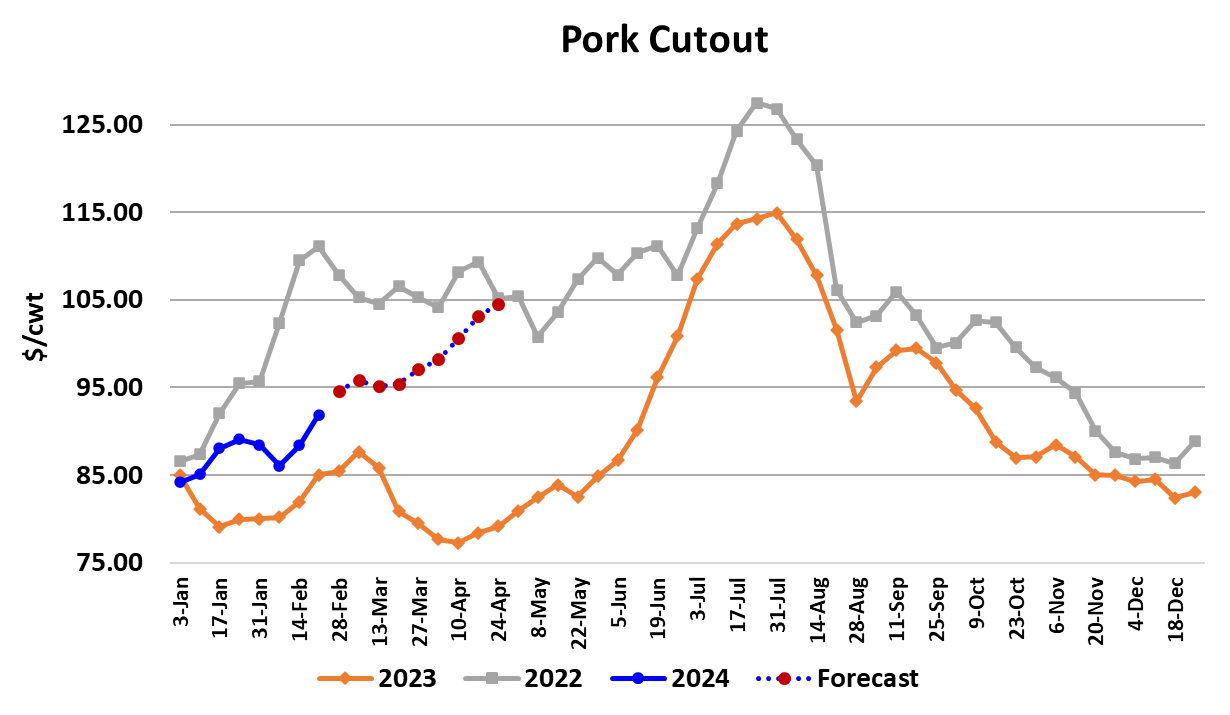

It was a trifecta week in the US hog and pork complex—the negotiated markets move up a little over $3, the LHI gained a little over $3 and the pork cutout moved $3.49 higher on a weekly average basis. The only one that didn’t join the “three club” was the nearby LH futures, which only added $2.63 on the week, but that can be excused because the futures had already put in a substantial upward move the previous week. This week’s gains were a little stronger than what we’ve seen in the recent past, where the cutout has inched up a dollar or so each week, with periodic dips. In fact, I have to go all the way back to the week of Labor Day to find an instance where the cutout gained more than it did this week, and that’s not even a fair comparison because it was a major holiday week. So, there is good reason for this week’s optimism. Of course the important question is whether or not the market can sustain and perhaps even build upon its newfound strength. I think it is possible. The fundamental forecast has the cutout gaining roughly $3 again next week before cooling back down to a more measured rate of increase. Pork demand appears to be on the mend and kills are beginning to lighten up seasonally, so there is solid fundamental footing for expectations. The combined margin easily cleared the zero line this week for the first time since mid-October, indicating that improving demand is generating more margin to be shared among the supply chain segments. Further, all of the retail primals saw solid price increases this week and both the hams and bellies were strongly higher. Trim is the only part of the carcass that isn’t in an uptrend. Trim demand will get a strong boost as baseball season approaches and hot dog manufacturing gears up. Besides, trim only contributes a small amount to the overall cutout value anyway. This week’s slaughter tallied 2.58 million head, up about 20,000 from the week before but now solidly below the 2.6 million head level that has dominated non-holiday weeks since October. Next week will mark the end of the Dec/Feb quarter and the early estimate has next week’s kill at 2.54 million head. Of course, even that will still be overkilling the Jun/Aug pig crop and the cumulative overkill for the quarter is going to be close to 1 million head. The future is looking brighter however, as sow slaughter during this quarter is currently about 40k head stronger than the Dec 1 inventory would suggest and that means that producers are culling at fairly strong clip. A 40k over-kill on sows might not sound like much, but if you consider that each sow might produce as many as 22 piglets per year, then we are taking almost 900,000 finished hogs off of the table that would otherwise be burdening the market. Of course, we don’t yet have any insight into how many gilts are being redirected back into the breeding herd, but the big over-kills would suggest there is a strong parade of gilts going to slaughter also. So producers appear to be setting the table for better times ahead. I calculate producer margins at -$13/head currently and at the rate things are going, they could see positive margins by mid-March. In fact, the current forecast has them at +$30/head by early May. Will the return of positive margins derail efforts to make significant reductions to the breeding herd? It could, but I’m hopeful that producers have learned enough hard financial lessons over the past couple of years that they will stay the course. Barrow and gilt weights were reported down a pound this week at 214, but that is likely just noise in an otherwise sideways pattern that weights are expected to be in for the next couple of months. The real seasonal trend lower isn’t likely to materialize until mid-April or later. Export demand appears to be on good footing, but it’s impossible to know for sure since the weekly export data seems to have been out of kilter lately. I’ve got per-capita pork consumption averaging about 2% below last year in the first half of 2024 and if that comes true it will be price supportive. Combine that with 5% improvement in demand over last year’s dismal first half and the potential for much stronger pricing seems to be in the cards. Of course, we must keep in mind that pork demand is prone to hitting an “air pocket” out of nowhere and it seems that the March/April timeframe has a propensity for that, so that is something that market participants need to be aware of. I am a little surprised that the summer futures haven’t taken more of a leadership role in this recent rally. The Jul contract settle just a bit over $100 on Friday, but that doesn’t seem like enough for a market where demand is in recovery and supply will soon shrink seasonally. Fundamentally, it is easy to justify $107 or so for July hogs and $112 for the cutout. May futures also look abnormally undervalued. There is currently a $12 gap between Apr and Jun, and the May is only positioned $3 over the Apr, suggesting that traders expect most of the price gains will occur after May expires. I would argue that May would be better positioned near the middle of the Apr/Jun spread. Next week, expect further gains in both the negotiated markets and the cutout. The ham market will be key—if it can build on the momentum it established this week then another solid gain in the cutout is likely.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}