Pork Wrap February 2

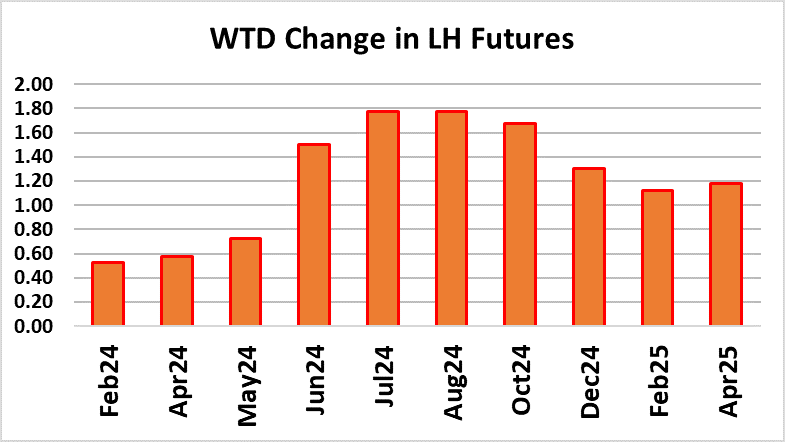

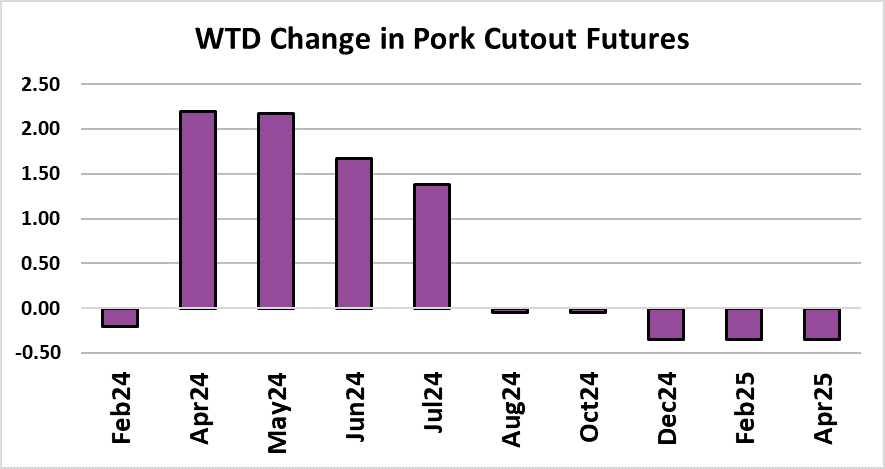

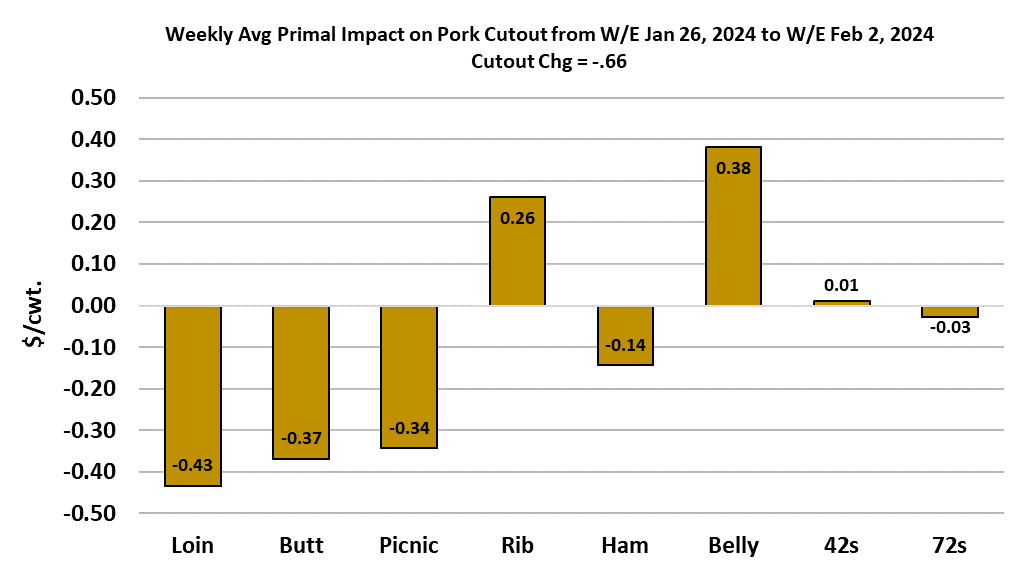

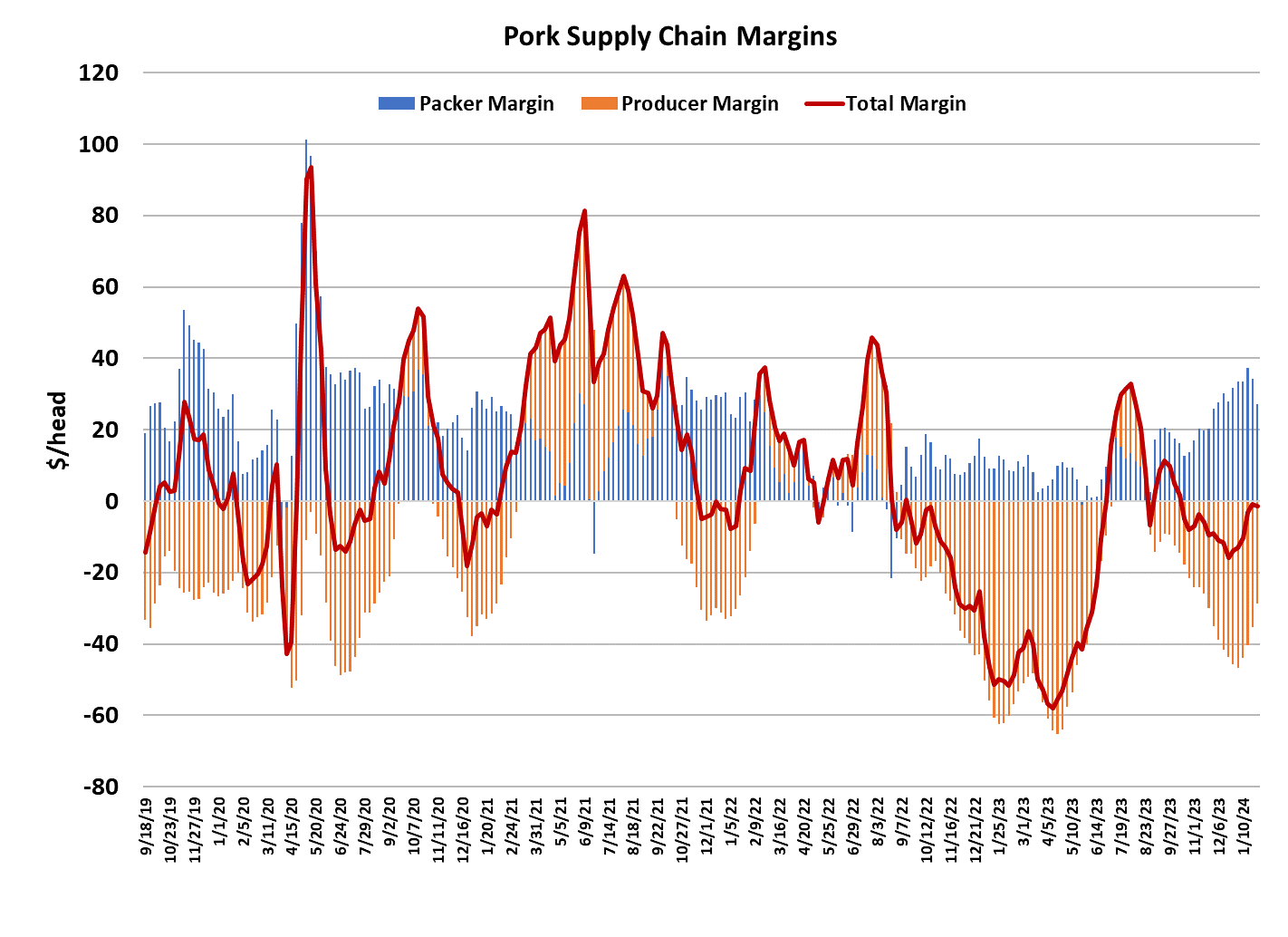

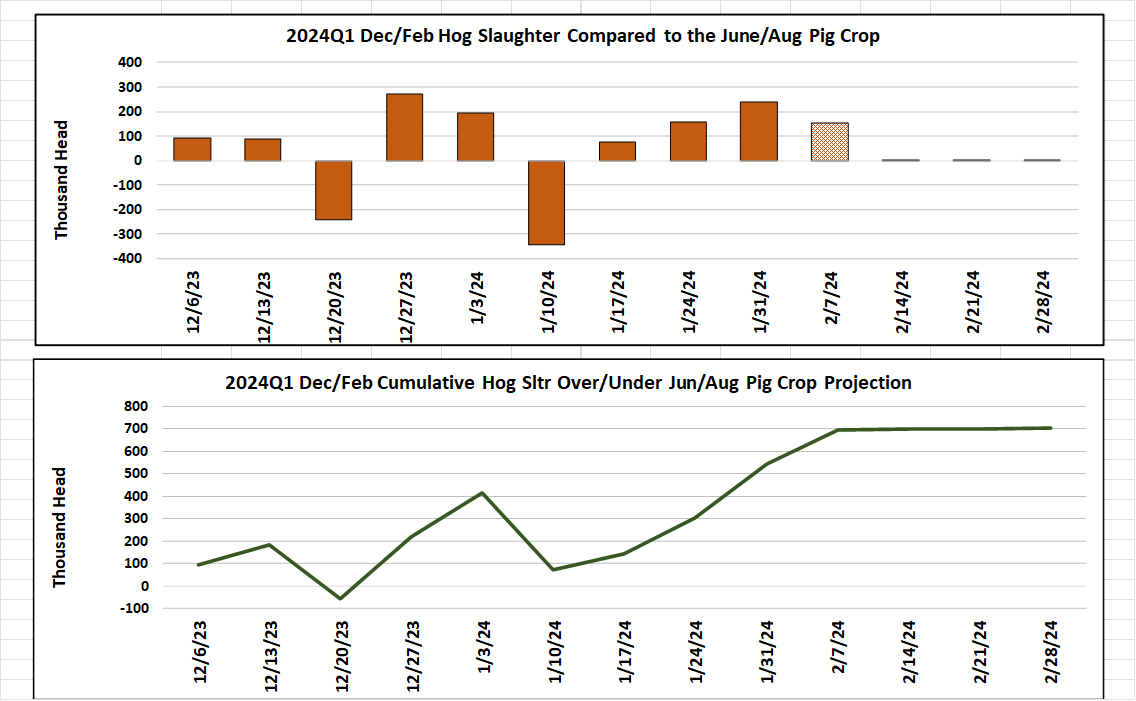

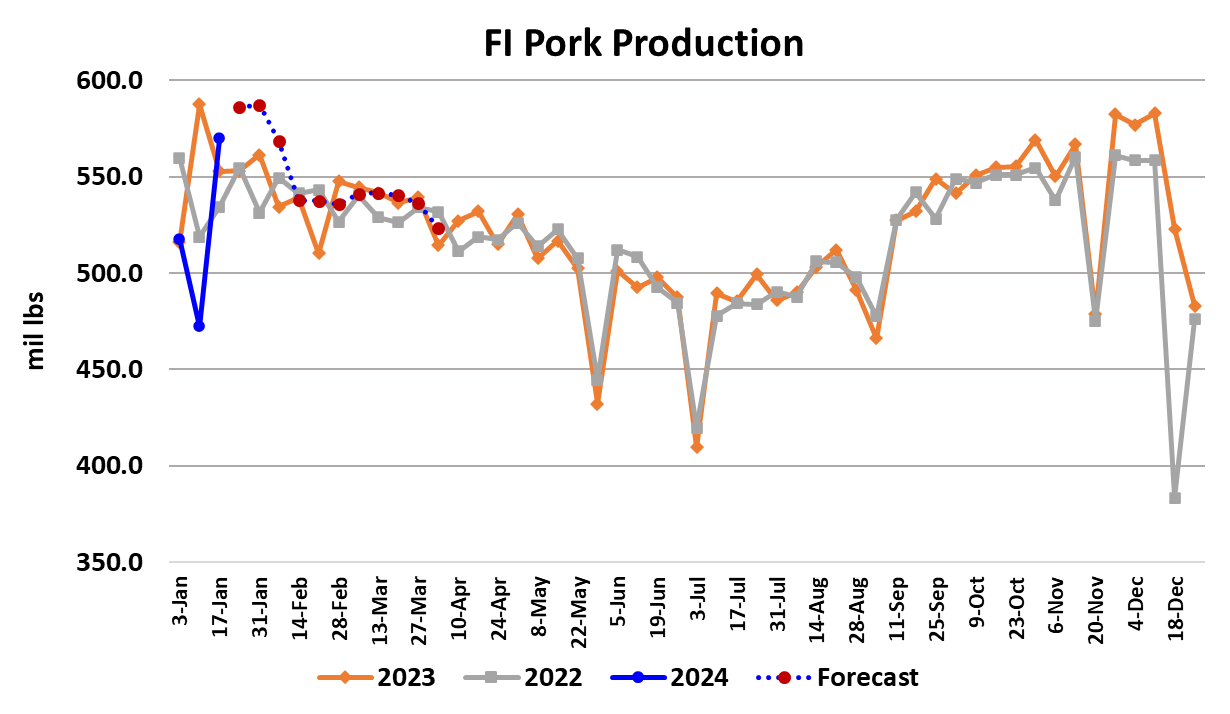

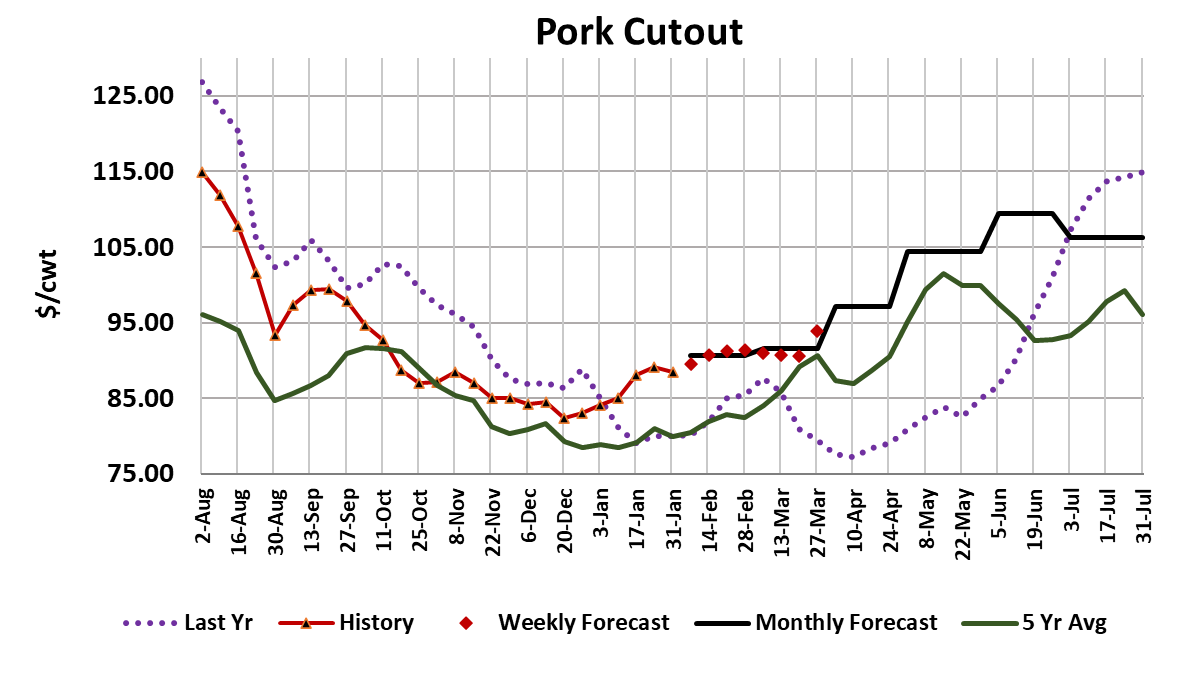

Pork packing margins are shrinking rapidly, dropping from $37/head two weeks ago to $27/head this week. The problem for packers is that hog prices are rising while the cutout remains stuck in the upper 80s. This week the WCB negotiated base price added $9.58/cwt. on a weekly average basis, while the pork cutout lost $0.66/cwt. in averaging $88.43. Of course, $27/head is still a very good margin, but the rate at which it has eroded is impressive. Last year at this time, packer margins were only $12/head and the five-year average for the first week in February is $18/head. Margins are still plenty healthy enough to keep packers interested in killing every hog they can get their hands on. This week’s slaughter clocked in at 2.69 million head and it looks like packers are gearing up for about a 2.63 million head kill next week. That results in a lot of pork that needs to be marketed, but so far the market has handled these big volumes without much trouble. Pork production this week is estimated at 587 million pounds, up 4.6% from last year. At the same time, the pork cutout is 10.5% stronger than this time last year. That implies much better demand this year compared to last. The attached chart shows that we are still badly over-killing USDA’s revised estimate of the Jun/Aug pig crop. That overkill is now estimated at 700k head and is likely to challenge 1 million head before the end of February. Still, kills should start to ease seasonally lower as we move through February and that bodes well for the cutout. It won’t rocket higher, but I expect the cutout to trade over $90 within a couple of weeks. This week, the retail primals were down slightly while the rib and belly primals exerted a small positive influence on the cutout. Actually, the changes were pretty small in all primals on a weekly average basis, so it is more like everything is just treading water. The combined margin ticked a little lower this week as the losses in the packer margin slightly outweighed the gains in producer margins. I don’t think that the downturn is large enough to indicate that a top is being put in, but it does bear close watching. The US economy seems to be hitting on all cylinders here in Q1, with stock indices regularly hitting all-time highs and unemployment remaining low. Inflation seems to be fading fast also. That should be supportive to pork demand and may at least partially explain why demand is running hotter this year compared to last. It looks like the industry may escape the super-weak demand environment that took hold last year in Q1. Given that the pork cutout was essentially treading water this week, it isn’t surprising that the front end of the futures curve also finished the week nearly unchanged. The summer contracts however, put in stronger gains, perhaps reflecting optimism that this year will not be as bad as some may have initially thought. Even last year, after a horrible spring price-wise, the LHI reached $106 near the end of July. Traders may be breathing a sigh of relief concerning the demand side at the moment, but they are still likely harboring concerns about the persistently large slaughter volumes and the apparent inability of producers to rein-in production. That is a very real concern. It seems a given that USDA will report the breeding herd down again in the March H&P report, but the wild card is productivity. As we’ve seen in the past couple of reports, super-strong productivity has easily swamped the breeding herd reductions that producers offered. Until traders can see some evidence of meaningful reduction in the productive capacity of the hog sector, they are probably going to remain reluctant to price the 2024 summer contracts over what we realized in 2023. The Lenten season is just around the corner, with Ash Wednesday coinciding with Valentines Day this year. That could temper demand just a tad, but doesn’t seem to have as big of an impact in current times as it did a few decades back. One thing to keep an eye on is the belly market, which made a top last year just after the Feb contract expired and then trended lower into Apr expiration. That move was counter-seasonal and doesn’t seem likely to repeat this year, but it could become a concern for some traders as Feb expires and they shift their focus to Apr. I have the belly primal holding in a sideways pattern for much of Feb and March, and believe that the risk is that bellies could outperform the forecast. The normal seasonal for hams has them moving higher from here, so it may be that primal that takes over leadership in moving the cutout upward as we head toward spring. Next week, watch for further gains in negotiated hog prices and perhaps even a dollar or so increase in the cutout if hams can get some traction. Feb futures will expire a week from Wednesday and it appears that the LHI is tracking toward an expiration in the $75-77 range.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}