Pork Wrap February 18

Cash hog prices continued higher this week as the WCB negotiated

market was up $5.80 on a weekly average basis and the National

negotiated market gained a little over $8. Those gains were enough to

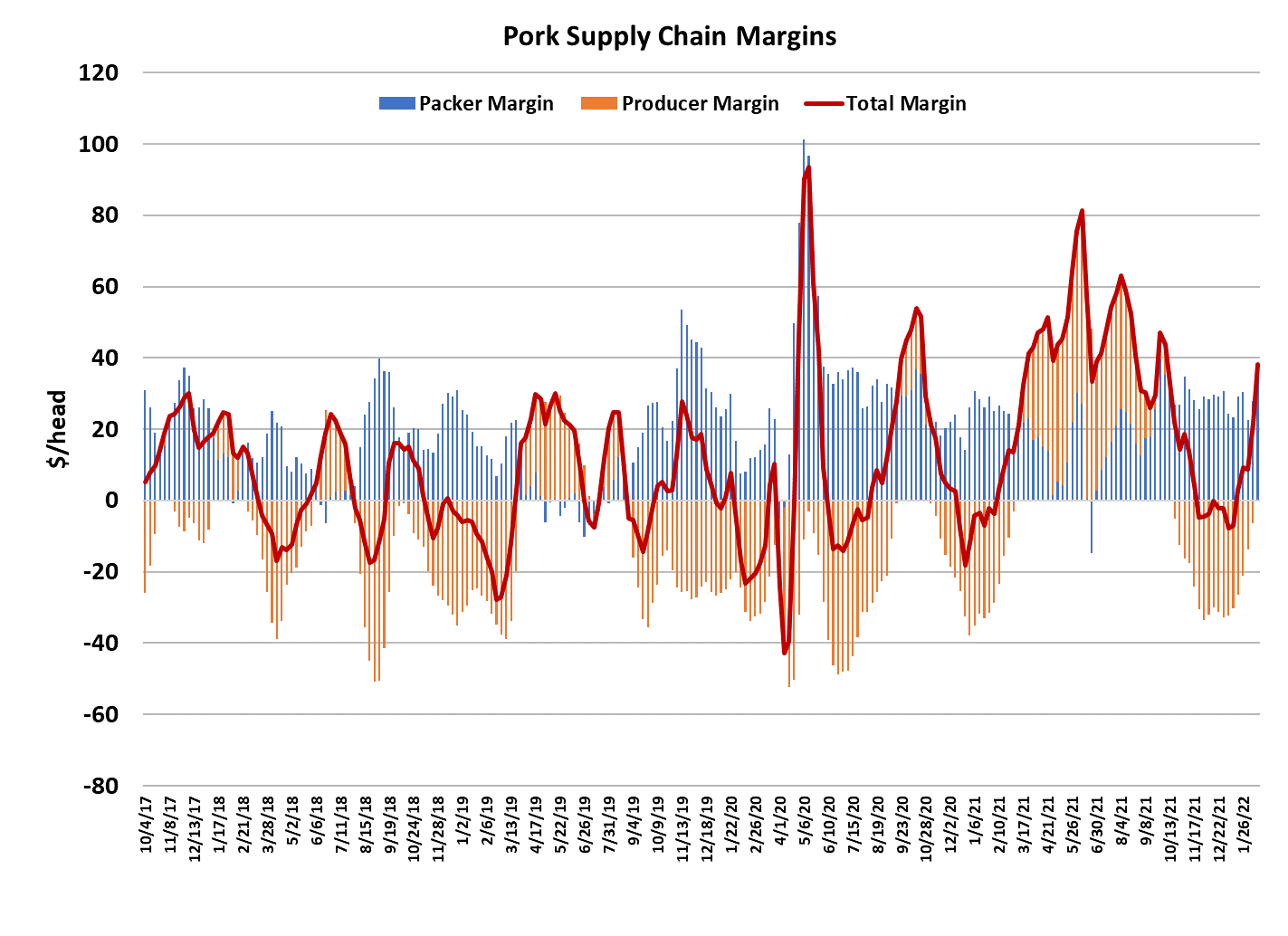

push producer margins into positive territory after over three months of

being deep underwater. Packers could afford to pay those high hog

prices because the prices they were receiving for pork increased. The

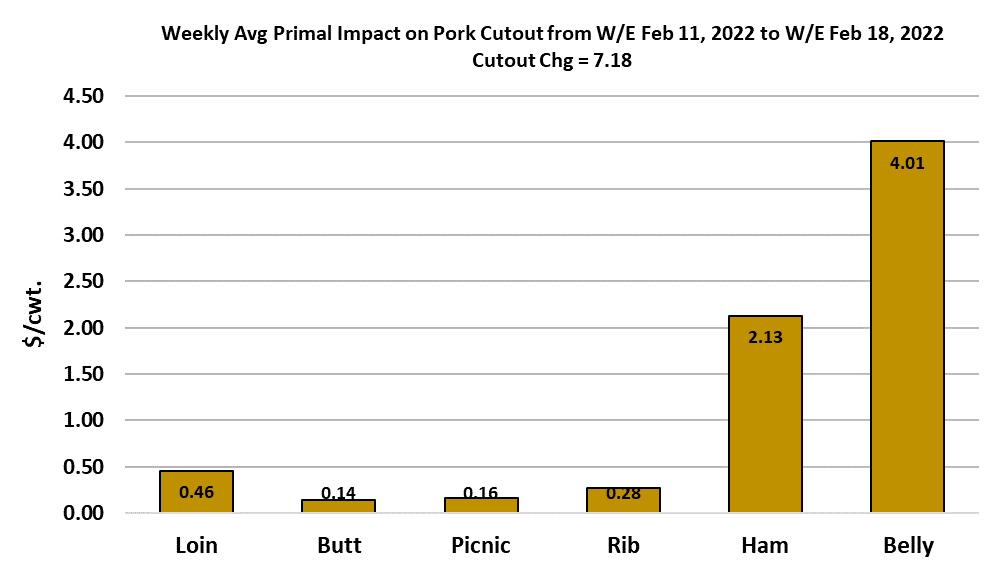

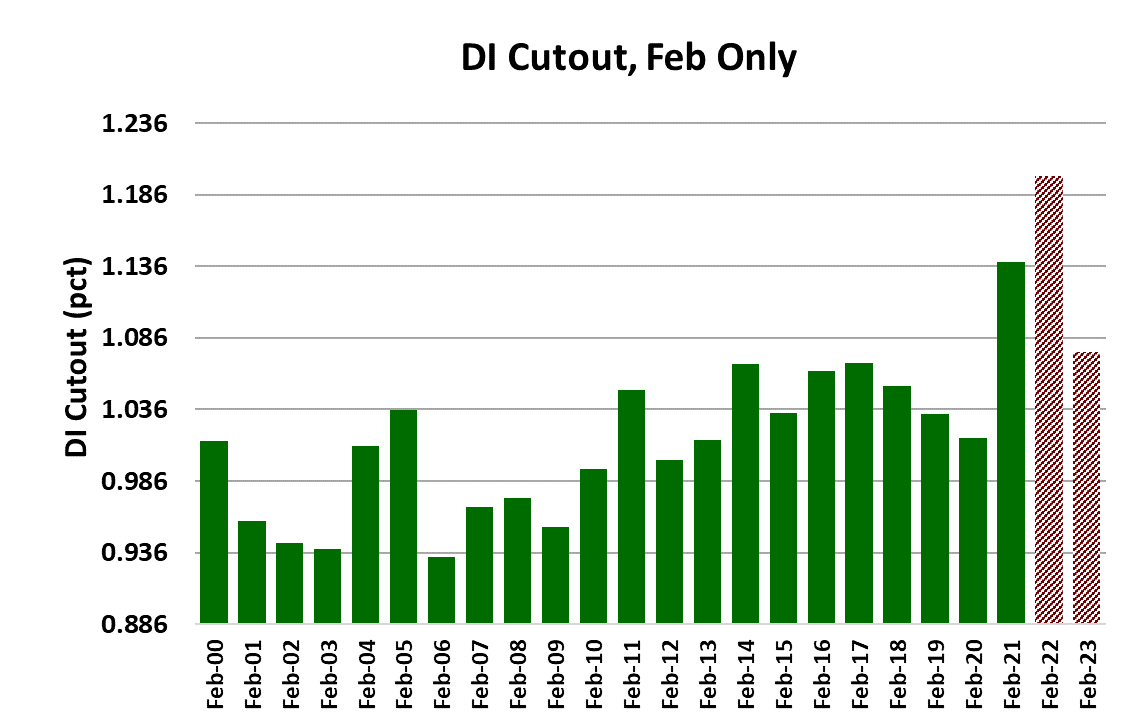

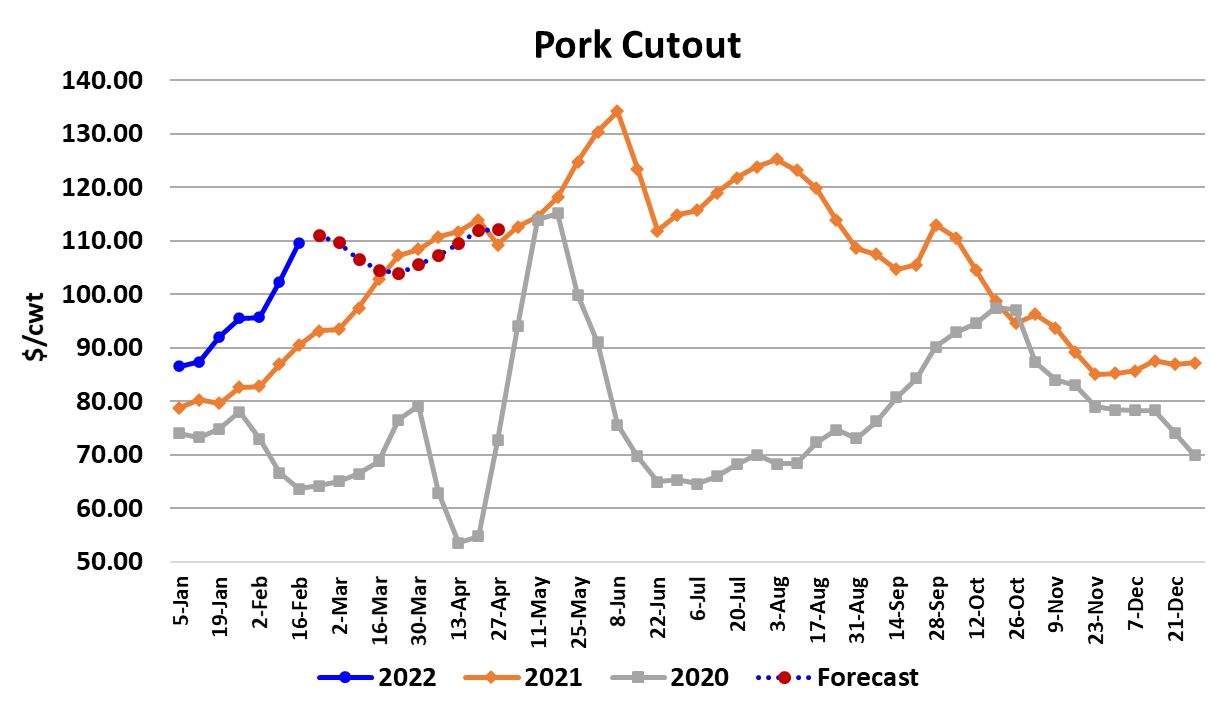

cutout gained $7.18 this week to average $109.53. Triple digit cutouts in

February are pretty rare and it’s even rarer to see triple digit hog prices,

but that may be where we are headed very soon. The LHI is currently

poised to reach $97 early next week and expected to average over $101

by the time next week is done. Packer margins remain very healthy, with

this week’s margin estimated to be over $31 per head. As a result,

packers are eager to push the kills higher and not afraid to pay up for hogs

if they have to. This week’s slaughter clocked in at 2.51 million head, just

a hair smaller than last week, but still about 90k stronger than what the

Jun/Aug pig crop implied.

Next week is the end of the Dec/Feb quarter and it looks like the industry

will have over-killed USDA’s estimate of the prior pig crop by about 500k.

I guess it is a good thing that the hog supply was larger than advertised

over the past few weeks or else price levels likely would have surpassed

the eye-popping levels that we are currently experiencing. Barrow and gilt

carcass weights declined another pound this week and seem to be

behaving in normal seasonal fashion. Both kills and carcass weights

both should plateau for the next several weeks and thus hold pork

production relatively steady around 535 million pounds per week. Toward

the end of March, both kills and carcass weights should start to move

seasonally lower and by the time we get to mid-May pork production will

likely only be about 500 million pounds per week. That would be about

3.3% below last year’s production level, but keep in mind that exports

aren’t likely to be nearly as strong as what we saw last year, so that will

help to offset some of the YOY production decline. When we get into the

summer months, the industry will be slaughtering the Dec/Feb pig crop,

which USDA hasn’t reported yet, but my estimate is that it will be about

1% larger than last year.

In all, the supply side of the market looks a bit tighter than last year, but

not excessively tight, particularly as we move deeper into spring and early

summer. It is the demand side that is causing most of the headaches

right now. I estimate that the cutout demand index for January was 1.09,

up about half a percent from last year and the February demand index is

close to 1.2, up 5.2% from last year. Just to put that 1.2 February demand

index into perspective, prior to 2021 the highest February demand index

on record was 1.07 in 2017. So, this is by far the strongest February

demand environment ever seen. That is why the cutout is brushing up

against 110. f course that begs the question, “Why now? Why is demand

suddenly so strong for pork?” I suspect that it is related to consumers

climbing back down the protein ladder and trading out of beef and into

pork as their pandemic savings dwindle and high prices on everything

else in the economy gobble up any extra disposable income they might

have

If that theory is correct, then this demand strength isn’t likely to last a

long time since consumers will eventually move down from pork to

poultry. The one caveat to that is that the poultry sector is nervously

watching the spread of avian influenza right now and that has the

potential to disrupt things for all animal proteins. If the bird flu spreads

widely to commercial broiler operations, then massive depopulations

will be necessary and that will seriously limit broiler production, raising

prices and thus supporting pork demand. On the other hand, if it

doesn’t spread widely but it does cause our trading partners to ban US

poultry, then there is the risk that poultry prices plummet in the US as

we try to clear a lot more chicken through domestic channels that would

normally have gone overseas. That would hurt pork demand. And

finally, if a “bird flu epidemic” starts to be reported in the popular press it

can depress consumer demand for poultry and thus boost beef and

pork demand. So, there are a lot of different angles to the avian

influenza story that we need to keep an eye on in the coming weeks.

This week it was big gains in both the bellies and hams that drove the

cutout higher, with only a small amount of help from the retail primals.

That tells me that the demand surge is coming primarily from the

processing sector. Belly slicers are probably ramping up production in

order to fill increasing orders from foodservice as the pandemic wanes.

Americans will likely travel in record numbers this spring and summer

after two years of not being able to travel safely. That should drive

consumption through the foodservice channel higher and a lot of bacon

is used in foodservice applications. With the hams, I think we may be

seeing signs that more boning labor is becoming available because the

amount of hams sold bone-in over the last few weeks seems to be

down from where it was back in Q4. When processors are able to

debone more hams, thus adding value to them, the price level for the

ham primal should be generally higher. We should watch trimmings

prices closely because as more deboning occurs, that should increase

trim volumes and thus drive prices lower. So far that hasn’t happened

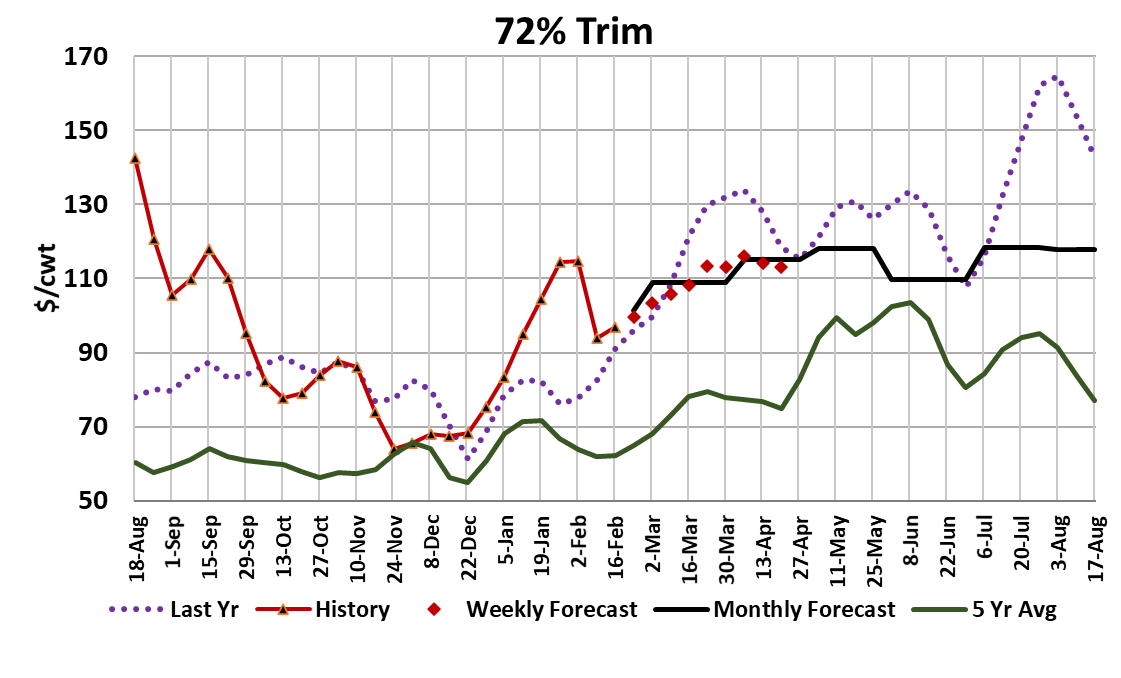

to a large degree. 42s have been trending solidly higher since mid-December and likewise for the 72s, except for a sharp drop two weeks

ago.

This week, the 72s regained their footing and added about $3/cwt.

Futures traders have been busy buying the futures curve with both

hands. The Apr contract has gone from about $86 in mid-January to

over $109 today. That’s $23 gain in a month is astounding. Shorting

this market has been like standing in front of a runaway train. Those

that have tried it probably don’t want to do it again anytime soon. The

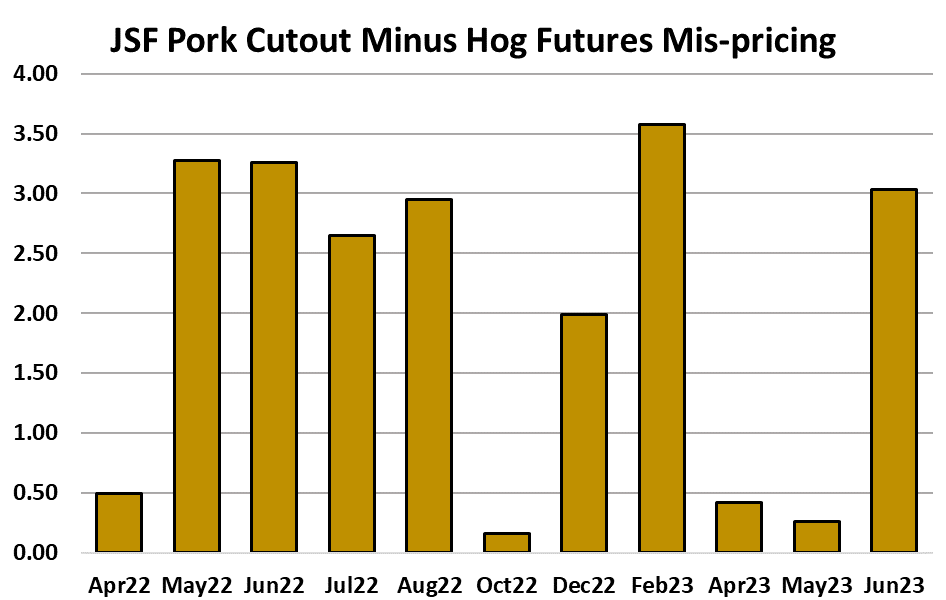

mis-pricing chart shows just how inflated the futures curve is now

relative to my read of the fundamentals. Once the demand side of the

market cools down however, a good bit of the recent strength in the

curve is likely to get removed. Next week, watch the bellies and hams,

those have been the primary price drivers. Keep an eye out for news

on avian influenza because that has the potential to become a big

market disruptor.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}