Pork Wrap February 17

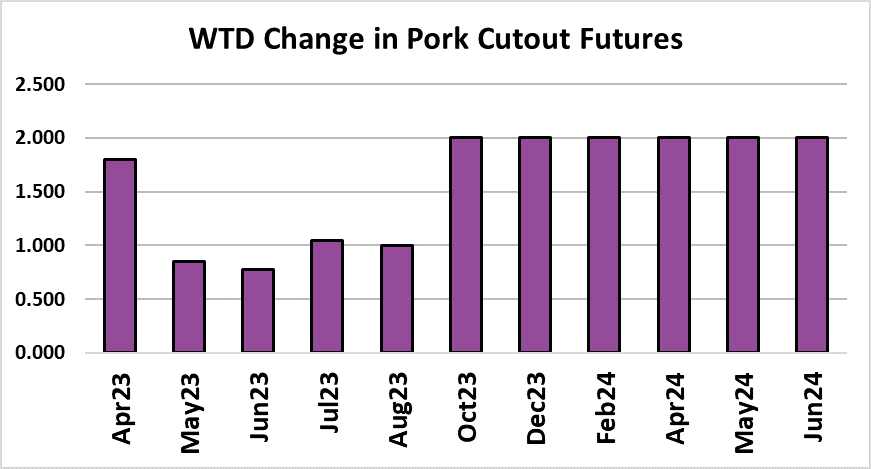

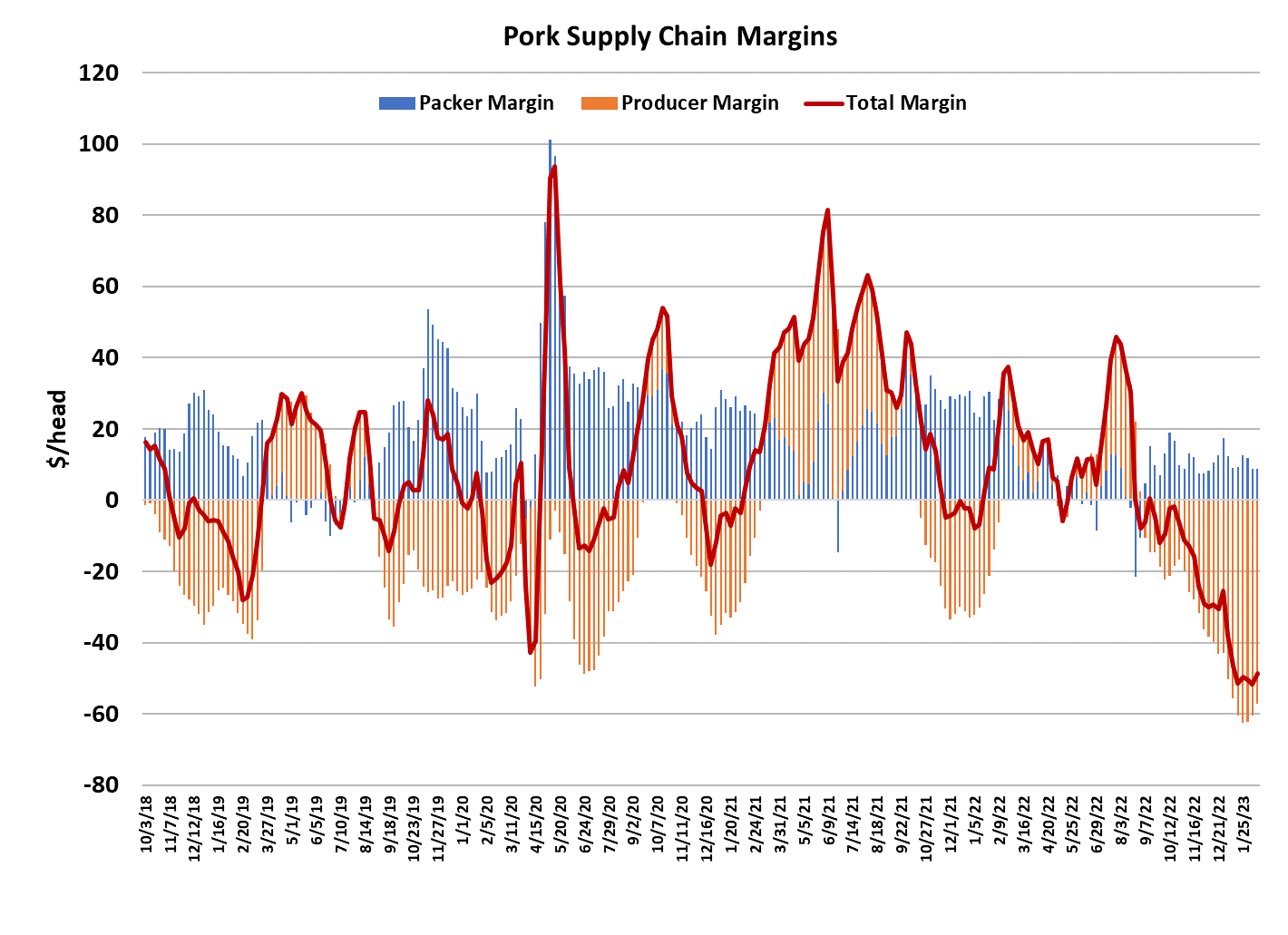

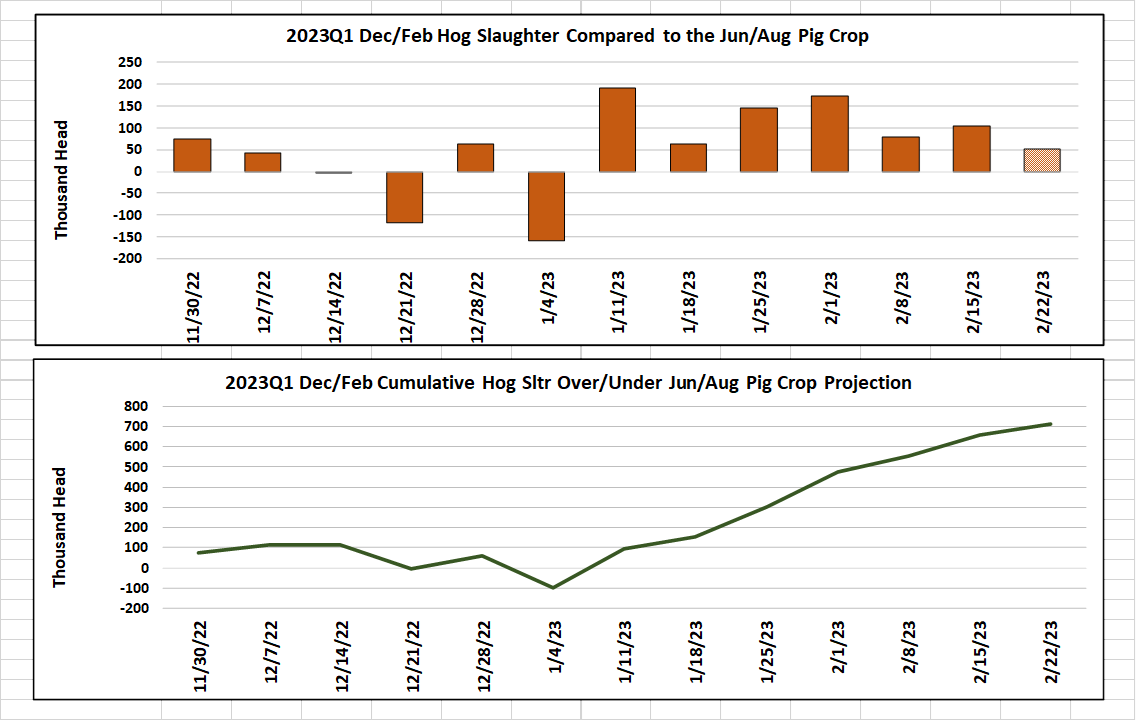

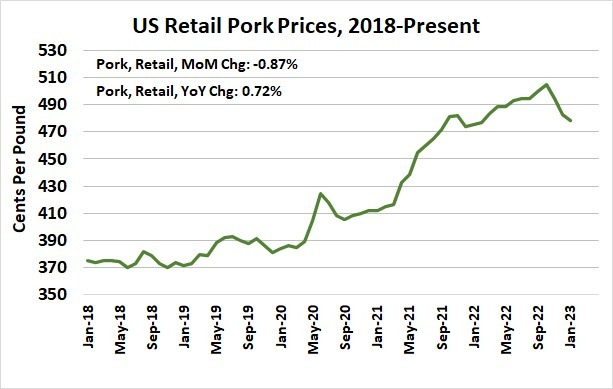

The pork market gained just a bit more upward momentum this week as the cutout averaged $81.94, up $1.76. However, the negotiated hog markets did not gain nearly as much as they did the week before. The WCB negotiated price added only $0.94/cwt this week and the NDD market was up $0.78. Packers probably made a conscious decision not to press the kill too hard amid signs that the availability of cash hogs is tighter than it was a few weeks ago. Packer margins rang in at $8.75/head, up only very slightly from last week. Margins are still very low for this time of year and packers must surely recognize that they need to keep a light hand on the kill throttle or risk running the cash hog market up and thus damaging their precarious margin situation. Pork packers seem to be more adept at that than beef packers have been. Still, I don’t expect that we are going to see packer margins much over about $10/head for the next couple of months. After that, hog supplies will start to tighten in earnest a that probably implies packer margins in the low single digits during late spring and summer, with a very real possibility that they could see some long stretches of negative margins in that timeframe. Bellies led the price gains this week, but all of the primals were up to some degree. That makes me think that this week’s small gain was mostly a function of last week’s lighter production rather than any substantial improvement in pork demand. The combined margin ticked a little higher but still seems stuck at a very low level. USDA reported the average retail pork price during January at $4.79/pound. That was down a little from December, but still higher than last year. I think that we can expect the next couple of prints on that retail price data to continue to show softening retails. Beef and chicken wholesale prices seem to be moving upward faster than pork at the moment, so that should give some incentive for retailers to shift their ads in pork’s direction over the next few weeks. Perhaps that will help jump start this pork market that has been somewhat like watching paint dry so far in 2023. Of course, slow moving markets like that are not very appealing to futures traders. The Feb contract expired this week just a bit under $76, but the LHI hasn’t moved very much since then. Apr has traded between $85 and $88 since Feb expired, and that is a pretty big premium for a market where the underlying cash prices aren’t moving much at all. I expect that traders will begin to fade Apr lower to tighten up the basis somewhat in the next couple of weeks, but that slow easing is likely to be punctuated with sharp jumps higher every time the cutout or negotiated market shows signs that it might be waking up from its slumber. The fundamental forecast has fair value for the LHI at Apr expiration around $89, but my sense is that target will need to be lowered in coming weeks due to lack of movement in the underlying. This week’s slaughter came in at 2.51 million head, up about 20k from last week. Next week should closer to 2.45 million head with a light Saturday and some slight pullback on Monday’s kill due to the Presidents Day holiday. Still, the attached chart makes it clear that the industry has been over-killing the Jun/Aug pig crop since early January. It looks like the pig crop estimate may have been about 700,000 head too small. That raises the risk that when the March/May quarter arrives we will be seeing weekly kills larger than the 2.4-2.45 million head per week that the Sep/Nov pig crop suggested. Barrow and gilt carcass weights were steady this week at 215 pounds and are likely to hold in the 214-215 pound range for a few weeks unless packers develop an urge to pull harder on the hog supply than they have recently. USDA will give us another Hogs and Pigs survey on March 30 and I expect that it will show the breeding herd has been reduced from what they reported in December (but still larger than last year). Producer margins have been absolutely dismal since about October as the orange bars on the combined margin chart indicate. High corn prices bear a lot of the responsibility for that and, while the long-run outlook seems to support lower corn prices, in the near-term they could go higher as uncertainties begin to build ahead of the growing season. That means probably 4-6 more months of high corn prices and poor producer profitability, which might just be the straw that breaks the camel’s back and forces some producers to exit the industry. It isn’t very likely that super-strong demand like we saw during the pandemic will bail out producers this year or next. If producers shrink the herd then less hogs means less need for packing plants and it wouldn’t be surprising to see some of those go dark next year. At times exports have rescued the industry, but it doesn’t look like 2023 is going to be a stellar year for exports either. It is hard to see anyone in the pork supply chain that is going to be very happy this year, outside of perhaps retailers. Consumers sure aren’t happy with the prices they are seeing, packers are having to make do with much smaller margins and producers are deep in the red. Even futures traders are probably not happy with the super-sedate cash market fundamentals. It must be February. Next week, watch for some further drying of the paint.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}