Pork Wrap February 16

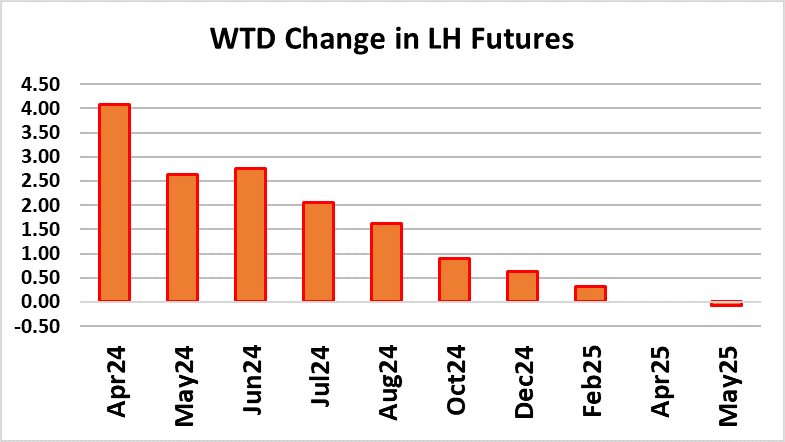

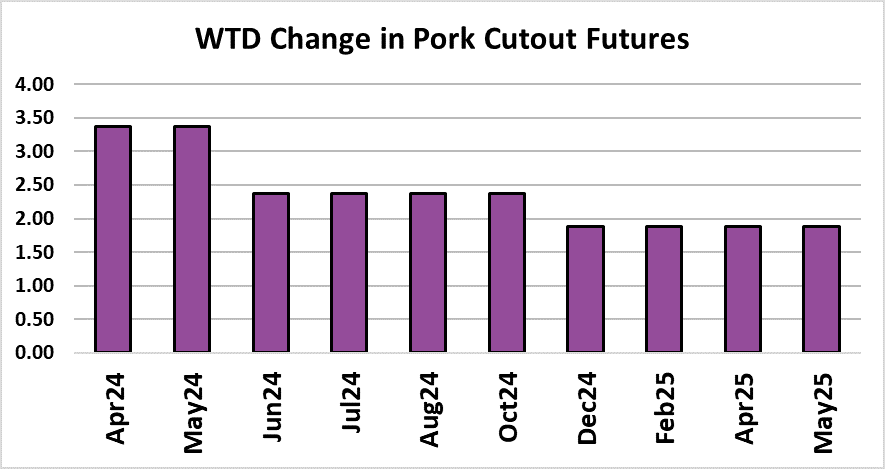

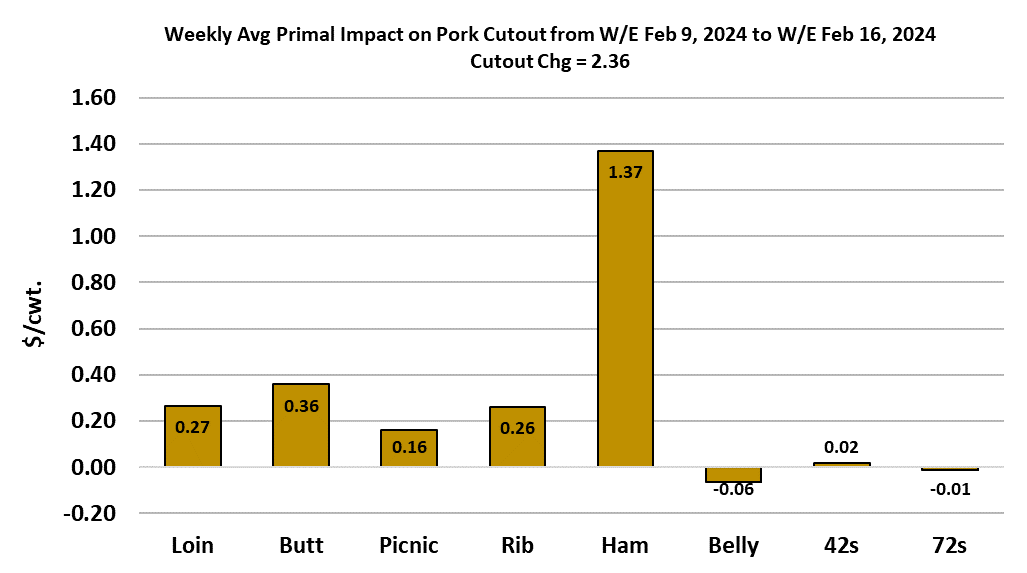

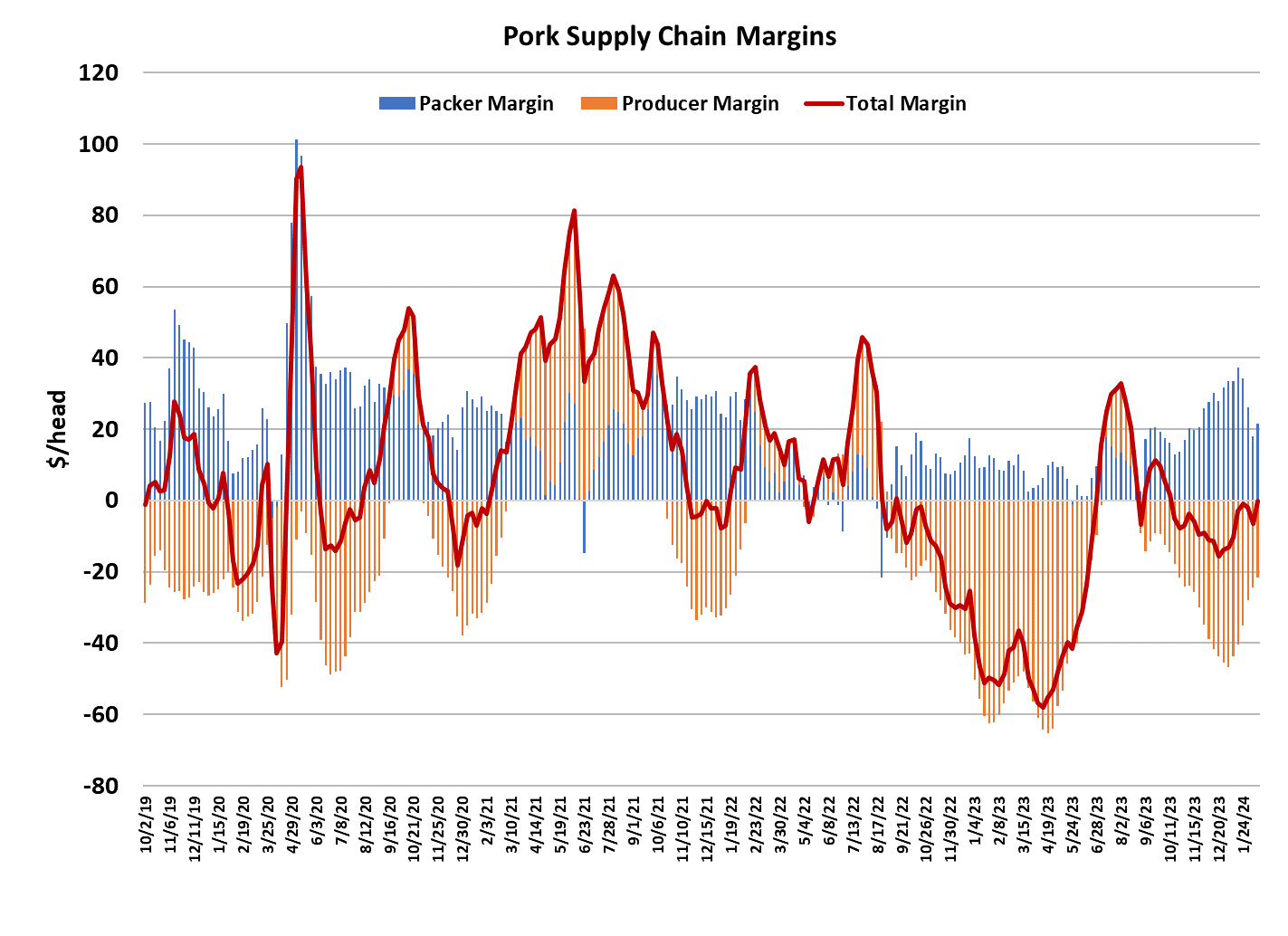

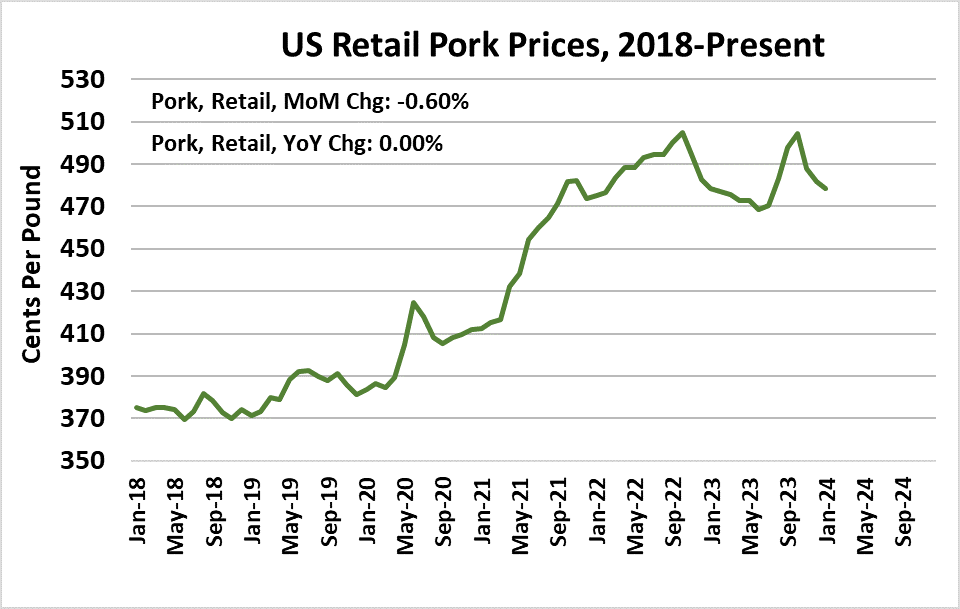

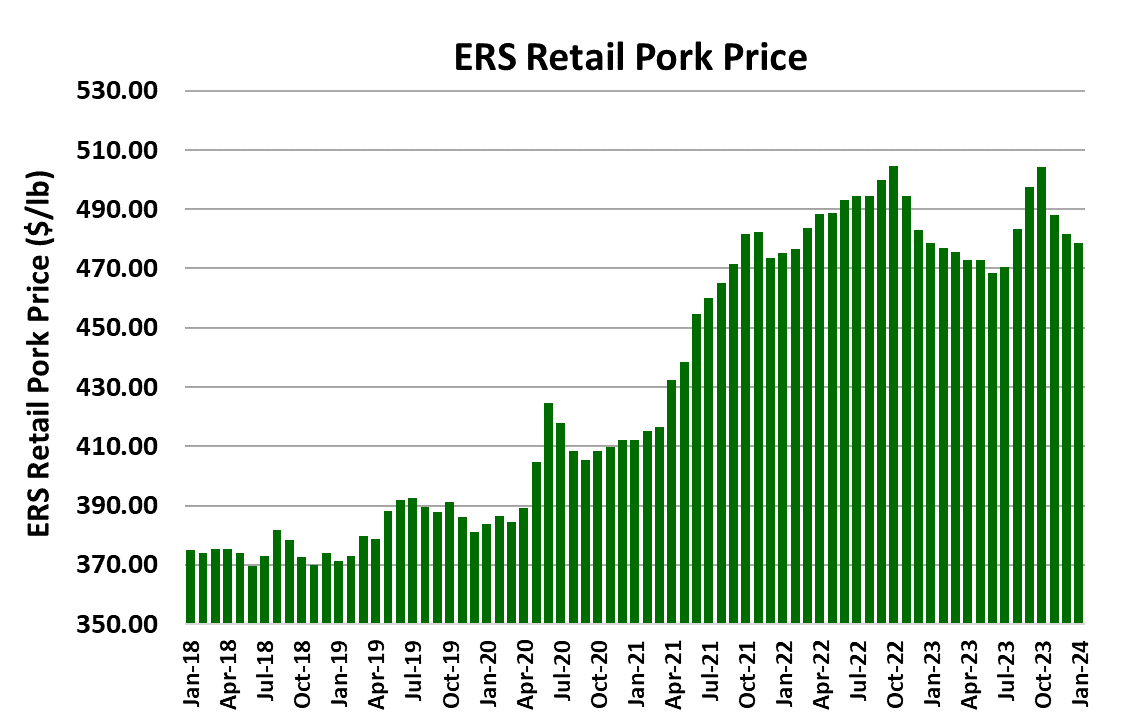

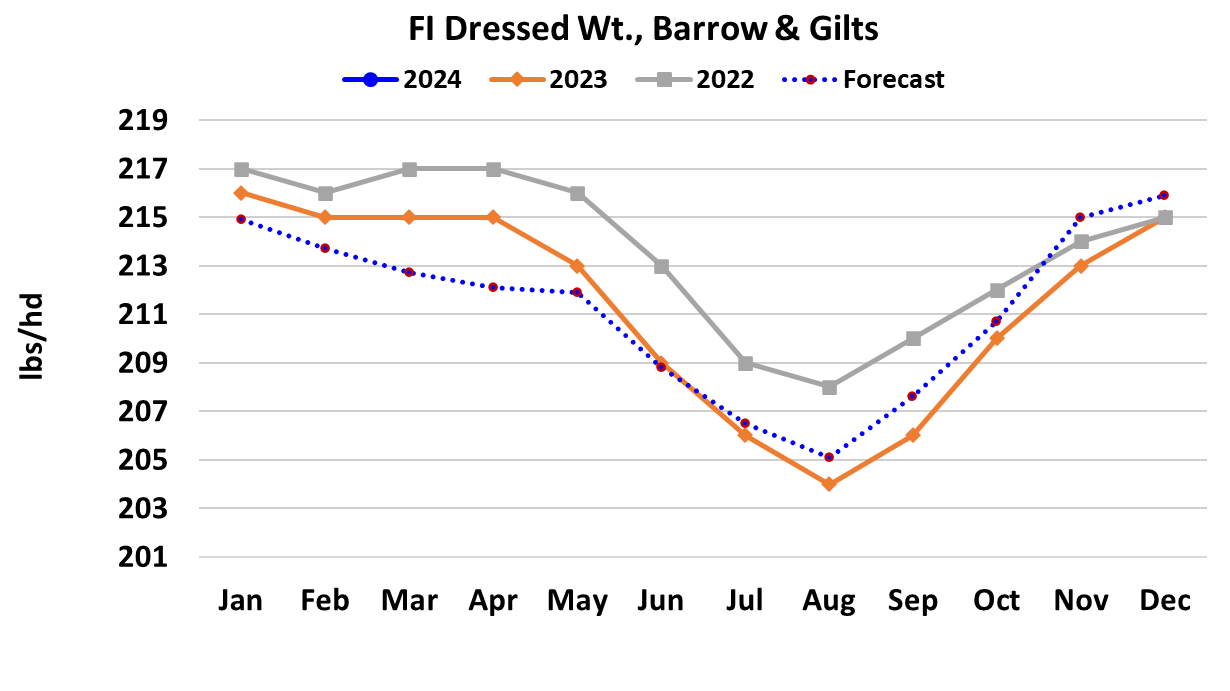

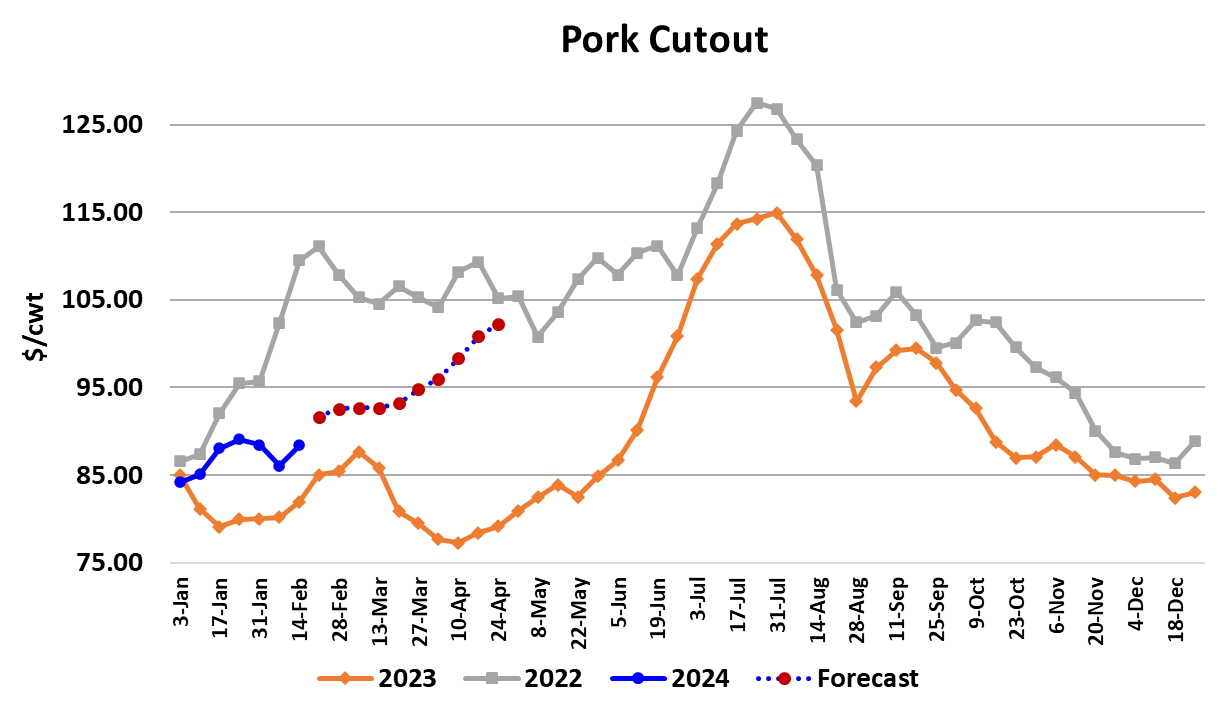

The hog and pork complex resumed its upward push this week as the cutout gained $2.36 to average $88.39/cwt. and the WCB negotiated market added $3.47 on a weekly average basis. Friday afternoon, the cutout broke above the $90 level for the first time since early October. That helped to inspire confidence in the futures market, and the Apr contract added a little over $4 on the week. Feb futures expired at $75.12 on Wednesday. Earlier this year, traders seemed to be concerned that demand softness and big hog supplies would cause price levels to soften in late winter, much like we saw last year. That fear seems to be rapidly dissipating and with the cutout now over $90 in mid-February, it makes one wonder why the summer futures are still trading below the $100 mark. This week’s boost in the cutout was largely driven by the hams, but the retail items also pitched in. Toward the end of the week, bellies started to firm also. All of the major primals are now trending higher except the bellies and it looks like they may be starting a new uptrend. That would leave the trims as the only items that are still solidly in a downtrend. Given how large production has been recently, the price gains that we saw this week seem to be pointing toward some improvement in demand. The combined margin turned back higher this week and looks poised to enter into positive territory after tracking below zero since September. There is also some help coming on the supply side as weekly kills should start to ease lower from now until they put in their annual bottom in late June or early July. This week’s kill was reported at 2.56 million head—the first non-holiday kill below 2.6 million head since early October. It is really starting to feel like the hog and pork complex is now slowing turning the corner, leaving the big supply/low price environment of winter behind and gearing up for the tight supply/high price environment that dominates in summer. Of course, this week is just one baby step in that direction and we should still have ample pork availability in the near-term, but if demand is truly improving as supplies are slowly shrinking, then that provides cause for optimism that last year’s spring price disaster won’t be repeated this year. FI barrow and gilt carcass weights were reported steady at 215 pounds this week and are dead-on with last year’s level. Expect carcass weights to track mostly sideways through February and March before starting their seasonal trek lower in mid-April. Packer margins have come down a lot in the last three weeks, but are still above $20/head and that provides plenty of incentive for packers to kill every hog they can get their hands on. As a result, hog producers are likely to continue to see better pricing in the negotiated market and the strong pull on hogs for slaughter should keep marketings current and reduce the potential for backlogging animals. I calculate producer margins this week at about -$21/head, which is a vast improvement over the -$47/head that they realized in early January. The current forecast has producer margins moving into positive territory by early April, which should be welcomed given that producers haven’t seen a positive margin since late August. In fact, my calculations indicate that hog producers only experienced positive margins in seven weeks out of 52 last year. Producers need to maintain their herd reduction efforts even if margins do move positive in April. The sow kill was larger than expected again this week, so there is some evidence that the herd winnowing is still in progress. Producers have been getting some relief lately from input costs as both corn and soymeal prices have been tracking lower and there is considerable optimism that this growing season will result in strong production, keeping prices on the defensive. Of course, it is only February, and the crop isn’t even in the ground yet, so a lot could go wrong between now and harvest that might upset that prediction. Every spring there seems to be at least one or two waves of panic brought on by weather concerns and/or flooding that causes corn futures to rally. That is likely to be the case again this year too. But if producers can stay the course on reducing the breeding herd and corn prices don’t surge, then they stand a good chance of finishing the year in much better financial shape than they did in 2023. USDA released the results of their retail price survey this week which indicated a 0.6% decline pork prices in January compared to December and retail prices are now dead even with last year. Given that inflation is running just over 3%, the fact that pork prices are unchanged from last year is a small victory. Of course, now that the cutout is tracking higher, there is risk that retailers will begin to increase their pricing in the months ahead. USDA released some really goofy export numbers this week that showed total pork exports almost doubled from the week before, with huge increases to China and Mexico. It looks like some type of data error that will likely retrace next week. Traders seemed to recognize this and largely ignored the export numbers. Next week, look for more of the same—another move higher in the cutout and stronger cash hog pricing. If bellies join the hams in moving higher as it appears, the gain in next week’s cutout could be impressive.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}