Pork Wrap February 13

no pdf

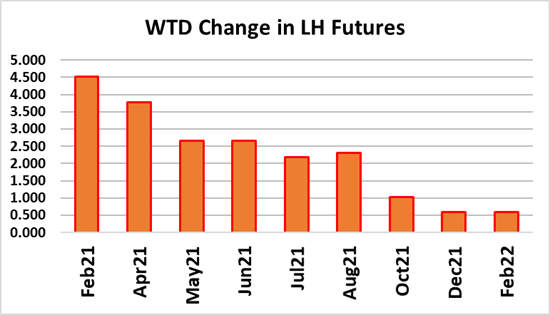

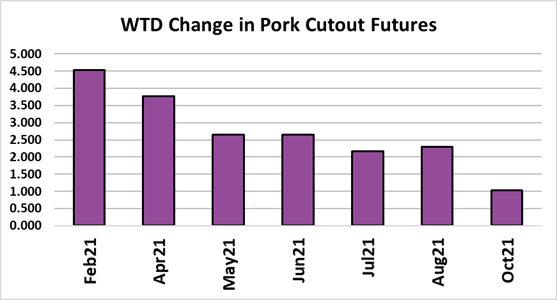

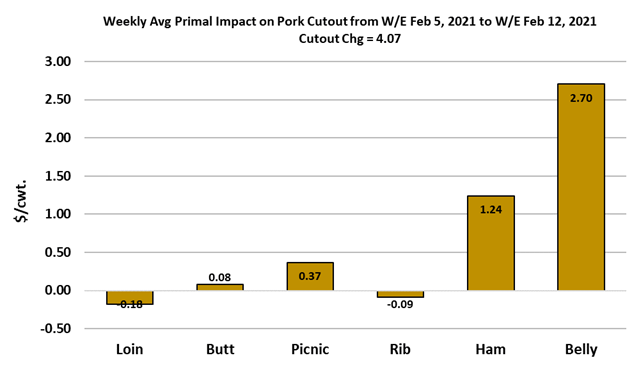

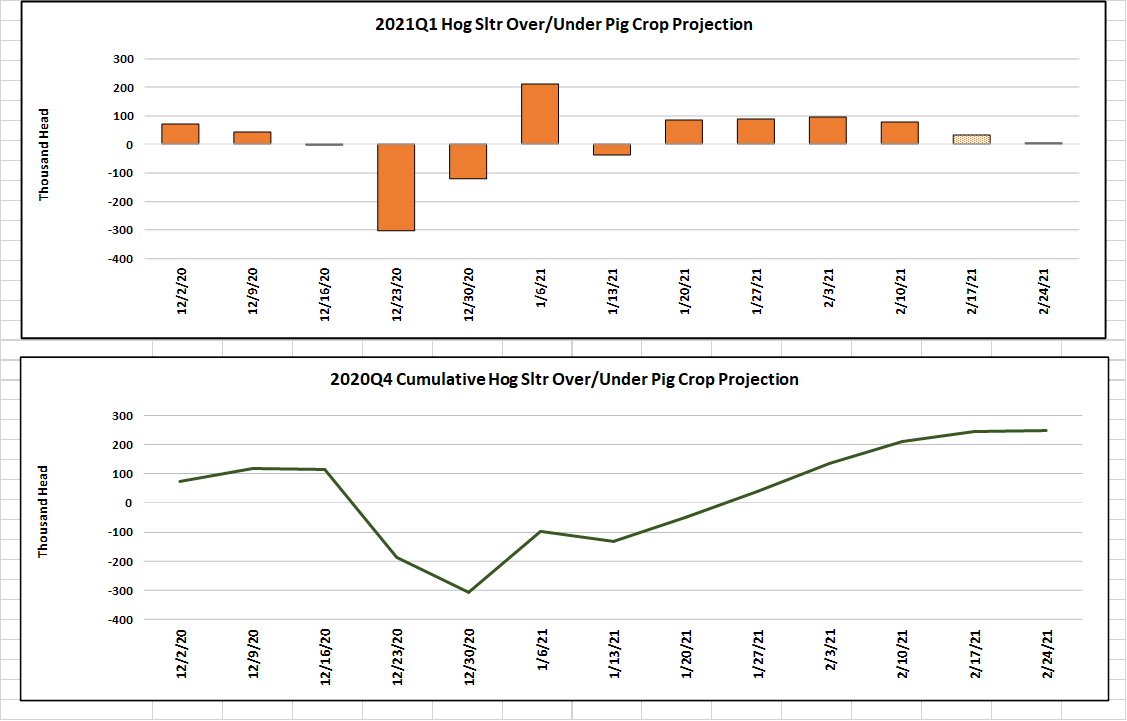

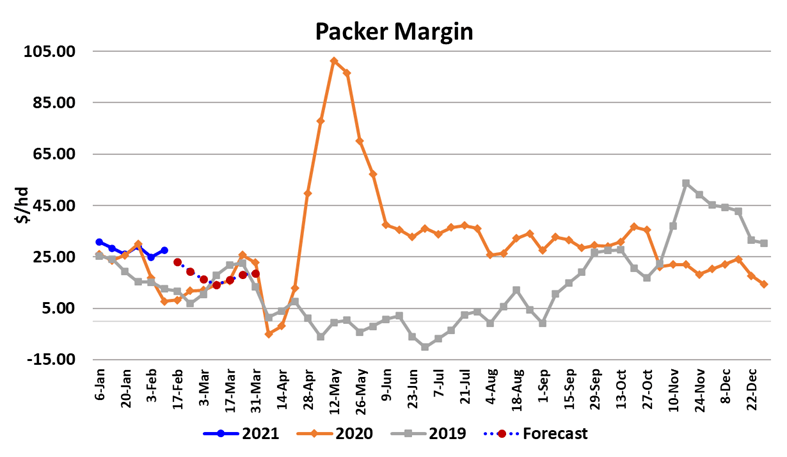

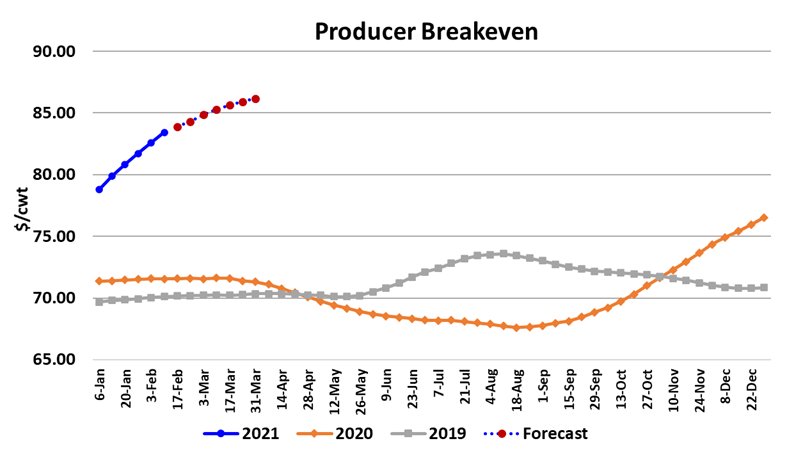

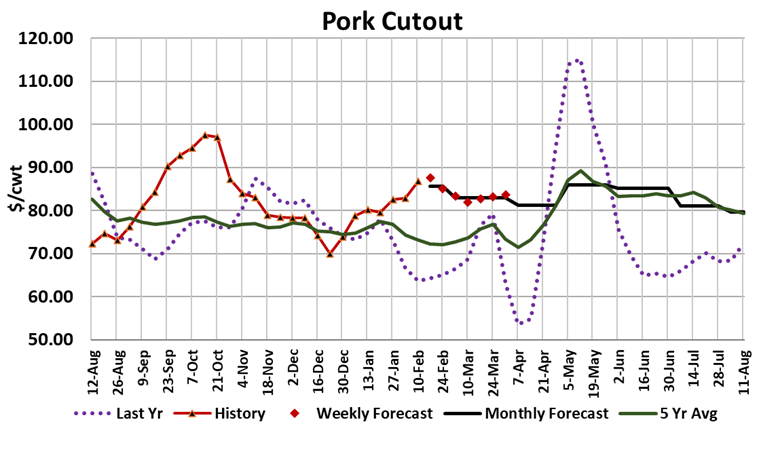

The pork cutout marched higher this week, adding a little over $4 from Friday to Friday. The negotiated market kept pace with the NDD market adding $4 also. That means packer margins remained intact¡ªnow near $27/hd. As long as the cutout is rising, I¡¯m guessing that packers won¡¯t mind similar gains in the cash hog markets. The important question is why is the cutout approaching $90 in the middle of February? This feels a lot like last October. I don¡¯t think the supply side can be blamed for this rally in the cutout. This week¡¯s kill came in at 2.66 million head, only about 1% smaller than last year. If we factor in carcass weights, which are heavier than last year, then pork production this week was a half-percent larger than last year. However, last year at this time the cutout was $66¡ªa full $20 lower than this week¡¯s cutout. So, clearly demand is what is driving this rally. The weekly export numbers have been rather stagnant and below last year, so it doesn’t seem like exports are to blame unless some product is being exported that is not being captured in the weekly FAS numbers. We thought that might be the case last October when the market did this, but once the official export data became available it was clear that exports weren’t the driver. The chart below indicates that it was the hams and bellies that boosted the cutout this week. The bellies are driven by retail feature activity and cold storage stocks are really low so this could be a temporary rally driven by retailers. Those usually don¡¯t last long before the primal comes crashing back down. The hams are more difficult to figure out. Easter is only 7 weeks away, so it¡¯s could be some last minute processing. If that is the case, then it will be done soon. There were signs today that the loin primal is starting to slip, but the rest of the carcass held up very well. The combined margin chart below shows the margin moving higher now and just a tad above the zero line. It head-faked me for a couple of weeks by jiggling sideways, but now it appears to be tracking higher. One thing to notice about that chart is that in recent weeks the packer margin (blue bars) has been rather stable and the producer margin (orange bars) has been improving and is what has driven the combined margin higher lately. That is indicative of a market where gains in the cutout are being passed along to producers. I¡¯d like to think that means that producers had some leverage over packers, but if you look at the packer margin chart below for the second week of February, we can see that 2021 margins are record large. That doesn¡¯t seem like a situation where producers have a lot of leverage. Producer margins were about -$24/head this week and they would need the LHI to be above $83 just to breakeven. Higher feed costs are really starting to drive producer breakevens upward. It is good that some margin improvement is trickling down to producers, but it is important to remember that consumers are the source that drives pricing throughout the supply chain. If consumer demand falters, and it will eventually, then producers are going to be skewered by both a falling cutout and rising grain prices. Having said that, there are four stories going on simultaneously and they are all bullish: 1) the current cold snap in the Midwest will take weight off of hogs in the near-term, 2) high corn prices are going to lead to high hog prices eventually, 3) demand is phenomenal right now and there is a tendency to project that demand strength into the back of the curve, and 4) there is a strong belief among money managers that we are beginning a commodity super-cycle and inflation is going to gain steam in 2021. My thoughts on these are 1) yes, but it¡¯s very short term. 2) corn prices are not all that high and there is no guarantee they will stay up here. 3) this is just a rookie mistake, and 4) possibly, but these things tend to develop over years, not weeks, and more evidence is needed. So I guess you can say that I¡¯m not sold on the idea that hog and pork prices have moved to a whole new level and are going to stay there. Keep in mind that the cutout peaked around $100 back in October but had lost $22 by the Dec expiration. I suspect that a similar turn will happen soon, with the cutout peaking in the low $90s and the retreating back down to the low $80s or high $70s. Next week, the thing to watch is the cutout, particularly the bellies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}