Pork Wrap February 11

Cash hogs continued to march higher this week, with the WCB adding a

little over $5 on a weekly average basis and the NDD negotiated price up

$1.59. It seems that hog availability in the Western Cornbelt region must

be quite a bit tighter than in the other regions. Prices out of the WCB

have been running very strong relative to the national average over the

past several weeks. That has led some to speculate that perhaps there

are bigger disease issues in that region. Whatever the cause, the rally in

cash hogs has been impressive. In the six weeks since the end of 2021,

negotiated hog prices in the WCB have gained over $28/cwt. What’s

more, the rally has yet to show any sign of slowing down. Normally, such

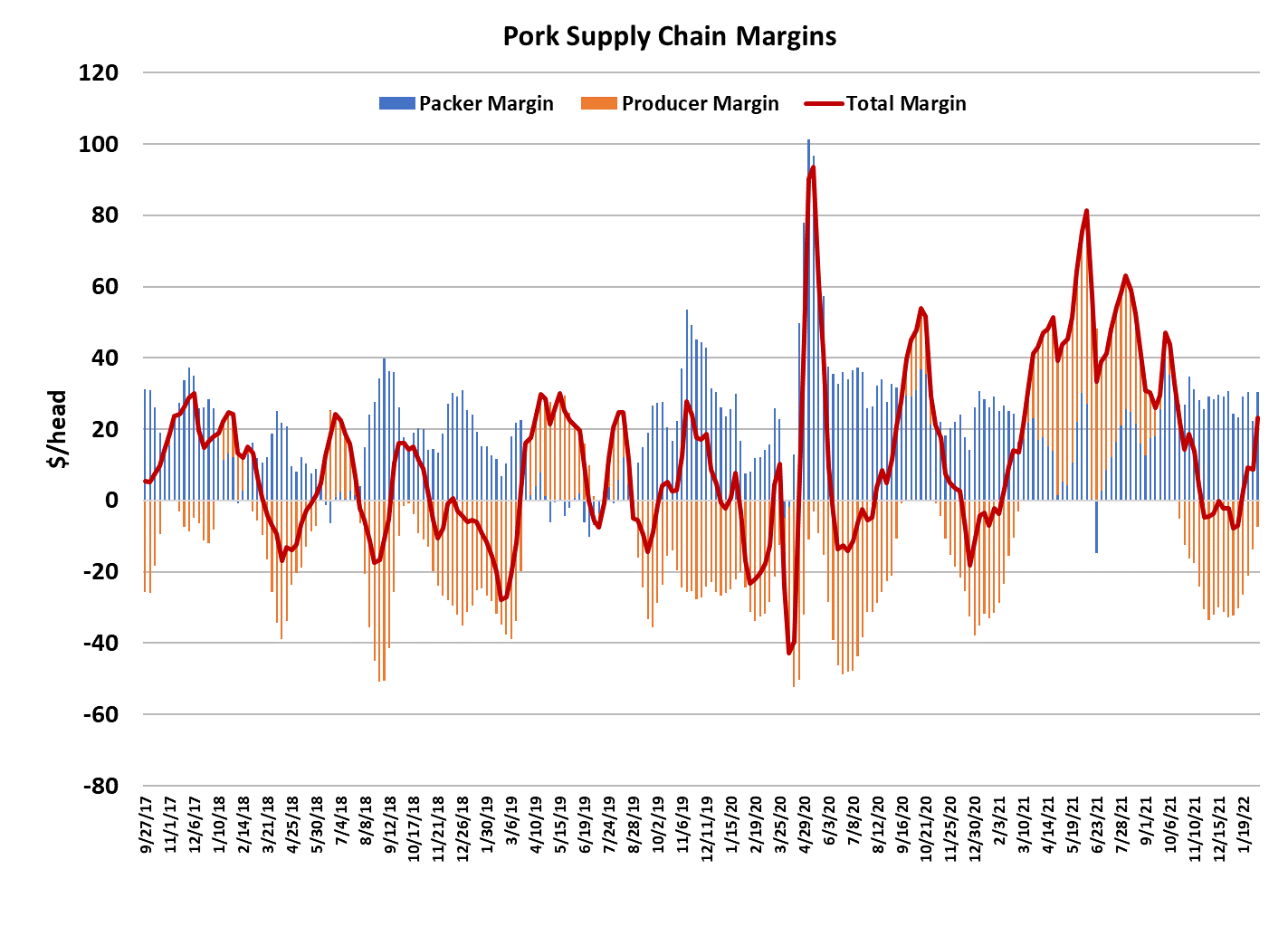

a rapid increase in cash hog prices we might expect packer margins to

come under serious pressure, but so far that hasn’t been the case. In

fact, packer margins expanded over $6/head this week to nearly $29

because the cutout gained over $6/cwt to average $102.35 for the week.

That is the first triple-digit cutout since mid-October and is more than $15

over the same week last year.

Weekly pork production was about 5% under last year, so that explains

part of the strength in the cutout, but it is pretty clear that export volumes

are well below last year and import volumes are well above last year. So,

total availability here in February is only about 3% below last year. The

real difference maker is demand, which is considerably stronger than it

was last year at this time. Last February was when the “great demand

bubble of 2021” first started and the cutout gained $28 over the Feb/

March period last year then kept on rising through the spring and early

summer. It is unlikely that demand this spring and summer will be as

strong as it was last year, but right now pork demand is in an upcycle as

indicated by the combined margin chart below. My theory is that

consumers are moving back down the protein ladder and trading down

from beef to pork. That will give us strong pork demand for a few weeks,

but eventually they will trade out of pork and into cheaper chicken.

For now however, demand is quite strong and this week it was most

evident in the hams and bellies, which accounted for most of the cutout’s

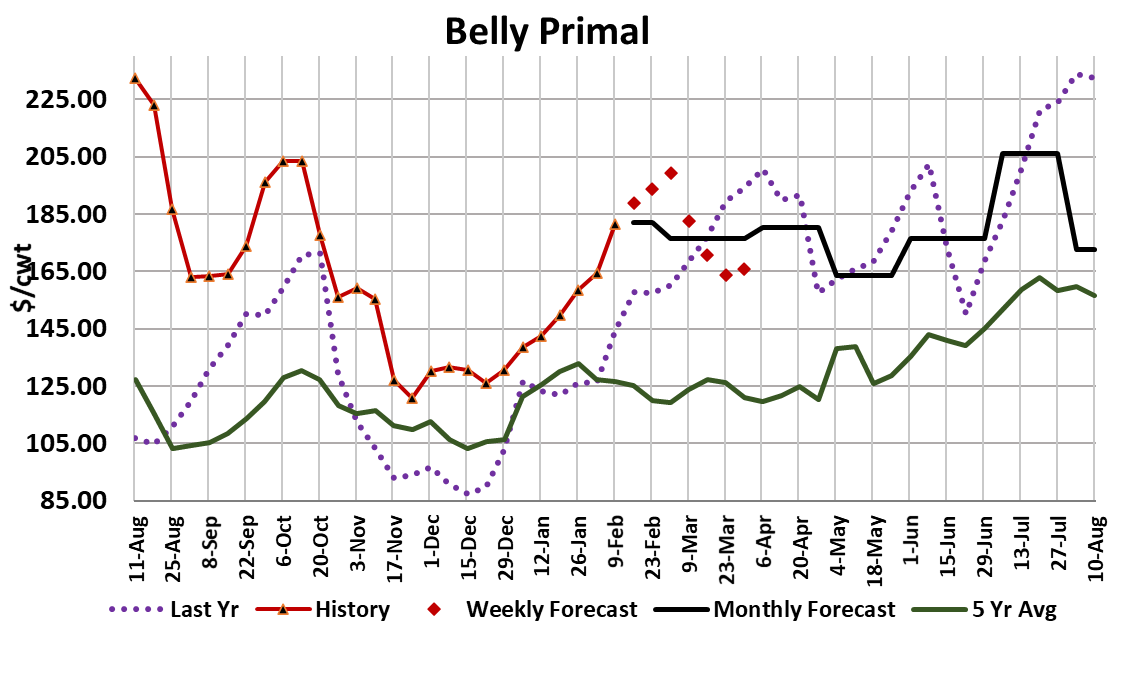

gain while the retail primals were only slightly higher. The rally in bellies

is somewhat unusual in that it has been going on for seven weeks now.

Normally, bellies rally hard for 3-4 weeks and then fall rapidly. The

forecast has bellies moving higher for another 2-3 weeks before price

levels cause users to back away and prices to fall. Belly pricing often

follows retail bacon features. When the retailers decide to feature bacon

heavily, belly prices will rise for a few weeks leading up to the promotion

and then fall hard once all of the raw material has been procured. On the

ham side, we have seen the bone-in hams begin to creep higher and of

course, there is the periodic price spike caused by boneless ham buyers

coming into the market. If buyers haven’t secured their Easter ham

needs yet, they will likely be hurrying to get that done in the next couple

of weeks and after that we could see ham prices sag once again.

Although the retail primals didn’t post the sizable gains that the

processing primals did this week, it is still noteworthy that they did not

weaken. Retail prices are very high and this week USDA released the

results of its retail price survey for January which showed a slight

uptick in pork prices. Those prices are a little below the peak they

made back in November, but not by much. Retail pork prices were

about 35% lower than beef prices during January and that is what will

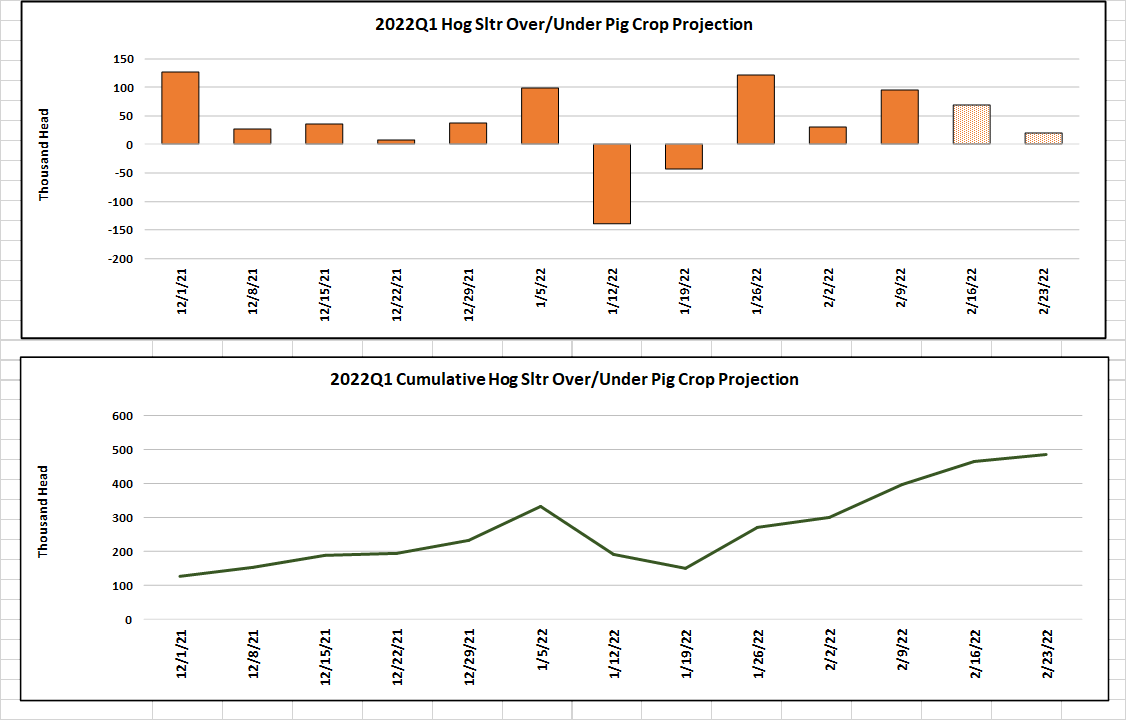

matter most to consumers. On the supply side, this week’s slaughter

was estimated at 2.52 million head, up 71,000 from the week before.

That turned out to be about 100k larger than what the pig crop implied,

thus we continue to see weekly kills larger than expected, outside of

the two weeks in early January when omicron-related absenteeism

constrained kills. It looks to me like when the Dec/Feb quarter comes

to a close in a couple of weeks, we will have over-killed the pig crop by

about 500,000 head and USDA will likely revise that pig crop upward in

its March Hogs and Pigs report.

Carcass weights moved a pound lower this week and that pulled the

DTDS weights, which had crept into positive territory, back down to

zero. That helped to relieve any concerns that hogs might be backing

up in the system. The big mystery at this time is why weights aren’t

unusually light given what appears to be a strong pull on the spot hog

supply. In fact, the daily weight data reported by packers as part of the

requirements for mandatory price reporting, shows weights for

producer sold hogs modestly above where they have been in recent

years. So, the mystery remains, but it is very clear that cash hog

prices are in a strong uptrend. International trade is perhaps the

weakest part of the fundamental picture for hogs right now. The

official export totals for December, which were just released this week,

showed a 16.4% YOY decline in pork exports and for 2021 as a whole,

exports were 3.5% below last year. Pork imports, on the other hand,

were very strong in December, up 50% YOY.

Right now, pork prices in the US are among some of the highest in the

world and naturally that is attracting imports from countries where the

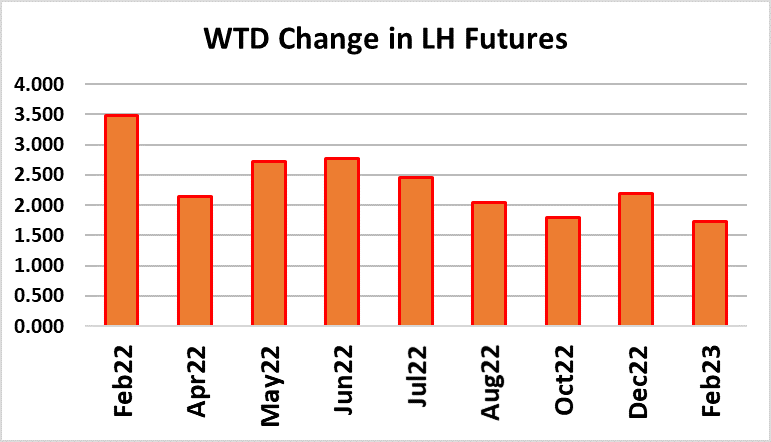

internal price is a lot lower. Futures traders have been trying to stay

ahead of a rapidly rising Lean Hog Index that looks like it may be close

to $91.50 when the February contract expires on Monday. If you

recall, the Dec contract expired at close to $72, so we’ve had almost a

$20 increase in two months. There was some mild selling in the hog

futures on Thursday and Friday, but that was mostly corrective in

nature and not related to anything negative in the fundamentals.

Given that the cutout printed at an eye-popping $110 this afternoon, it

is very likely that the bulls will be back on Monday morning with their

horns sharpened. Next week, watch the bellies and hams. Those

have been the primary source of strength in the cutout. If they start to

show some cracks then we might have to conclude that the uptrend in

the hog and pork complex is nearing its end.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}