Pork Wrap February 10

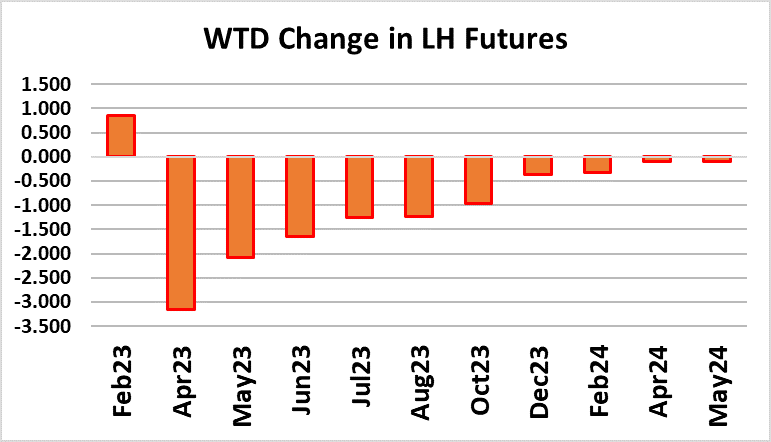

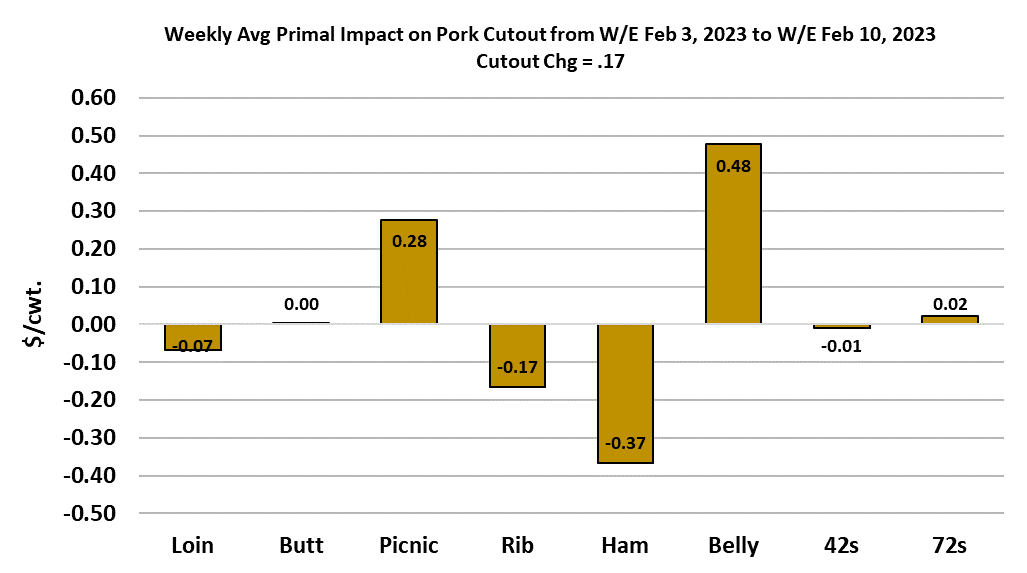

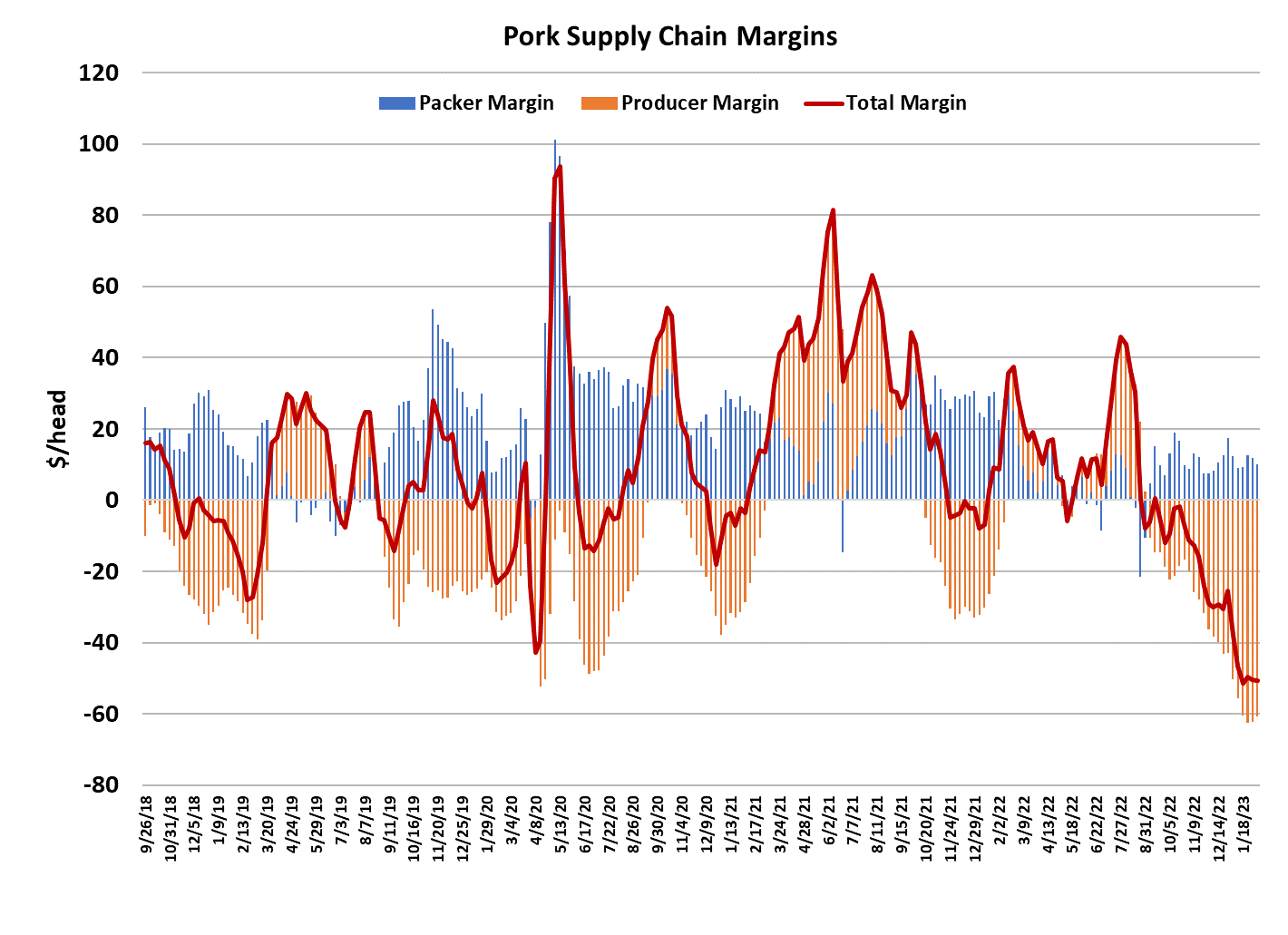

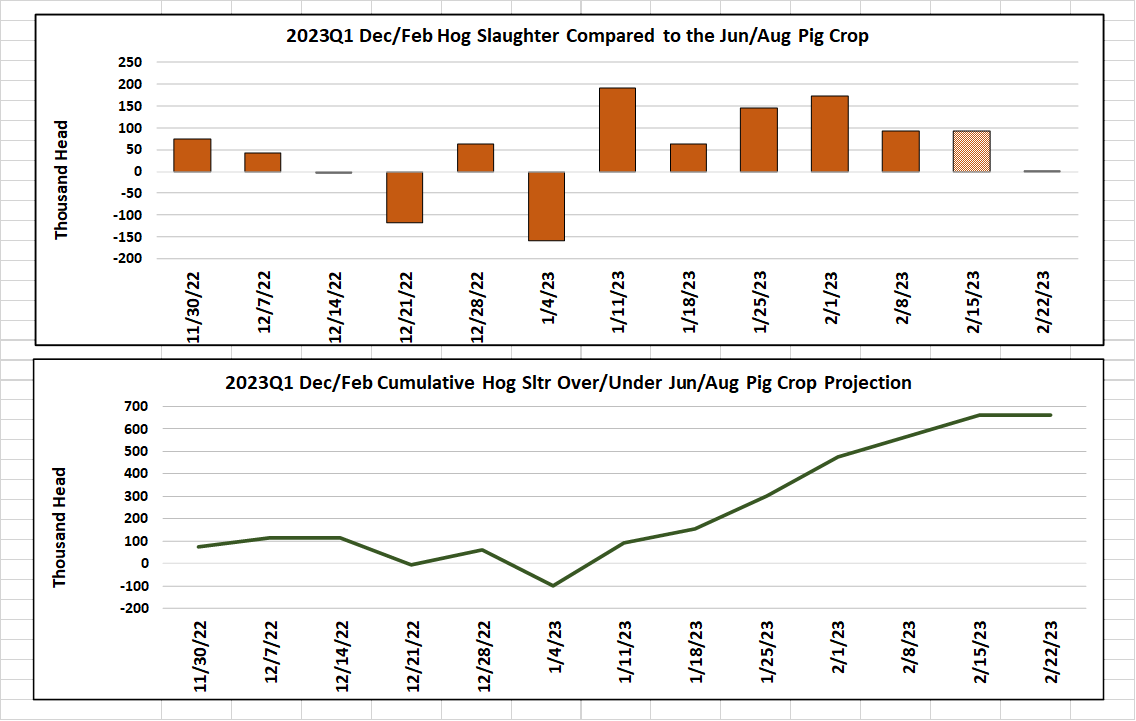

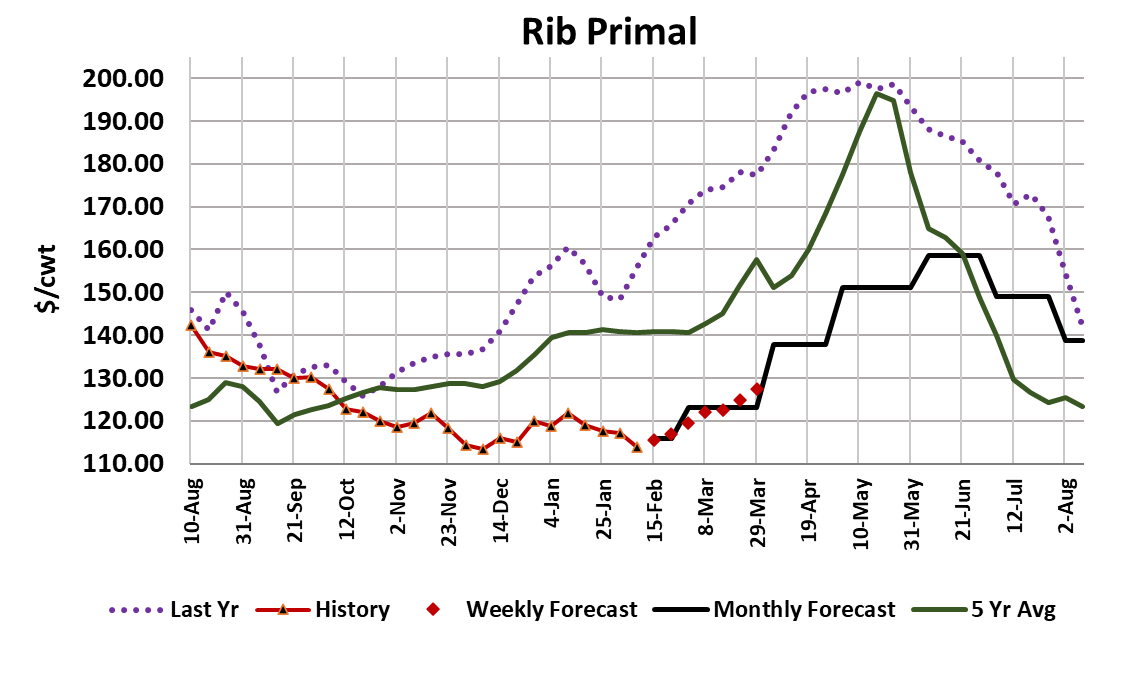

Finally there was some substantive movement in prices, but unfortunately for packers it was the prices on the wrong end of their profit equation that were increasing. The WCB negotiated market added $4.50/cwt. on a weekly average basis and the NDD market gained $3.77/cwt. The pork cutout?—it gained a mere $0.17/cwt. In the last three weeks, the cutout has managed to gain about $1. It has been worse than watching paint dry. Packer margins fell to about $10/head and should get compressed more next week as the full effect of the negotiated price increase gets baked into the LHI. Last week I highlighted the negotiated markets, and the WCB in particular, as something to watch and this week that didn’t disappoint. I would say that the negotiated price increases are a sign of the hog supply starting to tighten and weights seem to confirm that as well. FI barrow and gilt carcass weights have dropped three pounds in the last three weeks. The more timely daily weights from the 201 report suggest that trend is continuing. Packers have kept kills large and that did a good job of clearing through the backlog that might have resulted from the holidays and helped to dispense some of the hogs that went under-counted in last summer’s pig crop. This week’s kill came in at 2.5 million head, a little smaller than the week before, but still well above what the pig crop indicated. The attached charts demonstrates that the cumulative over-kill in this Dec/Feb quarter is likely to be something in the neighborhood of 700,000 head. The big unknown is whether or not those larger-than-expected hog supplies are going to continue into March/May. Packers probably hope that they will because larger hog supplies mean larger margins in general, but there will almost certainly be some seasonal tightening in hog numbers during March and April. Packer margins averaged about $10/head in Jan/Feb, but I suspect that would have been several dollars lower had the hog supply been as advertised by the USDA survey. It doesn’t help matters that pork demand has been very lethargic since late fall. The combined margin looks like it is comfortable at these very low levels. Low prices across the hog and pork complex have created a financial disaster for producers and not a great result for packers either. This week the bellies tried to show some life, but that positive contribution to the cutout was mostly offset by weakness in the ham primal. If we look at the price charts for each primal almost every one of them has been in a sideways pattern for the last four or five weeks. That is very unusual. Hams are particularly problematic because they make up such a large percentage of the cutout that it is difficult to get much upward movement in the cutout without some help from the hams. My price forecast has the cutout rising $10 over the next six weeks, but given that nothing has moved very much in the past four weeks, it is difficult to believe that call. It’s not like I’m dialing in really strong demand to arrive at that forecast, it really only takes a return to something closer to average demand to get there. This long period of weak pricing has probably created a lot of complacency among the pork buying community. Buyers haven’t needed to be in a hurry to source product and probably are staying more hand-to-mouth than they should. That has the potential to cause a rush for coverage at the first signs of strengthening pork prices. So we could end up with this relatively tranquil period being broken by a sharp move higher at some point. We will probably need to push kills down to 2.4 million head or below in order to see that happen. There is a big difference in beef and pork demand in that pork typically doesn’t show up in high-end foodservice applications like beef does. Well-off consumers are still exhibiting strong demand, but pork doesn’t benefit as much from that as beef does. Pork caters more to the less-well-off consumer and has to compete more directly with chicken. Demand seems to be struggling amongst those nearer the bottom of the income pyramid and that is bad for pork. For example, pork ribs are the most expensive part of the carcass on a per-pound basis, but that primal is struggling with weak demand and prices well below last year and the five-year average. In beef, the most expensive primals, ribs and loins, are the ones that are over-performing right now. It is a tough dilemma for pork demand. Some stimulus checks would help a lot, but that’s not going to happen. Anyway, it will be interesting to see if packers can have any success moving the cutout higher next week as they watch their hog costs climb. If the cutout does post a substantive gain, I would bet on the bellies being an important contributor.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}