Pork Wrap December 31

The hog and pork complex remained stuck in neutral for yet another

week. The WCB cash market averaged $0.25 lower on the week,

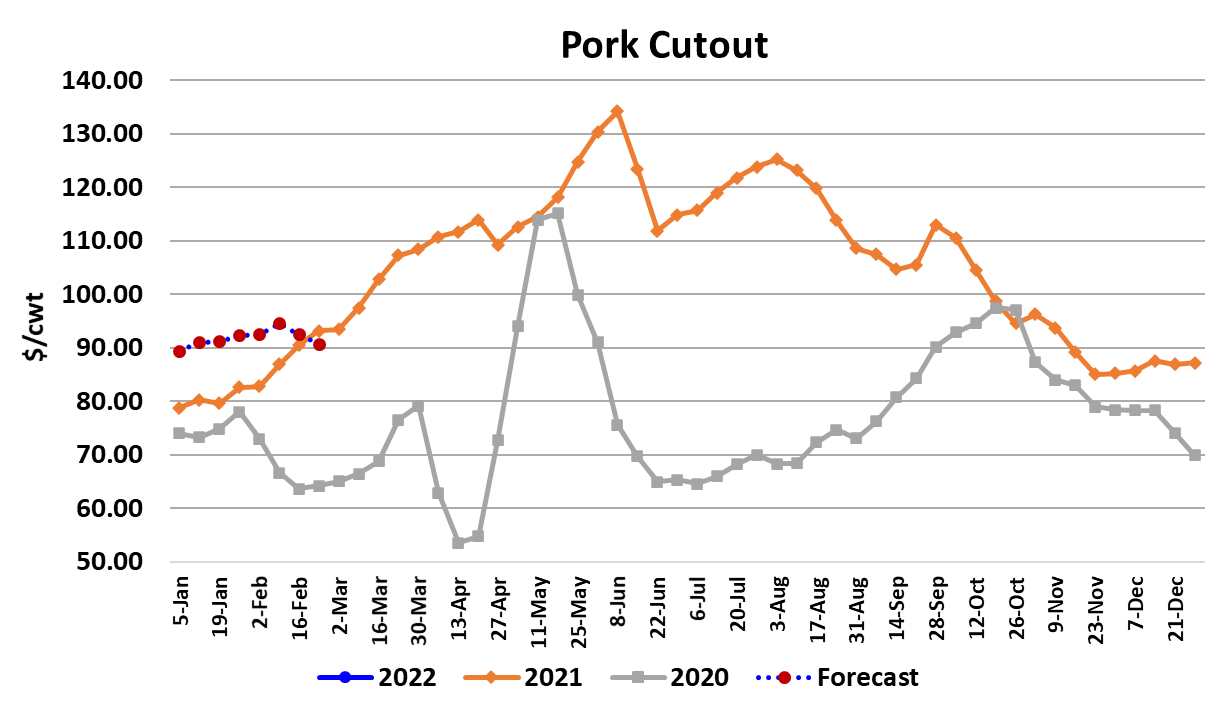

while NDD cash market posted a $0.94 gain. The cutout managed

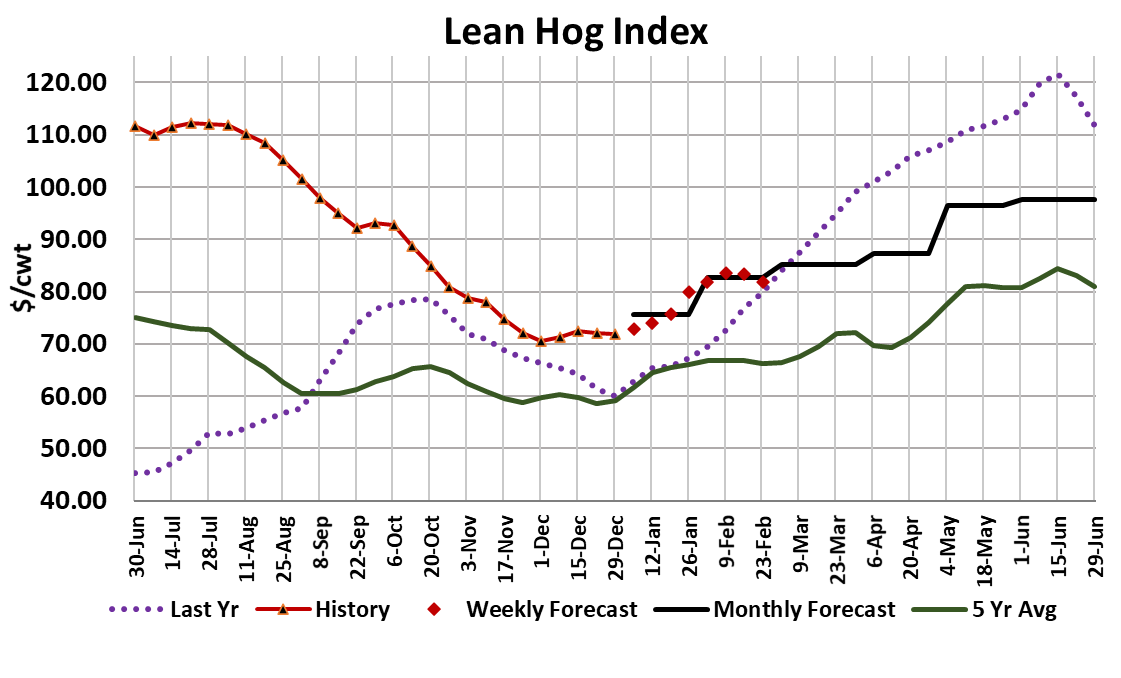

$0.33 higher on a weekly average basis. As a result, the LHI was

almost unchanged on the week, averaging $71.93. It feels like

participants all up and down the supply chain are just waiting to see

what happens next. Last week’s Christmas-shortened kill was the

second smallest weekly kill of the year, yet the cutout went nowhere in

the ensuing days. That is because buyers also take the holidays off

and plan well in advance for these last weeks of the year. The real

challenge will come next week when buyers are back at their desks

and pork production ramps back up to non-holiday levels.

I am seeing some signs in the retail cuts that they may be poised to

move higher in the next few weeks. We’ve already seen some steady

price increases in the butts and ribs, but I think now the loin primal

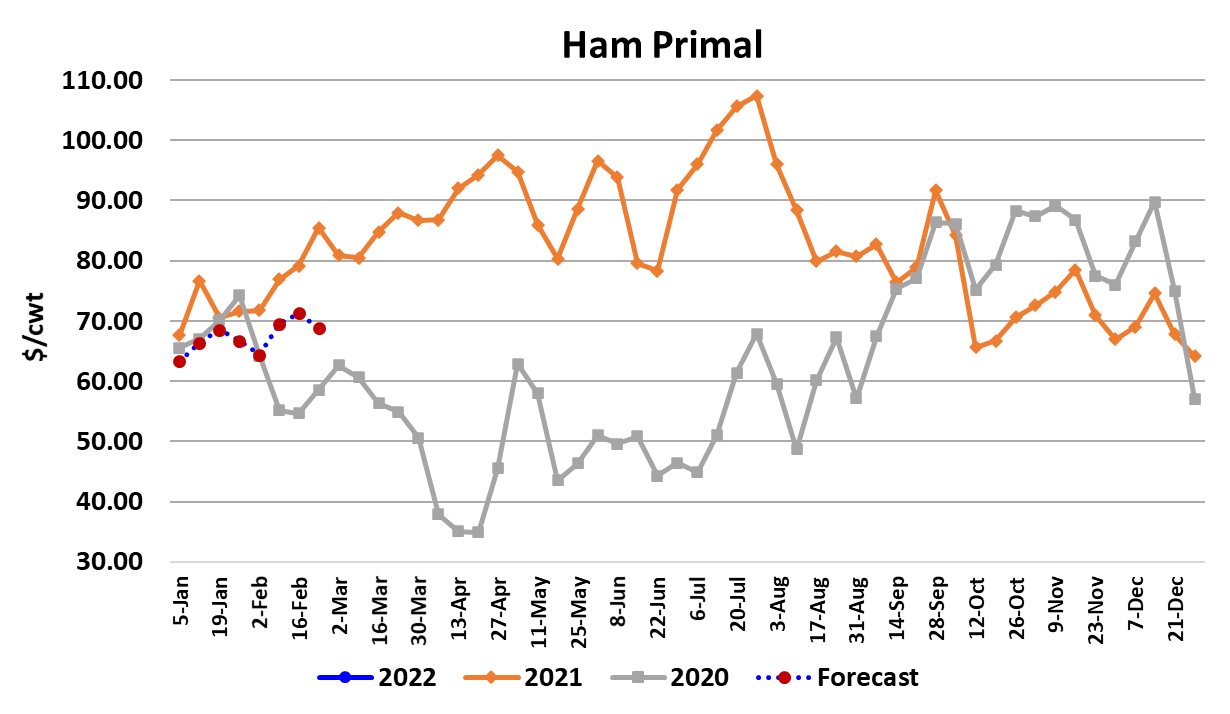

could start to attract some interest. The worst is probably over for the

hams and their next move should be higher, but it will be more of a

slow steady grind higher rather than a rocket launch. The chart below

indicates that the hams were the biggest drag on the cutout again this

week, but modest improvements in belly pricing largely offset the

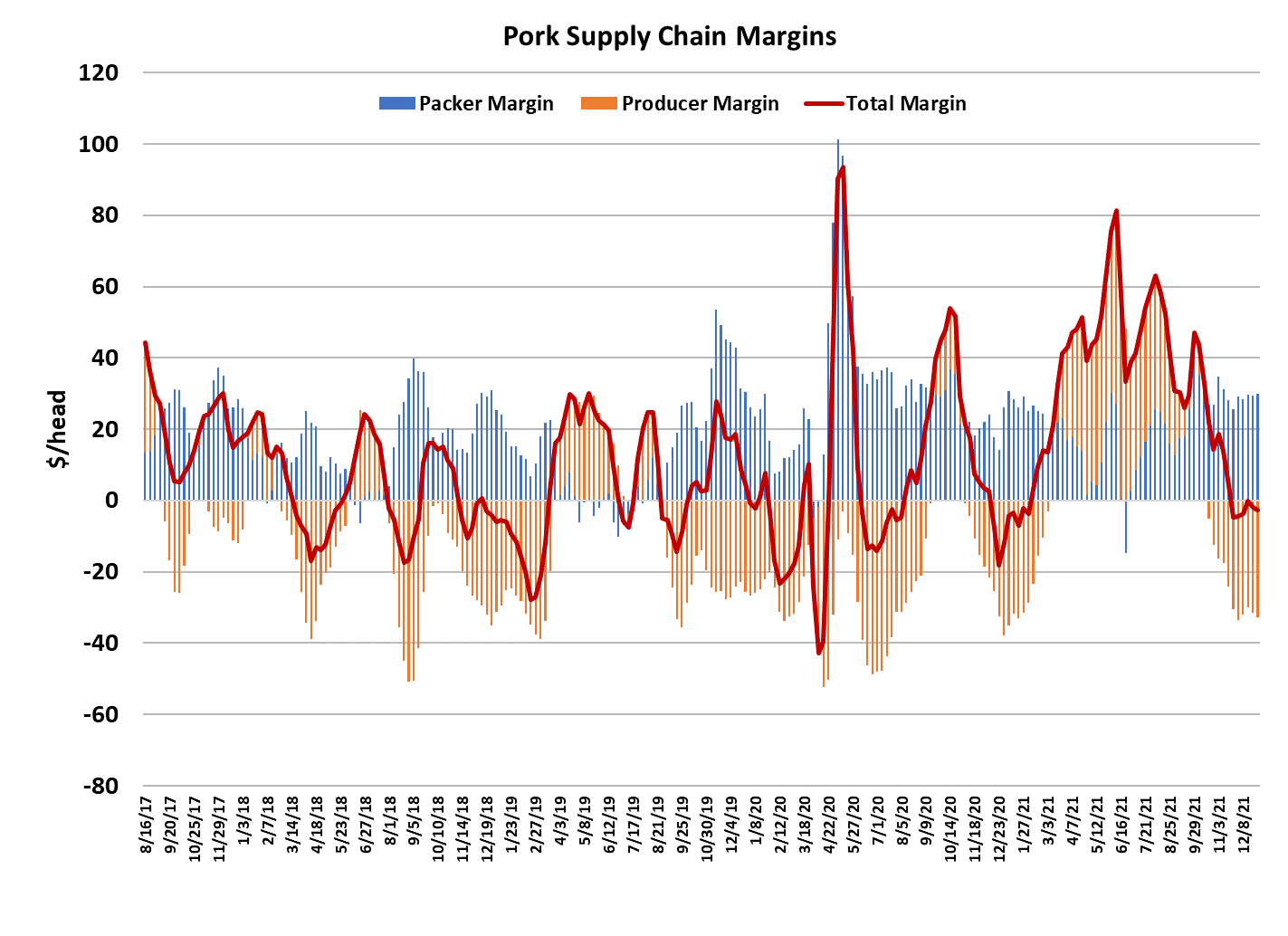

weakness in the hams. Overall pork demand appeared to be making a

near-term bottom a couple of weeks back, but the combined margin

chart indicates that the holiday period disrupted any chance for it to

gain traction. Now that the holidays are behind us, perhaps that

demand upcycle will get back on track. Soaring omicron infections in

the US remain a potential risk/benefit to pork demand. The risk part

lies with the possibility that so many consumers get sick that they just

don’t feel like eating at all and certainly don’t feel like going to the

grocery store.

The benefit potential is related to the chance that consumers return to a

stay-at-home approach for a while and thus shift a significant portion of

their consumption from the foodservice channel to retail, which we

already know is positive for demand. Another risk from the omicron

surge is the potential for plant workers to get sick en masse and thus

cause packers to have to scale back the kill substantially. This seems

like a very real possibility that hasn’t been talked about nearly enough.

So far, the daily kills have held up well, but states where most hog

packing plants are located have yet to see the surge like the coastal

states have. It is just a matter of time before states like Iowa see huge

spikes in infections. North Carolina, where the largest hog slaughter

facility in the nation is located, is now recording huge increases. It is

true that the packing plant workforce is more than 90% vaccinated, but

this variant seems to make people sick in spite of being vaccinated.

And then there is the issue of kids, who are getting sick in record

numbers. That could cause school closures in early January and thus

generate high absenteeism as plant workers stay home to care for their

kids.

Keep in mind that hog supplies are seasonally very large. This

would be a bad time to lose a chunk of processing capacity. If

plants do get constrained by labor problems, then I think we can

expect the cutout to rally as buyers get shorted and we would

probably see some retrenchment in the negotiated hog markets.

Any such labor constriction probably wouldn’t last very long,

perhaps 2-3 weeks, because people infected with this variant seem

to recover rather quickly, especially if they are vaccinated.

Epidemiologists tell us that we are likely to see a huge and rapid

spike in infections and then a very quick decline. So the worst of it

might be over by the end of January, but it could do plenty of

damage to the pork supply chain in just a few weeks. This week’s

kill looks like it is on track to come in at 2.16 million head, but we

won’t know for sure until Monday because Friday was a

USDA holiday.

Next week, I see the kill bouncing back to about 2.45 million

head if covid doesn’t cause too many problems. Kills are still

coming in a little above what the prior pig crop implied, but the

over-killing doesn’t seem to be as severe as it was in the recently

completed Sep/Nov quarter. USDA reported barrow and gilt

weights down a pound this week, but they could bounce back in the

next couple of data reports that will cover the holiday period. At

present, weights seem to be pretty normal and don’t indicate any

backing up in the pipeline. With demand due to cycle higher

and supplies potentially getting crimped by covid, the

potential for higher pork prices in the next few weeks is high.

Traders who were long the February contract seemed to grow tired

of waiting for some upward movement in the lean hog index and

that contract lost almost $2 on the week. More importantly, the

spread between the Feb pork cutout futures and the Feb hog

futures increased substantially this week and that shows that

traders are revising their expectations for packer margins in

February upward.

Packer margin expansion is exactly what we would expect to

happen if processing capacity gets compromised, so it looks like

traders are starting to position themselves for a higher probability

of slaughter disruptions in the weeks ahead. In all though, the

futures curve doesn’t look too far out of line with my

fundamental forecast, at least through June, and the supply

picture beyond June depends on pig crops that haven’t been born

yet. Next week, watch the daily covid infection counts and watch

the daily slaughter numbers for signs that throughput is being

affected by the virus. The omicron surge is going to be the main

story of interest for the next couple of weeks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}