Pork Wrap December 30

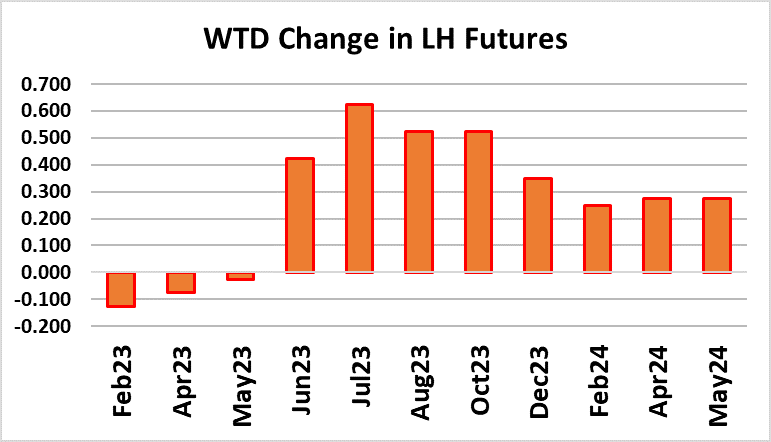

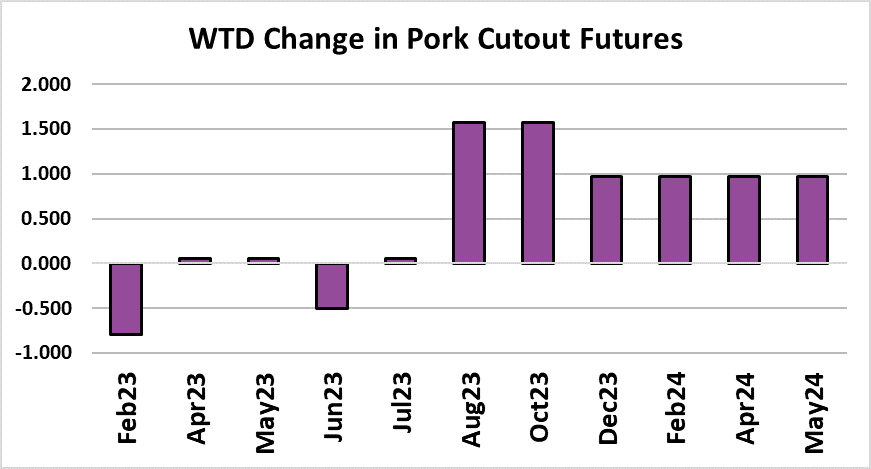

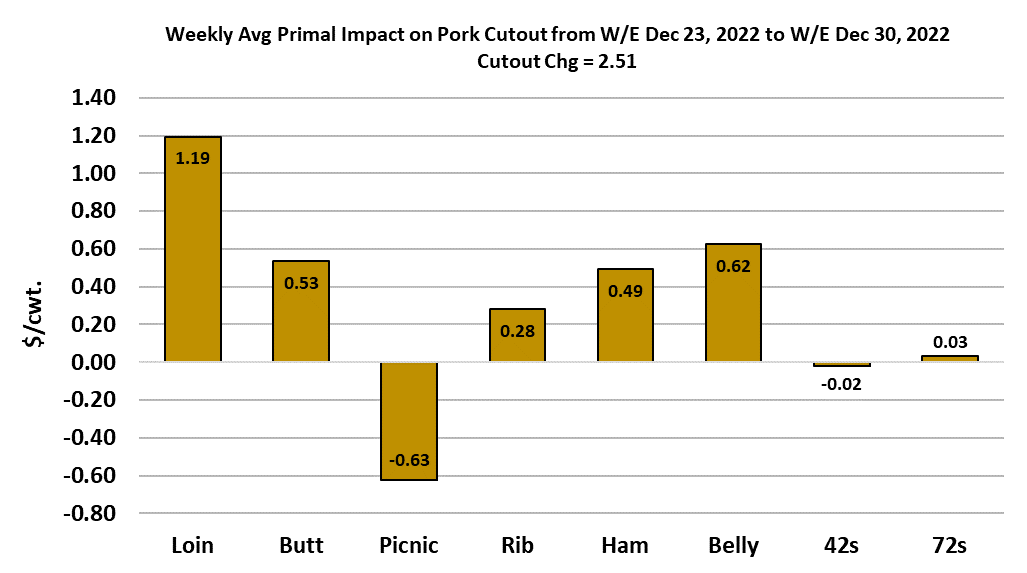

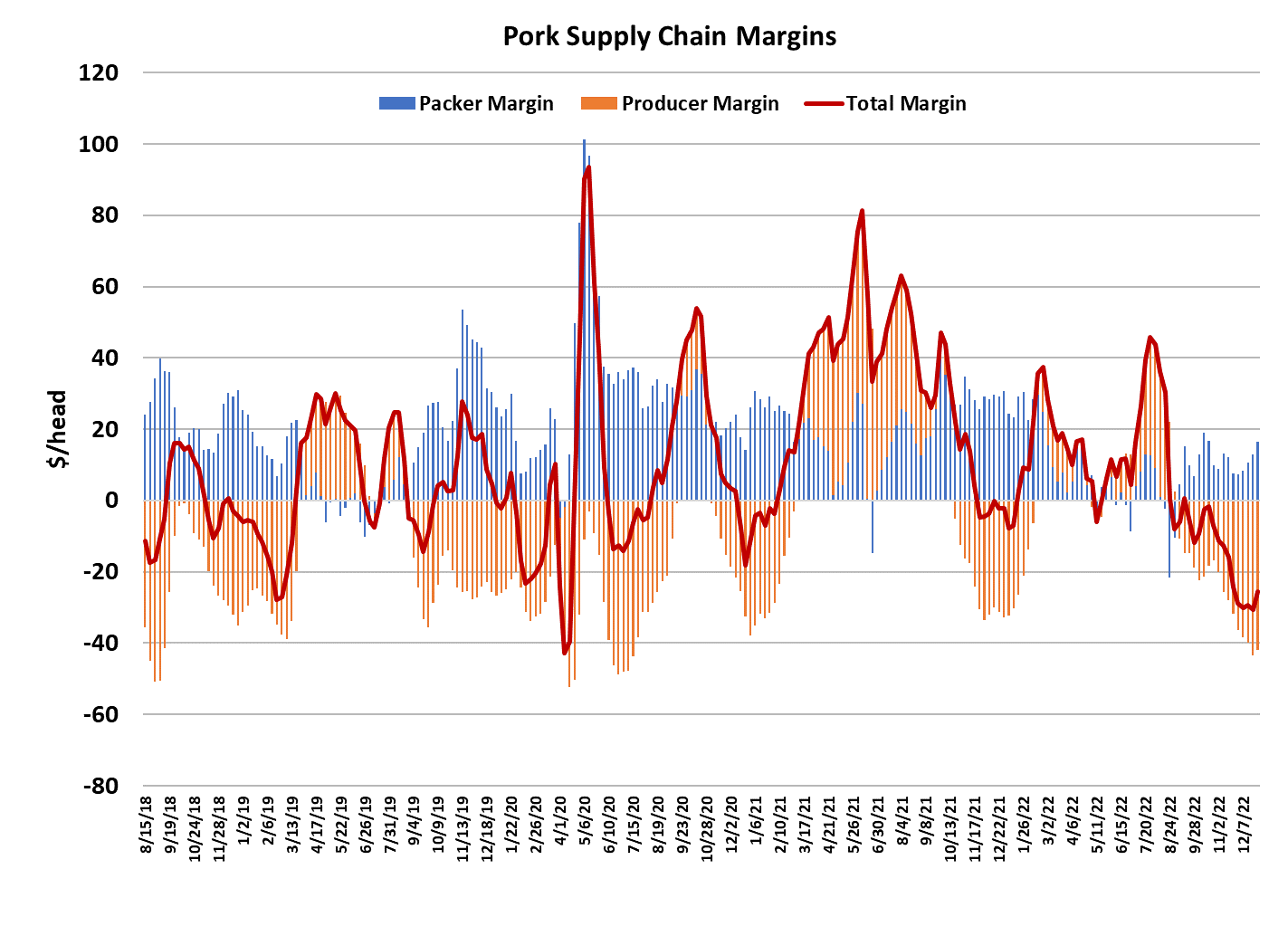

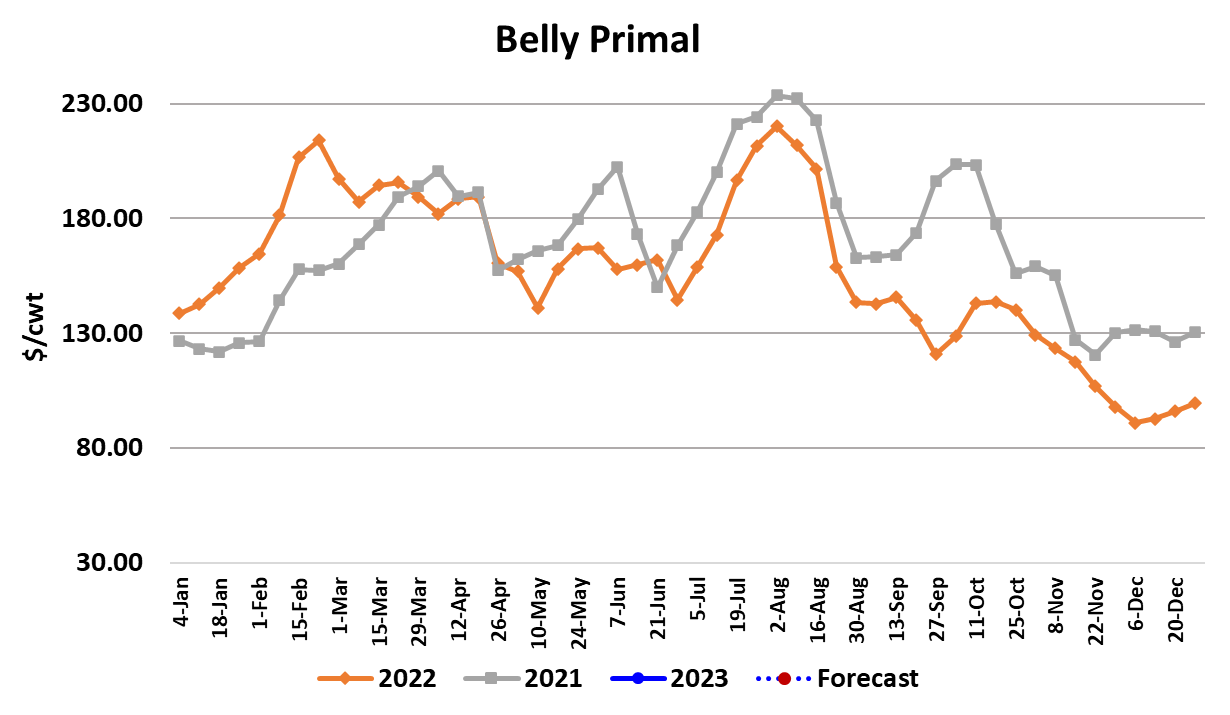

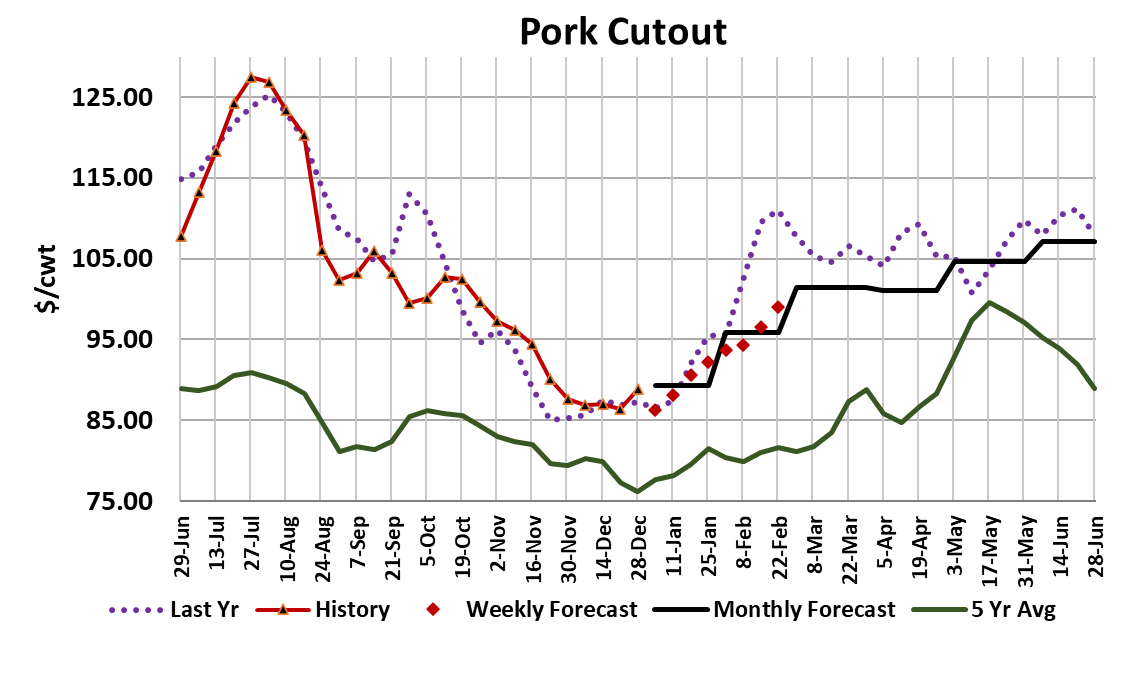

The holidays and last week’s weather forced a kill slowdown by pork packers and that had the effect of improving their margins. The cutout gained $2.51/cwt. on a weekly average basis and the WCB negotiated cash market dropped almost $4.50/cwt. That pushed packer margins up to about $17/head—the largest since early October. Pork buyers seemed to be caught a little by surprise and the cutout ran over $90/cwt. early in the week, but eased as the week progressed and production increased. Prior to the holidays, there were already signs that some of the tightness in the cash hog market was starting to ease and the smaller kills have helped that along. However, once normal weekly kills resume, I would expect to see at least a modest rebound in the cash hog market because there are still more shackles than hogs to fill them. All of the primals except picnics participated in this week’s cutout gain. Pics have been very high during Q4 and the normal seasonal pattern is for prices to deteriorate as January approaches. The fact that all of the other primals advanced suggests that this increase in the cutout was driven more by supply constriction than by any new burst in pork demand. The combined margin did turn a tad bit higher, but it hasn’t been too convincing so far. Futures traders got overly-excited on Tuesday when the noon cutout printed close to $98 and they drove the Feb contract up nearly $4 to peak near $91.50. That left a huge basis between the cash index near $80 and the nearby futures. Traders spent the remainder of the week reducing that and Feb finished on Friday at $87.70. While the short kills did goose the cutout briefly, it is falling now and the concern is that it might continue to slide as production begins to normalize after the holidays. This week’s kill totaled 2.19 million head, a big improvement over last week’s 1.78 million, and the forecast is looking for something over 2.3 million next week. Packers appear to be gearing up for a huge Saturday kill next week to help cover some of the production shortfall from being dark on Monday in observance of New Year’s. Barrow and gilt carcass weights were steady at 215 pounds this week and they will likely drop one pound when next week’s data is revealed. There should still be some modest upward pressure on weights during Jan/Feb and right now the forecast has them topping out around 218. My guess is that improving slaughter levels could push the cutout back down to $85 or so, but before long stronger demand will begin to emerge for the bellies and the retail items and that could begin to move the cutout higher to the point where we could see it trade in the low $90s by the end of January. Bellies are expected to play a major role in reversing the cutout’s fortune as the slicers run more hours after the holiday lull. Of course, there are still a lot of bellies in cold storage, so there is some risk that the belly primal might underperform the forecast in January. Hams have faded right on schedule for the end of December, but there are rumors of large orders being placed by Mexican buyers and that probably limits the downside risk in the next few weeks. Domestic buyers will also be sniffing around the ham market looking to procure raw material for processing ahead of Easter. There were probably a lot of Easter ham buyers that have been sitting on their hands during December waiting for a break in ham pricing and these buyers could start to come into the market in the next few weeks. So if we have both bellies and hams poised for moving higher, it will be difficult not to see some gains in the cutout. The retail cuts, primarily butts and loins, typically perform well during January as retailers like to feature them as a lower-priced alternative for cash-strapped consumers after the holidays. So there is another reason to look for some lift in the cutout. While domestic demand appears poised to improve, I still have concerns about export demand. Covid is raging in China now and will likely kill any interest those buyers might have had in procuring US pork. Hog and pork prices inside China are moving lower as the population is more focused on health care than on what they are going to eat in the near term. The covid surge in China also has the potential to snarl some supply chains again as port workers fall ill and factories can’t be staffed. That won’t be good for the global macroeconomy and it won’t be good for China’s pork demand either. One thing we need to keep in mind as we think about pork demand over the next couple of months is that it is likely to fall well short of the phenomenal demand that was posted in Q1 of last year. Last year’s Q1 demand index registered 1.065—the highest ever outside of 2014 when PEDv caught buyers by surprise. I’m forecasting Q1 of 2023 to see a demand index near 0.99. For the current quarter (q4) the demand index is running close to 8 percentage points below the prior year, so it doesn’t seem like a big stretch to forecast Q1 down 7.5 points. I think the risk is that demand comes in softer than what I have currently dialed in. Next week, watch for the cutout to ease a little more as pork inventories improve and watch for negotiated hog prices to stabilize and perhaps inch a little higher as packers line up their post-holiday kill schedules.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}