Pork Wrap December 3

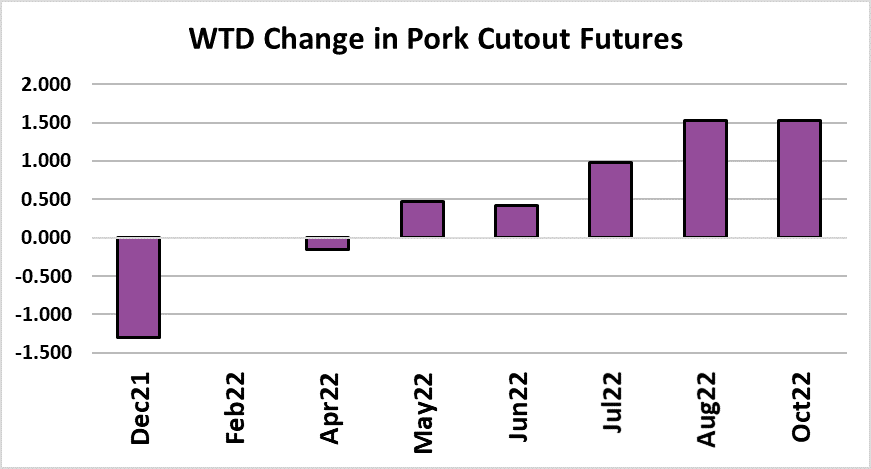

On a weekly average basis, the pork cutout was essentially

unchanged this week, but Friday-to-Friday it was down $2.61.

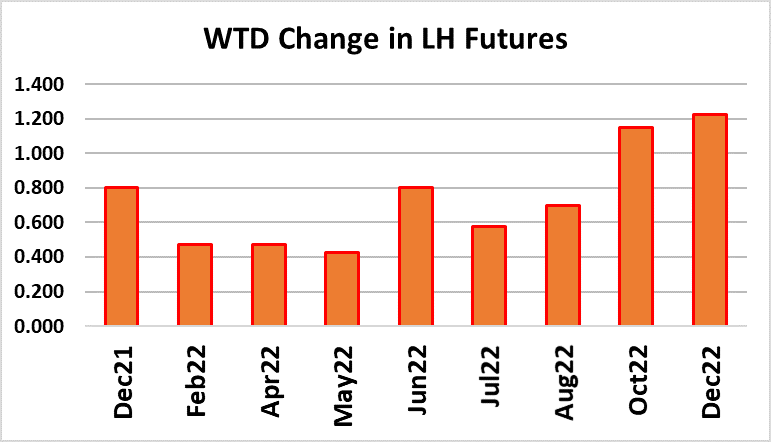

Cash hogs rallied strongly this week, with the WCB negotiated

market gaining over $9 and the NDD market up nearly $7 Fridayto-Friday. Of course this begs the question as to why packers

would be paying so much more for cash hogs at a time of year

when kills are near their peak and cutout values are struggling. I

don’t have a good answer for that other than perhaps the supply of

hogs is tightening and packers have commitments to fill. The

WCB market jumped almost $4 today and as this week’s higher

hog prices flow into the LHI, it will pressure packer margins.

This week margins averaged a little over $29/head, but that could

drop below $25/head next week. On Monday morning, I’m pretty

sure packers will be telling buyers that they need to increase

asking prices for pork because their input costs are going up.

Whether or not buyers go along with that remains to be seen.

Packers will have a lot of product to move next week given that

the kill totaled 2.67 million head. That is the largest kill this fall

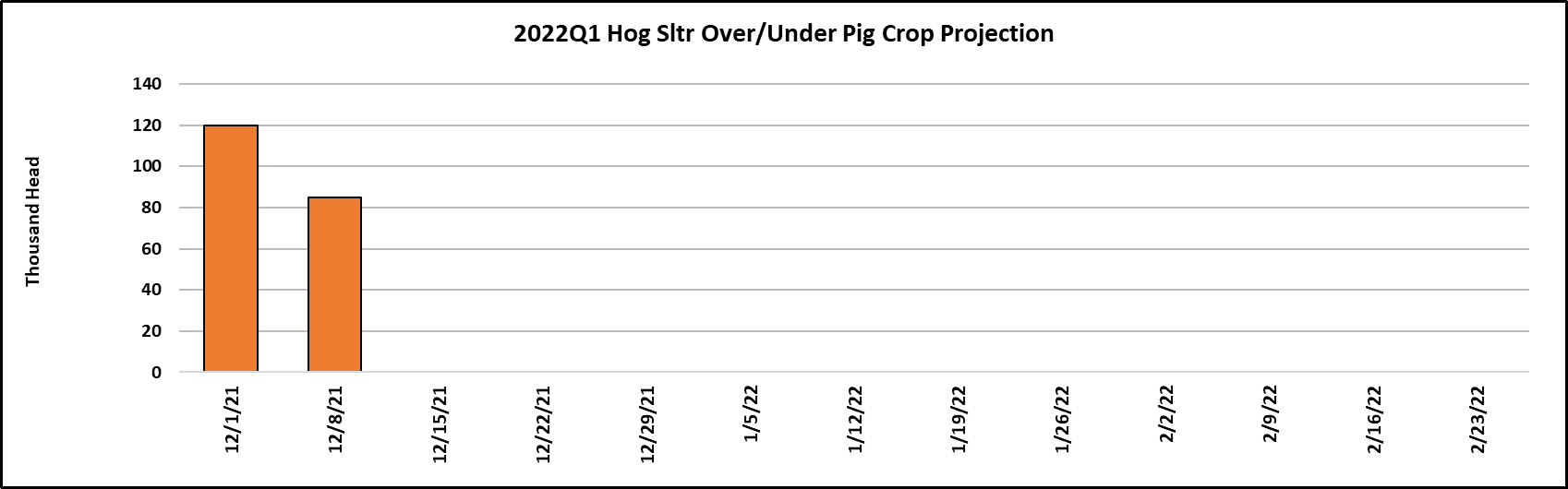

and probably marks the seasonal peak. After under-killing the pig

crop significantly during the Sep/Nov quarter, now the first two

weeks of the Dec/Feb quarter have seen a 200k over-kill. It is still

early, but we have to be thinking about the possibility that USDA

may have under-estimated the summer pig crop. However, the

fact that the negotiated hog market is moving rapidly higher

doesn’t fit well with the idea that there are more pigs than

expected out there.

FI hog weights were flat this week, but will probably increase at

least a couple more pounds before they top in late December.

The DTDS weights do not suggest that hog producers are highly

current, which makes the sharp rise in cash hog prices even more

difficult to understand. Packers are scheduled to kill 265k

tomorrow, which is about 100k less than they did last Saturday as

they were playing catch-up from the Thanksgiving holiday. This

week’s kill may be the largest of the season, but kills will stay large

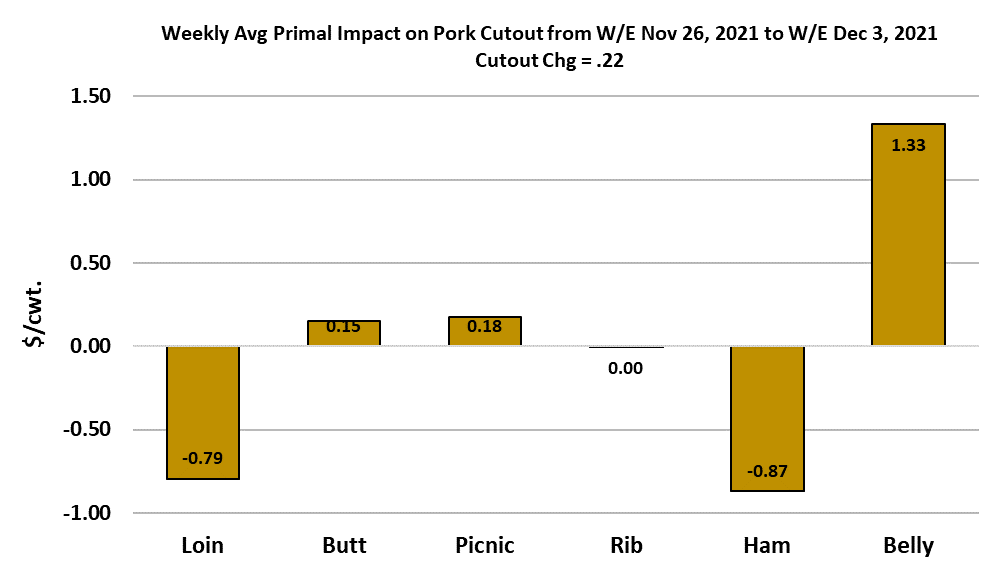

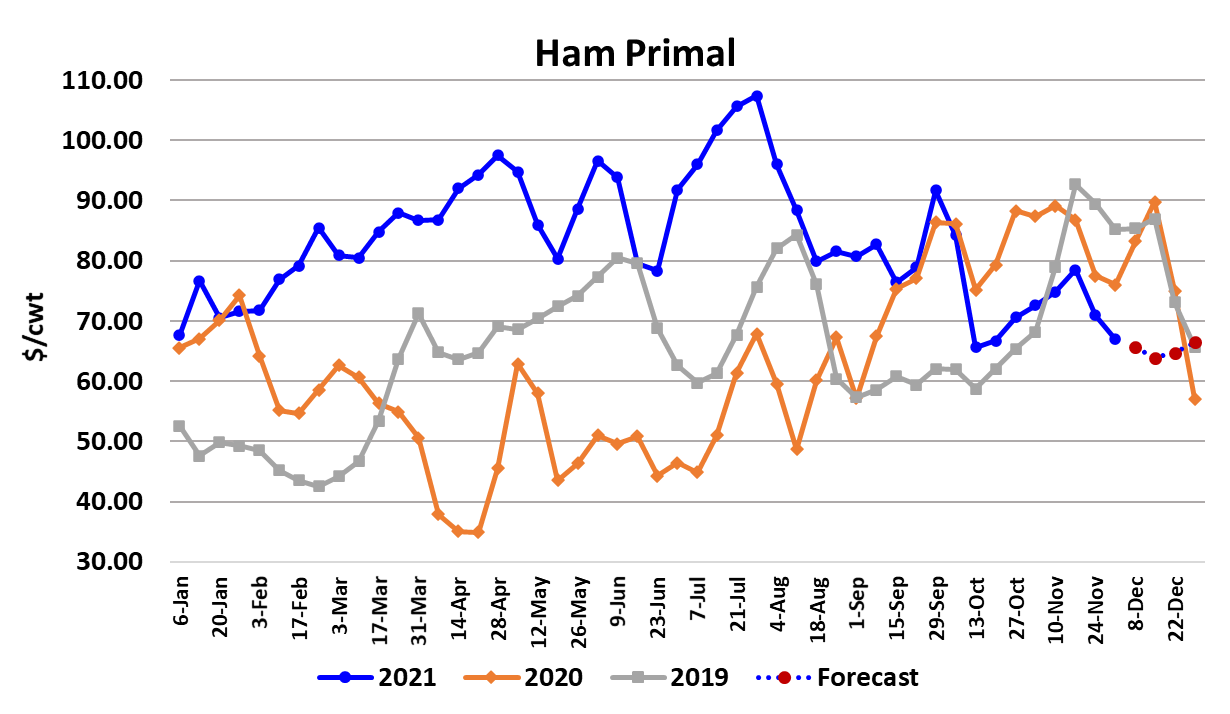

into January, excepting the holiday weeks. Bellies and hams

moved in opposite directions this week, with bellies showing some

strength and hams continuing lower. If the bellies are really

starting an new uptrend, it would be pretty unusual because they

typically weaken into the end of the year. Hams normally crash

lower during the last half of December, but they are already so low

that it is hard to imagine that this year’s December drop will match

those of years past.

So, this unusual price behavior in the processing items has left

observers scratching their head as to the likely direction of the

cutout in the next few weeks. I am among them. My

fundamental forecast basically has the gains in some areas

offsetting the losses in other areas so that the cutout holds in

the mid $80s over the next few weeks. My sense is that the risk

to that forecast is on the downside. Now, we can extend that

thought to the LHI, which has its own conundrum as negotiated

hog prices move higher while the cutout potentially moves

lower. Friday was a good example.

Negotiated hogs were quoted $4 higher and the cutout was

quoted almost $7 lower. This is confounding trader’s efforts to

forecast where the Dec futures will expire in just 7 trading days.

The cutout is only a few dollars above where it was last year at

this time, yet the weekly kills have been coming in 3-4% below

last year. The difference this year is that China has really

reduced its purchases of US pork, leaving more to be disposed

of in the domestic market. The current forecast has per capita

disappearance during Nov/Dec up about 3% from last year.

Fortunately for packers, demand is much stronger this year

than it was last year or we might be looking at a cutout in the

mid $70s instead of the mid $80s. I do get the sense that

demand is slowly fading and expect that to continue unless the

new COVID variant ends up encouraging consumers to hunker

down at home again.

That would be positive for pork demand. It will probably be

several more weeks before we can accurately assess that risk.

There is another Hogs and Pigs report on the horizon—due out

two days before Christmas. That should provide some clarity

to the supply picture. I’m expecting the breeding herd to be up

slightly YOY, but recognize that it could be down slightly as

producers eschew expansion in this time of uncertainty. Next

week, watch the bellies and hams for direction. That is likely to

be where most of the action lies. The official export data for

October will be released next week also. A 10% YOY decline

or more wouldn’t be surprising.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}